Green-Car Sales Trend

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Q2 2021 Americas VT56.Docx

Title: TPMS Tools Q2 2021 Software Release Notes TPMS Product(s): Q2 2021 ATEQ VT56 Introduction The software update includes new OE coverage, improved programmable sensor coverage, new functionalities and corrections. Vehicles All worldwide brands, Americas region Novi, Michigan: ATEQ is proud to announce the new Q2 2021 software release. The latest software update includes new vehicle model coverage, updated OE sensor information, increased TPMS coverage for Aftermarket sensor brands, and new Aftermarket TPMS sensor brands. New version now available: DA1-38-13 (Or higher) New vehicle models added: Acura MDX Kia Carnival Lucid Air Beta 1 Volkswagen ID.4 Volkswagen Taos New Brand(s): Lucid Motors Updated OE sensor information: BMW 3 BMW 4 BMW M3 BMW M4 BMW M5 BMW M8 BMW X3 BMW X4 Chevrolet Captiva Sport Chevrolet Silverado Dodge Durango Ford Police Interceptor Sedan Ford Police Interceptor Utility Ford Police Interceptor Hybrid Ford Special Service Police Sedan Ford SSV Plug-In Hybrid Ford Taurus Freightliner Sprinter Genesis G80 Genesis G90 ateq-tpms.com - 888-621-TPMS (8767) Genesis GV80 Honda CR-V Honda Insight Honda Passport Honda Ridgeline Hyundai Elantra Hyundai Palisade Hyundai Santa Fe Hyundai Sonata Hyundai Tucson Hyundai Venue Kia Forte Kia K5 Kia Rio Kia Rondo Kia Sorento Kia Stinger Kia Telluride Land Rover Defender Land Rover Discovery Sport Land Rover Range Rover Evoque Lexus IS Series Mazda CX-3 Mazda CX-30 Mazda CX-5 McLaren P1 Mitsubishi Eclipse Cross Mitsubishi i-MiEV Mitsubishi Mirage Nissan Frontier Nissan Kicks Nissan Pathfinder Pontiac G3 Toyota Land Cruiser Toyota Sienna Updated Aftermarket Sensor Coverage: Alligator Sens.it Schrader EZ-Sensor BH Sens IntelliSens UVS, ECS (formally Huf) Hamaton U-Pro BWD Standard QWIK Mobiletron Orange Universal NAPA QWIK Steelman Select MAX T.O.T.A.L. -

(Pmv) Prices Issued by Car Dealers As of 06Th July 2021

PASSENGER MOTOR VEHICLES (PMV) PRICES ISSUED BY CAR DEALERS AS OF 06TH JULY 2021 Prices on the JPES website are every 2 weeks. For the most up-to-date prices, please download the PenggunaBijak mobile app SER SHOWROOM PRICE ON-THE-ROAD PRICE PMV MODEL & BRAND DESCRIPTION DATE ISSUED No. (SRP) (OTR) 1.00 ALFA ROMEO (G.H.K. MOTORS SDN BHD) 1.01 ALFA ROMEO GIULIA 620 GME 2.0L AUTO SEDAN PETROL $ 63,900.00 $ 65,800.00 5-Jun-21 1.02 ALFA ROMEO GIULIA 620 QV V6 2.9L AUTO SEDAN PETROL $ 139,973.00 $ 144,094.00 5-Jun-21 1.03 ALFA ROMEO GIULIA VELOCE 620 2.0L AUTO GME 2000 SEDAN PETROL $ 72,700.00 $ 74,800.00 5-Jun-21 1.04 ALFA ROMEO STELVIO 2.0L AUTO AWD SUV PETROL $ 75,500.00 $ 77,800.00 5-Jun-21 2.00 AUDI (T.C.Y. MOTORS SDN BHD) 2.01 AUDI A4 2.0L TFSI (40) S-TRONIC AUTO LIMOUSINE PETROL $ 70,243.00 $ 72,169.00 3-Jul-21 2.02 AUDI A4 2.0L TFSI QUATTRO (45) S-TRONICS LINE AUTO LIMOUSINE PETROL $ 80,055.00 $ 82,185.00 3-Jul-21 2.03 AUDI A6 3.0L TFSI QUATTRO S-TRONIC AUTO SEDAN PETROL $ 109,930.00 $ 112,716.00 3-Jul-21 2.04 AUDI A8L 3.0L (55) TFSi QUATTRO TIPTRONIC AUTO SEDAN PETROL $ 181,740.00 $ 186,015.00 3-Jul-21 2.05 AUDI Q2 1.4L TFSI (35) S-TRONIC AUTO SUV PETROL (S-LINE) $ 53,918.00 $ 55,444.00 3-Jul-21 2.06 AUDI Q3 1.4L TFSI AUTO S-TRONIC SPORTBACK PETROL -ADVANCE LINE $ 59,977.00 $ 61,625.00 3-Jul-21 2.07 AUDI Q3 2.0L TFSI S-TRONIC AUTO SUV PETROL (ADVANCED LINE) $ 65,427.00 $ 67,251.00 3-Jul-21 2.08 AUDI Q5 2.0L TFSI QUATTRO S-TRONIC AUTO SUV PETROL (S-LINE BE) $ 89,800.00 $ 92,134.00 3-Jul-21 2.09 AUDI Q5 2.0L TFSI QUATTRO S-TRONIC AUTO SUV PETROL (S-LINE) $ 82,800.00 $ 84,971.00 3-Jul-21 2.10 AUDI Q7 2.0 TFSI (45) QUATTRO TIPTRONIC AUTO AWD 5-SEATERS SUV PETROL $ 111,689.00 $ 114,472.00 3-Jul-21 2.11 AUDI Q7 3.0 TFSI (55) QUATTRO TIPTRONIC AUTO AWD 5-SEATERS SUV PETROL $ 128,236.00 $ 131,409.00 3-Jul-21 AUDI Q7 3.0 TFSI (55) QUATTRO TIPTRONIC AUTO AWD 5-SEATERS SUV PETROL - S 2.12 $ 137,371.00 $ 140,728.00 3-Jul-21 LINE 2.13 AUDI RS5 2.9L TFSI QUATTRO TIPTRONIC AUTO SPORTBACK PETROL $ 164,354.00 $ 168,282.00 3-Jul-21 3.00 BAIC (T.C.Y. -

New Car Buyer's Guide

NEW CARBUYER’S GUIDE 2020 MODELS THANKSGIVINGHANKSGIVING WEEKENDWEEKEN PHOENIX CONVENTION CENTER ·thurs. -sun. 500+ New vehicles ·75+ road test vehicles experience Camp Jeep ·driving simulators FAMILY FRIENDLY ·non-selling show ·ONCE-A-YEAR BUY DISCOUNTED TICKETS: autoshowphoenix.com produced by: Sponsored by: AR-SPAD1108095026 2020-MODEL ARIZONA INTERNATIONAL AUTO SHOW ROLLS INTO PHOENIX CONVENTION CENTER THANKSGIVING WEEKEND NEW VEHICLES, PRE-PRODUCTION MODELS, EXOTICS, CAMP JEEP, TEST DRIVES AND MORE he 2020-model Arizona International Auto several manufacturers including Bentley Scottsdale, Lamborghini Show returns to Phoenix for Thanksgiving Chevrolet, Chrysler, Dodge, North Scottsdale and Aston Martin weekend Thursday, Nov. 28 through Fiat, Ford, Jeep, Ram, Subaru, Scottsdale. Additionally, the 1985 Sunday, Dec. 1. For four thrilling days, the and Volkswagen. The 2020 Ram 1500 Indianapolis 500 winning Indy car driven by PhoenixT Convention Center will be packed with and 2020 Jeep Gladiator are among the vehicles Danny Sullivan will be on display, courtesy of nearly 500 of the latest cars, trucks, crossovers, available for road tests. Also, showgoers can get Penske Museum. SUVs and alternative fuel options from 30- behind a wheel of thrilling racing simulators on the plus manufacturers, as well as exotics, new show floor including the Dodge Demon Simulator, Family Day is Sunday, Dec. 1! On this special technologies, pre-production models, driving Ford Sim-zilla Driving Simulator and Hyundai day, all children 12 and under are admitted free simulators and more than 75 vehicles to road Racing Simulator. when accompanied by a paying adult, courtesy of test at the event. American Family Insurance. Kids are invited to take Professional 4x4 drivers will take passengers on a spin on the American Family Kids Test Track all From casual enthusiasts to car lovers, everyone is a thrilling interactive adventure along an off-road show days. -

Hyundai Auto Lease Securitization Trust 2020-A

Presale: Hyundai Auto Lease Securitization Trust 2020-A January 8, 2020 PRIMARY CREDIT ANALYST Preliminary Ratings Timothy J Moran, CFA, FRM New York Preliminary amount Legal final (1) 212-438-2440 Class(i) Preliminary rating Type Interest rate(ii) (mil. $) maturity timothy.moran A-1 A-1+ (sf) Senior Fixed 132.60 Jan. 15, 2021 @spglobal.com A-2 AAA (sf) Senior Fixed 321.85 May 16, 2022 SECONDARY CONTACT A-3 AAA (sf) Senior Fixed 321.85 July 17, 2023 Steve D Martinez New York A-4 AAA (sf) Senior Fixed 71.53 Dec. 15, 2023 (1) 212-438-2881 B AA+ (sf) Subordinate Fixed 45.97 May 15, 2024 steve.martinez @spglobal.com Note: This presale report is based on information as of Jan. 8, 2020. The ratings shown are preliminary. Subsequent information may result in the assignment of final ratings that differ from the preliminary ratings. Accordingly, the preliminary ratings should not be construed as evidence of final ratings. This report does not constitute a recommendation to buy, hold, or sell securities. (i)All or a portion of one or more classes of notes may be initially retained by the sponsor Hyundai Capital America or its affiliate. (ii)The actual coupons of these tranches will be determined on the pricing date. Profile Expected closing date Jan. 22, 2020. Collateral Prime auto lease receivables. Origination trust Hyundai Lease Titling Trust. Issuer Hyundai Auto Lease Securitization Trust 2020-A. Sponsor, servicer, and administrator Hyundai Capital America Inc. (BBB+/Stable/A-2). Depositor Hyundai HK Lease LLC. Indenture trustee U.S. -

Approval Car Price Issued As of 31St January 2020

APPROVAL CAR PRICE ISSUED AS OF 31ST JANUARY 2020 DATE SHOWROOM PASSENGER MOTOR VEHICLES BRAND PASSENGER MOTOR VEHICLES MODEL /TYPE DATE ISSUED PRICE (SRP) EFFECTIVE EXPIRY ALFA ROMEO ALFA ROMEO GIULIA 620 QV V6 (G.H.K MOTORS SDN BHD) ALFA ROMEO GIULIA 620 QV V6 2.9L AUTO SEDAN PETROL 27-May-19 21-Apr-19 20-Apr-20 $139,973.00 ALFA ROMEO GIULIA 620 GME ALFA ROMEO GIULIA 620 GME 2.0L AUTO SEDAN PETROL 27-May-19 21-Apr-19 20-Apr-20 $63,353.00 ALFA ROMEO STELVIO ALFA ROMEO STELVIO 2.0L 8-SPEED AUTOMATIC TRANSMISSION AWD SUV 7-Jan-20 1-Dec-19 30-Nov-20 $75,262.00 PETROL (SOLID PAINT) ALFA ROMEO STELVIO 2.0L 8-SPEED AUTOMATIC TRANSMISSION AWD SUV 7-Jan-20 1-Dec-19 30-Nov-20 $77,538.00 PETROL (SPECIAL PAINT) ALFA ROMEO VELOCE 620 2.0L GME 2000 ALFA ROMEO GIULIA VELOCE 620 2.0L AUTO GME 2000 SEDAN PETROL 27-Jul-19 3-Jun-19 2-Jun-20 $69,666.00 AUDI AUDI A3 TFSI S-TRONIC (T. C. Y. MOTORS SDN BHD) AUDI A3 1.2L TFSI S-TRONIC AUTO SEDAN PETROL 26-Dec-19 31-Dec-19 30-Dec-20 $43,631.00 AUDI A3 TFSI S-TRONIC SPORTBACK AUDI A3 1.2L TFSI S-TRONIC AUTO SPORTBACK PETROL 7-Sep-19 11-Sep-19 10-Sep-20 $46,803.00 AUDI A4 TFSI S-TRONIC BLACK EDITION AUDI A4 2.0L TFSI S-TRONIC AUTO SEDAN PETROL - BLACK EDITION 19-Jun-19 3-Jun-19 2-Jun-20 $55,068.00 AUDI A4 TFSI QUATTRO S-TRONIC AUDI A4 2.0L TFSI QUATTRO S-TRONIC AUTO AWD SEDAN PETROL 19-Jun-19 3-Jun-19 2-Jun-20 $67,560.00 AUDI A4 TFSI ULTRA QUATTRO S-TRONIC AUDI A4 2.0L TFSI ULTRA QUATTRO AWD S-TRONIC AUTO SEDAN PETROL 25-Feb-19 11-Feb-19 10-Feb-20 $68,676.00 AUDI A5 TFSI QUATTRO S-TRONIC COUPE AUDI A5 2.0L TFSI -

Rota Special Report: 15 Pages

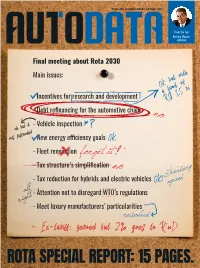

Year 26 | August 2018 | Edition 347 From the Top Antonio Megale, Anfavea Final meeting about Rota 2030 Main issues: OK but with a limit of - Incentives for research and development R$ 1,5 bi - Debt refinancing for the automotive chain no - Vehicle inspection ok but it was suspended- New energy efficiency goals OK - Fleet renovation forget it - Tax structure’s simplification no Treasury - Tax reduction for hybrids and electric vehicles OK! agreed all - Attention not to disregard WTO’s regulations right! - Meet luxury manufacturers’ particularities resolved - Ex-tariff: zeroed but 2% goes to R’nD ROTA SPECIAL REPORT: 15 PAGES. 4 » INDEX INDUSTRIAL POLICY Everything you wanted to know about Rota 2030 but you had no THE ABC OF ROTA 2030 14 one to ask about it, from behind the scenes to the rules of the program INDUSTRY Exclusive survey points the platforms manufactured in Brazil and LANÇAMENTOS 26 their correlation with sales of the models that they originate PRODUCTION MARKET The segment regains spirit in spite of a new suspension of city BUSES 98 buses bidding in São Paulo: there are other markets to explore. MARKET Ford and Volkswagen present Ka and Gol families with automatic LAUNCHES 36 transmission to try to combat Chevrolet Onix and Hyundai HB20 SUPPLIERS Novelties are bringing a splash of color to the area of paints, AUTOMOTIVE PAINTS 38 especially in new technologies. But the cost factor is still an impediment. SUPPLIERS FCA awards its main partners and gives the warning so that they RECOGNITION 42 get ready to meet a timetable of 25 launches PEOPLE The farewell to Sergio Marchionne and the implications of his EXECUTIVES 44 sudden death within the structure of Fiat Chrysler Automobiles 6 8 24 46 50 LENSES FROM THE TOP AUTODATA ASKS PEOPLE & BUSINESS END OF CHAT The backstage of the Antonio Megale talks We choose a theme Executive moves The most relevant automotive industry. -

Customer Analysis of Mid-Range Sport Utility Vehicle in India Rahul Singh1and Shiny Raizada2*

Singh & Raizada (2020): Customer analysis of SUV Nov 2020 Vol. 23 Issue 17 Customer Analysis of Mid-Range Sport Utility Vehicle in India Rahul Singh1and Shiny Raizada2* 1Student, MBA, 2Assistant Professor,Symbiosis School of Sports Sciences, Symbiosis International (Deemed University), Pune, Maharashtra, India *Corresponding author: [email protected] (Raizada) Abstract Background:In India, the automobile industry has grown extensively in the past few years and to be very specific Sport Utility Vehicles (SUV) has been one of the major boosters in the industry.Methods: The objective of this study was to analyze the consumer behaviour, thinking and usage patterns of those who have bought a mid-range priced SUV (10 to 20 lakhs) in the last 10 months (June 2019 to April 2020) or is planning to buy one in the next 10 months (May 2020 to March 2021). Hyundai Creta, KIA Seltos, MG Hector, TATA Harrier, Mahindra XUV 500, Toyota Innova, VitaraBrezza and Hyundai Venue were considered for the study from a particular segment. The sample of approximately 130 customers were taken and the analysis was done based on the data recorded in four major sections, i.e. Media Consumption, Unaided recall, Brand preferences and Price perception and decision making.Conclusion:The results indicated that most of the consumers were mostly active on Social Media Platform like Facebook and rated almost every SUV value for money which was included in the survey. In fact almost every participant in the survey was satisfied with the purchase they made to spend money on their SUVs. Keywords: Automobile Industry, Sport Utility Vehicles (SUV), Consumer Behavior How to cite this article: Singh R, Raizada S (2020): Customer analysis of mid range sport utility vehicle in India, Ann Trop Med & Public Health; 23(S17): SP231739. -

![[En]=> (LV-CAN200)](https://docslib.b-cdn.net/cover/0743/en-lv-can200-1080743.webp)

[En]=> (LV-CAN200)

[en]=> (LV-CAN200) year program № from Rear right door Total CNG use CNG level (in kilograms) Ignition Engine is working on CNG Front left door Front right door Rear left door Trunk cover Engine cover (Hood) Charging cable connected Charging the battery Electric engine working Oil pressure / level Washer fluid level indicator turned Low AdBlue level Total mileage of the vehicle (dashboard) Vehicle mileage - (counted) Total fuel consumption Total fuel consumption - (counted) Fuel level (in percent) Fuel level (in liters) Engine speed (RPM) Engine temperature Vehicle speed Acceleration pedal position Total CNG consumption - (counted) CNG level (in percent) 1 ABARTH 124 SPIDER 2016 → 12259 2020-06-30 + + + + + + + + + + + + + + 2 ABARTH 595 2016 → 12687 2019-05-30 + + + + + + + + + + + + + + 3 ABARTH 695 2017 → 12687 2019-05-30 + + + + + + + + + + + + + + 4 ACURA RDX 2010 → 11113 2017-09-01 + + + + + + + + + + + + + + + + 5 ACURA RDX 2007 → 11113 2017-09-01 + + + + + + + + + + + + + + + + 6 ACURA TL 2004 → 11167 2017-09-01 + + + + + + + + + + + + 7 ACURA TLX 2015 → 12363 2019-05-19 + + + + + + + + + + + + + + + + 8 ACURA TSX 2009 → 12578 2019-01-16 + + + + + + + + + + + + + + + + 9 ACURA TSX 2004 → 11167 2017-09-01 + + + + + + + + + + + + 10 ALFA ROMEO 159 2005 → 11128 2017-09-01 + + + + + + + + + + + + + + 11 ALFA ROMEO BRERA 2008 → 11128 2017-09-01 + + + + + + + + + + + + + + 12 ALFA ROMEO GIULIA 2017 → 12242 2019-05-22 + + + + + + + + + + + + + + + 13 ALFA ROMEO GIULIETTA 2013 → 11127 2019-04-10 + + + + + + + + + + + + + + 14 ALFA ROMEO -

IIHS Status Report Newsletter, Vol. 55, No. 1, February 13, 2020

StatusInsurance Institute for Highway Safety Report | Highway Loss Data Institute Vol. 55, No. 1 February 13, 2020 64 vehicles earn safety awards More vehicles come with standard autobrake Good headlights are still mostly optional What’s behind pedestrian deaths on freeways? ixty-four cars and SUVs qualify for with the right headlights can be a challenge the front crash prevention requirements for an award from the Insurance Insti- for consumers. We wanted to reward auto- either award with optional equipment. S tute for Highway Safety under new makers that have removed this obstacle.” However, 20 TOP SAFETY PICK+ win- criteria that prioritize the protection of pe- Six of the “plus” winners — the Genesis ners and 26 TOP SAFETY PICK winners destrians in addition to vehicle occupants. G70, Honda Insight, Hyundai Nexo, Lexus come with standard systems, as automakers To qualify for a 2020 TOP SAFETY PICK NX, Subaru Crosstrek Hybrid and Tesla move to meet their voluntary commitment or TOP SAFETY PICK+ award, vehicles Model 3 — aren’t sold with anything other on automatic emergency braking (AEB). The must have good ratings in each of the Insti- than good-rated headlights. A good rating commitment calls for front AEB to be stan- tute’s six crashworthiness evaluations. They means headlights provide the best balance dard on all but the heaviest passenger vehi- must also have good or acceptable head- of visibility and lack of excessive glare for cles by 2022 (see p. 4). lights and available front crash prevention drivers of oncoming vehicles. The voluntary commitment calls only for that earns advanced or superior ratings in Good visibility is key to avoiding crashes systems that avoid crashes with other vehi- both vehicle-to-vehicle and vehicle-to-pe- in the dark. -

![[En]=> (LV-CAN200)](https://docslib.b-cdn.net/cover/8156/en-lv-can200-1458156.webp)

[En]=> (LV-CAN200)

[en]=> (LV-CAN200) year program № from Engine is working on CNG Front left door Front right door Rear right door Trunk cover Oil pressure / level Total mileage of the vehicle (dashboard) Total fuel consumption Fuel level (in percent) Fuel level (in liters) Engine temperature Vehicle speed Acceleration pedal position Total CNG consumption - (counted) CNG level (in percent) CNG level (in kilograms) Rear left door Engine cover (Hood) Vehicle mileage - (counted) Total fuel consumption - (counted) Engine speed (RPM) Total CNG use 1 ABARTH 124 SPIDER 2016 → 12259 2020-06-30 + + + + + + + + + + + + + 2 ABARTH 595 2016 → 12687 2019-05-30 + + + + + + + + + + + + + 3 ABARTH 695 2017 → 12687 2019-05-30 + + + + + + + + + + + + + 4 ACURA RDX 2010 → 11113 2017-09-01 + + + + + + + + + + + + + + + 5 ACURA RDX 2007 → 11113 2017-09-01 + + + + + + + + + + + + + + + 6 ACURA TL 2004 → 11167 2017-09-01 + + + + + + + + + + + 7 ACURA TLX 2015 → 12363 2019-05-19 + + + + + + + + + + + + + + + 8 ACURA TSX 2009 → 12578 2019-01-16 + + + + + + + + + + + + + + + 9 ACURA TSX 2004 → 11167 2017-09-01 + + + + + + + + + + + 10 ALFA ROMEO 159 2005 → 11128 2017-09-01 + + + + + + + + + + + + + 11 ALFA ROMEO BRERA 2008 → 11128 2017-09-01 + + + + + + + + + + + + + 12 ALFA ROMEO GIULIA 2017 → 12242 2019-05-22 + + + + + + + + + + + + + + 13 ALFA ROMEO GIULIETTA 2013 → 11127 2019-04-10 + + + + + + + + + + + + + 14 ALFA ROMEO GIULIETTA 2010 → 11127 2017-09-01 + + + + + + + + + + + + + 15 ALFA ROMEO GT 2005 → 11128 2017-09-01 + + + + + + + + + + + 16 ALFA ROMEO MITO 2014 → 11127 2017-09-01 -

Country Report

Country Report Country Automotive Market Insights Editorial Dear Reader, Aborum et aborionsequi omnihicit aliate susOdia doluptatem ellaces accus abor solum liquis et erit aspedi volorepra conseque et elis intibeaque pelestio od ut optas pora- tur iorecti tem que sitat que que evenis sum eaqui doluptas ent aut ipiet officae ssima- gnit etur sandipi cientionet pelit, sandandit quatet, cullignime qui core occusdae plibus. Obis moluptia porporatur aut repudiantiam aut ant lant alit, omnimin ihilibus rem sequi dollenis quas elent, tentus es es di solesequi- sim ius. As rae. Ut il et eum etum repero moluptate velenda il miligni mpores sunt vel ipis rerferum volorro es rem volupta dion recea nis dolup- tur, omnis sus dus eaquidel incti custem eos exeratu rerchil iquatet quat acillupta dolupta a sunt apicit la doluptia solorep elenimustem rero dis modicipsa por as mo iducid quatem in nissinum ut remolessedi undit omnis sit qui cus as magnis rehent faccae pro temod. Kind regards, Carlo Simongini Founder & Managing Partner [email protected] Automotive Market Insights - 4 Table of Contents | Executive Summary | Key Economic Factors | Country market in the World Country World’s Rank (2012- 2013) Sales volume (2010-2013) World’s market share (2010 -2013) 2013 Monthly sales volume Market growth rate (2011-2013) | Market Segmentation Market segmentation Segment dynamics Top models by segment | Brand Performance Top 25 Brands ranking World’s Brand market share Country Brand market share Brand relatively strength index | Models Performance World Best-selling cars Country Best-selling cars Top50 Models ranking | 2014 Forecast Annual volume forecast Annual volume trend Monthly volume forecast Executive Summary Country Country invelene mporro tem hita dolut porpore scient. -

Car Wars 2020-2023 the Rise (And Fall) of the Crossover?

The US Automotive Product Pipeline Car Wars 2020-2023 The Rise (and Fall) of the Crossover? Equity | 10 May 2019 Car Wars thesis and investment relevance Car Wars is an annual proprietary study that assesses the relative strength of each automaker’s product pipeline in the US. The purpose is to quantify industry product trends, and then relate our findings to investment decisions. Our thesis is fairly straightforward: we believe replacement rate drives showroom age, which drives market United States Autos/Car Manufacturers share, which drives profits and stock prices. OEMs with the highest replacement rate and youngest showroom age have generally gained share from model years 2004-19. John Murphy, CFA Research Analyst Ten key findings of our study MLPF&S +1 646 855 2025 1. Product activity remains reasonably robust across the industry, but the ramp into a [email protected] softening market will likely drive overcrowding and profit pressure. Aileen Smith Research Analyst 2. New vehicle introductions are 70% CUVs and Light Trucks, and just 24% Small and MLPF&S Mid/Large Cars. The material CUV overweight (45%) will likely pressure the +1 646 743 2007 [email protected] segment’s profitability to the low of passenger cars, and/or will leave dealers with a Yarden Amsalem dearth of entry level product to offer, further increasing an emphasis on used cars. Research Analyst MLPF&S 3. Product cadence overall continues to converge, making the market increasingly [email protected] competitive, which should drive incremental profit pressure across the value chain. Gwen Yucong Shi 4.