Consultation Response

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Aspects of Leases Collated Responses

Collated responses to Discussion Paper on Aspects of Leases: Termination (DP No 165) Consultation period ended: 14 September 2018 This document contains the text of consultation responses. CONTENTS 1. ANDERSON STRATHERN LLP ......................................................................... 3 2. BOOTS ............................................................................................................. 10 3. BRODIES LLP .................................................................................................. 15 4. BURNESS PAUL LLP ...................................................................................... 26 5. CMS CAMERON MCKENNA NABARRO OLSWANG LLP ............................. 42 6. CRAIG CONNAL QC ........................................................................................ 52 7. DENTONS UK AND MIDDLE EAST LLP ......................................................... 62 8. DLA PIPER SCOTLAND LLP .......................................................................... 72 9. DR CRAIG ANDERSON, ROBERT GORDONS UNIVERSITY ........................ 80 10. DWF LLP ....................................................................................................... 90 11. ERIC YOUNG, ERIC YOUNG & CO .............................................................. 98 12. FACULTY OF ADVOCATES ....................................................................... 100 13. FEDERATION OF SMALL BUSINESSES ................................................... 114 14. GILLESPIE MACANDREW LLP ................................................................. -

Civil Legal Assistance Register

Civil register at 17.09.21 Firm Name Address Line1 Address Line2 Address Line3 Postcode Phone Number 1ST LEGAL LIMITED 68 KYLE STREET AYR KA7 1RZ 01292 290666 A C MILLER & MACKAY 63 SCOTT STREET PERTH PH2 8JN 01738 620087 A C O'NEILL & CO SECOND FLOOR 32 HIGH STREET DUMBARTON G82 1LL 01389 762997 A C WHITE 23 WELLINGTON SQUARE AYR KA7 1HG 01292 266900 A J GORDON & CO SOLICITORS 2 BOTANIC CRESCENT GLASGOW G20 8QQ 07812 000554 AAMER ANWAR & CO 63 CARLTON PLACE GLASGOW G5 9TW 0141 429 7090 ABERDEIN CONSIDINE & CO 5-9 BON-ACCORD CRESCENT ABERDEEN AB11 6DN 01224 337421 ADAIRS 3 CASTLE STREET DUMBARTON G82 1QS 01389 767625 ADAMS LAW 11 KINGSKNOWE PARK EDINBURGH EH14 2JQ 0131 443 4436 AFFINITY FAMILY LAW 4 THE CHALET BROOMKNOWE ROAD KILMACOLM PA13 4JG 01505 873751 AITKENS 17 GRAMPIAN COURT BEVERIDGE SQUARE LIVINGSTON EH54 6QF 01506 417737 AJ BRADLEY & CO FLOOR 4, SUITE 13 111 UNION STREET GLASGOW G1 3TA 0141 374 0474 ALAN MEECHAN SOLICITORS C/O 19 BATHGATE ROAD BLACKBURN WEST LOTHIAN EH47 7LN 07878 159264 ALEXANDER BOYD 93 HIGH STREET, MERCHANT CITY GLASGOW G1 1NB 0141 237 3137 ALEXANDER MCBURNEY 338 DUMBARTON ROAD GLASGOW G11 6TG 0141 576 4808 ALEXIS HUNTER FAMILY LAW CARTSIDE HOUSE, 1/7 CLARKSTON ROAD CATHCART GLASGOW G44 4EF 0141 404 0124 ALI & CO SUITE 540 103 BYRES ROAD GLASGOW G11 5HW 07849 007 162 ALLAN BLACK & MCCASKIE 151 HIGH STREET ELGIN IV30 1DX 01343 543355 ALLAN KERR 13 GRANGE PLACE KILMARNOCK AYRSHIRE KA1 2AB 01563 571571 ALLAN MCDOUGALL MCQUEEN 3 COATES CRESCENT EDINBURGH EH3 7AL 0131 225 2121 ALLCOURT 1 LENNOX HOUSE ALMONDVALE -

Set up for the Future COVID-19 Marks One of Those Seminal Changes in the Human Story

Leaders in law: accredited Employee ownership: Divorce in a recession: legal technologists strength in adversity issues in valuing assets P.15 P.18 P.22 Journal of the Law Society of Scotland Volume 65 Number 9 – September 2020 Set up for the future COVID-19 marks one of those seminal changes in the human story. What new skills do we require as a result? Scottish Land Law Publishing under the auspices of the Scottish Universities Law Institute, the second volume to this well-established and respected work is a thoroughly updated and comprehensive account of Scottish land law. It brings together material of significant practical importance in relation to the rights and obligations inherent in the ownership of land. Key legislation includes: • The Conveyancing and Feudal Reform (Scotland) Act 1970 • The Title Conditions (Scotland) Act 2003 3rd Edition, Volume 2 • The Land Reform (Scotland) Act 2003 October 2020 | £100 9780414017832 Continuing from Volume I, the content of Volume II includes: Chapter 19: General Principles of Security Rights Chapter 20: Standard Securities PLACE YOUR ORDER TODAY Chapter 21: Floating Charges sweetandmaxwell.co.uk +44 (0)345 600 9355 Chapter 22: Involuntary Heritable Securities Chapter 23: Title Conditions and other Burdens Chapter 24: Real Burdens Chapter 25: Servitudes Chapter 26: Judicial Variation and Discharge of Title Conditions Chapter 27: Public Access Rights Chapter 28: Nuisance and other Delicts Chapter 29: Social Control of Land Use Chapter 30: Compulsory Acquisition Chapter 31: Community Rights to Buy REUTERS/Russell Cheyne TR1218702/08-20 Click here to see Peter’s welcome Scottish Land Law message Publishing under the auspices of the Scottish Universities Law Institute, the second volume Publishers Editor to this well-established and respected work is a thoroughly updated and comprehensive The Law Society of Scotland Email > [email protected] Atria One, 144 Morrison Street, account of Scottish land law. -

FLB Booklet V2.Indd 1 10/11/2011 12:24 Contents

tHe family law association Guide to separation and divorce in scotland m familylaassociation FLB booklet v2.indd 1 10/11/2011 12:24 Contents INTRODUCTION: Breaking up is hard to do 3 EDITOR ROGER CHAPTER 1: Do I need a solicitor? 4 MACKENZIE, MACLAY MURRAY CHAPTER 2: The family home 7 & SPENS, GLASGOW CHAPTER 3: Children 10 CHAPTER 4: Domestic violence – interdicts and exclusion orders 14 CHAPTER 5: Aliment and child support 18 CHAPTER 6: Division of matrimonial property 22 CHAPTER 7: Divorce 30 CHAPTER 8: Cohabitation 34 CHAPTER 9: Common myths and misconceptions 38 CHAPTER 10: Agreements 40 MEMBER LISTINGS 43 m familylaassociation FLB booklet v2.indd 2 10/11/2011 12:24 3 IntroDUCtIon Breaking up is hard to do Graham THE ending of a relationship is available. Negotiation, mediation, Harding, always a diffi cult time for those collaboration or arbitration may Chair of the involved. It does not just affect well offer a less expensive and more Family Law the couple themselves but also effective solution than court action. Association children, grandparents, other family There will be practical matters members and even friends. Anyone to consider at an early stage, such as: considering separation should who will look after the children; how therefore take time to fully consider will the mortgage or rent be paid; are its effects before making such a there state benefi ts available; what major decision. fi nancial support does one party owe This easy-to-read guide is to the other? intended to assist anyone whose In the longer term, decisions marriage, civil partnership or may have to be made on the division relationship has come to an end by of property. -

Scots Law 2020 – the Leading Conference & Exhibition Series Glasgow Hilton

Scots Law 2020 – the leading conference & exhibition series Glasgow Hilton The Conveyancing Conference Sponsored by: 9th March, 9.30am - 5.00pm 6 hours CPD Chair: Professor Kenneth C Ross, Loch Lomond & the Trossachs National Park Authority Access rights under the Land Reform (Scotland) Act 2003 Plans and consequences • Extent of rights and limits of rights • Registers Plans Reports • Creelman v Argyll and Bute Council • Real life examples of Plans Reports and adverse matters • Forbes v Fife Council • What to consider when remedial action is required • Manson v Midlothian Council • Requirements for new deed plans • Core paths and other paths Derek Hand, First Scottish • When is a garden not a garden? Professor Kenneth C Ross, Loch Lomond & the Trossachs National Park Authority Professional indemnity insurance for solicitors in Scotland • The Importance of risk management Enforcement of missives • The potential for conflict of interest in conveyancing transactions Alan McMillan, Burness Paull • Examples of claims against solicitors working in conveyancing transactions • Actions to reduce risk Common good law - perils and pitfalls Matthew Thomson, Lockton • What is common good, exactly? • When is something inalienable? The Private Housing (Tenancies) (Scotland) Act 2016 • Title issues and the Common Good Register • New Model Tenancy Agreements • Missive issues - court authority • Restrictions on rent review • The new consultation regime and community empowerment • Rent Pressure Zones Andrew C Ferguson, Fife Council • Termination of leases -

Solicitor Panel Spreadsheet

Solicitor Panel Spreadsheet How to search this spreadsheet: To search this spreadsheet, press "Ctrl" and "F" together to display the search box. Enter the solicitor name to search for a specific solicitor or the first part of your postcode to look for solicitors in your area. Select "Find All" and any solicitors which are relevant to your search criteria will be displayed. Solicitor Name GORDON BROWN ASSOCIATES DUMMY SOLICITOR DAVID AULD & CO GORDONS PROPERTY LAWYERS B LEGAL LTD HOWES PERCIVAL FIELD CUNNINGHAM & CO SUSAN HOWARTH & CO AUSTIN SANDERS ROWLAND TILDESLEY & HARRIS A D VARLEY & CO ADAMS TAYLOR A H BROOKS & CO HALSALLS A L HUGHES & CO HALSALLS ABBOTT WALKER & CO ABELS ABOUDI BRADLEY & CO ABRAMS COLLYER HAGUE LAMBERT ADAM DOUGLAS & SON ADAMS & REMERS ADAMS HARRISON ADAMS HARRISON ADAMS HETHERINGTON ADAMS HETHERINGTON ADDISONS ADLAMS ADAMS DELMAR ACKLAM BOND ALAN HODGE SOLICITORS ALAN SIMPSON & CO ALBINSON NAPIER & CO ALDERSON DODDS ALEN-BUCKLEY & CO HUTCHINSON MAINPRICE PASSMORE'S ALISTER PILLING ALKER & BALL BEECHAM PEACOCK ALLENS ALMY & THOMAS AMPHLETTS ANDERSON LONGMORE & HIGHAM ALLINGTON HUGHES ANDREW HILL ANDERSONS ANDERSONS ANDREW C BLUNDY SOLICITOR ANDREW J FENNY & CO ANDREW M FORD INC GW HAMMOND & CO ANDREW THORNE & CO ANTHONY CLARK & CO ANTHONY FOLEY ANTHONY WALTERS & COMPANY APPLEBY HOPE & MATTHEWS ARNOLD DAVIES VINCENT EVANS ARNOLD FOOKS CHADWICK ARNOLD GREENWOOD ANTHONY JACOBS & CO ANTHONY C CARTER ARCHERS ASCROFT WHITESIDE ASKEW BUNTING ASCROFT RAE ASH CLIFFORD ASKEWS ASKEW BUNTING ATHA BARTON & CO ATKINS BASSETT ATKINSON -

ROLL CALL: 2019 Teps

ROLL CALL: 2019 TEPs STEP is delighted to announce that over 600 of our members achieved TEP status in 2019. Full Member status – achievable via three routes – allows exclusive use of the TEP designation and STEP logo, enhancing members’ profile in the industry and promoting their specialist knowledge to both clients and colleagues. NAME BRANCH ORGANISATION Carey Abma Abma STEP Toronto MD Financial Management Camila Abreu STEP Brazil Emma Adkins STEP East Midlands Sarah-Jane Adkins STEP Bristol CVC Solicitors Marwa Akef STEP Montreal Stephen Alexander STEP Jersey Mourant Samera Ali STEP Scotland Miller Hendry Edward Allanby STEP Bermuda Leman Management Limited Hannah Allen STEP Yorkshire Helen Allen STEP Northern Ireland GMcG Group David Allen STEP East Midlands Tinn Criddle Solicitors Jose Alvarez STEP Miami Nicola Alvaro STEP Italy Generali Luxembourg S.A. Ivan Ang STEP Singapore Marisa Anggoro STEP Singapore Sequent Singapore Ltd Marie Antoine STEP Geneva Reliance Trust Company SA Ruth Appleton STEP Gloucestershire and Wiltshire Tayntons (LS) Ltd Gerard Aquilina STEP London Central Cone Marshall Ltd Carlos Arazoza STEP Miami Arazoza & Fernandez-Fraga, PA David Arellano De Figueiredo STEP Curacao Corporate Agents N.V (Corpag Group) Karin Arvidsson STEP Geneva EFG Bank Geneva Kristina Ash STEP Seattle/Pacific Northwest Smith & Zuccarini, PS Fiona Ashmead STEP Suffolk and North Essex Aliah Ashraf STEP Scotland Mitchells Roberton Jacqueline Ashton STEP Yorkshire LCF Barber Titleys Michel Assouad STEP Montreal Josephine Attwood STEP Guernsey Saffery Champness Charlotte Baden-Powell STEP London Central Streathers LLP (Hampstead) Birgit Badke STEP Okanagan BMO Private Banking The Society of Trust and Estate Practitioners is a company limited by guarantee incorporated in England and Wales. -

November 2013 CPD Programme

The Royal Faculty of Procurators in Glasgow September - November 2013 CPD Programme Sponsored by • Special offer – if you book three seminars at the outset you will receive a further seminar within the same programme free of charge (not including the PI Conference; free seminar will be the least expensive). • Unless otherwise stated the seminars will be held in the Royal Faculty Hall. Coffee and biscuits will be available prior to the seminars. • Please do not hesitate to advise us by email ([email protected]) prior to the event, of any questions you wish to ask the various speakers. Otherwise questions will be taken on the night. • Seminar prices for members - £35 for lunchtime seminars, £50 for evening seminars and £100 for ½-day conferences seminar prices for non-members - £50 for lunchtime seminars, £75 for evening seminars and £150 for ½-day conferences In addition there are reduced rates available for trainees, paralegals and unemployed legal practitioners. A number of seminars will be made available as recordings on the Royal Faculty website. For details please see – www.rfpg.org/cpd:recorded-seminars 1. Dean’s Debate: Future Trends for the Provision of Legal Services in Scotland – to merge or not to merge? Austin Lafferty (Partner, Lafferty Law), Gilbert Anderson (Partner, DAC Beachcroft), Bruce Beveridge (President, Law Society of Scotland) to Chair 5 Sept. 2013 Thursday 5.45pm – 7.15pm The Royal Faculty is holding a debate focusing on mergers in Scots Law. In order to get a breadth of different views and opinions heard, we have invited three fantastic participants. Austin Lafferty was President of the Law Society of Scotland until May 2013. -

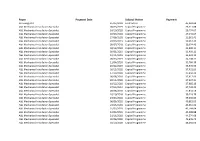

Payee Payment Date Subject Matter Payment

Payee Payment Date Subject Matter Payment 2G Energy Ltd 25/07/2018 Contractors 45,041.88 A&L Mechanical Installation Specialist 06/03/2019 Capital Programme 26,211.88 A&L Mechanical Installation Specialist 24/10/2018 Capital Programme 26,774.67 A&L Mechanical Installation Specialist 02/07/2018 Capital Programme 27,141.67 A&L Mechanical Installation Specialist 27/06/2018 Capital Programme 29,361.42 A&L Mechanical Installation Specialist 20/03/2019 Capital Programme 30,263.40 A&L Mechanical Installation Specialist 09/07/2018 Capital Programme 30,674.40 A&L Mechanical Installation Specialist 03/12/2018 Capital Programme 31,990.11 A&L Mechanical Installation Specialist 09/01/2019 Capital Programme 33,409.12 A&L Mechanical Installation Specialist 12/11/2018 Capital Programme 34,091.10 A&L Mechanical Installation Specialist 06/03/2019 Capital Programme 34,208.32 A&L Mechanical Installation Specialist 11/04/2018 Capital Programme 35,784.39 A&L Mechanical Installation Specialist 20/02/2019 Capital Programme 35,976.95 A&L Mechanical Installation Specialist 26/11/2018 Capital Programme 37,421.00 A&L Mechanical Installation Specialist 17/10/2018 Capital Programme 37,434.42 A&L Mechanical Installation Specialist 06/08/2018 Capital Programme 37,612.66 A&L Mechanical Installation Specialist 28/11/2018 Capital Programme 37,637.21 A&L Mechanical Installation Specialist 19/12/2018 Capital Programme 37,685.16 A&L Mechanical Installation Specialist 27/03/2019 Capital Programme 37,728.29 A&L Mechanical Installation Specialist 28/08/2018 Capital Programme -

Top 100 Pension Schemes 2016

www.professionalpensions.com | December 2016 Top 100 pension schemes 2016 000_PPDCSUPP_1116_cover.indd 1 14/12/2016 10:18 Top 100 pension schemes 2016 Professional Pensions analysed data from the Top 100 Schemes 2016. This is what we found… rofessional Pensions has total value of assets in top 100 Actuarial advisers teamed up with Pension schemes stood at around £860bn at A total of 73 schemes included data Funds Online to bring you the time the data was assembled. on actuarial advisers – with a total a definitive listing of the Of the 78 schemes where of nine advisers represented on Plargest 100 pension schemes in the membership information was actuarial panels. UK (see following pages). available, 7,772,802 – an average of It was noted that several of The data in these tables comes just under 100,000 members per these schemes had multiple from Pension Funds Online as at scheme. actuarial advisers. In total, 31 October 2016. Should you have However, the majority of this however, Willis Towers Watson any queries about any of the infor- membership are now deferred or held a total of 26 appointments mation contained in these pages, pensioner members – with the 67 (34.2%); Aon Hewitt and Hymans please contact Neil Blain at neil. schemes providing data in this Robertson each held 13 appoint- [email protected]. To read area having a total of 1,947,672 ments (17.1% each); Mercer held Pension Funds Online in full, visit: active members. The 78 schemes 11 appointments (14.5%); Barnett www.pensionfundsonline.co.uk. providing deferred data had a total Waddingham held 6 appointments of 2,746,188 deferred members and (7.9%); the Government Actuary’s The schemes the 77 schemes with pensioner Department held three appoint- Professional Pensions has analysed data had a total of 2,995,503 ments (3.9%); Punter Southall the top 100 data, finding that the pensioner members. -

New Lawyers Finding Their Career Plans Stalled by the Recession Should Not Despair – Say Those Who Came Through the Last Slump in 2008 Scottish Land Law

Radical approach to Law and Tech Conference: The Expert Witness children’s rights highlights of a virtual event Index 2020 P.16 P.18 P.49 Journal of the Law Society of Scotland Volume 65 Number 10 – October 2020 Up in smoke? New lawyers finding their career plans stalled by the recession should not despair – say those who came through the last slump in 2008 Scottish Land Law Publishing under the auspices of the Scottish Universities Law Institute, the second volume to this well-established and respected work is a thoroughly updated and comprehensive account of Scottish land law. It brings together material of significant practical importance in relation to the rights and obligations inherent in the ownership of land. Key legislation includes: • The Conveyancing and Feudal Reform (Scotland) Act 1970 • The Title Conditions (Scotland) Act 2003 3rd Edition, Volume 2 • The Land Reform (Scotland) Act 2003 October 2020 | £100 9780414017832 Continuing from Volume I, the content of Volume II includes: Chapter 19: General Principles of Security Rights Chapter 20: Standard Securities PLACE YOUR ORDER TODAY Chapter 21: Floating Charges sweetandmaxwell.co.uk +44 (0)345 600 9355 Chapter 22: Involuntary Heritable Securities Chapter 23: Title Conditions and other Burdens Chapter 24: Real Burdens Chapter 25: Servitudes Chapter 26: Judicial Variation and Discharge of Title Conditions Chapter 27: Public Access Rights Chapter 28: Nuisance and other Delicts Chapter 29: Social Control of Land Use Chapter 30: Compulsory Acquisition Chapter 31: Community Rights to Buy REUTERS/Russell Cheyne TR1218702/08-20 Click here to see Peter’s welcome Scottish Land Law message Publishing under the auspices of the Scottish Universities Law Institute, the second volume Publishers Editor to this well-established and respected work is a thoroughly updated and comprehensive The Law Society of Scotland Email > [email protected] Atria One, 144 Morrison Street, account of Scottish land law.