March 2017 Selector High Conviction Equity Fund Quarterly Newsletter #55

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sigma Emerging Companies Strategy

Sigma Emerging Companies Strategy Quarterly update as at 30 June 2017 Since Quarter FYTD 1 year 3 years 5 years Inception^ % % % % p.a. % p.a. % p.a. Sigma Emerging Companies Strategy* (1.3) 20.9 20.9 5.7 8.5 6.5 S&P/ASX Small Ord. Acc. Index (0.3) 7.0 7.0 7.1 5.7 1.7 Value added (detracted) (1.0) 13.9 13.9 (1.4) 2.8 4.8 *Gross Performance. Past performance is not a reliable indicator of future performance. ^Since Inception: 1 January 2010 Key points • Small Cap “value opportunity” clearly evident as traditional metrics remain compelling • Cyclical sectors expected to benefit as earnings bottom and risk appetite increases • Fund positioned for cyclical re-rating and away from lower return defensives Individual stock performance of note • The absence of Mayne Pharmaceuticals (-24%), Sigma The Sigma Emerging Companies Strategy (Strategy) Pharmaceuticals (32%) and Myer (-31%) contributed to underperformed a falling small cap market in the June quarter. performance in a relative sense. Stock selection was important, and generally speaking over Strategy performance was driven negatively by: the last 6 months we have seen the performance tilt away from the value recovery we saw during the first half of the financial • Infigen (-25%), lower following an earnings downgrade due year. A recovery in high PE stocks and the move towards to poor wind conditions in the final quarter which impacted more defensive positioning has proven to be a drag on the power generation. We view this as a one-off event and portfolio. -

Realindex Australian Share Fund

Realindex Australian Share Fund Fact sheet - 31 Aug 2015 Fund strategy Fund facts The Realindex Australian Share Fund uses the RAFI® methodology in the Benchmark S&P / ASX 200 Accumulation Index construction of its portfolios which selects and weights companies Funds under management $2800.1 million according to their economic footprint defined by fundamental measures of Inception Date 17 November 2008 company size (sales, cash flow, book value and dividends). The portfolio is further enhanced by applying additional factors such as quality of earnings and debt coverage. Commentary The Realindex Australian Shares Fund returned -7.39% (gross of fees) during August 2015 outperforming the S&P/ASX 200 Accumulation Index which returned -7.79% (its worst monthly performance since October 2008). Value (-7.3%) slightly outperformed Growth (-8.0%) during the month, extending the longer-term outperformance trend (-2.4% vs. -6.1%, 12 months to 31 August 2015). This outcome is typically favourable for portfolio performance, given the Value tilt inherent in the Fundamental Indexation methodology. The Materials sector (-5.2%) was the top contributor to relative performance during the month, driven by overweight holdings in steel companies Sims Metal Management (+21.4%) and BlueScope Steel (+18.7%). Sims reported a better-than-expected FY15 result, while BlueScope committed to $200m cost out by FY17, which was well received by investors. An overweight holding in Spark New Zealand (+13.0%) led the portfolio’s outperformance in the Telecommunications sector (-8.3%). Spark rallied after announcing positive earnings growth and an annual dividend increase at its FY15 results. Spark was the top contributor to relative performance across the portfolio at a company level. -

ASD NTA & Allotment Notice

Friday, 8 March 2019 ASD NTA & Allotment Notice Smartshares Limited would like to report details of the Units on Issue for the Australian Dividend Fund (ASD) as at 7 March 2019. Units on Issue: 15,304,541 Units Allotted/(Redeemed): - Net Tangible Assets (NTA): $1.61250 Tracking Difference: 1.04% The objective of the Australian Dividend Fund (ASD) is to provide a return that closely matches the return on the S&P/ASX Dividend Opportunities Index. The S&P/ASX Dividend Opportunities Index comprises the 50 highest yielding common stocks from the Australian equity market. The following companies are currently held in the Fund: Code Security description ABC Adelaide Brighton Ltd. APA APA Group API Australian Pharmaceutical Industries Ltd. ASL Ausdrill Ltd. AST AusNet Services Ltd. ASX ASX Ltd. AWC Alumina Ltd. BEN Bendigo and Adelaide Bank Ltd. CBA Commonwealth Bank of Australia CCL Coca-Cola Amatil Ltd. CTX Caltex Australia Ltd. CWN Crown Resorts Ltd. DLX DuluxGroup Ltd. DOW Downer EDI Ltd. ECX Eclipx Group Ltd. FMG Fortescue Metals Group Ltd. GUD G.U.D. Holdings Ltd. GWA GWA Group Ltd. HVN Harvey Norman Holdings Ltd. IAG Insurance Australia Group Ltd. ILU Iluka Resources Ltd. ING Inghams Group Ltd. IPH IPH Ltd. JBH JB Hi-Fi Ltd. LLC Lendlease Group MFG Magellan Financial Group Ltd. MIN Mineral Resources Ltd. MMS McMillan Shakespeare Ltd. MQG Macquarie Group Ltd. MTS Metcash Ltd. NEC Nine Entertainment Co. Holdings Ltd. NHC New Hope Corporation Ltd. PDL Pendal Group Ltd. PMV Premier Investments Ltd. RIO Rio Tinto Ltd. www.smartshares.com RRL Regis Resources Ltd. -

Annual Report 2018 Sustainability Report 2018

SUSTAINABILITY REPORTANNUAL REPORT 2018 SIMS METAL MANAGEMENT LIMITED SUSTAINABILITY REPORT 2018 ABOUT THIS REPORT Stewards of our world’s limited resources... ABOUT SIMS METAL MANAGEMENT ALIGNING TO INVESTOR INTEREST We at Sims Metal Management are proud Over the past year, our investors of our role as stewards of our world’s have increasingly asked about Sims’ Recycling for posture and performance in the areas >100 years limited resources for over 100 years. As a global leader of metals and electronics of environmental, social and corporate recycling we play an intrinsic role in the governance (ESG). As the graphic below circular economy, by keeping resources in illustrates, Sims is very much aligned with use as long as possible, extracting the the circular economy – where materials maximum value from those resources remain in useful life for as long as possible. >250 facilities We discuss this in detail later in this report. including JVs while in use, and then recovering and regenerating products and materials at In June 2017, the G20 Financial Stability the end of their useful life. Our efforts Board’s Task Force on Climate-Related contribute to the sustainable future of Financial Disclosures (TCFD) released its our world. final recommendations on the disclosure Operations in Our core businesses are: of the risks and opportunities as we 18 countries transition into a lower carbon economy. • Metals Recycling - As the world’s We have organized this report around leading publicly listed metals recycler, the four main categories of the TCFD Sims buys and sells ferrous and recommendations. (Governance, Strategy, non-ferrous recycled metals. -

SIMS GROUP LIMITED Annual REPORT 2008 SIM S G R O U P L IM IT E D a N N U a L RE P O R T 2 0

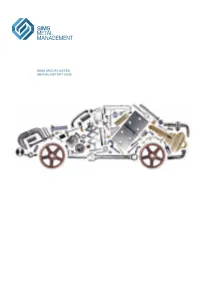

SIMS GROUP LIMITED GROUP SIMS ANN U a L REPORT2008 L ThE average motor vEhIcle SIMS GROUP LIMITED Lasts 13.5 yEars anD comprises annUaL report 2008 approximately 15,000 IndividuaL Parts, Of whIch 80% are potentially recOverable. Approximately 68% Of a vEhIcle’S Parts by weighT aRE steel, followed by plastic (9%) anD nOn ferrous metals (8%), with ThE remaInder rubber, glass anD other materials. www.simsMM.cOM finanCiaL Summary Corporate DireCtory For the year ended 30 June 2008 SeCuritieS exChange LiSting Shareholder enquirieS The Company’s ordinary shares are quoted Enquiries from investors regarding their $7.67 b 38% $433m 81% 306¢ 60% 130¢ 8% on the Australian Securities Exchange under share holdings should be directed to: the ASX Code ‘SGM’. Computershare Investor Services Pty Limited TotaL REvEnue Profit after Tax EaRnIngs per ShaRE DIvidends per Share The Company’s American Depositary Shares Level 3 (ADSs) are quoted on the New York Stock 60 Carrington Street Exchange under the symbol ‘SMS’. The Company Sydney NSW 2000 has a Level II ADS program, and the Depositary Postal Address: is the Bank of New York Mellon Corporation. GPO Box 7045 ADSs trade under cusip number 829160100 Sydney NSW 2001 with each ADS representing one (1) ordinary Telephone: 1300 855 080 share. Further information and investor Facsimile: (02) 8235 8150 enquiries on ADSs may be directed to: Company SeCretarieS $181m 42% 14.6% 22% 10.9% 43% $8.02 72% The Bank of New York Mellon Corporation Frank Moratti Depositary Receipts Division Scott Miller Net caSh flowS Return -

Weekly Ratings, Targets, Forecast Changes

Weekly Ratings, Targets, Forecast Changes Sep 03, 2018 By Rudi Filapek-Vandyck, Editor FNArena Guide: The FNArena database tabulates the views of eight major Australian and international stock brokers: Citi, Credit Suisse, Deutsche Bank, Macquarie, Morgan Stanley, Morgans, Ord Minnett and UBS. For the purpose of broker rating correlation, Outperform and Overweight ratings are grouped as Buy, Neutral is grouped with Hold and Underperform and Underweight are grouped as Sell to provide a Buy/Hold/Sell (B/H/S) ratio. Ratings, consensus target price and forecast earnings tables are published at the bottom of this report. Summary Period: Monday August 27 to Friday August 31, 2018 Total Upgrades: 16 Total Downgrades: 24 Net Ratings Breakdown: Buy 40.93%; Hold 43.41%; Sell 15.67% Securities analysts in Australia are still issuing more recommendation downgrades than upgrades, but at least the gap between the two is narrowing noticeably. In contrast to prior weeks, both tables for the week ending Friday, 31st August 2018, are populated by stocks receiving multiple switches in stockbroker ratings. FNArena counted 16 upgrades and 24 downgrades pulling the ratio for the four weeks of August just below 1:2. Receiving multiple upgrades were ambitious gold miner Northern Star Resources (2x) and Regis Resources (gold and nickel) and Sims Metal Management (scrap) with the latter two enjoying three upgrades post results releases. Only six of the 16 upgrades involves a Buy rating. On the flipside,FNArena nutritional supplements provider Blackmores was downgraded three times during the week, of which two downgrades moved to Sell, while fruit and veggies grower Costa Group was downgraded twice, both to Neutral/Hold; troubled contractor RCR Tomlinson was also downgraded twice (one Sell only), while fresh Sell ratings fell upon the likes of Bega Cheese, WiseTech Global, Qube Holdings, Virgin Australia and Reliance Worldwide. -

For Personal Use Only

29 October 2019 ASX Limited ASX Market Announcements Office Exchange Centre Level 6, 20 Bridge Street SYDNEY NSW 2000 EINVEST FUTURE IMPACT SMALL CAPS FUND (MANAGED FUND) (ASX: IMPQ) Monthly portfolio disclosure notification 31 August 2019 We advise that the portfolio for the Fund as at 31 August 2019 comprised the following securities: Stock Name Ticker % total portfolio ALS LTD ALQ 2.64% AUB GROUP LTD AUB 2.31% BENDIGO AND ADELAIDE BANK BEN 2.94% BLACKMORES LTD BKL 1.86% BRAVURA SOLUTIONS LTD BVS 1.75% CALIX LIMITED CXL 1.63% CASH Cash 6.84% CHARTER HALL EDUCATION TRUST CQE 2.89% CITY CHIC COLLECTIVE LTD CCX 3.45% CLEANAWAY WASTE MANAGEMENT L CWY 2.13% FISHER & PAYKEL HEALTHCARE FPH 2.83% G8 EDUCATION LTD GEM 2.75% GENEX POWER LTD GNX 1.59% HEALIUS LTD HLS 2.96% HRL HOLDING HRL 1.87% IMRICOR MEDICAL SYSTEMS-CDI IMR 3.18% INFIGEN ENERGY IFN 2.69% INGENIA COMMUNITIES GROUP INA 3.20% INTEGRAL DIAGNOSTICS LTD IDX 4.75% INVOCARE LTD IVC 1.41% IRESS LTD IRE 2.52% JANUS HENDERSON GROUP-CDI JHG 1.61% For personal use only KATHMANDU HOLDINGS LTD KMD 2.84% LINK ADMINISTRATION HOLDINGS LNK 1.13% MERCURY NZ LIMITED MCY 4.44% MERIDIAN ENERGY LTD MEZ 3.99% NETWEALTH GROUP LTD NWL 1.97% Perennial Investment Management Limited. ABN 13 108 747 637 AFS Licence No. 275101 www.perennial.net.au Level 27, 88 Phillip Street, Sydney NSW 2000, Australia. Tel: 1300 730 032 (from overseas +612 8274 2777) Email: [email protected] NEXT SCIENCE NXS 0.22% NIB HOLDINGS LTD NHF 3.24% OOH!MEDIA LTD OML 1.69% ORORA LTD ORA 1.86% PENDAL GROUP LTD PDL 1.66% PHOSLOCK ENVIRONMENTAL TECHN PET 1.25% POLYNOVO LTD PNV 1.38% RESMED INC-CDI RMD 2.23% SIMS METAL MANAGEMENT LTD SGM 4.62% SPARK NEW ZEALAND LTD SPK 2.73% SYNLAIT MILK LTD SM1 2.34% TELIX PHARMACEUTICALS LTD TLX 1.33% VISTA GROUP INT LTD VGL 1.30% Yours sincerely, Bill Anastasopoulos Company Secretary Perennial Investment Management Limited as Responsible Entity for eInvest Future Impact Small Caps Fund (Managed Fund). -

Quarterly Commentary 30 June 2017

QUARTERLY COMMENTARY 30 JUNE 2017 1 of 15 Q2 2017 COMMENTARY It is often difficult to pinpoint exactly why certain sectors of a sharemarket become cheap relative to others. Even harder is pinning down the catalyst that will bring the valuation pendulum back into a more sustainable position. Hardest of all though is getting the timing right - the point in the cycle when this catalyst will actually take effect. We tend not to obsess about the catalyst or the timing. Instead, we look for the pendulums that are at or near an extreme; those companies or sectors which we think are likely to reward investors handsomely when the pendulum rights itself. SIMON MAWHINNEY, CFA Relative to large companies, Australia’s small capitalisation Managing Director & Chief Investment Officer shares are nearing extreme valuations. Graph 1 illustrates this and plots the performance of the S&P/ASX Small Ordinaries Accumulation Index relative to the S&P/ASX 100 Accumulation Index (the largest 100 companies). Graph 1: Performance of small companies relative to large companies in Australia 1.00 0.90 0.80 0.70 0.60 0.50 Small Companies Relative to Large Companies Large to Relative Companies Small 0.40 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 Source: Iress, S&P/ASX Small Ordinaries Accumulation Index relative to the S&P/ASX 100 Accumulation Index 2 of 15 Q2 2017 Despite the small end of town having rebounded a little from its the pendulum’s shift is determining whether it is permanent or early-2015 lows, it has significantly underperformed over the whether it will return to its swing path. -

Longwave Capital Partners Invests with a Philosophy Informed by the Belief That for Small Caps, Quality Is a Key Driver of Long-Term Investment Outperformance

// Longwave Capital Partners invests with a philosophy informed by the belief that for small caps, quality is a key driver of long-term investment outperformance. When we assess companies considering Environmental, Social and Governance (ESG) characteristics, we see them as markers of quality. // Historically, we have considered ESG as a component in the The first stage uses systematic fundamental assessments to fundamental assessment that determines the quality of a identify companies that exhibit characteristics which have business – factored into the quality score that we use to drive historically been high probability markers of failure or our valuation. This is calculated by applying a discount rate to underperformance. These are low-quality companies we look to our sustainable, mid-cycle earnings estimate in forecast year ensure are not present in our portfolio. Based upon our current five. We believe the equity risk premium required of higher- criteria across the different models we employ, around 85% of quality companies is lower than average companies, and lower- the small caps we assess have a reasonable probability of failure quality companies require a higher equity risk premium than or long-term underperformance. We construct a systematic average. portfolio of the remaining 15%, built from the ensemble of our While cognisant of the impact ESG factors have on the quality of different quality models. a business (and thereby its value), our previous approach did not It would appear at first glance that using available ESG data and have the same objective level of data capture or comparability testing for performance would be an appropriate measure to as the investment process that we now employ, driven by enhance our existing systematic process. -

TOP KEY BOARD and EXECUTIVE MOVEMENTS in AUSTRALIA 4Th – 8Th DECEMBER 2017

TOP KEY BOARD AND EXECUTIVE MOVEMENTS IN AUSTRALIA 4th – 8th DECEMBER 2017 Actinogen Medical Ltd: George Morstyn has been appointed as a Non-Executive Accent Group Ltd: Brett Blundy has been appointed as a Non-Executive Director. AMP Ltd: Jenny Fagg has been appointed as Chief Risk Officer, effective 9 February 2017. Australia and New Zealand Banking Group Ltd: Chief Risk Officer, Nigel Williams, will retire at the end of March 2018. Brisbane Broncos Ltd: Dennis Watt has resigned as Chairman and the role will be taken over by Karl Morris. Cape Lambert Resources Ltd: Stefan Müller has been appointed as a Non-Executive Director taking effect on 1 January 2018. Centuria Capital Ltd: Evelyn Horton has been appointed to the Board as a Non- Executive Director and Roger Dobson will be stepping down as a Non-Executive Director, effective 1 December 2017. Challenger Ltd: Melanie Willis and John Green have been appointed as Non- Executive Directors, effective 6 December 2017. Chorus Ltd: Joanna Crawford has been permanently confirmed as General Manager, Customer Care. Vanessa Oakley has been appointed as General Manager, Strategy and Business Operations commencing in March 2018 and Scott Newton has resigned from Chorus. Coca-Cola Amatil Ltd: Peter West has been appointed as Managing Director of the company’s Australian Beverages’ Business. DuluxGroup Ltd: Garry Hounsell has resigned as a Non-Executive Director, effective 31 December 2017. GetSwift Ltd: Nevash Pillay has been appointed as a Non-Executive Director. Lovisa Holdings Ltd: Interim Chief Financial Officer, Matt Lauder, has been appointed Chief Financial Officer and Company Secretary on a permanent basis. -

FTSE Publications

2 FTSE Russell Publications FTSE Developed Asia Pacific ex 19 August 2021 Japan ex Controversies ex CW Index Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) a2 Milk 0.1 NEW CJ Cheiljedang 0.1 KOREA GPT Group 0.22 AUSTRALIA ZEALAND CJ CheilJedang Pfd. 0.01 KOREA Green Cross 0.05 KOREA AAC Technologies Holdings 0.16 HONG KONG CJ Corp 0.04 KOREA GS Engineering & Construction 0.07 KOREA ADBRI 0.04 AUSTRALIA CJ ENM 0.05 KOREA GS Holdings 0.06 KOREA Afterpay Touch Group 0.61 AUSTRALIA CJ Logistics 0.04 KOREA GS Retail 0.04 KOREA AGL Energy 0.12 AUSTRALIA CK Asset Holdings 0.5 HONG KONG Guotai Junan International Holdings 0.01 HONG KONG AIA Group Ltd. 4.6 HONG KONG CK Hutchison Holdings 0.64 HONG KONG Haitong International Securities Group 0.02 HONG KONG Air New Zealand 0.02 NEW CK Infrastructure Holdings 0.11 HONG KONG Hana Financial Group 0.36 KOREA ZEALAND Cleanaway Waste Management 0.08 AUSTRALIA Hang Lung Group 0.07 HONG KONG ALS 0.14 AUSTRALIA CLP Holdings 0.5 HONG KONG Hang Lung Properties 0.15 HONG KONG Alteogen 0.06 KOREA Cochlear 0.37 AUSTRALIA Hang Seng Bank 0.44 HONG KONG Altium 0.09 AUSTRALIA Coles Group 0.5 AUSTRALIA Hanjin KAL 0.04 KOREA Alumina 0.1 AUSTRALIA ComfortDelGro 0.08 SINGAPORE Hankook Technology Group 0.1 KOREA Amcor CDI 0.54 AUSTRALIA Commonwealth Bank of Australia 4.07 AUSTRALIA Hanmi Pharmaceutical 0.06 KOREA AmoreG 0.05 KOREA Computershare 0.21 AUSTRALIA Hanmi Science 0.03 KOREA Amorepacific Corp 0.21 KOREA Contact Energy 0.14 NEW Hanon Systems 0.07 KOREA Amorepacific Pfd. -

STOXX Pacific 100 Last Updated: 01.08.2017

STOXX Pacific 100 Last Updated: 01.08.2017 Rank Rank (PREVIOU ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) S) AU000000CBA7 6215035 CBA.AX 621503 Commonwealth Bank of Australia AU AUD Y 98.1 1 1 AU000000WBC1 6076146 WBC.AX 607614 Westpac Banking Corp. AU AUD Y 72.3 2 2 AU000000ANZ3 6065586 ANZ.AX 606558 Australia & New Zealand Bankin AU AUD Y 58.9 3 3 AU000000BHP4 6144690 BHP.AX 614469 BHP Billiton Ltd. AU AUD Y 56.2 4 5 AU000000NAB4 6624608 NAB.AX 662460 National Australia Bank Ltd. AU AUD Y 54.3 5 4 AU000000CSL8 6185495 CSL.AX 618549 CSL Ltd. AU AUD Y 38.8 6 6 AU000000TLS2 6087289 TLS.AX 608545 Telstra Corp. Ltd. AU AUD Y 33.0 7 7 AU000000WES1 6948836 WES.AX 694883 Wesfarmers Ltd. AU AUD Y 31.3 8 8 AU000000WOW2 6981239 WOW.AX 698123 Woolworths Ltd. AU AUD Y 23.4 9 9 AU000000RIO1 6220103 RIO.AX 622010 Rio Tinto Ltd. AU AUD Y 18.9 10 11 AU000000MQG1 B28YTC2 MQG.AX 655135 Macquarie Group Ltd. AU AUD Y 18.6 11 10 AU000000TCL6 6200882 TCL.AX 689933 Transurban Group AU AUD Y 15.9 12 12 AU000000SCG8 BLZH0Z7 SCG.AX AU01Z4 SCENTRE GROUP AU AUD Y 14.9 13 14 AU000000WPL2 6979728 WPL.AX 697972 Woodside Petroleum Ltd. AU AUD Y 14.4 14 13 AU000000SUN6 6585084 SUN.AX 658508 SUNCORP GROUP LTD. AU AUD Y 12.5 15 15 AU000000AMC4 6066608 AMC.AX 606660 Amcor Ltd. AU AUD Y 12.0 16 16 AU000000QBE9 6715740 QBE.AX 671574 QBE Insurance Group Ltd.