On the Upswing

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

PUBLIC NOTICE Federal Communications Commission 445 12Th St., S.W

PUBLIC NOTICE Federal Communications Commission 445 12th St., S.W. News Media Information 202 / 418-0500 Internet: https://www.fcc.gov Washington, D.C. 20554 TTY: 1-888-835-5322 DA 19-275 Released: April 10, 2019 MEDIA BUREAU ESTABLISHES PLEADING CYCLE FOR APPLICATIONS TO TRANSFER CONTROL OF NBI HOLDINGS, LLC, AND COX ENTERPRISES, INC., TO TERRIER MEDIA BUYER, INC., AND PERMIT-BUT-DISCLOSE EX PARTE STATUS FOR THE PROCEEDING MB Docket No. 19-98 Petition to Deny Date: May 10, 2019 Opposition Date: May 28, 2019 Reply Date: June 4, 2019 On March 4, 2019, Terrier Media Buyer, Inc. (Terrier Media), NBI Holdings, LLC (Northwest), and Cox Enterprises, Inc. (Cox) (jointly, the Applicants) filed applications with the Federal Communications Commission (Commission) seeking consent to the transfer of control of Commission licenses through two separate transactions.1 First, Terrier Media and Northwest seek consent for Terrier Media to acquire companies owned by Northwest holding the licenses of full-power broadcast television stations, low-power television stations, and TV translator stations (the Northwest Applications). Next, Terrier Media and Cox seek consent for Terrier Media to acquire companies owned by Cox holding the licenses of full-power broadcast television stations, low-power television stations, TV translator stations, and radio stations (the Cox Applications and, jointly with the NBI Applications, the Applications).2 Pursuant to a Purchase Agreement between Terrier Media and the equity holders of Northwest dated February 14, 2019, Terrier Media would acquire 100% of the interest in Northwest.3 Pursuant to a separate Purchase Agreement between Terrier Media and Cox and affiliates of Cox, Terrier Media would acquire the companies owning all of Cox’s television stations and the licenses and other assets of four of Cox’s radio stations.4 The Applicants propose that Terrier Media, which is a newly created company, will become the 100% indirect parent of the licensees listed in the Attachment. -

Apollo Global Management Appoints Tetsuji Okamoto to Head Private Equity Business in Japan

Apollo Global Management Appoints Tetsuji Okamoto to Head Private Equity Business in Japan NEW YORK, NY – December 5, 2019 – Apollo Global Management, Inc. (NYSE: APO) (together with its consolidated subsidiaries, “Apollo”) today announced the appointment of Tetsuji Okamoto as a Partner, Head of Japan, leading Apollo Private Equity’s efforts in Japan. Mr. Okamoto will play a lead role in building Apollo’s Private Equity business in Japan, including originating and executing deals and identifying cross-platform opportunities. He will report to Steve Martinez, Senior Partner, Head of Asia Pacific, and will begin in this newly created role on December 9, 2019. “This appointment and the new role we’ve created is a reflection of the importance we place on Japan and the opportunities we see in the wider region for growth and diversification,” Apollo’s Co-Presidents, Scott Kleinman and James Zelter said in a joint statement. “Tetsuji’s addition signals Apollo’s meaningful long-term commitment to expanding its presence in the Japanese market, which we view as a key area of investment focus as we seek to build value and drive growth for Japanese corporations and our investors and limited partners,” Mr. Martinez added. Mr. Okamoto, 39, brings more than 17 years of industry experience to the Apollo platform and the Private Equity investing team. Most recently, Mr. Okamoto was a Managing Director at Bain Capital, where he was a member of the Asia Pacific Private Equity team for eleven years, responsible for overseeing execution processes for new deals and existing portfolio companies in Japan. At Bain Capital he was also a leader on the Capital Markets team covering Asia. -

How Will Financial Services Private Equity Investments Fare in the Next Recession?

How Will Financial Services Private Equity Investments Fare in the Next Recession? Leading funds are shifting to balance-sheet-light and countercyclical investments. By Tim Cochrane, Justin Miller, Michael Cashman and Mike Smith Tim Cochrane, Justin Miller, Michael Cashman and Mike Smith are partners with Bain & Company’s Financial Services and Private Equity practices. They are based, respectively, in London, New York, Boston and London. Copyright © 2019 Bain & Company, Inc. All rights reserved. How Will Financial Services Private Equity Investments Fare in the Next Recession? At a Glance Financial services deals in private equity have grown on the back of strong returns, including a pooled multiple on invested capital of 2.2x in recent years, higher than all but healthcare and technology deals. With a recession increasingly likely during the next holding period, PE funds need to develop plans to weather any storm and potentially improve their competitive position during and after the downturn. Many leading funds are investing in balance-sheet-light assets enabled by technology and regulatory change. Diligences now should test target companies under stressful economic scenarios and lay out a detailed value-creation plan, including how to mobilize quickly after acquisition. Financial services deals by private equity funds have had a strong run over the past few years, with deal value increasing significantly in Europe and the US(see Figure 1). Returns have been strong as well. Global financial services deals realized a pooled multiple on invested capital of 2.2x from 2009 through 2015, higher than all but healthcare and technology deals (see Figure 2). -

Form 3 FORM 3 UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D.C

SEC Form 3 FORM 3 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 OMB APPROVAL INITIAL STATEMENT OF BENEFICIAL OWNERSHIP OF OMB Number: 3235-0104 Estimated average burden SECURITIES hours per response: 0.5 Filed pursuant to Section 16(a) of the Securities Exchange Act of 1934 or Section 30(h) of the Investment Company Act of 1940 1. Name and Address of Reporting Person* 2. Date of Event 3. Issuer Name and Ticker or Trading Symbol Requiring Statement EASTMAN KODAK CO [ EK ] Chen Herald Y (Month/Day/Year) 09/29/2009 (Last) (First) (Middle) 4. Relationship of Reporting Person(s) to Issuer 5. If Amendment, Date of Original Filed C/O KOHLBERG KRAVIS ROBERTS & (Check all applicable) (Month/Day/Year) CO. L.P. X Director 10% Owner Officer (give title Other (specify 2800 SAND HILL ROAD, SUITE 200 below) below) 6. Individual or Joint/Group Filing (Check Applicable Line) X Form filed by One Reporting Person (Street) MENLO Form filed by More than One CA 94025 Reporting Person PARK (City) (State) (Zip) Table I - Non-Derivative Securities Beneficially Owned 1. Title of Security (Instr. 4) 2. Amount of Securities 3. Ownership 4. Nature of Indirect Beneficial Ownership Beneficially Owned (Instr. 4) Form: Direct (D) (Instr. 5) or Indirect (I) (Instr. 5) Table II - Derivative Securities Beneficially Owned (e.g., puts, calls, warrants, options, convertible securities) 1. Title of Derivative Security (Instr. 4) 2. Date Exercisable and 3. Title and Amount of Securities 4. 5. 6. Nature of Indirect Expiration Date Underlying Derivative Security (Instr. 4) Conversion Ownership Beneficial Ownership (Month/Day/Year) or Exercise Form: (Instr. -

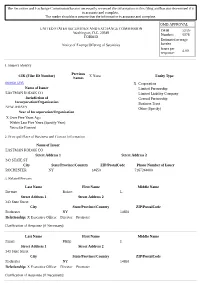

The Securities and Exchange Commission Has Not Necessarily Reviewed the Information in This Filing and Has Not Determined If It Is Accurate and Complete

The Securities and Exchange Commission has not necessarily reviewed the information in this filing and has not determined if it is accurate and complete. The reader should not assume that the information is accurate and complete. OMB APPROVAL UNITED STATES SECURITIES AND EXCHANGE COMMISSION OMB 3235- Washington, D.C. 20549 Number: 0076 FORM D Estimated average Notice of Exempt Offering of Securities burden hours per 4.00 response: 1. Issuer's Identity Previous CIK (Filer ID Number) X None Entity Type Names 0000031235 X Corporation Name of Issuer Limited Partnership EASTMAN KODAK CO Limited Liability Company Jurisdiction of General Partnership Incorporation/Organization Business Trust NEW JERSEY Other (Specify) Year of Incorporation/Organization X Over Five Years Ago Within Last Five Years (Specify Year) Yet to Be Formed 2. Principal Place of Business and Contact Information Name of Issuer EASTMAN KODAK CO Street Address 1 Street Address 2 343 STATE ST City State/Province/Country ZIP/PostalCode Phone Number of Issuer ROCHESTER NY 14650 7167244000 3. Related Persons Last Name First Name Middle Name Berman Robert L. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Faraci Philip J. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Haag Joyce P. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Kruchten Brad W. -

TRS Contracted Investment Managers

TRS INVESTMENT RELATIONSHIPS AS OF DECEMBER 2020 Global Public Equity (Global Income continued) Acadian Asset Management NXT Capital Management AQR Capital Management Oaktree Capital Management Arrowstreet Capital Pacific Investment Management Company Axiom International Investors Pemberton Capital Advisors Dimensional Fund Advisors PGIM Emerald Advisers Proterra Investment Partners Grandeur Peak Global Advisors Riverstone Credit Partners JP Morgan Asset Management Solar Capital Partners LSV Asset Management Taplin, Canida & Habacht/BMO Northern Trust Investments Taurus Funds Management RhumbLine Advisers TCW Asset Management Company Strategic Global Advisors TerraCotta T. Rowe Price Associates Varde Partners Wasatch Advisors Real Assets Transition Managers Barings Real Estate Advisers The Blackstone Group Citigroup Global Markets Brookfield Asset Management Loop Capital The Carlyle Group Macquarie Capital CB Richard Ellis Northern Trust Investments Dyal Capital Penserra Exeter Property Group Fortress Investment Group Global Income Gaw Capital Partners AllianceBernstein Heitman Real Estate Investment Management Apollo Global Management INVESCO Real Estate Beach Point Capital Management LaSalle Investment Management Blantyre Capital Ltd. Lion Industrial Trust Cerberus Capital Management Lone Star Dignari Capital Partners LPC Realty Advisors Dolan McEniry Capital Management Macquarie Group Limited DoubleLine Capital Madison International Realty Edelweiss Niam Franklin Advisers Oak Street Real Estate Capital Garcia Hamilton & Associates -

Bain, Ares Moves Stoke Alts Fund Arms Race

Bain, Ares Moves Stoke Alts Fund Arms Race By Tom Stabile February 15, 2017 Bain Capital, Ares Management, and various private equity peers have cranked up their efforts to reach retail investors through a wave of new products and partnerships in the increasingly active non-traded registered fund marketplace. The firms have built up their presence in the market for non-traded business development company (BDC), real estate investment trust (REIT), closed-end, and interval funds over the past year through a mix of new products, joint ventures, acquisitions, and subadvisory mandates. The scrum in the past year also has included private equity managers such as Blackstone Group, Apollo Global Management, and Providence Equity Partners; real estate fund managers Rialto Capital Management and Colony NorthStar; and hedge funds such as Magnetar Capital and Och-Ziff Capital Management. And they are often partnering with active players in the non-traded registered alts fund business, such as FS Investments, CION Investments, and Griffin Capital, each of which has stepped up new product efforts. Blackstone, Apollo, KKR, and Carlyle Group had established footholds in this market in recent years through earlier rounds of partnerships, but the range of new moves – and addition of peer firms to the fray – has created a bustle. “There continues to be a retail invasion of the market by these big [managers],” says Rajib Chanda, a partner at Simpson, Thacher & Bartlett who specializes in registered fund law. “There definitely has been a renewed interest in the interval funds structure.” The non-traded registered product market’s earlier push several years ago largely involved establishing broader fund of funds-style structures, but now there is much more activity on single funds and narrower investment options, Chanda says. -

ANNUAL REVIEW 2017 Land of the Giants Cycle-Tested Credit Expertise Extensive Market Coverage Comprehensive Solutions Relative Value Focus

ANNUAL REVIEW 2017 Land of the giants Cycle-Tested Credit Expertise Extensive Market Coverage Comprehensive Solutions Relative Value Focus Ares Management is honored to be recognized as Lender of the Year in North America for the fourth consecutive year as well as Lender of the Year in Europe Lender of the year in Europe Ares Management, L.P. (NYSE: ARES) is a leading global alternative asset manager with approximately $106 billion of AUM1 and offices throughout the United States, Europe, Asia and Australia. With more than $70 billion in AUM1 and approximately 235 investment professionals, the Ares Credit Group is one of the largest global alternative credit managers across the non-investment grade credit universe. Ares is also one of the largest direct lenders to the U.S. and European middle markets, operating out of twelve office locations in both geographies. Note: As of December 31, 2017. The performance, awards/ratings noted herein may relate only to selected funds/strategies and may not be representative of any client’s given experience and should not be viewed as indicative of Ares’ past performance or its funds’ future performance. 1. AUM amounts include funds managed by Ivy Hill Asset Management, L.P., a wholly owned portfolio company of Ares Capital Corporation and a registered investment adviser. learn more at: www.aresmgmt.com | www.arescapitalcorp.com The battle of the brands the US market on page 80, advisor Hamilton TOBY MITCHENALL Lane said it had received a record number EDITOR'S of private placement memoranda in 2017 – ISSN 1474–8800 LETTER MARCH 2018 around 800 – and that this, combined with Senior Editor, Private Equity faster fundraising processes, has made it dif- Toby Mitchenall, Tel: +44 207 566 5447 [email protected] ficult to some investors to make considered Special Projects Editor decisions. -

Bain Capital Distressed and Special Situations 2019 (A), LP

COMMONWEALTH OF PENNSYLVANIA PUBLIC SCHOOL EMPLOYEES’ RETIREMENT SYSTEM Public Investment Memorandum Bain Capital Distressed and Special Situations 2019 (A), L.P. High Yield/Private Credit Commitment James F. Del Gaudio Senior Portfolio Manager April 22, 2019 COMMONWEALTH OF PENNSYLVANIA PUBLIC SCHOOL EMPLOYEES’ RETIREMENT SYSTEM Recommendation: PSERS Investment Professionals, together with Hamilton Lane Advisors, L.L.C. (“Hamilton Lane”), recommend the Board commit up to $200 million to Bain Capital Distressed and Special Situations 2019 (A), L.P. (the “Fund”, or “DSS 19”). Bain Capital Credit, LP (“Bain” or the “Firm”) is seeking to raise their third dedicated distressed and special situations fund, DSS 19, which will focus on global special situations opportunities and distressed securities, targeting $3 billion in commitments. Firm Overview: Bain Capital Credit, LP, an affiliate of Bain Capital, LP, is a leading global credit specialist. The Firm was formed as Sankaty Advisors in 1998 by Jonathan Lavine, Managing Partner and CIO, based on the idea that one could successfully apply the same level of rigorous analysis developed in Bain Capital’s Private Equity business to credit investing. With approximately $39 billion in assets under management as of January 1, 2019, Bain Capital Credit invests across the full spectrum of credit strategies, including leveraged loans, high-yield bonds, distressed debt, direct lending, structured products, non-performing loans (“NPLs”), and equities. Bain Capital Credit currently has 297 employees in -

LIFE at KKR We Are Investors

LIFE AT KKR We are investors. But we're more than that. IT'S IN OUR DNA We're collaborative team players who are curious communities. We often measure success over about the world around us. We're passionate about years, not quarters. We value integrity in all that we always learning more and pushing to be better. do, whether it's presenting numbers accurately or Here, we're never finished growing or discovering being open and honest with a portfolio company new ideas. executive. People want to do business with those they like and trust. It's a mantra instilled in all of us People want to do business from the top down. with those they like and trust As a firm we manage investments across multiple asset classes and as individuals we are encouraged to think creatively to solve problems, explore opportunities, take on new responsibilities and challenges, put our clients first and contribute to our LIFE AT KKR | 2 We are investors. But we're more than that. Culture & Work Environment For over 40 years, our At KKR, you'll find a team of curious, driven, dedicated and intelligent professionals who enjoy working together. We all work collaborative approach hard to create a friendly environment that encourages asking continues to drive our culture questions and reaching out to others. Teamwork Entrepreneurial Spirit Integrity No matter where you sit in the Some of our best ideas come from It's at the heart of everything we do organization, you have the full giving people the time to explore, from our internal interactions to resources, network, skills and research and have conversations. -

Mercer Capital's Value Focus

MERCER CAPITAL’S VALUE FOCUS » THIRD QUARTER 2009 Mercer Capital provides asset managers, trust companies, and investment consultants Asset Management with corporate valuation, fi nancial reporting valuation, transaction advisory, portfolio valuation, and related services. Call Matt Industry Crow or Brooks Hamner at 901.685.2120 to discuss your needs in confi dence. Segment Focus: Alternative Asset Managers It is no surprise that companies employing massive amounts of leverage to make risky bets 20.00% on perceived mispricings and underperforming businesses have seen their own share prices 10.00% fl uctuate wildly over the last 12 months. Most 0.00% notably, Fortress Investment Group lost nearly 90% of its market cap in the fourth quarter of -10.00% 2008, which preceded a seven-fold increase in the months to follow. Most other publicly -20.00% traded hedge funds and private equity managers have experienced similar volatility, as our index -30.00% of alternative asset managers dropped roughly -40.00% half its value in the fourth quarter last year and is up almost 60% year-to-date. Investor anxiety, -50.00% credit disruptions, market deterioration and BX BAM FIG GLG OZM subsequent recovery, coupled with a gradual Alternative Asset Managers S&P 500 thawing of the credit markets and a few quarters of earnings surprises, are largely to blame for these variations. Political events may have also contributed to the volatility of these insider trading scheme could revitalize investor scrutiny and induce investments. Many analysts have suggested that compensation limits at even tighter regulation of alternative asset managers, whose reputation Wall Street fi rms that owe money to the government will unintentionally and AUM are still badly bruised from the catastrophic second half of benefi t hedge funds and other alternative asset managers, who may be last year. -

Private Equity in the 2000S 1 Private Equity in the 2000S

Private equity in the 2000s 1 Private equity in the 2000s Private equity in the 2000s relates to one of the major periods in the history of private equity and venture capital. Within the broader private equity industry, two distinct sub-industries, leveraged buyouts and venture capital experienced growth along parallel although interrelated tracks. The development of the private equity and venture capital asset classes has occurred through a series of boom and bust cycles since the middle of the 20th century. As the 20th century ended, so, too, did the dot-com bubble and the tremendous growth in venture capital that had marked the previous five years. In the wake of the collapse of the dot-com bubble, a new "Golden Age" of private equity ensued, as leveraged buyouts reach unparalleled size and the private equity firms achieved new levels of scale and institutionalization, exemplified by the initial public offering of the Blackstone Group in 2007. Bursting the Internet Bubble and the private equity crash (2000–2003) The Nasdaq crash and technology slump that started in March 2000 shook virtually the entire venture capital industry as valuations for startup technology companies collapsed. Over the next two years, many venture firms had been forced to write-off large proportions of their investments and many funds were significantly "under water" (the values of the fund's investments were below the amount of capital invested). Venture capital investors sought to reduce size of commitments they had made to venture capital funds and in numerous instances, investors sought to unload existing commitments for cents on the dollar in the secondary market.