A Model of Dynamic Limit Pricing with an Application to the Airline Industry

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Three Types of Collusion: Fixing Prices, Rivals, and Rules Robert H

University of Baltimore Law ScholarWorks@University of Baltimore School of Law All Faculty Scholarship Faculty Scholarship 2000 The Three Types of Collusion: Fixing Prices, Rivals, and Rules Robert H. Lande University of Baltimore School of Law, [email protected] Howard P. Marvel Ohio State University, [email protected] Follow this and additional works at: http://scholarworks.law.ubalt.edu/all_fac Part of the Antitrust and Trade Regulation Commons, and the Law and Economics Commons Recommended Citation The Three Types of Collusion: Fixing Prices, Rivals, and Rules, 2000 Wis. L. Rev. 941 (2000) This Article is brought to you for free and open access by the Faculty Scholarship at ScholarWorks@University of Baltimore School of Law. It has been accepted for inclusion in All Faculty Scholarship by an authorized administrator of ScholarWorks@University of Baltimore School of Law. For more information, please contact [email protected]. ARTICLES THE THREE TYPES OF COLLUSION: FIXING PRICES, RIVALS, AND RULES ROBERTH. LANDE * & HOWARDP. MARVEL** Antitrust law has long held collusion to be paramount among the offenses that it is charged with prohibiting. The reason for this prohibition is simple----collusion typically leads to monopoly-like outcomes, including monopoly profits that are shared by the colluding parties. Most collusion cases can be classified into two established general categories.) Classic, or "Type I" collusion involves collective action to raise price directly? Firms can also collude to disadvantage rivals in a manner that causes the rivals' output to diminish or causes their behavior to become chastened. This "Type 11" collusion in turn allows the colluding firms to raise prices.3 Many important collusion cases, however, do not fit into either of these categories. -

Monopoly Pricing in a Time of Shortage James I

Loyola University Chicago Law Journal Volume 33 Article 6 Issue 4 Summer 2002 2002 Monopoly Pricing in a Time of Shortage James I. Serota Vinson & Elkins L.L.P. Follow this and additional works at: http://lawecommons.luc.edu/luclj Part of the Law Commons Recommended Citation James I. Serota, Monopoly Pricing in a Time of Shortage, 33 Loy. U. Chi. L. J. 791 (2002). Available at: http://lawecommons.luc.edu/luclj/vol33/iss4/6 This Article is brought to you for free and open access by LAW eCommons. It has been accepted for inclusion in Loyola University Chicago Law Journal by an authorized administrator of LAW eCommons. For more information, please contact [email protected]. Monopoly Pricing in a Time of Shortage James L Serota* I. INTRODUCTION Traditionally, the electric power industry has been heavily regulated at both the federal and state levels. Recently, the industry has been evolving towards increasing emphasis on market competition and less pervasive regulation. Much of the initial impetus for change has occurred during periods of reduced demand and increased supply. More recently, increases in demand and supply shortages have led to brownouts, rolling blackouts, price spikes and accusations of "price gouging."' The purpose of this paper is to examine the underlying economic and legal bases for regulation and antitrust actions, and the antitrust ground rules for assessing liability for "monopoly pricing in times of shortage." In this author's view, price changes in response to demand are the normal reaction of a competitive market, and efforts to limit price changes in the name of "price gouging" represent an effort to return to pervasive regulation of electricity. -

Regulation Methods in Natural Monopoly Markets Case of Russian Gas Network Companies

International Journal of Engineering Research and Technology. ISSN 0974-3154, Volume 12, Number 5 (2019), pp. 624-630 © International Research Publication House. http://www.irphouse.com Regulation Methods in Natural Monopoly Markets Case of Russian Gas Network Companies Filatova Irina1, Shabalov Mikhail2 and Nikolaichuk Liubov3 Department of Economics, Accounting and Finance, Saint Petersburg Mining University, Russian Federation. 1ORCIDs: 0000-0002-0505-8274, 20000-0003-2224-6530, 30000-0001-5013-1787 Abstract difficult to predict and regulate. It is worth noting that the state in the gas distribution industry acts simultaneously as The main stakeholders in the gas distribution sector two stakeholders: the first reflects its interests as an authority (government, shareholders and consumers) have different regulating the functioning and development of the industry; interests and goals. The state, as a regulatory body, should and the second one represents the interests of the state as the find the best regulatory methods in order to achieve the main shareholder of gas companies. maximum effect of public welfare: direct (pricing) and indirect (price influencing). The use of the “costs plus” A key tool designed to ensure a balance of interests of the method makes it possible to set the lowest possible tariffs for above parties is the policy of state price regulation, the goal of the transportation of natural gas, but it leads to the emergence which is to prevent market failures in order to maintain and of a “tariff precedent”, a loss of profits for companies, limited strengthen public welfare [2, 3]. At the same time, the need investment in the development of the sector. -

Methods for Increasing Competition in Telecommunications Markets

Methods for Increasing Competition in Telecommunications Markets By Mark Jamison Public Utility Research Center University of Florida Gainesville, Florida March 2012 Contact Information: Dr. Mark Jamison, Director Public Utility Research Center PO Box 117142 205 Matherly Hall University of Florida Gainesville, FL 32611-7142 +1.352.392.6148 [email protected] The author would like to thank Dr. Janice Hauge for her helpful comments on this paper and Professor Suphat Suphachalasai for his recommendations on content. The author also would like to thank Thammasat University and the National Telecommunications Commission of Thailand for their generous financial support. All errors and omissions are the responsibility of the author. Abstract We examine the concepts of workable competition, barriers and conduct that limit the achievement of workable competition, and steps that sector regulators can take to address these obstacles. The concept of workable competition is an attempt to describe a market situation that does not fit the model of perfect competition, but that has enough features of perfect competition that government intervention is unnecessary and possibly even counterproductive. The first attempt to define workable competition focused on issues of product differentiation, the number and size-distribution of producers, restrictions on output, imperfection in the value chain, information, scale economies, and producer ability to change output. Most recently a simple set of metrics emerged, namely that there should be at least 5 reasonably comparable rivals, none of the firms should have more than a 40 percent market share, and entry by new competitors must be easy. Barriers to achieving workable competition can be divided into demand side market features, supply side market features, and firm conduct issues. -

Maximum Price Fixing

University of Chicago Law School Chicago Unbound Journal Articles Faculty Scholarship 1981 Maximum Price Fixing Frank H. Easterbrook Follow this and additional works at: https://chicagounbound.uchicago.edu/journal_articles Part of the Law Commons Recommended Citation Frank H. Easterbrook, "Maximum Price Fixing," 48 University of Chicago Law Review 886 (1981). This Article is brought to you for free and open access by the Faculty Scholarship at Chicago Unbound. It has been accepted for inclusion in Journal Articles by an authorized administrator of Chicago Unbound. For more information, please contact [email protected]. Maximum Price Fixing Frank H. Easterbrookf If all of the grocers in a city agreed to sell 100-watt light bulbs for no more than fifty cents, that would be maximum price fixing. If a group of optometrists agreed to charge no more than $30 for an eye examination and to display a distinctive symbol on the shops of parties to the agreement, that would be maximum price fixing. And if most of the physicians in a city, acting through a nonprofit association, offered to treat patients for no more than a given price if insurance companies would agree to pay the fee, that agreement would be maximum price fixing too. A maximum price appears to be a boon for consumers. The optometrists' symbol, for example, helps consumers find low-cost suppliers of the service. But the agreement also appears to run afoul of the rule against price fixing, under which "a combination formed for the purpose and with the effect of raising, depressing, fixing, pegging, or stabilizing the price of a commodity .. -

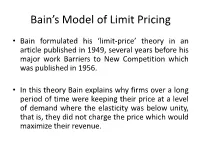

Bain's Model of Limit Pricing

Bain’s Model of Limit Pricing • Bain formulated his ‘limit-price’ theory in an article published in 1949, several years before his major work Barriers to New Competition which was published in 1956. • In this theory Bain explains why firms over a long period of time were keeping their price at a level of demand where the elasticity was below unity, that is, they did not charge the price which would maximize their revenue. His conclusion was that the traditional theory was unable to explain this empirical fact due to the omission from the pricing decision of an important factor, namely the threat of potential entry. Traditional theory was concerned only with actual entry, which resulted in the long-run equilibrium of the firm and the industry (where P = LAC). Limit Pricing • Traditional theory only discusses actual entry , not potential entry of firms. This leads to normal profits in long run in perfect and imperfect competition. • According to Bain Firms don’t maximise profit in the short run due to fear of potential entry of new firms attracted by the maximum profits. These entry can reduce their long run profit. Definition of Limit Pricing It is the highest price that a existing firm charges without fear of attracting new firms. Entry prevention price acts as barrier to entry of new firms. Assumptions • There is a determinate long-run demand curve for industry output, which is unaffected by price adjustments of sellers or by entry. Hence the market marginal revenue curve is determinate. The long-run industry-demand curve shows the expected sales at different prices maintained over long periods. -

Market Entry, Monopolistic Competition, and Oligopoly

8 Market Entry, Monopolistic Competition, and Oligopoly Chapter Summary This chapter is about market entry, monopolistic competition, and oligopoly. In a monopolistically competitive market, firms differentiate their products, and entry continues until each firm in the market makes zero economic profit. In an oligopoly, a few firms serve a market, and firms have an incentive to act strategically: They may cooperate to fix prices and may price their products strategically to keep other firms out of the market. In markets with a small number of firms, the role of public policy is to regulate monopolists and promote competition. Here are the main points of the chapter: • The entry of a firm into a market decreases the market price, decreases output per firm, and increases the average cost of production. • In the long-run equilibrium with monopolistic competition, marginal revenue equals marginal cost, price equals average cost, and economic profit is zero. • A firm can use celebrity endorsements and other costly advertisements to signal its belief that a product will be appealing. • Each firm in an oligopoly has an incentive to underprice the other firms, so price fixing will be unsuccessful unless firms have some way of enforcing a price-fixing agreement. • To prevent a second firm from entering a market, an insecure monopolist may commit itself to producing a relatively large quantity and accepting a relatively low price. • Under an average-cost pricing policy, the regulated price for a natural monopoly is equal to the average cost of production. • The government uses antitrust policy to break up some dominant firms, prevent some corporate mergers, and regulate business practices that reduce competition. -

Final Rule: Regulation

SECURITIES AND EXCHANGE COMMISSION 17 CFR PARTS 200, 201, 230, 240, 242, 249, and 270 [Release No. 34-51808; File No. S7-10-04] RIN 3235-AJ18 REGULATION NMS AGENCY: Securities and Exchange Commission. ACTION: Final rules and amendments to joint industry plans. SUMMARY: The Securities and Exchange Commission (“Commission”) is adopting rules under Regulation NMS and two amendments to the joint industry plans for disseminating market information. In addition to redesignating the national market system rules previously adopted under Section 11A of the Securities Exchange Act of 1934 (“Exchange Act”), Regulation NMS includes new substantive rules that are designed to modernize and strengthen the regulatory structure of the U.S. equity markets. First, the "Order Protection Rule" requires trading centers to establish, maintain, and enforce written policies and procedures reasonably designed to prevent the execution of trades at prices inferior to protected quotations displayed by other trading centers, subject to an applicable exception. To be protected, a quotation must be immediately and automatically accessible. Second, the "Access Rule" requires fair and non- discriminatory access to quotations, establishes a limit on access fees to harmonize the pricing of quotations across different trading centers, and requires each national securities exchange and national securities association to adopt, maintain, and enforce written rules that prohibit their members from engaging in a pattern or practice of displaying quotations that lock or cross automated quotations. Third, the "Sub-Penny Rule" prohibits market participants from accepting, ranking, or displaying orders, quotations, or indications of interest in a pricing increment smaller than a penny, except for orders, quotations, or indications of interest that are priced at less than $1.00 per share. -

Monopolization, Mergers, and Markets: a Century Past and the Future

Monopolization, Mergers, and Markets: A Century Past and the Future Phillip Areedat Significant anniversaries are often occasions for wholesale general- ization, congratulation, or lamentation. My theme is the narrower one of, to borrow a phrase, the law in search of itself. The statutes on which it rests are so general that antitrust law shares a great deal with the com- mon law and is no more to be judged in gross than the law of contracts. Were I nevertheless to generalize grossly, I would point to the large and perhaps increasing number of sensible decisions giving coherence to anti- trust policy. Of course, not all decisions fall within that happy category. I have been asked to discuss the future viability of legal doctrines concerning monopolies, mergers, and markets, and to comment on which of them either promote the public interest or impair it by obstructing the benefits sometimes flowing from a firm's integration or expansion. In this Article, I cannot summarize the several volumes of the Areeda-Tur- ner treatise' or its supplement2 that touch on these subjects but must limit my discussion to a few salient monopolization-merger-market doc- trines. Although doctrines take their meaning mainly from their applica- tions, I distinguish sensible doctrines from their aberrant applications and consider their viability by examining both unsatisfactory current approaches ripe for change and developing tendencies toward reform. I MONOPOLIZATION Sherman Act section 2 declares simply that monopolization is a crime, along with attempts and conspiracies to monopolize.3 It does not define monopoly, explain whether mere monopoly is unlawful in the absence of impropriety, or specify any criteria for determining whether an impropriety has occurred. -

1 © 2011 Richard S. Markovits This “Book” (Two-Volume Study) Has Nine

THE ECONOMICS OF INTERPRETING AND APPLYING U.S. AND E.C./E.U. ANTITRUST LAW: A SUMMARY © 2011 Richard S. Markovits This “book” (two-volume study) has nine inter-related components. First, it articulates or (in one instance) discusses operational definitions of seven economic concepts that play a critical role in U.S. antitrust law and E.C./E.U. competition law. The first is the general concept of conduct undertaken with specific anticompetitive intent—i.e., conduct that would have been unprofitable if its profitability was not otherwise distorted by the extant Pareto imperfections whose perpetrator-perceived ex ante profitability was critically inflated by the perpetrator’s belief that it would or might reduce the absolute attractiveness of the offers against which the perpetrator would have to compete. This concept covers the cognate U.S. Sherman Act concepts of a restraint of trade, monopolizing conduct, or an attempt to monopolize, the E.C./E.U. now- Article 101 concept of conduct whose object is the prevention or restriction of competition, and the E.C./E.U. now-Article 102 concept of conduct that is exclusionary. The second economic concept that this book operationalizes is the concept of predatory conduct, which is a subtype of conduct undertaken with specific anticompetitive intent: conduct is correctly termed predatory if (1) its perpetrator’s (or perpetrators’) ex ante perception that it was profitable was critically affected by the perpetrator’s perception that it would reduce the absolute attractiveness of the best offers against which the perpetrator would have to compete by driving a rival out, deterring a rival from introducing a new investment that would be rivalrous with one or more projects of the perpetrator, or by inducing an actual/potential rival of the perpetrator to relocate/locate an investment further away in product-space from the perpetrator’s project(s) and (2) these effects would render the conduct profitable though economically inefficient if its profitability were not otherwise distorted. -

Strategic Business Behavior and Antitrust

WORKING PAPERS STRATEGIC BUSINESS BEHAVIOR AND ANTITRUST Charles A. Holt and David T. Scheffman WORKING PAPER NO. 162 April 1988 FfC Bureau of Economics working papers are preliminary materials circulated to stimulate discussion and critical comment All data contained in them are in the public domain. This iucludes information obtained by the Commi~on which has become part of pob6c record. The analyses and conclusions set forth are those of the authors and do not nece.\Wily reflect the views of other members of the Bureau of Economics, other Commission ~ or the Commission itself. Upon request, single copies of the paper will be provided. References in publications to FfC Bureau of Economics working papers by FfC economists (other than acknowledgement by a writer that he has access to such unpUblished materials) should be cleared with the author to protect the tentative character of these papers. BUREAU OF ECONOMICS FEDERAL TRADE COMMISSION WASHINGTON, DC 20580 Strategic Business Behavior and Antitrust- Charles A. Holt and David T. Scheffman 1 I. In troduction During the seventies business consultants and academics became interested in "business strategy" as an instrument for improving profitability. The emphasis of this approach was generally on actions that a firm could take to improve its long run competitive position. At about the same time, there was a renewed interest by industrial organization economists and antitrust authorities in the possibility that monopoly power could be created or enhanced through predatory or limit pricing or through use of non-price instruments such as investments, patents, contracts, etc. Finally, the renaissance of game theory that also began in the seventies spawned a renewed interest in theories of oligopoly that explicitly incorporated dynamic and "stra tegic" elemen ts. -

Chapter 13 Advanced Topics in Business Strategy

Managerial Economics & Business Strategy Chapter 13 Advanced Topics in Business Strategy McGraw-Hill/Irwin Copyright © 2010 by the McGraw-Hill Companies, Inc. All rights reserved . Overview I. Limit Pricing to Prevent Entry II. Predatory Pricing to Lessen Competition III. Raising Rivals’ Costs to Lessen Competition IV. Price Discrimination as a Strategic Tool V. Changing the Timing of Decisions VI. Penetration Pricing to Overcome Network Effects 13-2 Limit Pricing Strategy where an incumbent (existing firm) prices below the monopoly price in order to keep potential entrants out of the market. Goal is to lessen competition by eliminating potential competitors’ incentives to enter the market. 13-3 Monopoly Profits This monopolist is earning positive $ Π M economic profits. MC These profits may P M induce other firms AC to enter the market. AC M Questions: D M Can the monopolist prevent entry? M Q Q If so, is it profitable MR to do so? 13-4 Limit Pricing Incumbent produces QL instead of monopoly output (Q M). Resulting price, P L, is lower than monopoly $ M price (P ). Entrant's residual Residual demand demand curve curve is the market P M M L demand (D ) minus Q P L . AC Entry is not profitable P = AC D M because entrant’s residual demand lies below AC. Optimal limit pricing Q Q M Q L Quantity results in a residual demand such that, if the entrant entered and produced Q units, its profits would be zero. 13-5 Potential Problems with Limit Pricing It isn’t generally profitable for the incumbent to maintain an output of Q L once entry occurs.