Australia & New Zealand Report 2018

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Code Security Description AAD ARDENT LEISURE GROUP ABC ADELAIDE BRIGHTON AGL AGL ENERGY LTD AHG AUTOMOTIVE HOLDINGS G AMP AMP LI

15-Jun-16 Australian Dividend Index Trust NTA & Allotment Notice The manager of the Australian Dividend Index Trust advises that as at close of business on 14 June 2016 a total of Nil units has been redeemed or allotted since 13 June 2016. The total number of units on issue on that day was 39,290,493. The asset backing for each ASD unit at close of business (Sydney) on 14 June 2016 was $1.49373 (NTA is net of applicable tax liability). The tracking difference was 2.35% Please note Basket applications and redemptions will be unavailable from Wednesday 15 June to Wednesday 29 June. Basket applications and redemptions will resume on Thursday 30 June. The following companies are currently in the Fund: Code Security description AAD ARDENT LEISURE GROUP ABC ADELAIDE BRIGHTON AGL AGL ENERGY LTD AHG AUTOMOTIVE HOLDINGS G AMP AMP LIMITED ANZ AUSTRALIA AND NEW ZEA APA APA GROUP AST AUSNET SERVICES ASX ASX LIMITED BEN BENDIGO AND ADELAIDE BOQ BANK OF QUEENSLAND CBA COMMONWEALTH BANK OF CGF CHALLENGER LIMITED CIM CIMIC GROUP LIMITED O CSR CSR LIMITED DOW DOWNER EDI LIMITED DUE DUET GROUP FLT FLIGHT CENTRE TRAVEL FXJ FAIRFAX MEDIA LTD FXL FLEXIGROUP LIMITED GEM G8 EDUCATION ORD GMA GENWORTH MORTGAGE INS HVN HARVEY NORMAN HOLDING IAG INSURANCE AUSTRALIA G IFL IOOF HOLDINGS LTD JBH JB HI-FI LIMITED LLC LENDLEASE CORPORATION MMS MCMILLAN SHAKESPEARE MQG MACQUARIE GROUP LTD NAB NATIONAL AUSTRALIA BA NVT NAVITAS LIMITED ORI ORICA LIMITED PPT PERPETUAL TRUSTEES AU PTM PLATINUM ASSET MANAGE RFG RETAIL FOOD GROUP RIO RIO TINTO LIMITED SHL SONIC HEALTHCARE LTD SKI SPARK INFRASTRUCTURE SPK SPARK NEW ZEALAND LIM SPO SPOTLESS GROUP HOLDIN SUL SUPER RETAIL GROUP LI SUN SUNCORP GROUP LTD SVW SEVEN GROUP HOLDINGS SYD SYDNEY AIRPORT UNITS TCL TRANSURBAN GROUP (ORD TLS TELSTRA CORPORATION L WBC WESTPAC BANKING CORP WES WESFARMERS LIMITED WOW WOOLWORTHS LIMITED WPL WOODSIDE PETROLEUM LT For further information please contact: Smartshares Limited 0800 80 87 80 [email protected]. -

The State of the Deal and Deloitte Queensland Index

The State of the Deal and Deloitte Queensland Index March 2021 – Queensland Index Exceeds $100 billion THE STATE OF THE DEAL | March 2021 – Queensland Index Exceeds $100 billion Contents Executive Summary 1 Then & Now – Investment Landscape 3 Then & Now – Deloitte Queensland Index 4 Queensland Economic Update 7 The Deloitte Queensland Index Q1 2021 8 Contacts 11 Sources 12 ii THE STATE OF THE DEAL | March 2021 – Queensland Index Exceeds $100 billion Executive Summary Following the significant rebound in the second half of 2020, companies in the Deloitte Queensland Index exceeded $100 billion at 31 March 2021, the highest month end market capitalisation on record for the State. Deloitte Queensland Index S&P/ASX All Ordinaries Companies in the Deloitte return in Q1 2021 return in Q1 2021 Queensland Index 3.5% 2.4% 169 at 31 March 2021 10.6% in Q4 2020 14.0% in Q4 2020 173 at 31 December 2020 90 companies increased Market capitalisation as at Mar-21 market capitalisation (53%) 66 companies decreased market $101.6b capitalisation (39%) 12 no movement (7%) $97.2b as at Dec-20 $18.5b as at Sep-02 5 delistings 1 listing (1%) Announced QLD M&A Disclosed value of announced transactions in Q1 2021 QLD M&A transactions in Q1 2021 64 $1.9b 92 in Q4 2020 $3.3b in Q4 2020 1 THE STATE OF THE DEAL | March 2021 – Queensland Index Exceeds $100 billion The Deloitte Queensland Index increased by 3.5% in Q1 2021 Queensland M&A more broadly remains strong with with total market capitalisation increasing to $101.6b at 64 transactions announced in Q1 2021 including: Mar-21, the highest month end value on record for the State. -

Annual Report 2014 Contents

#LOVEBOQ ANNUAL REPORT 2014 CONTENTS DIRECTORS’ REPORT 2 DIRECTORS’ DETAILS 2 OPERATING AND FINANCIAL REVIEW 5 PERFORMANCE REMUNERATION REPORT 12 INTRODUCTORY MESSAGE 12 REMUNERATION REPORT 12 LEAD AUDITOR’S INDEPENDENCE DECLARATION 36 CORPORATE GOVERNANCE 37 SNAPSHOT FINANCIAL REPORT 47 INCOME STATEMENTS 47 STATEMENTS OF COMPREHENSIVE INCOME 48 BALANCE SHEETS 49 STATEMENTS OF CHANGES IN EQUITY 50 STATEMENTS OF CASH FLOWS 54 NOTES TO THE FINANCIAL STATEMENTS 55 OTHER INFORMATION 113 DIRECTORS’ DECLARATION 113 INDEPENDENT AUDITOR’S REPORT TO THE MEMBERS 114 SHAREHOLDING DETAILS 116 SHAREHOLDER INFORMATION 119 PERFORMANCE SNAPSHOT STATUTORY NETafter PROFITtax EARNINGS PER SHARE cash basic up up 5m to . to $260 89.5c CASH EARNINGS after tax DIVIDEND PERfull SHAREyear ordinary up up to $301.2m to 66c 1 Bank of Queensland Limited and its Controlled Entities A.B.N. 32 009 656 740. DIRECTORS’ REPORT Year Ended 31 August 2014 The Directors’ present their report together with the financial report of Bank of Queensland Limited (“the Bank”) and of the Consolidated Entity, being the Bank and its controlled entities for the year ended 31 August 2014 and the independent auditor’s report thereon. DIRECTORS’ DETAILS The Directors of the Bank at any time during or since the end of the financial year are: Name, qualifications and independence status Age Experience, special responsibilities and other Directorships Roger Davis 62 Mr Davis was appointed Chairman on 28 May 2013 and has been a Director since August B.Econ. (Hons), 2008. He has 32 years’ experience in banking and investment banking in Australia, the US and Master of Philosophy Japan. -

Code Security Description ARI Arrium Ltd AWC Alumina Ltd AWE AWE

10-Sep-15 Australian Resources Index Trust NTA & Allotment Notice The manager of the Australian Resources Index Trust advises that as at close of business on 9 September 2015 a total of Nil units has been redeemed or allotted since 8 September 2015. The total number of units on issue on that day was 6,091,647. The asset backing for each ASR unit at close of business (Sydney) on 9 September 2015 was $3.25876 (NTA is net of applicable tax liability). The tracking difference was 1.03% Please note Basket applications and redemptions will be unavailable from Wednesday 09 September 2015 to Friday 25 September 2015. Basket applications and redemptions will resume on Monday 28 September 2015. The following companies are currently in the Fund: Code Security description ARI Arrium Ltd AWC Alumina Ltd AWE AWE Ltd BHP BHP Billiton Ltd BPT Beach Energy Limited BSL Bluescope Steel Ltd CTX Caltex Australia Ltd DLS Drillsearch Energy Ltd EVN Evolution Mining Ltd FMG Fortescue Metals Group IGO Independence Group NL ILU Iluka Resources Ltd KAR Karoon Gas Australia Limited LNG Liquefied Natural Gas Limited NCM Newcrest Mining Ltd NST Northern Star Resources Ltd ORG Origin Energy Ltd OSH Oil Search Ltd OZL OZ Minerals Limited PDN Paladin Energy Ltd. RIO Rio Tinto Ltd RRL Regis Resources Ltd S32 South32 Limited SFR Sandfire Resources NL SGM Sims Metal Management Ltd SIR Sirius Resources NL STO Santos Ltd SXY Senex Energy Limited SYR Syrah Resources Limited WHC Whitehaven Coal Ltd WOR WorleyParsons Ltd WPL Woodside Petroleum Ltd WSA Western Areas Ltd For further information please contact: Smartshares Limited 0800 80 87 80 [email protected]. -

Fidelity Future Leaders Fund: Themes, Lessons and Thank You the Strong Bounce in the Australian Equity Market in Headwinds for the Economy

From the desk of James Abela March 2019 Fidelity Future Leaders Fund: Themes, lessons and thank you The strong bounce in the Australian equity market in headwinds for the economy. The Reserve Bank is becoming February was broadly interpreted as unsustainable more cautious as global growth slows and a rate cut due to lower earnings expectations and weaker looks imminent. outlooks. However, a number of companies reported For investors this will mean a greater focus on balance a more confident outlook and as a result energy, sheets as sustainability moves to front of mind. High risk/ metals, financials, technology, healthcare and low quality businesses which have experienced phenomenal industrials all performed better than expected. support in the search for yield over the last few years will Results season delivered some big positive price moves see this wane as liquidity slows and risk tolerance declines. from those quality growth stocks or cyclicals that delivered Some critical lessons from history form the foundations strong results. Altium, Appen, A2 Milk, Bluescope Steel, of my portfolio construction process: Cleanaway and Breville were notable winners. On the flipside there were some big negative price moves from 1. The Fund’s Quality, Momentum, Transition and Value those that disappointed such as Blackmores, Bingo, Pact (QMTV) framework is a balanced approach that can and Eclipx, proving that markets are still challenging deliver alpha throughout the cycle and is key from a companies that are exposed to cyclical softness or portfolio risk management perspective. competitive market structures. 2. Remember 2007 – high leverage is not an everlasting Some fundamental themes that emerged from the provider of growth. -

Monthly NTA and Performance Update

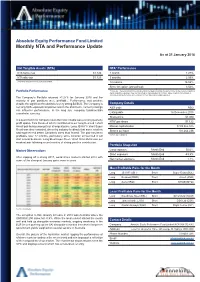

Absolute Equity Performance Fund Limited Monthly NTA and Performance Update As at 31 January 2018 Net Tangible Assets (NTA) NTA* Performance NTA before tax $1.122 1 month 1.27% NTA after tax $1.123 3 months 2.59% $ currency notation refers to Australian Dollars. 12 months 16.02% Since inception (annualised) 3.52% Portfolio Performance *Before tax. These calculations are unaudited and intended to illustrate the performance of the investment portfolio minus corporate expenses. They are calculated on a pre-dividend NTA basis. ‘Since inception (annualised)’ is annualised NTA performance since listing at $1.065 after listing related expenses The Company’s Portfolio returned +1.27% for January 2018 and the majority of pair positions were profitable. Performance was positive despite the significant headwind of a very strong $A/$US. The Company is Company Details net long $US-exposed companies and in the short term, currency swings ASX code AEG can influence performance. In the long run, company fundamentals overwhelm currency. Listing date 16 December 2015 Share price $1.080 In a quiet month for company news the most notable was a strong quarterly NTA* per share $1.122 profit update from Resmed which contributed to our long Resmed / short Ansell pair being amongst our strongest pairs. Long JB Hi-Fi / short Super Market capitalisation $109,365,375 Retail was also rewarded, driven by industry feedback that some retailers Shares on Issue 101,264,236 had experienced better Christmas sales than feared. The pair has been profitable over 12 months, particularly since Amazon announced it will *Before tax ex-dividend start a local business. -

Industry Associations & ASX Companies

Industry Associations, ASX Companies, Shareholder Interests and Lobbying CONTENTS About the Authors ........................................................................................................................ 3 ACCR ............................................................................................................................................ 3 About ISS-caer ............................................................................................................................. 3 About the Report .......................................................................................................................... 4 Foreword ...................................................................................................................................... 4 Introduction .................................................................................................................................. 5 Report Structure .......................................................................................................................... 6 PART 1 - Background ................................................................................................................... 8 What is an Industry Association? .............................................................................................. 8 Advantages and Disadvantages of Belonging to an Industry Association ........................... 10 Australian Legislation and Regulations Covering Industry Associations ............................. 11 -

Socially Conscious Australian Equity Holdings

Socially Conscious Australian Equity Holdings As at 30 June 2021 Country of Company domicile Weight COMMONWEALTH BANK OF AUSTRALIA AUSTRALIA 10.56% CSL LTD AUSTRALIA 8.46% AUST AND NZ BANKING GROUP AUSTRALIA 5.68% NATIONAL AUSTRALIA BANK LTD AUSTRALIA 5.32% WESTPAC BANKING CORP AUSTRALIA 5.08% TELSTRA CORP LTD AUSTRALIA 3.31% WOOLWORTHS GROUP LTD AUSTRALIA 2.93% FORTESCUE METALS GROUP LTD AUSTRALIA 2.80% TRANSURBAN GROUP AUSTRALIA 2.55% GOODMAN GROUP AUSTRALIA 2.34% WESFARMERS LTD AUSTRALIA 2.29% BRAMBLES LTD AUSTRALIA 1.85% COLES GROUP LTD AUSTRALIA 1.80% SUNCORP GROUP LTD AUSTRALIA 1.62% MACQUARIE GROUP LTD AUSTRALIA 1.54% JAMES HARDIE INDUSTRIES IRELAND 1.51% NEWCREST MINING LTD AUSTRALIA 1.45% SONIC HEALTHCARE LTD AUSTRALIA 1.44% MIRVAC GROUP AUSTRALIA 1.43% MAGELLAN FINANCIAL GROUP LTD AUSTRALIA 1.13% STOCKLAND AUSTRALIA 1.11% DEXUS AUSTRALIA 1.11% COMPUTERSHARE LTD AUSTRALIA 1.09% AMCOR PLC AUSTRALIA 1.02% ILUKA RESOURCES LTD AUSTRALIA 1.01% XERO LTD NEW ZEALAND 0.97% WISETECH GLOBAL LTD AUSTRALIA 0.92% SEEK LTD AUSTRALIA 0.88% SYDNEY AIRPORT AUSTRALIA 0.83% NINE ENTERTAINMENT CO HOLDINGS LIMITED AUSTRALIA 0.82% EAGERS AUTOMOTIVE LTD AUSTRALIA 0.82% RELIANCE WORLDWIDE CORP LTD UNITED STATES 0.80% SANDFIRE RESOURCES LTD AUSTRALIA 0.79% AFTERPAY LTD AUSTRALIA 0.79% CHARTER HALL GROUP AUSTRALIA 0.79% SCENTRE GROUP AUSTRALIA 0.79% ORORA LTD AUSTRALIA 0.75% ANSELL LTD AUSTRALIA 0.75% OZ MINERALS LTD AUSTRALIA 0.74% IGO LTD AUSTRALIA 0.71% GPT GROUP AUSTRALIA 0.69% Issued by Aware Super Pty Ltd (ABN 11 118 202 672, AFSL 293340) the trustee of Aware Super (ABN 53 226 460 365). -

Asx Clear – Acceptable Collateral List 28

et6 ASX CLEAR – ACCEPTABLE COLLATERAL LIST Effective from 20 September 2021 APPROVED SECURITIES AND COVER Subject to approval and on such conditions as ASX Clear may determine from time to time, the following may be provided in respect of margin: Cover provided in Instrument Approved Cover Valuation Haircut respect of Initial Margin Cash Cover AUD Cash N/A Additional Initial Margin Specific Cover N/A Cash S&P/ASX 200 Securities Tiered Initial Margin Equities ETFs Tiered Notes to the table . All securities in the table are classified as Unrestricted (accepted as general Collateral and specific cover); . Specific cover only securities are not included in the table. Any securities is acceptable as specific cover, with the exception of ASX securities as well as Participant issued or Parent/associated entity issued securities lodged against a House Account; . Haircut refers to the percentage discount applied to the market value of securities during collateral valuation. ASX Code Security Name Haircut A2M The A2 Milk Company Limited 30% AAA Betashares Australian High Interest Cash ETF 15% ABC Adelaide Brighton Ltd 30% ABP Abacus Property Group 30% AGL AGL Energy Limited 20% AIA Auckland International Airport Limited 30% ALD Ampol Limited 30% ALL Aristocrat Leisure Ltd 30% ALQ ALS Limited 30% ALU Altium Limited 30% ALX Atlas Arteria Limited 30% AMC Amcor Ltd 15% AMP AMP Ltd 20% ANN Ansell Ltd 30% ANZ Australia & New Zealand Banking Group Ltd 20% © 2021 ASX Limited ABN 98 008 624 691 1/7 ASX Code Security Name Haircut APA APA Group 15% APE AP -

Australian Equities Lending Margins Effective 21 April 2021

Australian Equities Lending Margins Effective 21 April 2021 Stock ASX Margin Stock ASX Margin Stock ASX Margin Code Rate Code Rate Code Rate A2B Australia A2B 40% AusNet Services AST 70% Costa Group Holdings CGC 60% The A2 Milk Company A2M 65% ASX ASX 75% Challenger Financial Australian Agricultural Company AAC 55% AUB Group AUB 50% Services Group CGF 70% Adelaide Brighton ABC 70% Australian United Challenger Capital Notes CGFPA 60% Abacus Property Group ABP 60% Investment Company AUI 70% Challenger Capital Notes 2 CGFPB 60% Audinate Group AD8 40% Aventus Retail Property Group AVN 50% Challenger Capital Notes 3 CGFPC 60% Adairs ADH 40% Alumina AWC 70% Charter Hall Group CHC 70% APN Industria REIT ADI 40% Accent Group AX1 40% Champion Iron CIA 50% Australian Ethical Amaysim Australia AYS 40% Cimic Group CIM 70% Investment Limited AEF 40% Aurizon Holdings AZJ 75% Carlton Investments CIN 50% Australian Foundation Bapcor BAP 60% Centuria Industrial REIT CIP 60% Investment Company AFI 75% Baby Bunting Group BBN 40% Collins Foods CKF 50% Ainsworth Game Technology AGI 40% Bendigo & Adelaide Bank BEN 70% Class CL1 40% AGL Energy AGL 75% Bendigo & Adelaide Bank BENHB 65% Clean Teq Holdings CLQ 40% AGL Energy USFDS AGLHA 75% Bendigo & Adelaide Bank CPS BENPE 65% Clover Corporation CLV 40% Automotive Holdings Group AHG 55% Bendigo & Adelaide Bank CPS BENPF 65% Charter Hall Long Wale REIT CLW 60% Asaleo Care AHY 50% Bendigo & Adelaide Bank CPS BENPG 65% Centuria Metropolitan REIT CMA 50% Auckland International Airport AIA 70% Bell Financial Group -

FTSE World Asia Pacific

2 FTSE Russell Publications 19 August 2021 FTSE World Asia Pacific Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) a2 Milk 0.04 NEW Asustek Computer Inc 0.1 TAIWAN Cheil Worldwide 0.02 KOREA ZEALAND ASX 0.12 AUSTRALIA Cheng Shin Rubber Industry 0.03 TAIWAN AAC Technologies Holdings 0.05 HONG KONG Atlas Arteria 0.05 AUSTRALIA Chiba Bank 0.04 JAPAN ABC-Mart 0.02 JAPAN AU Optronics 0.08 TAIWAN Chicony Electronics 0.02 TAIWAN Accton Technology 0.07 TAIWAN Auckland International Airport 0.06 NEW China Airlines 0.02 TAIWAN Acer 0.03 TAIWAN ZEALAND China Development Financial Holdings 0.07 TAIWAN Acom 0.02 JAPAN Aurizon Holdings 0.05 AUSTRALIA China Life Insurance 0.02 TAIWAN Activia Properties 0.03 JAPAN Ausnet Services 0.03 AUSTRALIA China Motor 0.01 TAIWAN ADBRI 0.01 AUSTRALIA Australia & New Zealand Banking Group 0.64 AUSTRALIA China Steel 0.19 TAIWAN Advance Residence Investment 0.05 JAPAN Axiata Group Bhd 0.04 MALAYSIA China Travel International Investment <0.005 HONG KONG ADVANCED INFO SERVICE 0.06 THAILAND Azbil Corp. 0.06 JAPAN Hong Kong Advantech 0.05 TAIWAN B.Grimm Power 0.01 THAILAND Chow Tai Fook Jewellery Group 0.04 HONG KONG Advantest Corp 0.19 JAPAN Bandai Namco Holdings 0.14 JAPAN Chubu Elec Power 0.09 JAPAN Aeon 0.2 JAPAN Bangkok Bank (F) 0.02 THAILAND Chugai Seiyaku 0.27 JAPAN AEON Financial Service 0.01 JAPAN Bangkok Bank PCL (NVDR) 0.01 THAILAND Chugoku Bank 0.01 JAPAN Aeon Mall 0.02 JAPAN Bangkok Dusit Medical Services PCL 0.07 THAILAND Chugoku Electric Power 0.03 JAPAN Afterpay Touch Group 0.21 AUSTRALIA Bangkok Expressway and Metro 0.02 THAILAND Chunghwa Telecom 0.17 TAIWAN AGC 0.08 JAPAN Bangkok Life Assurance PCL 0.01 THAILAND CIMB Group Holdings 0.08 MALAYSIA AGL Energy 0.04 AUSTRALIA Bank of East Asia 0.03 HONG KONG CIMIC Group 0.01 AUSTRALIA AIA Group Ltd. -

For Personal Use Only Use Personal For

ADDRESS CONTACT DETAILS UNIT REGISTRY Level 16 Telephone +61 2 9409 3670 c/- Link Market Services Limited 61 Lavender Street Investor Services 1800 ARDENT Level 12, 680 George Street Milsons Point NSW 2061 Fax +61 2 9409 3679 Sydney NSW 2000 AUSTRALIA www.ardentleisure.com Locked Bag A14 Sydney South NSW 1235 Telephone 1300 720 560 [email protected] ASX RELEASE 13 June 2012 The Manager Company Notices Section ASX Limited 20 Bridge Street SYDNEY NSW 2000 Dear Sir/Madam MORGAN STANLEY CONFERENCE PRESENTATION Please find attached for release to the market a presentation to be given by Mr Greg Shaw today at the Morgan Stanley Emerging Companies Conference. Yours faithfully Alan Shedden Company Secretary Ardent Leisure Group is a specialist operator of leisure and entertainment assets across Australia, New Zealand and the United States. The Group operates Dreamworld, WhiteWater World, SkyPoint, d’Albora Marinas, AMF and Kingpin bowling centres and Goodlife fitness centres across Australia and New Zealand. The Group also operates the Main Event family entertainment centres in the United States. For further information on the Group’s activities please visit our website at www.ardentleisure.com.au For personal use only Ardent Leisure Group Comprising Ardent Leisure Trust ARSN 093 193 438 (Manager: Ardent Leisure Management Limited ABN 36 079 630 676, AFS Licence No. 247010) and Ardent Leisure Limited ABN 22 104 529 106 Morgan Stanley 2012 Emerging Companies Conference For personal use only Ardent Leisure Profile ― Ardent Leisure is one of Australia’s largest specialist operators of leisure and entertainment assets. ― Occupies dominant positions in a range of affordable leisure sectors: Sector Businesses Number Theme parks Dreamworld, WhiteWater World, and SkyPoint 3 Bowling AMF and Kingpin 49 Health Clubs Goodlife Health Clubs 45 Family Entertainment Centres Main Event USA 10 Marinas D’Albora Marinas 7 ― Resilient earning streams from diverse affordable leisure product range which For personal use only appeals to price conscious consumer.