Statement of Accounts 2007/084.28MB

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

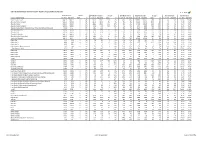

Hallett Arendt Rajar Topline Results - Wave 1 2020/Last Published Data

HALLETT ARENDT RAJAR TOPLINE RESULTS - WAVE 1 2020/LAST PUBLISHED DATA Population 15+ Change Weekly Reach 000's Change Weekly Reach % Total Hours 000's Change Average Hours Market Share STATION/GROUP Last Pub W1 2020 000's % Last Pub W1 2020 000's % Last Pub W1 2020 Last Pub W1 2020 000's % Last Pub W1 2020 Last Pub W1 2020 Bauer Radio - Total 55032 55032 0 0% 18160 17986 -174 -1% 33% 33% 155537 154249 -1288 -1% 8.6 8.6 15.9% 15.7% Absolute Radio Network 55032 55032 0 0% 4908 4716 -192 -4% 9% 9% 34837 33647 -1190 -3% 7.1 7.1 3.6% 3.4% Absolute Radio 55032 55032 0 0% 2309 2416 107 5% 4% 4% 16739 18365 1626 10% 7.3 7.6 1.7% 1.9% Absolute Radio (London) 12260 12260 0 0% 715 743 28 4% 6% 6% 5344 5586 242 5% 7.5 7.5 2.7% 2.8% Absolute Radio 60s 55032 55032 0 0% 136 119 -17 -13% *% *% 359 345 -14 -4% 2.6 2.9 *% *% Absolute Radio 70s 55032 55032 0 0% 212 230 18 8% *% *% 804 867 63 8% 3.8 3.8 0.1% 0.1% Absolute 80s 55032 55032 0 0% 1420 1459 39 3% 3% 3% 7020 7088 68 1% 4.9 4.9 0.7% 0.7% Absolute Radio 90s 55032 55032 0 0% 851 837 -14 -2% 2% 2% 3518 3593 75 2% 4.1 4.3 0.4% 0.4% Absolute Radio 00s 55032 55032 0 0% 217 186 -31 -14% *% *% 584 540 -44 -8% 2.7 2.9 0.1% 0.1% Absolute Radio Classic Rock 55032 55032 0 0% 740 813 73 10% 1% 1% 4028 4209 181 4% 5.4 5.2 0.4% 0.4% Hits Radio Brand 55032 55032 0 0% 6657 6619 -38 -1% 12% 12% 52607 52863 256 0% 7.9 8.0 5.4% 5.4% Greatest Hits Network 55032 55032 0 0% 1264 1295 31 2% 2% 2% 9347 10538 1191 13% 7.4 8.1 1.0% 1.1% Greatest Hits Radio 55032 55032 0 0% 845 892 47 6% 2% 2% 6449 7146 697 11% 7.6 8.0 0.7% -

Metro Radio Is Very Much in Touch with ‘Love of Life Round Here’

1 2 With Key 103 & Magic 1152’s weekly audience of 532,000 we can fill the Manchester Arena capacity 25 times! Source: RAJAR, Key 103 TSA. 6 Months, PE Sep 2012. Key 103 & Magic 1152 = Bauer Manchester 3 AUDIENCE POTENTIAL : 2,445,000 Male = 1,211,000 Female = 1,234,000 Source: RAJAR, Key 103 TSA. 6 Months, PE Sep 2012. 4 “Key 103 & Magic 1152 – Still Manchester’s Number One” • Key 103 and Magic 1152 retain their position as the commercial market leader in Greater Manchester with 532,000 listeners tuning into the stations each week. • Key 103’s Mike and Chelsea is Manchester’s most listened to commercial Breakfast show with 320,000 listeners tuning in each week, and OJ Borg’s Home time show continues to grow, increasing the station’s share in the afternoon to 8.9% (from 8) • In our core 25–44 demographic Key 103 remains number 1 for reach & share commercially, with a 17% higher share than Capital and 97.2% higher share for the demo than Smooth Source: RAJAR, Key 103 TSA. 6 Months, PE Sep 2012. Key 103 & Magic 1152 = Bauer Manchester 5 Combined Audience Mixed of adult contemporary music with unrivalled news and sports coverage, phone-ins and local information 61% 53% 47% 44% 39% 34% 22% Men Wome n 15 -24 25- 44 45+ ABC1 C2DE This shows a breakdown of our demographic here at Key103 & Magic 1152 to show a representation of the type of listeners we have and potential customers you could have. Breakdown by gender, age & social class in percentages respectively. -

Localness on Commercial Radio

Your response Question Your response Question 1: Do you agree that Ofcom’s duty to No. The majority of local commercial radio secure ‘localness’ on local commercial radio stations already produced very little stations could be satisfied if stations were able locally-made programming. to reduce the amount of locally-made programming they provide? If not, please Often, within the hours of locally-made explain the reasons and/or evidence which programmes, whilst the shows are produced support your view. within the region there is no effort in providing information relevant to the area. Instead there is often more effort in following the brand style (such as Heart), with any conversation relating to topics such as celebrity news/gossip. Question 2: Do you agree with our proposed No. As I work shifts, I often miss the limited amendments to the localness guidelines number of locally-made programmes, and relating to locally-made programming? If not, decreasing the number of hours of locally-made please specify any amendments you think programmes would make it harder for me to should be made instead (if any), and explain listen to locally-made programmes. the reasons and/or evidence which support your view. I would suggest a minimum 8 hours of locally-made programmes between 7am and 7pm, regardless of news provision. I would also like to see FM and AM stations using the same guidelines, considering that a large number of AM stations are now available on DAB. Question 3: Do you agree with our proposed I’m split down the middle with this one. -

Hallett Arendt Rajar Topline Results - Wave 4 2016/Last Published Data

HALLETT ARENDT RAJAR TOPLINE RESULTS - WAVE 4 2016/LAST PUBLISHED DATA Population 15+ Change Weekly Reach 000's Change Weekly Reach % Total Hours 000's Change Average Hours Market Share LOCAL COMMERCIAL Last Pub W4 2016 000's % Last Pub W4 2016 000's % Last Pub W4 2016 Last Pub W4 2016 000's % Last Pub W4 2016 Last Pub W4 2016 Bauer Radio - Total 54029 54029 0 0% 17873 17597 -276 -2% 33% 33% 156567 157032 465 0% 8.8 8.9 15.1% 15.0% Absolute Radio Network 54029 54029 0 0% 4471 4530 59 1% 8% 8% 31401 33073 1672 5% 7.0 7.3 3.0% 3.2% Absolute Radio 54029 54029 0 0% 2643 2141 -502 -19% 5% 4% 17996 15520 -2476 -14% 6.8 7.2 1.7% 1.5% Absolute Radio (London) 12015 12015 0 0% 894 750 -144 -16% 7% 6% 4707 4125 -582 -12% 5.3 5.5 2.3% 2.0% Absolute Radio (West Midlands) (was Planet Rock (West Midlands)) 3728 3727 -1 0% 242 251 9 4% 6% 7% 1573 2066 493 31% 6.5 8.2 2.3% 3.1% Absolute Radio 70s 54029 54029 0 0% 280 270 -10 -4% 1% *% 1147 1288 141 12% 4.1 4.8 0.1% 0.1% Absolute 80s 54029 54029 0 0% 1458 1529 71 5% 3% 3% 8080 8955 875 11% 5.5 5.9 0.8% 0.9% Absolute Radio 90s 54029 54029 0 0% 703 727 24 3% 1% 1% 2716 2971 255 9% 3.9 4.1 0.3% 0.3% Absolute Radio Classic Rock 54029 54029 0 0% 646 703 57 9% 1% 1% 2856 3316 460 16% 4.4 4.7 0.3% 0.3% Bauer City Network 54029 54029 0 0% 6999 6947 -52 -1% 13% 13% 60344 60303 -41 0% 8.6 8.7 5.8% 5.8% Radio Aire 639 639 0 0% 79 86 7 9% 12% 13% 470 546 76 16% 6.0 6.4 4.1% 5.1% Radio Aire 2 988 988 0 0% 62 62 0 0% 6% 6% 857 735 -122 -14% 13.9 11.9 4.6% 4.2% Radio Aire 3 639 640 1 0% 4 3 -1 -25% 1% 1% 8 9 1 13% 2.0 2.6 0.1% 0.1% Radio Borders (Bauer Borders) 109 109 0 0% 54 51 -3 -6% 50% 47% 674 709 35 5% 12.4 13.8 34.3% 35.1% C.F.M. -

QUARTERLY SUMMARY of RADIO LISTENING Survey Period Ending 18Th September 2016

QUARTERLY SUMMARY OF RADIO LISTENING Survey Period Ending 18th September 2016 PART 1 - UNITED KINGDOM (INCLUDING CHANNEL ISLANDS AND ISLE OF MAN) Adults aged 15 and over: population 54,029,000 Survey Weekly Reach Average Hours Total Hours Share in Period '000 % per head per listener '000 TSA % All Radio Q 48165 89 19.2 21.5 1037657 100.0 All BBC Radio Q 34823 64 9.9 15.3 534097 51.5 All BBC Radio 15-44 Q 14248 56 5.8 10.3 146226 36.7 All BBC Radio 45+ Q 20575 72 13.5 18.9 387871 60.7 All BBC Network Radio1 Q 32107 59 8.5 14.4 460922 44.4 BBC Local Radio Q 8429 16 1.4 8.7 73174 7.1 All Commercial Radio Q 34762 64 8.8 13.7 475608 45.8 All Commercial Radio 15-44 Q 18096 72 9.4 13.2 238287 59.8 All Commercial Radio 45+ Q 16666 58 8.3 14.2 237321 37.1 All National Commercial1 Q 19503 36 3.3 9.1 177576 17.1 All Local Commercial (National TSA) Q 26781 50 5.5 11.1 298032 28.7 Other Radio Q 3933 7 0.5 7.1 27953 2.7 Source: RAJAR/Ipsos MORI/RSMB 1 See note on back cover. For survey periods and other definitions please see back cover. Please note that the information contained within this quarterly data release has yet to be announced or otherwise made public Embargoed until 00.01 am and as such could constitute relevant information for the purposes of section 118 of FSMA and non-public price sensitive 27th October 2016 information for the purposes of the Criminal Justice Act 1993. -

“Reaching 79% of Commercial Radio's Weekly Listeners…” National Coverage

2019 GTN UK is the British division of Global Traffic Network; the leading provider of custom traffic reports to commercial radio and television stations. GTN has similar operations in Australia, Brazil and Canada. GTN is the largest Independent radio network in the UK We offer advertisers access to over 240 radio stations across the country, covering every major conurbation with a solus opportunity enabling your brand to stand out with up to 48% higher ad recall than that of a standard ad break. With both a Traffic & Travel offering, as well as an Entertainment News package, we reach over 28 million adults each week, 80% of all commercial radio’s listeners, during peak listening times only, 0530- 0000. Are your brands global? So are we. Talk to us about a global partnership. Source: Clark Chapman research 2017 RADIO “REACHING 79% OF COMMERCIAL RADIO’S WEEKLY LISTENERS…” NATIONAL COVERAGE 240 radio stations across the UK covering all major conurbations REACH & FREQUENCY Reaching 28 million adults each week, 620 ratings. That’s 79% of commercial radio’s weekly listening. HIGHER ENGAGEMENT With 48% higher ad recall this is the stand-out your brand needs, directly next to “appointment-to-listen” content. BREAKFAST, MORNING, AFTERNOON, DRIVE All advertising is positioned within key radio listening times for maximum reach. 48% HIGHER AD RECALL THAN THAT OF A STANDARD AD BREAK Source: Clark Chapman research NATIONAL/DIGITAL LONDON NORTH EAST Absolute Radio Absolute Radio Capital North East Absolute Radio 70s Kiss Classic FM (North) Absolute -

QUARTERLY SUMMARY of RADIO LISTENING Survey Period Ending 2Nd April 2017

QUARTERLY SUMMARY OF RADIO LISTENING Survey Period Ending 2nd April 2017 PART 1 - UNITED KINGDOM (INCLUDING CHANNEL ISLANDS AND ISLE OF MAN) Adults aged 15 and over: population 54,029,000 Survey Weekly Reach Average Hours Total Hours Share in Period '000 % per head per listener '000 TSA % All Radio Q 48232 89 18.9 21.2 1023354 100.0 All BBC Radio Q 34182 63 10.0 15.8 540157 52.8 All BBC Radio 15-44 Q 13803 55 5.5 10.1 139700 37.8 All BBC Radio 45+ Q 20379 71 13.9 19.7 400458 61.3 All BBC Network Radio1 Q 31405 58 8.7 15.0 471434 46.1 BBC Local Radio Q 8264 15 1.3 8.3 68723 6.7 All Commercial Radio Q 34534 64 8.4 13.2 456489 44.6 All Commercial Radio 15-44 Q 17663 70 8.7 12.4 219184 59.2 All Commercial Radio 45+ Q 16872 59 8.3 14.1 237305 36.3 All National Commercial1 Q 18709 35 3.0 8.8 163867 16.0 All Local Commercial (National TSA) Q 26662 49 5.4 11.0 292622 28.6 Other Radio Q 3747 7 0.5 7.1 26708 2.6 Source: RAJAR/Ipsos MORI/RSMB 1 See note on back cover. For survey periods and other definitions please see back cover. Please note that the information contained within this quarterly data release has yet to be announced or otherwise made public Embargoed until 00.01 am and as such could constitute relevant information for the purposes of section 118 of FSMA and non-public price sensitive 18th May 2017 information for the purposes of the Criminal Justice Act 1993. -

Independent Radio (Alphabetical Order) Frequency Finder

Independent Radio (Alphabetical order) Frequency Finder Commercial and community radio stations are listed together in alphabetical order. National, local and multi-city stations A ABSOLUTE RADIO CLASSIC ROCK are listed together as there is no longer a clear distinction Format: Classic Rock Hits Broadcaster: Bauer between them. ABBEY 104 London area, Surrey, W Kent, Herts, Luton (Mx 3) DABm 11B For maps and transmitter details see: Mixed Format Community Swansea, Neath Port Talbot and Carmarthenshire DABm 12A • Digital Multiplexes Sherborne, Dorset FM 104.7 Shropshire, Wolverhampton, Black Country b DABm 11B • FM Transmitters by Region Birmingham area, West Midlands, SE Staffs a DABm 11C • AM Transmitters by Region ABC Coventry and Warwickshire DABm 12D FM and AM transmitter details are also included in the Mixed Format Community Stoke-on-Trent, West Staffordshire, South Cheshire DABm 12D frequency-order lists. Portadown, County Down FM 100.2 South Yorkshire, North Notts, Chesterfield DABm 11C Leeds and Wakefield Districts DABm 12D Most stations broadcast 24 hours. Bradford, Calderdale and Kirklees Districts DABm 11B Stations will often put separate adverts, and sometimes news ABSOLUTE RADIO East Yorkshire and North Lincolnshire DABm 10D and information, on different DAB multiplexes or FM/AM Format: Rock Music Tees Valley and County Durham DABm 11B transmitters carrying the same programmes. These are not Broadcaster: Bauer Tyne and Wear, North Durham, Northumberland DABm 11C listed separately. England, Wales and Northern Ireland (D1 Mux) DABm 11D Greater Manchester and North East Cheshire DABm 12C Local stations owned by the same broadcaster often share Scotland (D1 Mux) DABm 12A Central and East Lancashire DABm 12A overnight, evening and weekend, programming. -

THE VOICE of UK COMMERCIAL Annual Review 2011

Annual Review 2011 THE VOICE OF UK COMMERCIAL Contents 03 CHAIRMAN’S REVIEW 04 CEO’S REVIEW RADIO 06 12 18 REVENUE DIGITAL ORGANISATION 10 14 AUDIENCE INFLUENCE RadioCentre | Annual Review 2011 01 // 2011 has been a year where radio has continued to buck the trend and confound its critics as the only traditional medium to grow revenue. // 02 RadioCentre | Annual Review 2011 Chairman’s Review Welcome to the RadioCentre Review of An industry-wide marketing campaign was When I meet with my colleagues on the 2011. The last twelve months have been an launched by the RAB under the umbrella RadioCentre board each quarter, we are impressive year for commercial radio, with theme of Britain Loves Radio, with a mindful of the importance of all these continuing record audiences and strong national advertising campaign helping to services and the need to balance both the revenue growth, especially against the deliver this message. differing priorities of different members, and recessionary backdrop for all businesses. work for a secure and prosperous future for RAB also tackled the historic challenge of a the sector. I hope that 2012 proves It has been a year where radio has lack of creativity in radio advertising, with successful for you and for everyone involved continued to buck the trend and confound an important partnership with D&AD, the in our industry. its critics, as the only traditional medium to membership organisation which represents grow revenue. And if the forecasts are to be excellence in the creative, design and believed there could be more good news in advertising communities. -

Global Radio / Real and Smooth Limited REGIONAL ANALYSIS For

SLAUGHTER AND MAY Global Radio / Real and Smooth Limited REGIONAL ANALYSIS For each of the 7 SLC regions identified by the CC, Global has assessed the scale of the SLC and the customer benefits which will be lost through a divestment of any of the parties’ core stations (i.e. Smooth, Real, Capital and Heart). Global has quantified both the maximum likely scale of the SLC in each region and the customer benefit likely to be lost through divestment of core stations (to the extent this can be quantified). As a result of this analysis, Global has evidenced that any divestment of a core station would not be proportionate or reasonably justified in any of the 7 SLC areas. We comment on each of the 7 SLC areas in turn. Error! Unknown document property name. 2 1. EAST MIDLANDS Executive Summary 1.1 The scale of the SLC in the East Midlands is trivial. Based on the CC’s Provisional Findings, the revenues affected by the merger in the East Midlands are £[]. 1.2 While not accepting that any SLC found by the CC would lead to an increase in price, Global considers that any such increase would be small (not greater than 5%) given that the parties are not close competitors in the East Midlands and that Orion is a much closer competitor to both Capital and Smooth than they are to each other. A 5% price increase on the affected revenues in the East Midlands would imply the harm from the SLC is £[]. 1.3 Any harm from the SLC is substantially outweighed by the advertiser discounts that will be lost as a result of the divestment of Smooth East Midlands (£[]) which comprise: (i) Lost network discounts of £[]for contracted advertisers; and (ii) Lost single-region multi-brand discounts of £[] for non-contracted advertisers. -

QUARTERLY SUMMARY of RADIO LISTENING Survey Period Ending 14Th September 2014

QUARTERLY SUMMARY OF RADIO LISTENING Survey Period Ending 14th September 2014 PART 1 - UNITED KINGDOM (INCLUDING CHANNEL ISLANDS AND ISLE OF MAN) Adults aged 15 and over: population 53,502,000 Survey Weekly Reach Average Hours Total Hours Share in Period '000 % per head per listener '000 TSA % All Radio Q 47614 89 19.0 21.4 1019059 100.0 All BBC Radio Q 34845 65 10.2 15.7 545934 53.6 All BBC Radio 15-44 Q 15116 59 6.5 11.1 167165 41.7 All BBC Radio 45+ Q 19729 71 13.6 19.2 378769 61.3 All BBC Network Radio1 Q 31686 59 8.7 14.7 466020 45.7 BBC Local Radio Q 8945 17 1.5 8.9 79914 7.8 All Commercial Radio Q 34045 64 8.3 13.1 445056 43.7 All Commercial Radio 15-44 Q 17922 70 8.6 12.2 219118 54.7 All Commercial Radio 45+ Q 16124 58 8.1 14.0 225938 36.5 All National Commercial1 Q 16954 32 2.6 8.2 138195 13.6 All Local Commercial (National TSA) Q 27213 51 5.7 11.3 306861 30.1 Other Radio Q 3870 7 0.5 7.3 28069 2.8 Source: RAJAR/Ipsos MORI/RSMB 1 See note on back cover. For survey periods and other definitions please see back cover. Embargoed until 00.01 am Enquiries to: RAJAR, 6th floor, 55 New Oxford St, London WC1A 1BS 23rd October 2014 Telephone: 020 7395 0630 Facsimile: 020 7395 0631 e mail: [email protected] Internet: www.rajar.co.uk ©Rajar 2014. -

Media Kit Q4 2020

2021 GTN UK is the British division of Global Traffic Network; the leading provider of custom traffic reports to commercial radio and television stations. GTN has similar operations in Australia, Brazil and Canada. GTN is the largest Independent radio network in the UK We offer advertisers access to over 250 radio stations across the country, covering every major conurbation with a solus opportunity enabling your brand to stand out with up to 48% higher ad recall than that of a standard ad break. With both a Traffic & Travel offering, as well as an Entertainment News package, we reach over 28.6 million adults each week, 80% of all commercial radio’s listeners, during peak listening times only, 0530-0000. Are your brands global? So are we. Talk to us about a global partnership. Source: RAJAR Q4 2020/ Clark Chapman research RADIO “REACHING 73% OF COMMERCIAL RADIO’S WEEKLY LISTENERS…” NATIONAL COVERAGE 230 radio stations across the UK covering all major conurbations REACH & FREQUENCY Reaching over 28 million adults each week, 622 ratings. That’s 73% of commercial radio’s weekly listening. HIGHER ENGAGEMENT With 48% higher ad recall this is the stand-out your brand needs, directly next to “appointment-to-listen” content. BREAKFAST, MORNING, AFTERNOON, DRIVE All advertising is positioned within key radio listening times for maximum reach. 48% HIGHER AD RECALL THAN THAT OF A STANDARD AD BREAK Source: Clark Chapman research Source: RAJAR Q4 2020 NATIONAL/DIGITAL Absolute Radio Absolute Radio 70s (NR) Absolute 80s Absolute Radio 90s Absolute Radio