Chinese Equity

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

China Multi Asset Income Fund - 3-Year Class USD Fund Volatility

Principal China Multi Asset Income Fund - 3-year Class USD Fund Volatility 31 August 2021 10.83Low Lipper Analytics 15 Aug 2021 Fund Objective Fund Performance The Fund aims to provide income and 60% moderate capital growth through investments in one CIS, which invests 50% primarily in a diversified portfolio of securities related to China. 40% Currency: ISIN Code: 30% USD MYU1002GD004 20% Bloomberg Ticker: CIMCMUS MK 10% 0% Fund Information 7 7 8 8 8 8 8 8 9 9 9 9 9 9 0 0 0 0 0 0 1 1 1 1 1 -1 -1 -1 -1 -1 -1 -1 -1 -1 -1 -1 -1 -1 -1 -2 -2 -2 -2 -2 -2 -2 -2 -2 -2 -2 t c b r n g t c b r n l p v n r y l p v n b r n g c e e p u u c e e p u Ju e o a a a Ju e o a e p u u - 10% O D F A J A O D F A J S N J M M S N J F A J A Domicile Malaysia - 20% Base Currency US Dollar (USD) Fund Inception 3 July 2017 Fund Benchmark Benchmark The Fund adheres to the Past performance does not guarantee future results. Asset allocation and diversification do not ensure a profit or protect against a loss. benchmark of the Target Fund for performance Cumulative Performance (%) comparison. The Since YTD 1 Month 3 Months 6 Months 1-Year 3-Year 5-Year Inception benchmark of the Target Fund -8.70 -0.21 -9.33 -10.95 -1.42 17.94 N/A 19.79 Fund is 50% MSCI China Net + 50% Markit Benchmark/Target Return -4.47 0.22 -7.23 -7.95 2.29 22.31 N/A 33.59 iBoxx Asia Local Bond Index China Offshore for Calendar Year Returns (%) 2020 2019 2018 2017 2016 2015 comparison purpose. -

Hang Seng Indexes Announces Index Review Results

14 August 2020 Hang Seng Indexes Announces Index Review Results Hang Seng Indexes Company Limited (“Hang Seng Indexes”) today announced the results of its review of the Hang Seng Family of Indexes for the quarter ended 30 June 2020. All changes will take effect on 7 September 2020 (Monday). 1. Hang Seng Index The following constituent changes will be made to the Hang Seng Index. The total number of constituents remains unchanged at 50. Inclusion: Code Company 1810 Xiaomi Corporation - W 2269 WuXi Biologics (Cayman) Inc. 9988 Alibaba Group Holding Ltd. - SW Removal: Code Company 83 Sino Land Co. Ltd. 151 Want Want China Holdings Ltd. 1088 China Shenhua Energy Co. Ltd. - H Shares The list of constituents is provided in Appendix 1. The Hang Seng Index Advisory Committee today reviewed the fast expanding innovation and new economy sectors in the Hong Kong capital market and agreed with the proposal from Hang Seng Indexes to conduct a comprehensive study on the composition of the Hang Seng Index. This holistic review will encompass various aspects including, but not limited to, composition and selection of constituents, number of constituents, weightings, and industry and geographical representation, etc. The underlying aim of the study is to ensure the Hang Seng Index continues to serve as the most representative and important benchmark of the Hong Kong stock market. Hang Seng Indexes will report its findings and propose recommendations to the Advisory Committee within six months. The number of constituents of the Hang Seng Index may increase during this period. Hang Seng Indexes Announces Index Review Results /2 2. -

Greater China 2019

IR Magazine Awards – Greater China 2019 Winners and nominees AWARDS BY RESEARCH Best overall investor relations (large cap) ANTA Sports Products China Resources Beer WINNER China Telecom China Unicom Shenzhou International Group Holdings Best overall investor relations (small to mid-cap) Alibaba Pictures Group Far East Consortium International WINNER Health and Happiness H&H International Holdings Li-Ning NetDragon Websoft Holdings Best investor relations officer (large cap) ANTA Sports Products Suki Wong Cathay Financial Holdings Yajou Chang & Sophia Cheng China Resources Beer Vincent Tse WINNER China Telecom Lisa Lai China Unicom Jacky Yung Best investor relations officer (small to mid-cap) Agile Group Holdings Samson Chan BizLink Holding Tom Huang Far East Consortium International Venus Zhao WINNER Li-Ning Rebecca Zhang Yue Yuen Industrial (Holdings) Olivia Wang Best IR by a senior management team Maggie Wu, CFO & Daniel Zhang, Alibaba Group CEO Tomakin Lai Po-sing, CFO & China Resources Beer Xiaohai Hou, CEO Xiaochu Wang, CEO & Zhu WINNER China Unicom Kebing, CFO Wai Hung Boswell Cheung, CFO & Far East Consortium International David Chiu, Chairman & CEO Ma Jianrong, CEO & Cun Bo Wang, Shenzhou International Group Holdings CFO AWARDS BY REGION Best in region: China Alibaba Pictures Group ANTA Sports Products China Resources Beer WINNER China Telecom China Unicom Shenzhou International Group Holdings Best in region: Hong Kong AIA Group Far East Consortium International WINNER Health and Happiness H&H International Holdings Yue Yuen -

Biologics CDMO Trends and Opportunities in China

Volume 21 Issue 3 | July/August/September 2020 TM SHOW ISSUE CPhI: Festival of Pharma BIO Investor Forum - Digital 2020 ISPE Annual Meeting & Expo - Virtual CONTRACT MANUFACTURING Biologics CDMO Trends and Opportunities in China SUPPLY CHAIN Building Future-Proof Supply Chains with Graph Technology CLINICAL TRIALS Decentralization: A Direct Approach to Clinical Trials www.pharmoutsourcing.com Large enough to deliver, small enough to care. Balancing... ANALYTICAL SERVICES With over seven decades of experience, Mission Pharmacal Liquids has mastered the equilibrium of expertise and efficiency. DEVELOPMENT Our mid-sized advantage allows flexibility, responsiveness, and unmatched support in executing your vision while MANUFACTURING Semi-Solids providing a wide range of specialized services for products at any stage of their life cycle. Regardless of REGULATORY SUPPORT Tablets the scope and size of your project, we will create a custom program to meet your individual requirements and PACKAGING exceed expectations. Delivering on our ability to produce small or large scale, while providing personalized service and attention to detail on any sized project. missionpharmacal.com Contact us: [email protected] Copyright © 2020 Mission Pharmacal Company. All rights reserved. CDM-P2011912 A HEALTHY WORLD WITH AJINOMOTO BIO-PHARMA SERVICES, YOU HAVE THE POWER TO MAKE. To make your vision a reality. To make your program a sucess. To make a positive difference in the world. Your programs deserve the most comprehensive suite of CDMO services available, and Ajinomoto Bio-Pharma Services has the Power to Make your therapeutic vision a reality - from preclinical through commerical production. CDMO SERVICES: Small Molecules Large Molecules Process Development Oligos & Peptides High Potency & ADC Aseptic Fill Finish WHAT DO YOU WANT TO MAKE? www.AjiBio-Pharma.com FROM THE EDITOR Editor's Message Effi ciency: One Step at a Time I like to think that in a previous life (or maybe in a future life) I was an effi ciency expert. -

HSBC Emerging Market Sustainable Equity UCITS ETF

Sustainably Invested MX-PE HSBC ETFs PLC - HSBC Emerging Market Sustainable Equity UCITS ETF HSEF LN Aug 31 2021 Fund IE00BKY59G90 Aug 31 2021 Fund Objective and Strategy Investment Objective The Fund aims to track as closely as possible the returns of the FTSE Emerging ESG Low Carbon Select Index (the “Index”). The Fund will invest in or gain exposure to shares of companies which make up the Index. Investment Policy The Index seeks to achieve a reduction in carbon emissions and fossil fuel reserves exposure, improvement of the FTSE Russell ESG rating and also applies the United Nations Global Compact exclusionary criteria.The Fund will be passively managed and will aim to invest in the shares of the companies in generally the same proportion as in the Index. However, there may be circumstances when it is not possible or practical for the Fund to invest in all constituents of the Index. The Fund can gain exposure by using other investments such as depositary receipts, derivatives or funds.The Fund may invest up to 35% in securities from a single issuer during exceptional market conditions.The Fund may invest up to 10% in funds and up to 10% in total return swaps and contracts for difference.See the Prospectus for a full description of the investment objectives and derivative usage. Since Inception Performance (%) Fund Details UCITS V Compliant Yes 130 Fund Reference Benchmark 125 Distribution Type Accumulating 120 2 115 Ongoing Charge Figure 0.180% 110 105 Share Class Base Currency USD 100 95 90 Domicile Ireland ISIN IE00BKY59G90 Share -

HSBC Global Investment Funds CHINESE EQUITY Monthly Report 31 August 2021 | Share Class IC

HSBC Global Investment Funds CHINESE EQUITY Monthly report 31 August 2021 | Share class IC Share Class Details Investment objective Key metrics The Fund aims to provide long term capital growth by investing in a portfolio of Chinese shares. NAV per Share USD 163.81 Performance 1 month -0.91% Investment strategy Volatility 3 years 21.14% Fund facts In normal market conditions, the Fund will invest at least 90% of its assets in shares (or securities UCITS V compliant Yes similar to shares) of companies of any size that are based in, or carry out the larger part of their business activities in, China, including Hong Kong SAR. The Fund can invest up to 70% in China Dividend treatment Accumulating A and China B-shares. For China A-shares, up to 70% through the Shanghai-Hong Kong Stock Dealing frequency Daily Connect and/or the Shenzhen-Hong Kong Stock Connect, and up to 50% in CAAPs. The Fund Valuation Time 17:00 Luxembourg may invest up to 10% of its assets in other funds, including HSBC funds. The Fund will not invest more than 10% of its assets in Real Estate Investment Trusts. See the Prospectus for a full Share Class Base Currency USD description of the investment objectives and derivative usage. Domicile Luxembourg Inception date 27 July 2005 Main risks Fund Size USD 1,139,298,382 Reference 100% MSCI China 10/40 • The Fund's unit value can go up as well as down, and any capital invested in the Fund may benchmark Net be at risk. • The value of investible securities can change over time due to a wide variety of factors, Managers Caroline Yu Maurer including but not limited to: political and economic news, government policy, changes in Fees and expenses demographics, cultures and populations, natural or human-caused disasters etc. -

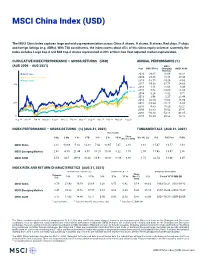

MSCI China Index (USD)

MSCI China Index (USD) The MSCI China Index captures large and mid cap representation across China A shares, H shares, B shares, Red chips, P chips and foreign listings (e.g. ADRs). With 730 constituents, the index covers about 85% of this China equity universe. Currently, the index includes Large Cap A and Mid Cap A shares represented at 20% of their free float adjusted market capitalization. CUMULATIVE INDEX PERFORMANCE — GROSS RETURNS (USD) ANNUAL PERFORMANCE (%) (AUG 2006 – AUG 2021) MSCI Year MSCI China Emerging MSCI ACWI Markets MSCI China 2020 29.67 18.69 16.82 MSCI Emerging Markets 2019 23.66 18.88 27.30 MSCI ACWI 2018 -18.75 -14.24 -8.93 400 2017 54.33 37.75 24.62 366.92 2016 1.11 11.60 8.48 324.55 2015 -7.62 -14.60 -1.84 2014 8.26 -1.82 4.71 2013 3.96 -2.27 23.44 252.73 2012 23.10 18.63 16.80 200 2011 -18.24 -18.17 -6.86 2010 4.83 19.20 13.21 2009 62.63 79.02 35.41 2008 -50.83 -53.18 -41.85 50 2007 66.24 39.82 12.18 Aug 06 Nov 07 Feb 09 May 10 Aug 11 Nov 12 Feb 14 May 15 Aug 16 Nov 17 Feb 19 May 20 Aug 21 INDEX PERFORMANCE — GROSS RETURNS (%) (AUG 31, 2021) FUNDAMENTALS (AUG 31, 2021) ANNUALIZED Since 1 Mo 3 Mo 1 Yr YTD 3 Yr 5 Yr 10 Yr Dec 31, 1992 Div Yld (%) P/E P/E Fwd P/BV MSCI China 0.01 -13.69 -5.00 -12.18 7.42 10.97 7.47 2.18 1.61 15.47 13.57 1.91 MSCI Emerging Markets 2.65 -4.00 21.49 3.07 10.25 10.80 5.22 7.75 2.07 15.98 13.07 2.00 MSCI ACWI 2.53 4.67 29.18 16.24 14.91 14.88 11.86 8.88 1.71 22.54 18.46 3.07 INDEX RISK AND RETURN CHARACTERISTICS (AUG 31, 2021) ANNUALIZED STD DEV (%) 2 SHARPE RATIO 2 , 3 MAXIMUM DRAWDOWN Turnover Since 1 3 Yr 5 Yr 10 Yr 3 Yr 5 Yr 10 Yr Dec 31, (%) Period YYYY-MM-DD (%) 1992 MSCI China 8.79 21.43 19.19 20.89 0.38 0.57 0.42 0.14 88.63 1993-12-31—2001-09-12 MSCI Emerging Markets 8.45 19.23 16.52 17.57 0.54 0.63 0.34 0.33 65.14 2007-10-29—2008-10-27 MSCI ACWI 3.17 17.93 14.46 13.77 0.80 0.95 0.83 0.47 58.06 2007-10-31—2009-03-09 1 Last 12 months 2 Based on monthly gross returns data 3 Based on ICE LIBOR 1M The China mainland equity market is comprised of A, B, H, Red chip and P chip share classes. -

Ireland Asia Report Ireland Asia Report Table of Contents

Ireland Asia Report Ireland Asia Report Table of Contents Ireland as an FDI location for Asian companies Martin Shanahan, CEO, IDA Ireland 2 Ireland’s open economy and its role in the Future of Global Trade Alan Duffy, CEO & Head of Banking, HSBC Ireland 4 An ideal gateway to Europe William Wu, Managing Director, Head of Corporate Banking Yangtze Delta and Western China at HSBC China 7 Asia Market Profiles 8 Mainland China and WuXi Biologics 8 Hong Kong and Goshawk 10 Japan and Indeed.com 12 India and NIIT 14 South Korea and SK Biotek 16 ASEAN and Keppel 18 The Ireland advantage for funds 20 Ireland – a well-rounded destination for people and investment, Chen Tian, Head of China Desk, Continental Europe, Commercial Banking, HSBC 22 Page 1 Ireland Asia Report Ireland Asia Report Ireland as an FDI location for Asian Companies Yet although there may be some unpredictable times Martin Shanahan, ahead, I remain confident in Ireland’s competitiveness CEO IDA Ireland and attractiveness as a place to do business. From regular recent contact between IDA Ireland and many of the leading multinationals here, I know how resilient these companies’ Irish operations are. I believe the supports that Ireland, as a nation, puts in place to welcome international investment are a key factor in this durability. The disruption to supply chains brought about by the We are all still coming to terms with crisis has highlighted how important it is to manage risk and avoid overdependency on a single source. If the shock that the Covid-19 crisis we apply this to an Irish context, it means not relying has delivered to our economy and on any one geographical region or industry sector for society. -

China's Healthcare System Uncovered

China’s Healthcare System Uncovered Theme Focus: Online Medicine and Potential Beneficiaries of the COVID-19 Virus Pandemic Q1 2020 KURE Quarterly Earnings Report [email protected] +1 (212) 933 0393 [email protected] +1 (212) 933 0393 Table of Contents KURE Standard Performance 3 China's Healthcare System Uncovered 4 Key Points on China Healthcare Sector 5 China Healthcare Sector Key Charts 6-7 Q1 2020 Performance Review 8 Online Medicine and Beneficiaries of the COVID-19 9-12 Virus Pandemic Overview 12-17 Top 10 KURE Holdings: Quarterly Earnings Update 18-26 Jiangsu Hengrui Med 18 Shenzhen Mindray 19 Wuxi Biologics 20-21 CSPC Pharmaceutical Group 21-22 Sino Biopharmaceutical 22-23 WuXi AppTec 23 Aier Eye Hospital Group 24 Yunnan Baiyao Group 25 Changchun High & New Tech 25 Innovent Biologics 26 Potential Risks 27-29 Citations 30 Definitions 30 kraneshares.com 2 [email protected] +1 (212) 933 0393 KraneShares MSCI All China Health Care Index ETF (Ticker: KURE) Standard Performance Cumulative % Data as of: 03/31/2020 Fund NAV Closing Price Index 1 Month -3.84% -5.34% -3.85% 3 Month 2.10% 3.03% 2.20% 6 Month 12.82% 13.26% 13.20% Since Inception -4.22% -4.26% -3.51% Avg Annualized % Data as of: 03/31/2020 Fund NAV Closing Price Index 1 Year 6.95% 7.58% 7.80% Since Inception -1.97% -1.99% -1.64% KURE’s gross expense ratio is 0.79%. Inception Date: 1/31/2018. The performance data quoted represents past performance. Past performance does not guarantee future results. -

Non-Collateralised Structured Products CREDIT SUISSE AG

Announcement on Valuation of Residual Value Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited (the stock exchange) take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. Non-Collateralised Structured Products Notice of Valuation of Residual Value of European Style (Cash Settled) Category R Callable Bull/Bear Contracts (the CBBCs) issued by CREDIT SUISSE AG (incorporated with limited liability under the laws of Switzerland) Sponsor/Manager CREDIT SUISSE (HONG KONG) LIMITED Terms not defined in this announcement have the same meaning as defined in the general conditions and the product conditions of the CBBCs (together, the conditions). Credit Suisse AG (the issuer) announces that under the conditions, following the occurrence of a mandatory call event (MCE) in respect of the CBBCs described in the table below in the pre- opening session or the continuous trading session or the closing auction session (as the case may be) of the stock exchange at the time (MCE time) and on the date (MCE date) specified in the table below, the amount of the residual value in respect of the CBBCs has been determined as follows: Stock Type MCE MCE Underlying Issue Size Number of Entitlement Board Lot Strike Maximum/ Residual Value Code Time Date (CBBCs) CBBC(s) (CBBCs) Price Minimum Trade per Board Lot per (HK$) Price (HK$) (HK$) Entitlement 52208 Bull 11:02:46 6 Jul 2021 WuXi Biologics (Cayman) Inc. -

HSBC Global Investment Funds - Hong Kong Equity

BM-BE HSBC Global Investment Funds - Hong Kong Equity Share Class PD 31 Jul 2021 PD LU0011817854 31/07/2021 Fund Objective and Strategy Investment Objective The Fund aims to provide long term capital growth by investing in a portfolio of Hong Kong SAR shares. Investment Policy In normal market conditions, the Fund will invest at least 90% of its assets in shares (or securities similar to shares) of companies of any size that are based in, or carry out the larger part of their business activities in, Hong Kong SAR.The Fund can invest up to 20% in China A and China B-shares. For China A-shares, up to 20% through the Shanghai-Hong Kong Stock Connect and/or the Shenzhen-Hong Kong Stock Connect, and up to 10% in CAAPs.The Fund may invest up to 10% in other funds, including HSBC funds.The Fund will not invest more than 10% in Real Estate Investment Trusts.See the Prospectus for a full description of the investment objectives and derivative usage. Share Class Details UCITS V Compliant Yes Performance (%) YTD 1M 3M 1Y 3Y¹ 5Y¹ Distribution Type Distributing PD -8.41 -9.67 -8.07 6.15 4.75 8.41 Distribution Frequency Annually Reference Dividend ex-date 08 Jul 2021 -5.59 -10.58 -10.06 9.13 3.25 9.08 Benchmark Dividend Yield 2 0.26% Last Paid Dividend 0.3857 Rolling Dealing Frequency Daily 31 Jul 2020-31 31 Jul 2019- 31 Jul 2018- 31 Jul 2017- 31 Jul 2016- Performance Valuation Time 17:00 Luxembourg Jul 2021 31 Jul 2020 31 Jul 2019 31 Jul 2018 31 Jul 2017 (%) Min. -

Altimeo Asset Management, Et Al. V. Wuxi Pharmatech (Cayman) Inc., Et Al. 19-CV-01654-Consolidated Amended Class Action Complain

Case 1:19-cv-01654-AJN Document 39 Filed 08/05/19 Page 1 of 114 UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK ALTIMEO ASSET MANAGEMENT, Case No. 1:19-cv-01654-AJN Individually and On Behalf of All Others Similarly Situated, CLASS ACTION Plaintiff, CONSOLIDATED AMENDED CLASS ACTION COMPLAINT v. JURY TRIAL DEMANDED WUXI PHARMATECH (CAYMAN) INC., GE LI, EDWARD HU, NING ZHAO, XIAOZHONG LIU, ZHAOHUI ZHANG, G&C PARTNERSHIP L.P., ABG II-WX LIMITED, BOYU CAPITAL FUND II, L.P., HILLHOUSE CAPITAL FUND II, L.P., PING AN LIFE INSURANCE COMPANY OF CHINA. LTD., TEMASEK LIFE SCIENCES PRIVATE LIMITED, G&C IV LIMITED, YINFU CAPITAL MANAGEMENT CO., YUNFENG II WX LIMITED, SEQUOIA CAPITAL CHINA GROWTH FUND III, L.P., CONSTANT CYPRESS LIMITED, and SPDB INTERNATIONAL HOLDINGS LIMITED, Defendants. Case 1:19-cv-01654-AJN Document 39 Filed 08/05/19 Page 2 of 114 TABLE OF CONTENTS I. NATURE OF THE ACTION ............................................................................................. 1 II. JURISDICTION AND VENUE ......................................................................................... 6 III. PARTIES ............................................................................................................................ 7 A. Lead Plaintiff .......................................................................................................... 7 B. Defendants .............................................................................................................. 7 1. The Individual Defendants .........................................................................