Macvisit: Luzhou Laojiao Invest in the Future, Learn from the Past

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

葡萄酒 House Pouring Wine

葡萄酒 House Pouring Wine 150ml 750ml 有气的葡萄酒 Sparkling Wine Glass Bottle SP101 Pol Remy Brut Nv (France) $12 $44 白葡萄酒 White Wine W201 Bellevie Pavillon Sauvignon Blanc (France) $11 $40 W202 Pierre Jean Colombard Chardonnay (France) $12 $44 W203 De Bortoli DB Family Selection $13 $50 Sauvignon Blanc (Australia) 红葡萄酒 Red Wine R301 Bellevie Pavillon Merlot (France) $11 $40 R302 Pierre Jean Merlot (France) $12 $44 R303 De Bortoli DB Family Selection $13 $50 Cabernet Sauvignon (Australia) 葡萄酒促销 Wine Promotion *Special deal with minimum purchase of 2 bottles house pouring wine to entitle to 15% discount off from the usual price listed above. Prices subjected to prevailing GST and Service Charge. 消费税与服务费另计。 All photos are meant for reference only. Presentation of dishes may vary without prior notice. 照片只供参考之用,摆设更改恕不作另行通知。 主酒单 Master Wine List 150ml 750ml 有气的葡萄酒 Sparkling Wine Glass Bottle SP101 Pol Remy Brut Nv (France) $12 $44 Pol Remy is produced in Burgundy, France from classic wine varieties perfect for the production of sparkling wine. It is light, fresh and fruity with aromas of apple and peach. With a delightfully easy-drinking style, it exudes aromas of creamy lemon and peach. The palate is gently off-dry and flows through to a satisfying finish. 香槟 Champagne CH102 Henri Abele Brut NV (France) $110 Pale golden colour with greenish highlights. Remarkably fine bubbles and a beautiful, persistent bead. Attractive and luscious, with hints of hawthorn and acacia blossoms as well as overtones of peach and apricot. Exceptional ripeness on the palate. Toasty, honey, and cinnamon flavours. This elegant cuvée has a full bodied, generous aftertaste. -

FTSE Publications

2 FTSE Russell Publications 01 October 2020 FTSE Value Stocks China A Share Indicative Index Weight Data as at Closing on 30 September 2020 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) Agricultural Bank of China (A) 4.01 CHINA Fuyao Glass Group Industries (A) 1.43 CHINA Seazen Holdings (A) 0.81 CHINA Aisino Corporation (A) 0.52 CHINA Gemdale (A) 1.37 CHINA Shanghai Fosun Pharmaceutical Group (A) 1.63 CHINA Anhui Conch Cement (A) 3.15 CHINA GoerTek (A) 2.12 CHINA Shenwan Hongyuan Group (A) 1.11 CHINA AVIC Investment Holdings (A) 0.61 CHINA Gree Electric Appliances Inc of Zhuhai (A) 7.48 CHINA Shenzhen Overseas Chinese Town Holdings 0.66 CHINA Bank of China (A) 2.23 CHINA Guangdong Haid Group (A) 1.24 CHINA (A) Bank Of Nanjing (A) 1.32 CHINA Guotai Junan Securities (A) 1.99 CHINA Sichuan Chuantou Energy (A) 0.71 CHINA Bank of Ningbo (A) 2 CHINA Hangzhou Hikvision Digital Technology (A) 3.56 CHINA Tbea (A) 0.86 CHINA Beijing Dabeinong Technology Group (A) 0.56 CHINA Henan Shuanghui Investment & Development 1.49 CHINA Tonghua Dongbao Medicines(A) 0.59 CHINA China Construction Bank (A) 1.83 CHINA (A) Weichai Power (A) 2.09 CHINA China Life Insurance (A) 2.14 CHINA Hengtong Optic-Electric (A) 0.59 CHINA Wuliangye Yibin (A) 9.84 CHINA China Merchants Shekou Industrial Zone 1.03 CHINA Industrial and Commercial Bank of China (A) 3.5 CHINA XCMG Construction Machinery (A) 0.73 CHINA Holdings (A) Inner Mongolia Yili Industrial(A) 6.32 CHINA Xinjiang Goldwind Science&Technology (A) 0.74 -

Luzhou Laojiao Co., Ltd. 2018 Annual Report April 2019

2018 Annual Report of Luzhou Laojiao Co.,Ltd. Luzhou Laojiao Co., Ltd. 2018 Annual Report April 2019 1 2018 Annual Report of Luzhou Laojiao Co.,Ltd. Section I Important Statements, Contents and Definitions The Board of Directors, Board of Supervisors, directors, supervisors and senior management guarantee that the information presented in this report is free of any false records, misleading statements or material omissions, and shall Individually and together be legally liable for truthfulness, accuracy and completeness of its contents. Mr. Liu Miao, responsible person for the Company, Ms. Xie Hong, responsible person for accounting work and Mr. Yan Li, responsible person for the Company’s financial affairs (Accounting Supervisor) have warranted that the financial statements in this report are true and complete. Other directors attended the board meeting to deliberate this report by themselves except the following directors. Name of directors who did not Position of directors who did not Reason for not attending Name of attend the meeting in person attend the meeting in person the meeting in person deputies Liu Miao Chairman of the Board work Lin Feng Shen Caihong Director work Jiang Yuhui Affected by risks, uncertainties and assumptions, the forward-looking statements concerning business objectives and future plans made in this report based on the subjective assumptions and judgments of the future policies and economic conditions may be significantly different from the actual results. Such statements shall not be considered as virtual promises of the Company to investors, and the investors and relevant persons shall maintain adequate risk awareness and shall understand the differences between plans, forecasts and commitments. -

China Consumer Close-Up

January 13, 2015 The Asian Consumer: A new series Equity Research China Consumer Close-up The who, what and why of China’s true consumer class Few investing challenges have proven more elusive than understanding the Chinese consumer. Efforts to translate the promise of an emerging middle class into steady corporate earnings have been uneven. In the first of a new series on the Asian consumer, we seek to strip the problem back to the basics: Who are the consumers with spending power, what drives their consumption and how will that shift over time? The result is a new approach that yields surprising results. Joshua Lu Goldman Sachs does and seeks to do business with +852-2978-1024 [email protected] companies covered in its research reports. As a result, Goldman Sachs (Asia) L.L.C. investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Sho Kawano Investors should consider this report as only a single factor +81(3)6437-9905 [email protected] Goldman Sachs Japan Co., Ltd. in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Becky Lu Appendix, or go to www.gs.com/research/hedge.html. +852-2978-0953 [email protected] Analysts employed by non- US affiliates are not registered/ Goldman Sachs (Asia) L.L.C. qualified as research analysts with FINRA in the U.S. January 13, 2015 Asia Pacific: Retail Table of contents PM Summary: A holistic view of the Asian consumer 3 China’s cohort in a regional context (a preview of India and Indonesia) 8 What they are buying and what they will buy next: Tracking 7 consumption desires 11 Seven consumption desires in focus 14 1. -

Pacer CSOP FTSE China A50 ETF Schedule of Investments July 31, 2020 (Unaudited) Shares Value COMMON STOCKS - 98.0% Agriculture - 1.6% Muyuan Foodstuff Co Ltd

Page 1 of 4 Pacer CSOP FTSE China A50 ETF Schedule of Investments July 31, 2020 (Unaudited) Shares Value COMMON STOCKS - 98.0% Agriculture - 1.6% Muyuan Foodstuff Co Ltd. - Class A 9,230 $ 120,977 Wens Foodstuffs Group Co Ltd. - Class A 4,660 15,857 136,834 Auto Manufacturers - 0.7% SAIC Motor Corp Ltd. - Class A 24,600 64,077 Banks - 23.7% Agricultural Bank of China Ltd. - Class H 352,300 163,039 Bank of China Ltd. - Class H 193,900 92,512 Bank of Communications Co Ltd. - Class A 184,100 125,556 China CITIC Bank Corp Ltd. - Class H 24,700 18,261 China Construction Bank Corp. - Class H 81,500 71,464 China Everbright Bank Co Ltd. - Class H 126,400 68,456 China Merchants Bank Co Ltd. - Class A 108,200 539,489 China Minsheng Banking Corp Ltd. - Class A 254,300 201,851 Industrial & Commercial Bank of China Ltd. - Class A 198,400 140,993 Industrial Bank Co Ltd. - Class A 127,400 285,849 Ping An Bank Co Ltd. - Class A 75,000 143,348 Shanghai Pudong Development Bank Co Ltd. - Class A 132,300 196,379 2,047,197 Beverages - 17.9% Jiangsu Yanghe Brewery Joint-Stock Co Ltd. - Class A 4,000 77,398 Kweichow Moutai Co Ltd. - Class A 4,000 961,777 Wuliangye Yibin Co Ltd. - Class A 16,200 504,835 1,544,010 Building Materials - 1.6% Anhui Conch Cement Co Ltd. - Class H 15,900 139,921 Coal - 0.5% China Shenhua Energy Co Ltd. -

Kweichow Moutai Growth Declines on Slow Deliveries

CHINA DAILY Tuesday, October 30, 2018 BUSINESS 17 Kweichow Moutai growth Execs optimistic on import expo By WANG YING in Shanghai products, their know-how, “Shanghai has become a [email protected] and how interesting they are vital center for advanced as a company,” said Brian technology leadership — for Top multinational corpora- Duperreault, president, CEO ABB and the world ... We will tions’ executives have and director of finance cor- make full use of the city’s declines on slow deliveries expressed their enthusiasm poration American Interna- existing advantages and for the first China Internation- tional Group Inc. make clear the main challen- al Import Expo set to launch According to Severin ges facing Shanghai, focus Share price of on Nov 5, as part of the nation’s Schwan, CEO of Roche Group, support policies on measures efforts to expand opening-up. the pharmaceuticals giant that can address the challen- liquor maker slips While attending the 30th will showcase its cutting-edge ges, and develop specific but consumption International Business Lead- technology at the import plans and solutions,” Spies- ers’ Advisory Council, held expo, covering early research shofer said, explaining the upgrades to buoy annually in Shanghai, busi- and development, integrated company’s rationale. ness leaders said they are diagnosis and treatment solu- “We are not only seeing future prospects optimistic about China’s tions, and personalised progress in Shanghai’s reform opening-up policy and new healthcare offerings. and opening-up, but we at By ZHU WENQIAN in Beijing opportunities. Roche are taking an active role and YANG JUN in Guiyang “The import expo is in the development of China’s unprecedented in China for biomedical industry. -

Jpmorgan Funds - China A-Share Opportunities Fund

Fund House of the Year Fund Selector Asia Awards - Singapore3) Singapore 2021 - Greater China/China Equity - Platinum4) FOR SINGAPORE INVESTORS ONLY SINGAPORE RECOGNISED SCHEME FACT SHEET | July 31, 2021 JPMorgan Funds - China A-Share Opportunities Fund INVESTMENT OBJECTIVE PERFORMANCE To provide long-term capital growth by investing primarily inCUMULATIVE PERFORMANCE (%) companies of the People's Republic of China (PRC). JPM China A-Share Opportunities A (acc) - USD CSI 300 (Net)1) EXPERTISE 300 200 Fund Manager Howard Wang, Rebecca Jiang 250 150 % CHANGE FUND INFORMATION (JPMorgan Funds - China A-Share Opportunities Fund) 200 100 Fund base currency Launch Date REBASED 150 50 CNH 11/09/15 Total fund size (m) Inception NAV 100 0 USD 8,051.8 USD 15.61 50 -50 ISIN code 08/15 08/16 08/17 08/18 08/19 08/20 08/21 LU1255011170 Since 11/09/15 Current charge Since 1 month 3months 1 year 3 years 5 years Initial : Up to 5.0% of NAV launch Redemption : Currently 0% (Up to 0.5% of NAV) A (acc) - USD (NAV to NAV) -7.9 -4.4 20.8 98.6 143.2 149.4 Management fee : 1.5% p.a. A (acc) - USD (Charges applied)* -12.3 -9.0 15.0 89.2 131.5 137.4 Subscription Channel Benchmark (in USD)1) -6.7 -4.9 12.3 52.4 69.1 59.2 Cash A (acc) - RMB (NAV to NAV) -8.0 -4.5 11.8 88.4 136.4 151.7 SRS(for platforms only) A (acc) - RMB (Charges applied)* -12.4 -9.0 6.4 79.4 125.1 139.7 RATINGS A (acc) - SGD (NAV to NAV) -7.3 -2.6 19.0 97.4 - 105.5 A (acc) - SGD (Charges applied)* -11.8 -7.2 13.3 88.0 - 95.7 Morningstar Analyst Rating Silver Morningstar Rating™ ★★★★★ ANNUALISED -

Premium China Funds Management

Premium China Fund Top 10 Portfolio Holdings as at 31 July 2020 Tencent (Media & Entertainment) Market Cap: USD 660.2 Billion • Tencent, a world leader in the internet-related services space, provides services across instant messaging, social media, email, web-portals, e-commerce, advertising, online payment as well as multiplayer games. • With offerings including QQ Instant Messenger and WeChat, Tencent is providing similar services to the likes of Facebook, Twitter and WhatsApp. By the end of Q2 2018, QQ had 803 million monthly active user accounts, whilst WeChat, since its launch in 2011, accommodates for over 1 Billion monthly active users. • In November 2017, Tencent's market value reached US$528 billion, surpassing Facebook’s market value at the time, which resulted in it being recognised as one of the world's top 5 most valuable public companies. Alibaba Group (Retailing) Market Cap: USD 681.2 Billion • Alibaba, an e-commerce giant, provides services ranging from web portals connecting businesses and consumers, electronic payment services and internet infrastructure. • Its flagship site Alibaba.com is the world’s largest online business-to-business trading platform for small businesses, handling sales between importers and exporters from over 240 countries. whilst its consumer-to-consumer portal—Taobao functions similar to eBay featuring nearly a billion products. Currently, it is amongst one of the 20 most visited websites globally on a consistent basis. • Global brands such as Nike, Uniqlo and Burberry, use Alibaba’s Tmall platform to market to an estimated 300 million shoppers. The companies online payment platform—Alipay is larger than PayPal and accounts for roughly half of all online payment transactions within China. -

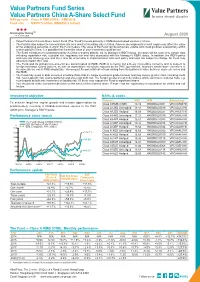

Value Partners Fund Series Value Partners China A-Share Select Fund

Value Partners Fund Series Value Partners China A-Share Select Fund NAV per unit : Class A RMB (CNH) – RMB19.19 Fund size : USD57.3 million (RMB393.2 million) HHH Morningstar RatingTM1 As at 31-08-2020 August 2020 • Value Partners China A-Share Select Fund (The “Fund”) invests primarily in RMB-denominated equities in China. • The Fund is also subject to concentration risk as a result of investing only in China. Adverse developments in such region may affect the value of the underlying securities in which the Fund invests. The value of the Fund can be extremely volatile and could go down substantially within a short period of time. It is possible that the entire value of your investment could be lost. • The Fund intends to invest predominantly in China A-shares directly, via its Manager’s RQFII quota. Investors will be subject to certain risks including repatriation risk, custodial risk, regulatory risk and risks associated with the Manager’s RQFII status. In addition, the RQFII policy and rules are relatively new and there may be uncertainty in implementation and such policy and rules are subject to change. All these may adversely impact the Fund. • The Fund and its primary investments are denominated in RMB. RMB is currently not a freely convertible currency and is subject to foreign exchange control policies, as well as repatriation restrictions imposed by the PRC government. Investors whose base currencies of investments are not in RMB should take into account the potential risk of loss arising from fluctuations in value between such currencies and the RMB. -

2020 Annual Report

AUGUST 31, 2020 2020 Annual Report iShares, Inc. • iShares ESG Aware MSCI EM ETF | ESGE | NASDAQ • iShares MSCI Emerging Markets ex China ETF | EMXC | NASDAQ • iShares MSCI Emerging Markets Min Vol Factor ETF | EEMV | Cboe BZX • iShares MSCI Emerging Markets Multifactor ETF | EMGF | Cboe BZX • iShares MSCI Global Min Vol Factor ETF | ACWV | Cboe BZX Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of each Fund’s shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report. You may elect to receive all future reports in paper free of charge. Ifyou hold accounts throughafinancial intermediary, you can follow the instructions included with this disclosure, if applicable, or contact your financial intermediary to request that you continue to receive paper copies ofyour shareholder reports. Please note that not all financial intermediaries may offer this service. Your election to receive reports in paper will apply to all funds held with your financial intermediary. If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive electronic delivery of shareholder reports and other communications by contactingyour financial intermediary. Please note that not all financial intermediaries may offer this service. -

China Weigao Reducer Success Case (Large Enterprise Version) Serial Company Name Serial Company Name

China Weigao reducer success case (large enterprise version) serial Company Name serial Company Name 1 Shanghai Automobile Group Co., Ltd. 231 Chongqing Textile Holding (Group) Company 2 Dongfeng Motor Corporation 232 Aoyang Group Co., Ltd. 3 Huawei Investment Holdings Co., Ltd. 233 Guangxi Shenglong Metallurgy Co., Ltd. 4 China Ordnance Equipment Group Corporation 234 Lingyuan Iron and Steel Group Co., Ltd. 5 China Minmetals Corporation 235 Futong Group Co., Ltd. 6 China FAW Group Corporation 236 Yongfeng Group Co., Ltd. 7 China Ordnance Industry Corporation 237 Shandong Taishan Iron and Steel Group Co., Ltd. 8 Beijing Automobile Group Co., Ltd. 238 Xinjiang Zhongtai (Group) Co., Ltd. 9 Shandong Weiqiao Venture Group Co., Ltd. 239 Guangdong Haida Group Co., Ltd. 10 China Aviation Industry Corporation 240 Jiangsu Yangzijiang Shipbuilding Group Corporation 11 Zhengwei International Group Co., Ltd. 241 Shenzhen Oufeiguang Technology Co., Ltd. 12 China Baowu Iron and Steel Group Co., Ltd. 242 Dongchen Holding Group Co., Ltd. 13 Lenovo Holdings Co., Ltd. 243 Xinjiang Goldwind Technology Co., Ltd. 14 China National Chemical Corporation 244 Wanji Holding Group Co., Ltd. 15 Hegang Group Co., Ltd. 245 Tsingtao Brewery Co., Ltd. 16 China Shipbuilding Industry Corporation 246 Tasly Holding Group Co., Ltd. 17 Guangzhou Automobile Industry Group Co., Ltd. 247 Wanfeng Auto Holding Group Co., Ltd. 18 Aluminum Corporation of China 248 Wuhan Institute of Posts and Telecommunications 19 China National Building Material Group Co., Ltd. 249 Red Lion Holdings Group Co., Ltd. 20 Hengli Group Co., Ltd. 250 Xinjiang Tianye (Group) Co., Ltd. 21 CRRC Corporation Limited 251 Juhua Group Company 22 Xinxing Jihua Group Co., Ltd. -

Luzhou Laojiao Co., Ltd. 2020 Interim Report

2020 Interim Report of Luzhou Laojiao Co., Ltd. Luzhou Laojiao Co., Ltd. 2020 Interim Report August 2020 1 2020 Interim Report of Luzhou Laojiao Co., Ltd. Section I Important Statements, Contents and Definitions The Board of Directors, Board of Supervisors, as well as directors, supervisors and senior management other than the following directors, supervisors and senior management that have expressed dissent against this report guarantee that the information presented in this report is free of any false records, misleading statements or material omissions, and shall individually and together be legally liable for truthfulness, accuracy and completeness of its contents. Liu Miao, responsible person for the Company, Xie Hong, responsible person for accounting work and Yan Li, responsible person for the Company’s financial affairs (Accounting Supervisor) have warranted that the financial statements in this report are true and complete. All the directors attended the board meeting to deliberate this report by themselves. Affected by risks, uncertainties and assumptions, the forward-looking statements concerning business objectives and future plans made in this report based on the subjective assumptions and judgments of the future policies and economic conditions may be significantly different from the actual results. Such statements shall not be considered as virtual promises of the Company to investors, and the investors and relevant persons shall maintain adequate risk awareness and shall understand the differences between plans, forecasts and commitments. The Company has no interim dividend plan, either in the form of cash or stock. This Report has been prepared in both Chinese and English. Should there be any discrepancies or misunderstandings between the two versions, the Chinese version shall prevail.