ANNUAL REPORT FUTURE2008-09 ©Istockphoto.Com

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

E-Government Progress Review South Kesteven District Council Audit

audit 2003/2004 E-government Progress Review South Kesteven District council INSIDE THIS REPORT PAGE 2-6 Summary PAGES 7-20 Detailed Report • Progress against ESD target (BVPI-157) resources • IEG3 ‘Traffic Lights’ assessment • Checklist for members and chief executives: • Leadership • Transforming services • Renewing local democracy • Promoting economic vitality PAGES 24-33 Appendices • Appendix 1 - SKDC Checklist for Members and Chief Executives • Appendix 2 - Comparative charts based on IEG3 ‘Traffic Lights’ • Appendix 3 – Good practice in Lincolnshire districts • Appendix 4 – Action plan Reference: KE011 E-government Progress Review Date: August 2004 audit 2003/2004 SUMMARY REPORT Introduction E-government is more than technology or the Internet or service delivery: it is about putting citizens at the heart of everything councils can do and building service access, delivery and democratic accountability around them. E-government includes exploiting the power of information and communications technology to help transform the accessibility, quality and cost-effectiveness of public services. It can be used to revitalise the relationship between citizens and the public bodies who work on their behalf. Local e-government is the realisation of this vision at the point where the vast majority of public services are delivered. In March 1999 the government produced a white paper Modernising Government, which included a new package of reforms and targets. The intention was that by 2002, 25 per cent of dealings by the public with government, including local government and the NHS, should have been capable of being conducted electronically, with 100 per cent of dealings capable of electronic delivery by 2005. In November 2002 the Office of the Deputy Prime Minister published the National Strategy for Local e-government. -

Advertising Signs On, Or Adjacent to the Highway

CORNWALL COUNTY COUNCIL COMMUNITY LIFE POLICY DEVELOPMENT AND SCRUTINY COMMITTEE ADVERTISING SIGNS ON, OR ADJACENT TO THE HIGHWAY SINGLE ISSUE PANEL DRAFT REPORT March 2005 CONTENTS ____________________________________________________________________ Executive Summary and Recommendations 1. Introduction 1 2. The Panel’s Findings 2 3. Conclusions 12 Appendix 1 – Summary of the Terms of Reference 13 Appendix 2 – Panel Members and Meetings 15 Appendix 3 – Witnesses 15 Appendix 4 – Employers Work Instructions – 16 Cumbria County Council EXECUTIVE SUMMARY Over the last 2-3 years there has been a notable increase in the amount of unauthorised advertising material being placed on, or adjacent to the highway. This varies from fly posting on the back of road signs, to trailers specifically designed to be left on, or adjacent to the roadside and has led to increasing concern within the County Council, district councils and from the general public. The removal of unauthorised signing is a controversial service area. In the past, programmes of work to remove signs have generated adverse comments from businesses and events organisers. The organisers of smaller events in particular often feel aggrieved as the display of signs and or flyers in the locality are often the only publicity for their events. At the present time the County Council does not have a formalised policy on the way in which it deals with advertising signs on or adjacent to the highway, and as a result officers instead adhere to a recognised working practice . As a result, the Advertising Signs on, or Adjacent to the Highway Single Issue Panel was established to consider the issues surrounding unauthorised signs which would influence the development of the Council’s policy. -

A New Geography of Local Government in Cornwall

Centre for Geography and Environmental Science A new geography of local government: The changing role of Town and Parish Councils in Cornwall, UK JUNE 2019 Jane Wills June 2 Localism and the role of Town and Parish Councils in Cornwall INTRODUCTION This report summarises research that has been undertaken as part of a larger project led by Locality, the national network of community organisations. It comprises material that forms part of phase two of the work undertaken for Locality’s Commission on the Future of Localism. The Commission has gathered evidence and ideas about efforts to engage local people in decision making and to strengthen community, and the challenges faced in realising these ambitions. Locality published the first round of findings in a report entitled People Power in early 2018 (Locality, 2018a). This report highlighted the need for greater thought and more focused action in relation to developing and supporting local institutions, fostering better relationships and building local capacity, in order to unlock the ‘power of community’. Building on the ideas developed in that report, phase two of the Commission’s work has involved action research with four local authorities (Cornwall, Southwark, Stevenage and Wigan) to explore the importance of geo-institutional inheritance and culture, local experiences, and the outcomes of efforts to foster localism. A report that draws on the learning from all four cases will be published late in 2019. This report focuses solely on the findings from the research undertaken with Town and Parish Councils (TPCs) in Cornwall. Conducted in late 2018 and early 2019, the author interviewed 27 individuals in 18 separate interviews, including representatives from 11 TPCs as well as the County Officer of Cornwall’s Association of Local Councils (CALC). -

IE Sub 200411 Energy Reduction and Renewable Energy Appendix 1

Appendix 1 LONDON BOROUGH OF BROMLEY IE&E SUB-COMMITTEE: 20 APRIL 2011 ENERGY REDUCTION & RENEWABLE ENERGY GENERATION: REPORT ES11052 APPENDIX 1: COUNCIL RENEWABLE ENERGY PROJECTS (BY SECTOR) SOLAR PHOTO-VOLTAICS & SOLAR THERMAL Cornwall County Hall: Solar Panels Cornwall Council is paving the way for a revolution in renewable energy with the installation of banks of solar panels on the roof of New County Hall. The 130 photo-voltaic panels will convert the above average levels of Cornish light into electricity that will power lights and computers in the Council building. http://www.cornwall.gov.uk/default.aspx?page=24157 Cornwall County Council: Solar Farm Cornwall Council is likely to become the first local authority in the UK to develop a large scale solar farm. The Cabinet of Cornwall Council approved the final business case for the solar farm at the Cabinet meeting 13 October 2010. Alec Robertson, Leader of Cornwall Council, said: “This is a huge opportunity for the Council, not just financially in terms of generating income that can be spent on frontline services, but also in terms of our green ambitions. This is an excellent example of Cornwall leading the way.” http://www.cornwall.gov.uk/Default.aspx?page=25943 Cherwell District Council: Solar Panels Cherwell District Council intends to install solar panels on five of its buildings, which it hopes would generate enough electricity to run them. So far the technology is being used on one building, Thorpe Lane depot, in Banbury. Now councillors are looking to expand the energy system to more of its buildings, including its Bodicote headquarters and Banbury Museum, in Castle Quay shopping centre, its sports centres and other buildings at Thorpe Lane. -

This Is the Author's Draft of a Paper Submitted for Publication in Nations

University of Plymouth PEARL https://pearl.plymouth.ac.uk Faculty of Health: Medicine, Dentistry and Human Sciences School of Nursing and Midwifery 2016-04-08 The fragmentation of the nation state? Regional development, distinctiveness, and the growth of nationalism in Cornish politics Willett, J http://hdl.handle.net/10026.1/5273 10.1111/nana.12188 Nations and Nationalism Wiley All content in PEARL is protected by copyright law. Author manuscripts are made available in accordance with publisher policies. Please cite only the published version using the details provided on the item record or document. In the absence of an open licence (e.g. Creative Commons), permissions for further reuse of content should be sought from the publisher or author. This is the author’s draft of a paper submitted for publication in Nations and Nationalism 2016 DOI: http://dx.doi.org/10.1111/nana.12188 The Fragmentation of the Nation State? Regional Development, Distinctiveness, and the Growth of Nationalism in Cornish Politics. Abstract Stateless nations across the EU have become increasingly vocal and confident in asserting a desire for autonomy, devolved governance, and independence. Meanwhile, identity politics has become a key factor of contemporary European regional development, with utility as a social, economic and governance tool. Culture has become a resource for regional branding to attract inward investment and differentiate in terms of competitiveness. The paper considers whether the utility of identity to regional development might provide an explanation for the growing confidence of EU stateless nations. We use the case study of Cornwall to explore the correlation, arguing that economic regionalism has provided a space for the articulation of national identities. -

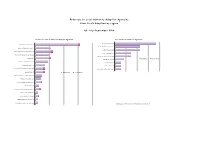

Q2 1617 LA Referrals

Referrals to Local Authority Adoption Agencies from First4Adoption by region Q2 July-September 2016 Yorkshire & The Humber LA Adoption Agencies North East LA Adoption Agencies Durham County Council 13 North Yorkshire County Council* 30 1 Northumberland County Council 8 Barnsley Adoption Fostering Unit 11 South Tyneside Council 8 Rotherham Metropolitan Borough Council 11 2 North Tyneside Council 5 Bradford Metropolitan Borough Council 10 Redcar Cleveland Borough Council 5 Hull City Council 10 1 Web Referrals Phone Referrals Middlesbrough Council 3 East Riding Of Yorkshire Council 9 City Of Sunderland 2 Cumbria County Council 7 Gateshead Council 2 Calderdale Metropolitan Borough Council 6 1 Newcastle Upon Tyne City Council 2 0 3.5 7 10.5 14 Leeds City Council 6 1 Web Referrals Phone Referrals Doncaster Metropolitan Borough Council 5 Hartlepool Borough Council 4 North Lincolnshire Adoption Service 4 1 City Of York Council 3 North East Lincolnshire Adoption Service 3 1 Darlington Borough Council 2 Kirklees Metropolitan Council 2 1 Sheffield Metropolitan City Council 2 Wakefield Metropolitan District Council 2 * Denotes agencies with more than one office entry on the agency finder 0 10 20 30 40 North West LA Adoption Agencies Liverpool City Council 30 Cheshire West And Chester County Council 16 Bolton Metropolitan Borough Council 11 1 Manchester City Council 9 WWISH 9 Lancashire County Council 8 Oldham Council 8 1 Sefton Metropolitan Borough Council 8 2 Web Referrals Phone Referrals Wirral Adoption Team 8 Salford City Council 7 3 Bury Metropolitan -

Update on Further Tender Opportunities for 2018 Contract Work on 28

28 March 2018 – Update on further tender opportunities for 2018 contract work On 28 February 2018 we published an update on the procurement process for 2018 civil legal aid contracts. This document provides further information about the tender opportunities that will open shortly to award additional: Face to face advice contracts; Housing Possession Court Duty Scheme (“HPCDS”) contracts; and Civil Legal Advice (“CLA”) specialist telephone advice contracts. Face to face services On 28 February we confirmed that as a result of the procurement process, there had been a good level of demand for face to face advice contracts. We also confirmed there were a small number of areas where the LAA wished to secure greater provision. We expect these tenders for additional face to face contract work to begin in late April 2018. We will be seeking additional services in the following areas only: a) 7 family procurement areas where fewer than five compliant bids were received; b) 39 housing and debt procurement areas where one or fewer compliant bids were received; and c) 6 immigration and asylum access points where one or fewer compliant bids were received. Annex A lists the procurement areas / access points in which we will be advertising additional face to face advice services. Any organisation who can meet the minimum contract requirements will be able to tender to deliver the advertised contract work under a 2018 Standard Civil Contract. This includes organisations that have already tendered for a 2018 Standard Civil Contract who wish to open additional offices in the advertised procurement areas /access points and organisations who have not previously tendered. -

Future Electoral Arrangements for Cornwall Council

Final recommendations Future electoral arrangements for Cornwall Council December 2009 Translations and other formats For information on obtaining this publication in another language or in a large-print or Braille version, please contact the Boundary Committee: Tel: 020 7271 0500 Email: [email protected] © The Boundary Committee 2009 The mapping in this report is reproduced from OS mapping by the Electoral Commission with the permission of the Controller of Her Majesty's Stationery Office, © Crown Copyright. Unauthorised reproduction infringes Crown Copyright and may lead to prosecution or civil proceedings. Licence Number: GD 03114G Contents Summary 1 Introduction 3 2 Analysis and final recommendations 7 Submissions received 7 Electorate figures 8 Council size 9 Electoral fairness 10 Draft recommendations 10 General analysis 11 Electoral arrangements 12 Penzance, St Ives & Hayle, Helston & The Lizard, 13 Falmouth & Penryn and Camborne & Redruth China Clay, St Agnes & Perranporth, St Austell, 21 St Blazey, Fowey & Lostwithiel and Truro Newquay, Bodmin, Wadebridge & Padstow, Camelford 28 and Bude Launceston, Liskeard, Looe & Torpoint, Callington 34 and Saltash Conclusions 39 Parish electoral arrangements 39 3 What happens next? 55 4 Mapping 57 Appendices A Glossary and abbreviations 59 B Code of practice on written consultation 63 C Table C1: Final recommendations for Cornwall Council 65 D Additional legislation we have considered 76 Summary The Boundary Committee for England is an independent statutory body which conducts electoral reviews of local authority areas. The broad purpose of an electoral review is to decide on the appropriate electoral arrangements – the number of councillors and the names, number and boundaries of wards or divisions – for a specific local authority. -

St Austell Main Report

Cornwall & Scilly Urban Survey Historic characterisation for regeneration ST AUSTELL CORNWALL ARCHAEOLOGICAL UNIT Objective One is part-funded by the European Union Cornwall and Scilly Urban Survey Historic characterisation for regeneration ST AUSTELL Kate Newell June 2002 CORNWALL ARCHAEOLOGICAL UNIT A service of the Historic Environment Section, Planning Transportation and Estates, Cornwall County Council Kennall Building, Old County Hall, Station Road, Truro, Cornwall, TR1 3AY tel (01872) 323603 fax (01872) 323811 E-mail [email protected] Acknowledgements This report was produced as part of the Cornwall & Scilly Urban Survey project (CSUS), funded by English Heritage and the Objective One Partnership for Cornwall and the Isles of Scilly (European Regional Development Fund). Peter Beacham (Head of Urban Strategies and Listing), Roger M Thomas (Head of Urban Archaeology) and Ian Morrison (Ancient Monuments Inspector for Devon, Cornwall and Isles of Scilly) liaised with the project team for English Heritage and provided valuable advice, guidance and support. Nick Cahill (The Cahill Partnership) acted as Conservation Supervisor to the project, providing vital support with the characterisation methodology and advice on the interpretation of individual settlements. Georgina McLaren (Cornwall Enterprise) performed an equally significant advisory role on all aspects of economic regeneration. Additional help has been given by Terry Clarke (Conservation Officer, Restormel Borough Council) and Victoria Northcott (Assistant Conservation Officer, Restormel Borough Council) and Keith Everitt (St Austell Bay Regeneration Officer, Restormel Borough Council). The Urban Survey Officers for CSUS are Kate Newell and Stephanie Russell. Kate Newell was the lead officer for the assessment of St Austell. Bryn Perry-Tapper is the project’s GIS/SMR Supervisor and has played an important role in developing the GIS, SMR and Web elements of the project and training the team. -

St Austell Town Plan 2012

St Austell Town Plan 2012 Produced by St Austell Town Council with the help and guidance of residents and visitors to the town 2 Welcome to the St Austell Town Plan I am very pleased to be able to introduce the St Austell Town Plan. I was born in St Austell and have lived here most of my life. I am very proud to be Mayor, and regard it as a great privilege to represent the people of St Austell along with my fellow members of the Town Council. St Austell is the largest town in Cornwall and this Plan represents a major step forward for its future development. The Plan is based on consultation with the community, not only when the Council was established, but more recently in June when many members of the public commented on an initial draft. I am grateful to all those who have contributed to its preparation. In this Plan we set out the changes and improvements which are needed and desirable in the town over the next four or five years. We suggest how these might take place and who should be involved in making them happen. St Austell, like many towns and cities, faces a number of challenges in these uncertain economic times but the town has always had the capacity to move forward, building on the achievements of the past. Today the people of St Austell still retain the potential and the strength to turn our vision for the town into reality. The Plan can only work, however, if the members of our community, elected and unelected, take an active role in making it happen. -

Annual Report 2008-2009

Redruth Town Council Consel An Dre Resrudh Annual Report for the Council Year 2008/2009 The Chambers Penryn Street Redruth TR15 2SP INTRODUCTION Welcome to our Annual Report. It is the Town Council’s policy to be open and informative. In this report you will find a set of financial accounts showing how the Council spends money on your behalf. During the year we have welcomed the Wilkinson’s store to Redruth, and despite losing the Co-op from the town centre this has brought a welcome boost to the shopping experience in Redruth. This year has also seen the launch of the Heart of Cornwall Loyalty Card which is available free of charge and can be used in member businesses throughout Redruth Camborne and Pool. As usual we have financially assisted a diverse range of local community groups from the Meals on Wheels service to the Christmas Events group. We run regular surgeries where members of the public can call in to discuss issues with Councillors, details of which can be found either by telephoning the office during working hours, or looking on our website (www.redruth-tc.gov.uk). In order to promote Redruth the Town Council took the decision to join with Camborne and Carn Brea Councils and Camborne-Pool-Redruth Regeneration to take part in a marquee at the Royal Cornwall Show. As we go to print preparations are underway for the event. The Council intends to highlight the many unique facilities we have in Redruth both to Cornish residents and to visitors, and we have produced a DVD entitled Redruth Revealed. -

(Public Pack)Item 3: Revised Appendices Agenda Supplement

Public Document Pack Agenda Supplement Meeting: County Council Time: 10.00 am Date: 10 March 2016 Venue: Council Chamber, County Hall, Colliton Park, Dorchester, DT1 1XJ Debbie Ward Contact: Lee Gallagher, Democratic Services Manager Chief Executive County Hall, Dorchester, DT1 1XJ 01305 224191 - Date of Publication: [email protected] Wednesday, 2 March 2016 3. Exploring Options for the Future of Local Government in 1 - 6 Bournemouth, Dorset and Poole To receive revised appendices to the report by the Chief Executive. This page is intentionally left blank Agenda Item 3 Appendix 1 Learning from Other Council Mergers Case Study: Wiltshire In December 2007 the government announced that five county areas would become unitary in 2009 – Wiltshire, Cornwall, Shropshire, Northumberland and Durham. The Wiltshire merger is cited as one of the most successful unitary initiatives in the UK, achieved on time and under budget, and gaining a glowing report from DCLG. It is the successor authority to Wiltshire County Council (1889–2009) and four district councils— Kennet, North Wiltshire, Salisbury, and West Wiltshire—all of which had been created in 1973 and were abolished in 2009 when Wiltshire Council was created. Wiltshire has a population of c. 435,000 who are represented by 98 Councillors (majority Conservative). In December 2007, the Government approved a bid from Wiltshire County Council for a unitary council to take over the responsibilities for all local government services in those areas in Wiltshire currently served by four district councils and the county council. A Statutory Instrument was subsequently approved by Parliament on 25 February 2008, establishing a new Wiltshire unitary authority from 1 April 2009.