Sui Southern Gas Company Limited 2

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CORPORATE PARTNERSHIPS REPORT WWF-Pakistan FY19

CORPORATE PARTNERSHIPS REPORT CORPORATE PARTNERSHIPS REPORT WWF-Pakistan FY19 For further information on specific partnerships, please contact WWF-Pakistan Asma Ezdi, Head of Marketing and Communications ([email protected]) WWF is one of the world’s largest and most experienced independent conservation organizations, with over 5 million supporters and a global network active in more than 100 countries. WWF’s mission is to stop the degradation of the planet’s natural environment and to build a future in which humans live in harmony with nature, by conserving the world’s biological diversity, ensuring that the use of renewable natural resources is sustainable, and promoting the reduction of pollution and wasteful consumption. Published in 2019 by WWF – World Wide Fund For Nature – Pakistan (Formerly World Wildlife Fund), Lahore, Pakistan. Any reproduction in full or in part must mention the title and credit the above- mentioned publisher as the copyright owner. © Text 2019 WWF-PK All rights reserved. 2 TAKING BOLD COLLECTIVE ACTION The time to act is now. We have put in place a global conservation strategy that reflects the way the world is changing, meets the big environmental challenges of the age and helps us simplify, unite and focus our efforts for greater impact. WWF will continue to deliver locally in crucial ecoregions around the world, but sharpen our focus on six global goals – wildlife, forests, oceans, freshwater, climate and energy, and food – and three key drivers of environmental degradation – markets, finance and governance. We are creating global communities of practice for each of the goals and drivers composed of specialists from WWF and key external partners. -

Of Pakistan Annual Report 2008

WAFAQI MOHTASIB (OMBUDSMAN) OF PAKISTAN ANNUAL REPORT 2008 Wafaqi Mohtasib (Ombudsman)’s Secretariat Islamabad — Pakistan Tele: (92) (51) 9252391–4, Fax: (92) (51) 9252178 Email: [email protected] Website: http://www.mohtasib.gov.pk ACRONYMS ADB Asian Development Bank AIOU Allama Iqbal Open University AOA Asian Ombudsman Association CNIC Computerized National Identity Card CDA Capital Development Authority CMIS Complaint Management Information System G.P Fund General Provident Fund HBFC House Building Finance Corporation ICT Information Communication Technology IOs Investigating Offi cers IOI International Ombudsman Institute KESC Karachi Electric Supply Company KW Kilowatt LESCO Lahore Electric Supply Company LUMS Lahore University of Management Sciences MIS Management Information System NADRA National Database Registration Authority NEPRA National Electric Power Regulatory Authority NIC National Identity Card NOC No Objection Certifi cate NRSC National Registration Services Centre NWD Nation-Wide Dialling NWFP North West Frontier Province OGRA Oil and Gas Regulatory Authority PEPCO Pakistan Electricity & Power Company PTA Pakistan Telecommunication Authority PESCO Peshawar Electric Supply Company PLI Postal Life Insurance PO President’s Order PRS Premium Rate Service PTCL Pakistan Telecommunication Company Limited REACH Responsive, Enabling, Accountable Systems for Children Rights RETA Regional Technical Assistance SLIC State Life Insurance Corporation SNGPL Sui Northern Gas Pipeline Limited SPGRM Strengthening Public Grievance -

Schedule of Charges 1 July 2017 - 31 December 2017 Bill Payment

Schedule of Charges 1 July 2017 - 31 December 2017 Bill Payment Paying bills now more convenient than ever. You can now conveniently pay your bills through ATMs, Online Banking and Standard Chartered Mobile App. Billers available on our digital channels K-Electric | Lahore Electric Supply Company (LESCO) | Sui Southern Gas Company (SSGC) | Sui Northern Gas Pipeline Limited (SNGPL) | PTCL | Mobilink | Ufone | Warid To view the complete list of billers, visit sc.com/pk Pay bills, transfer funds, check account balance and much more, anywhere and anytime, with our easy-to-use Standard Chartered Mobile App. Now available on iOS and Android. Pakistan Client touch points are as follows: Touch Points What to Do Branch Visit any branch Email Email at: [email protected] Contact Centre Call on: 021 111 002 002 or 042 111 002 002 Website Visit: www.sc.com/pk Visit: www.facebook.com/standardcharteredpk Social Media Visit: www.twitter.com/stanchartmenap Write to: SCBPL Client Care Unit, 1st Floor, Letter Jubilee Insurance Bldg, I. I. Chundrigar Road, Karachi Visit: BC&CPD – State Bank of Pakistan, Central Directorate, I.I. Chundrigar Road, Karachi. State Bank of Pakistan www.sbp.org.pk Email at: [email protected] Call on: 111 727 111 Visit: Banking Mohtasib Pakistan Secretariat, 5th Floor, Shaheen Complex, M.R. Kiyani Rd, Banking Mohtasib Karachi. Pakistan www.bankingmohtasib.gov.pk Email at: [email protected] Visit: Insurance Mohtasib Secretariat, 197/5, Insurance Ombudsmen 2nd Floor, Red Crescent Society, Dr. Daudpota Road, Saddar, Karachi Visit: Federal Ombudsmen Secretariat, Federal Ombudsmen 5th Floor, Shaheen Complex, M.R. -

Shariah Compliance Screening Report

Al-Hilal Shariah Advisors December 2016 Shariah Compliance Screening Report INSIDE Key Highlights ......................................................................................................................................... 3 Shariah Compliant Companies ............................................................................................................... 5 Shariah Non - Compliant Companies ...................................................................................................... 7 Suspended & Delisted Companies………………………………………………………………………………………………….....9 Approved Islamic Banks & Windows for Placements ........................................................................... 10 Screening Guidelines for Equity Securities ........................................................................................... 11 Purification Guidelines .......................................................................................................................... 12 Al-Hilal Shariah Advisors (Pvt.) Limited. (Formerly Fortune Islamic (Pvt.) Limited) P a g e | 2 Al-Hilal Shariah Advisors (Pvt.) Limited. (Formerly Fortune Islamic (Pvt.) Limited) 27 April, 2017 KEY HIGHLIGHTS We have conducted Shariah compliance screening of 524 selected companies listed on the Pakistan Stock Exchange as per their latest financial statements (December’16), on the basis of the Shariah compliance screening mechanism approved by our Shariah Supervisory Council headed by Mufti Irshad Ahmad Aijaz. Following are the results for -

World Bank Document

PROJECT INFORMATION DOCUMENT (PID) APPRAISAL STAGE Report No.: 64701 Natural Gas Efficiency Project Project Name Public Disclosure Authorized Region South Asia Country Pakistan Sector Oil and gas (100%) Lending Instrument Specific Investment Loan Project ID P120589 Borrower(s) Government of Pakistan Ministry of Petroleum and Natural Resources Pak Secretariat, Block A Pakistan Tel: (92-51) 921-1220 Fax: (92-51) 920-1770 [email protected] Implementing Agency Sui Southern Gas Company Limited (SSGC) Public Disclosure Authorized Sir Shah Suleman Road Gulshan-e-Iqbal Block 14 Karachi 75300 Pakistan Tel: (92-21) 9231602 Fax: (92-21) 9231620 [email protected] Environmental Screening Category [ ] A [X] B [ ] C [ ] FI [ ] TBD (to be determined) Date PID Prepared September 9, 2011 Date of Appraisal Completion February 14, 2011 Estimated Date of Board Approval December 15, 2011 Decision Project authorized to proceed to negotiations upon Public Disclosure Authorized agreement of pending conditions and/or assessments I. Country Context 1. Pakistan has important strategic endowments and development potential. The country is located at the crossroads of South Asia, Central Asia, China and the Middle East. This places Pakistan at the fulcrum of a regional market with a vast population, large and diverse resources, and an untapped potential for trade. But Pakistan faces long-term challenges to realizing its growth potential. It requires a strong and stable tax base, and more efficient public spending to expand fiscal space. Other measures required include creating adequate employment opportunities; improving income distribution; and harnessing economic competitiveness through trade, investment, improved business environment, and competition. Today, Pakistan’s key economic challenges are the large fiscal deficit and energy shortages. -

SAYYED MAZAHAR ALI AKBAR NAQVI, J.- Through These

IN THE SUPREME COURT OF PAKISTAN (APPELLATE JURISDICTION) PRESENT: MR. JUSTICE GULZAR AHMED, HCJ MR. JUSTICE IJAZ UL AHSAN MR. JUSTICE SAYYED MAZAHAR ALI AKBAR NAQVI CIVIL APPEAL NOs. 936 & 937 OF 2020 (On appeal against the judgment dated 07.04.2020 passed by the High Court of Sindh, Karachi in Constitutional Petition Nos. D-5850 & D-5851 of 2018) M/s Sui Southern Gas Company Ltd (In both cases) … Appellant VERSUS Zeeshan Usmani etc (In CA 936/2020) Saima Athar etc (In CA 937/2020) … Respondents For the Appellant: Mr. Asim Iqbal, ASC (In both cases) For Respondent (1): Malik Naeem Iqbal, ASC (Islamabad) Mrs. Abida Parveen Channar, AOR (through video link from Karachi) Date of Hearing: 18.02.2021 JUDGMENT SAYYED MAZAHAR ALI AKBAR NAQVI, J.- Through these appeals under Article 185 of the Constitution of Islamic Republic of Pakistan, 1973, the appellant has called in question the legality of the impugned consolidated judgment dated 07.04.2020 passed by the High Court of Sindh, Karachi, whereby the Constitutional Petitions filed by the respondents were disposed of and the appellant department was directed to regularize them in service. 2. Briefly stated the facts of the matter are that respondents No. 1 in both the appeals were appointed in the appellant Sui Southern Gas Company Ltd on contract basis vide order dated 14.11.2012. They remained working on contract until 31.12.2017 but were not regularized and their contract stood terminated on the said date i.e. 31.12.2017. It appears from the record that the appellant had framed a policy i.e. -

Internet Banking - Bill Payment Guide

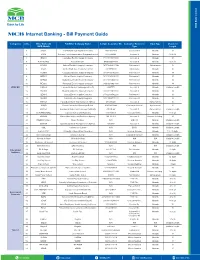

MCB Bank Limited Internet Banking - Bill Payment Guide Categories S.No. Biller Name On Full Biller Company Name Sample Consumer No. Consumer Reference Input Type Character MCB Mobile Type Length 1 SNGPL Sui Northern Gas Pipelines Limited 17647668748 Consumer # Numeric 11 2 PTCL Pakistan Telecommunication Company Limited 2105788644 Account ID Numeric 10 to 14 3 IESCO Islamabad Electric Supply Company 15141111610800 Account # Numeric 14 4 K-ELECTRIC Karachi Electric 0400000664365 Account # Numeric 10 to 15 5 LESCO Lahore Electricity Supply Company 10111440863100u Reference # Alphanumeric 15 6 SSGC Sui Southern Gas Company Limited 2827970000 Customer # Numeric 10 7 FESCO Faisalabad Electric Supply Company 08134130792600 Reference # Numeric 14 8 MEPCO Multan Electric Supply Company 16151121444300 Reference # Numeric 14 9 GEPCO Gujranwala Electric Power Company 01121330008100 Reference # Numeric 14 10 PESCO Peshawar Electric Supply Company 04261210027191 Reference # Numeric 14 Utility Bill 11 LWASA Lahore Water And Sewerage Authority 40097772 Account # Numeric Variable Length 12 HESCO Hyderabad Electric Supply Company 01373110013800 Account # Numeric 14 13 QESCO Quetta Electric Supply Company 07482430592200 Reference # Numeric 14 14 SEPCO Sukkur Electric Supply Company 02321548795135 Reference # Numeric 14 15 FWASA Faisalabad Water And Sanitation Agency w11200287 Account # Alpha numeric 10 16 KWSB Karachi Water And Sewerage Board N0073050000 Consumer Number Alphanumeric 11 17 RWASA Rawalpindi Water And Sewerage Authority A0100762 Account # -

Shariah Compliance Screening Report

Al-Hilal Shariah Advisors JUNE 2017 Shariah Compliance Screening Report Al-Hilal Shariah Advisors (Pvt.) Limited. INSIDE Key Highlights ................................ .......................................................................................................... 4 Shariah Compliant Companies ................................ ............................................................................... 8 Shariah Non - Compliant Companies .................................................................................................... 10 Suspended & Delisted Companies…………………………………………………………………………………………………...12 Approved list of Sukuk………………………………………………………………………………………………….....................13 Approved Islamic Banks & Windows for Placements……………….……………………………………………………….14 Approved list of charitable orginizations ............................................................................................. 15 Screening Guidelines for Equity Securities ........................................................................................... 16 Purification Guidelines .......................................................................................................................... 16 P a g e | 2 Al-Hilal Shariah Advisors (Pvt.) Limited. P a g e | 3 Al-Hilal Shariah Advisors (Pvt.) Limited. 14 July, 2017 KEY HIGHLIGHTS We have conducted Shariah compliance screening of 554 selected companies listed on the Pakistan Stock Exchange as per their latest financial statements (June’17), on the basis of the Shariah compliance -

Systematic GIS Development and Its Successful Implementation in SSGC-Pakistan

Sui Southern Gas Company Limited Information Technology Department Head Office, Karachi Pakistan Systematic GIS Development and its Successful Implementation in SSGC-Pakistan Authors Syed Ali Naqi, Zuhair Siddiqui Presented At: 2006 ESRI International GIS User Conference (San Diego, August 2006) Abstract: Utilities have prime importance in the worldwide development of urban and commercial centers. Natural gas is the most economical and reliable source for commercial and domestic energy consumers. The natural gas pipeline network was developed in Pakistan during 1950-1960s, and major expansion occurred in 1980-1990s to cover almost all major urban and rural areas. Most of the information is stored on manual paper maps having variable scales and several geometrical problems. The satisfactory supply of gas from stakeholders up to end-users demands an efficient information management system to streamline all relevant data sources. The rapid expansion and maintenance of gas pipeline network demands a proficient GIS, to serves as analytical decision support tool to foster the planning, development, and management process. This paper focuses on systematic development of GIS and its successful implementation as web based application in Sui Southern Gas Company (SSGC). Page 1 of 22 Introduction The paper starts with the overview of the Sui Southern Gas Company, its strategic vision and initiatives taken for the improvement of business processes through the use of technology; then it discuss SSGC’s GIS project background, vision & objectives, scope, its step by step development and its implementation as web based GIS application for better understating of seamless information which was previously stored at different locations on several unconnected traditional maps having variable scales and various geometrical problems. -

Post Event Report April 27, 2016

Post Event Report April 27, 2016 Organized by: www.solutions-inc.info Executive Summary . The Fourth Edition of Pakistan CIO Summit was held on April 05, 2016 at Marriott Hotel, Karachi . The theme of the summit was 'Solution for Tomorrow: Vision 2020' and Panel Discussions on Changing Face of Telecommunications / Evolving Role of CIO: Vision 2020 & Cloud Based Services / Business Intelligence: Vision 2020, were included. The year 2016 also witnessed the Second Edition of IT Showcase Pakistan , the allied expo in conjunction with 4th Pakistan CIO Summit 2016, held on April 5-6, 2016 at Marriott Hotel, Karachi . The summit and expo provided immense opportunities for learning, sharing experiences and networking . Business Beam, Fast-NU, IOBM and PAF-KIET were the Knowledge Partners for the event while ISACA Karachi Chapter, KPITB, MIT Enterprise Forum Pakistan, P@SHA, PSEB, OPEN Karachi Chapter, PTA, JumpStart and PISA were the Supporters for 4th Pakistan CIO Summit and 2nd IT Showcase Pakistan 2016 . RapidCompute, Viptela, REDtone Telecommunications, Inbox Business Technologies, New Horizon and VMware were Session Sponsors . Ms. Anusha Rahman Ahmed Khan, Federal Minister of IT and Telecom, was the Chief Guest for the show while Asim Shahryar Husain, Managing Director, PSEB was the Guest of Honor . 4th Pakistan CIO Summit 2016 was attended by 367 delegates representing 195 Companies. This includes 214 CIOs, IT Heads, IT Managers from 134 Organizations while 153 delegates represented 61 Companies from the IT Industry. The delegates included CIOs, IT Heads, IT Managers, Industry Experts, Decision Makers, Policy Makers and Academia . 19 Exhibitors from all cities of Pakistan including Karachi, Lahore, Islamabad and Peshawar. -

Standard Chartered Bank (Pakistan) Limited Board of Directors

STANDARD CHARTERED BANK (PAKISTAN) LIMITED BOARD OF DIRECTORS MR. SHAZAD DADA CEO/ EXECUTIVE DIRECTOR MR. CHRISTOS PAPADOPOULOS NON EXECUTIVE DIRECTOR & CHAIRMAN OF THE BOARD OF DIRECTORS MR. RAHEEL AHMED NON EXECUTIVE DIRECTOR MR. VINOD RAMABHADRAN NON EXECUTIVE DIRECTOR MR. NAJAM I. CHAUDHRI INDEPENDENT NON EXECUTIVE DIRECTOR & CHAIRMAN AUDIT COMMITTEE MR. PARVEZ GHIAS INDEPENDENT NON EXECUTIVE DIRECTOR MRS. SPENTA KANDAWALLA INDEPENDENT NON EXECUTIVE DIRECTOR SHAZAD DADA CEO/ EXECUTIVE DIRECTOR Shazad is the Chief Executive Officer and member of the Board of Directors of Standard Chartered Bank (Pakistan) Ltd., effective 3 October 2014. Shazad is a graduate with honours from University of Pennsylvania with Bachelors of Science and Bachelors of Arts degrees, and also has an MBA from the Wharton Business School, University of Pennsylvania. He is a seasoned banker and a prominent capital markets professional, with over 20 years of diverse experience with renowned financial institutions in the United States and Pakistan. Prior to joining Standard Chartered, he was the Chief Executive Officer and Managing Director of Barclays Pakistan. His experience spreads across Corporate, Investment and Retail Banking. Shazad was additionally the Head of Regional Transaction Services Steering Committee for Asia and India, UAE & Pakistan. He has also worked at the Deutsche Bank Securities Inc in New York for over 15 years in various capacities; last as the Managing Director in the Mergers, Acquisitions, and Corporate Advisory Group and was Head of Media M&A practice in the Americas. Moving back to Pakistan in late 2005 to head Deutsche Bank AG Pakistan as the Managing Director, Chief Country Officer and Head of Global Banking, Shazad has played an instrumental role in leading the turnaround of their Pakistan franchise. -

Make in Pakistan Panelists’ Profile

Make in Pakistan Panelists’ Profile Ali S. Habib is the founding and current Chairman of Indus Motor Company Limited (a joint venture with Toyota Motor Corporation) and is also on the Board of Directors of ThalNova Power Thar (Private) Ltd. He is currently on the Board of Directors of Habib Metropolitan Bank, Shabbir Tiles & Ceramics Ltd., Thal Ltd. Ali Habib is a graduate of the University of Minnesota (Mechanical Engineering). He has attended the PMD Program at Harvard University. He is the Founding Chairman of the Pakistan Automotive Manufacturers’ Association and the Founding Chairman Young Presidents Organization Pakistan Chapter and Founding Director of Pakistan Business Council. Mr. Ali Suleman Habib Panel Chair He also devotes his time and attention to social welfare, Chairman education and benevolent activities and is a Member on the Indus Motor Company Board of Governors of Habib University, as well as a Director on Limited the Board of Habib University Foundation and a Trustee of the Habib Education Trust. Abdul Razak Dawood is Chairman of Descon, which is involved in engineering, construction, chemicals and power. Descon Engineering is perhaps the first Pakistani multinational company to be operating in five countries, and having four overseas manufacturing units and more than 20,000 employees. Mr Dawood started his career in the family business at Lawrencepur Woolen and Textile Mills in 1968 and was then Mr. Abdul Razak Dawood transferred to Dawood Hercules Chemical Limited where he Chairman became the managing director from 1973 till 1981. In 1981, he Descon moved to Descon Engineering (Pvt.) Limited as its founder.