Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Directory Establishment

DIRECTORY ESTABLISHMENT SECTOR :RURAL STATE : MADHYA PRADESH DISTRICT : Anuppur Year of start of Employment Sl No Name of Establishment Address / Telephone / Fax / E-mail Operation Class (1) (2) (3) (4) (5) NIC 2004 : 0501-Fishing 1 HARFEEN H.NO.23 VILLAGE BAWDHWATOLA THASIL ANUPPUR DIST. ANUPPUR PIN CODE: NA , STD CODE: 2000 10 - 50 NA , TEL NO: NA , FAX NO: NA, E-MAIL : N.A. NIC 2004 : 1010-Mining and agglomeration of hard coal 2 PRINCIPAL GOVERNMENT HIGH SCHOOL GIRARI TEHSIL PUSHPRAJGARH DISTRICT ANUPPUR PIN CODE: 2000 101 - 500 484881, STD CODE: NA , TEL NO: NA , FAX NO: NA, E-MAIL : N.A. 3 COLE MINES VILLAGE BARTARAI TAHSIL KOTMA DIST. ANUPPUR PIN CODE: NA , STD CODE: NA , TEL NO: 1999 > 500 NA , FAX NO: NA, E-MAIL : N.A. NIC 2004 : 1531-Manufacture of grain mill products 4 AMA TOLA SWA SAYATHA SAMOH VILLAGE UFARIKHURD TASHIL PUSHPARAJGARH DISTRICT ANUPPUR PIN CODE: 484881, STD 2002 10 - 50 CODE: NA , TEL NO: 1, FAX NO: NA, E-MAIL : N.A. NIC 2004 : 1544-Manufacture of macaroni, noodles, couscous and similar farinaceous products 5 AMARBATI SWA SAYATHA SAMOH VILLAGE BENDI TAHSIL PUSHPRAJGARH DISTRTCT ANUPPUR PIN CODE: 484881, STD CODE: 2001 10 - 50 NA , TEL NO: NA , FAX NO: NA, E-MAIL : N.A. 6 NARMADA SWA SAYATHA SAMOH H.NO.31, KARRA TOLA TAHSIL ANUPPUR DISTRICT ANUPPUR PIN CODE: NA , STD CODE: NA , 2002 10 - 50 TEL NO: NA , FAX NO: NA, E-MAIL : N.A. 7 BACHHE LAL SINGH VILLAGE DHANPURI PUSAHPRAJGARH DIST. ANUPPUR PIN CODE: NA , STD CODE: NA , TEL NO: 2002 10 - 50 NA , FAX NO: NA, E-MAIL : N.A. -

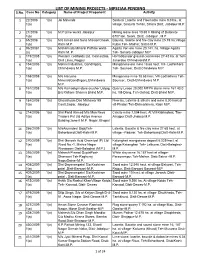

LIST of MINING PROJECTS - MPSEIAA PENDING S.No

LIST OF MINING PROJECTS - MPSEIAA PENDING S.No. Case No Category Name of Project Proponent Activity 1 22/2008 1(a) Jai Minerals Sindursi Laterite and Haematite mine 9.0 ha.. at 1(a) village, Sindursi Tehsil, Sihora Distt. Jabalpur M.P. 2 27/2008 1(a) M.P Lime works Jabalpur Mining lease area 10.60 h Mining of Dolomite 1(a) 6707 ton. Seoni, Distt. Jabalpur , M.P 3 65/2008 1(a) M/s Ismail and Sons MissionChowk, Bauxite, laterite and fire clay mine 25.19 ha.Village 1(a) Katni M.P . Kubin Teh- Maihar, Satna M.P. 4 96/20081 1(a) M/sNirmala Minaral Pathale ward- Agaria Iron ore mine 20.141. ha. Village Agaria (a) Katni M. P. Teh- Sehora Jabalpur M.P 5 119/2008 1(a) Western coalfields Ltd, Coal estate, Harradounder ground coal mines 27-45 ha. at Teh- 1(a) Civil Lines, Nagpur Junerdeo ChhindwaraM.P. 6 154/2008 1(a) Mohini Industries, Gandhiganj, Manganese ore mine 18.68 hect. Vill- Lodhikhera 1(a) Chhindwara M.P. Teh- Souncer, Distt.Chindwara M.P. 7 158/2008 1(a) M/s Haryana Manganese mine 18.68 hect. Vill-Lodhikhera Teh- 1(a) MineralsGandhiganj,Chhindwara Souncer, Distt-Chhindwara M.P. M.P. 8 161/2008 1(a) M/s Kamadigiri store crusher Udyog Quarry Lease 20,000 MTPA stone mine 161 43.0 1(a) Brij Kishore Sharma Bhind M.P. ha. Vill-Dang, Teh-Gohad, Distt-Bhind M.P. 9 184/2008 1(a) Ghanshyam Das Mahawar 95 Fireclay, Laterite & silica's and mine 8.00 hact.at 1(a) Cantt.Sadar, Jabalpur vill-Pindari Teh-Dhimarkhera, Katni M.P. -

Portrait of Population Madhya Pradesh

CENSUS OF INDIA, 1981 A PORTRAIT OF POPULATION MADHYA PRADESH Draft by M. L. SHARMA Deputy Director and M. G. MOHRIL .A ssistant Director DIRECTORATE OF CENSUS OPERATIONS MADHYA PRADESH BHOPAL (iii) ,,' 7f ,,' eI MADHYA PRADESH ADMINISTRATIVE DIVISIONS 1981 . " ,,' ..! DiStRICT HEAOI)UART~RS 'AHSILH(,I,OQUAATERS. t,Whlllll1t MI'IIt Gl dlltrict or tahilidillirl fr'Om tht n~lI\tm d~ ~rag~uQrtm or 1M tahiti IltQdqulrter, It hal bun ~ho\l'rt . wll~,ft bracklls thU1 (BASTAR) (Gira) 0 ..Z ~ ri e , ltuttr ~fiI " 114+16r 4ltlrid $ o",Arta klolotl to Cttio talilil 01 0Il1/t 'Utrltk II J .. Arft klo"ll• .!ttlJQiltlll' t'~lil, I I 3 so· I MADHYA PRADESH COMMUNICATIONS . , . " ,t ,f ~ , A\ \ ~ IOUNDm,SUTE ;8 OISHICI H~~ll SUTE miTAl .. UILVAY, iMAOGAU.f • IIEHEmU. NHMWmH. lOAD, NATlml~I;IIWAY .. STAlE Hr,HvAY KI[OMEHfS 32 0 32 64 96 121160 .Shontr; t~III1I.1 ~Illior dhlii(t. I LJ .iOL:J;o;;;oi . ArlO \,Io~ .. t. {)QIIQ \Qhsil Qt OI\iQ dil\ri,t, " Auo biron" 10 ~O~~oI9~r tQ~,11 (v) J(b)-364 R.G. Illllia/NDl 88 (vii) '''l i .f' z ~ % i til .'\' III 0 4 ...c ti: a:: ..::> G. • 4 ~ ... ~ % c cI 0 I-e 2 4 1&1 S; "/.,I&. k 0 0 0 c c 0 0 0 0 0 $ S $ 4 en ... 8 ~ ... ,.. ~ .. - :J IX ~ ... ... N ~ (J\ .. - . (000100 ~I ) I. Z ~e 0 - :~~ , ~ ""..J ..... 4 ~ ~ A- S 0 ..• a. :> I t ~ '> ~ I -0 Z .... :; -.. ;.~ ...0 ~~~ 0 0 0 0 0 0 0 0 c 0 0 0 0 0 0 0 0 CD S 0 CD ID 04 0 ~ ~ N N N ~ ~ .. -

Madhya Pradesh Urja Vikas Nigam Limited Page 94

Request for Proposal for Grid Connected SPPs in Madhya Pradesh under PM KUSUM - A Scheme a) In consideration of the [Insert name of the Bidder] (hereinafter referred to as (Bidder) submitting the response to Request for Proposal (RFP) for Selection of Solar Power Developer for Design, Engineering, Supply, Installation, Testing and Commissioning including construction of bay and related switchgear at sub-station along with Comprehensive Operation & Maintenance (for twenty-five (25) Operational Years of Grid Connected Solar based Power Plants (SPPs) of aggregate capacity of approximate 225 MW for Sale of Solar Power to MPPMCL at the delivery point in each substation at various locations in the state of Madhya Pradesh, India in response to the RFP dated ____________issued by Madhya Pradesh Urja Vikas Nigam Limited (hereinafter referred to as Nodal Agency) and Nodal Agency considering such response to the RFP of [insert the name of the RPG] (which expression shall unless repugnant to the context or meaning thereof include its executers, administrators, successors and assignees) and selecting the Project of the RPG and issuing LOA No. ____to (Insert Name of RPG) as per terms of RFP and the same having been accepted by the selected Project Company, M/ s {a Special Purpose Vehicle (SPV) formed for this purpose}, if applicable]. As per the terms of the RFP, the [insert name & address of bank] hereby agrees unequivocally, irrevocably and unconditionally to pay to Nodal Agency at [Insert Name of the Place from the address of the Nodal Agency] forthwith -

Madhya Pradesh.Xlsx

Madhya Pradesh S.No. District Name of the Address Major Activity Broad NIC Owner Emplo Code Establishment Description Activity ship yment Code Code Class Interval 130MPPGCL (POWER SARNI DISTT POWER 07 351 4 >=500 HOUSE) BETUL(M.P.) DISTT GENERATION PLANT BETUL (M.P.) 460447 222FORCE MOTORS ARCADY, PUNE VEHICAL 10 453 2 >=500 LTD. MAHARASHTRA PRODUCTION 340MOIL BALAGHAT OFFICER COLONEY MAINING WORK 05 089 4 >=500 481102 423MARAL YARN KHALBUJURG A.B. CLOTH 06 131 2 >=500 FACTORY ROAD MANUFACTRING 522SHRI AOVRBINDO BHOURASALA HOSPITAL 21 861 3 >=500 MEDICAL HOSPITAL SANWER ROAD 453551 630Tawa mines pathakheda sarni COOL MINING WORK 05 051 1 >=500 DISTT BETUL (M.P.) 460447 725BHARAT MATA HIGH BAJRANG THREAD 06 131 1 >=500 SCHOOL MANDAWAR MOHHALLA 465685 PRODUCTION WORK 822S.T.I INDIA LTD. PITHAMPUR RING MAKING OF 06 141 2 >=500 ROAD 453332 READYMADE CLOTHS 921rosi blue india pvt.ltd sector no.1 454775 DAYMAND 06 239 3 >=500 COTIND&POLISING 10 30 SHOBHAPUR MINSE PATHAKERA DISTT COL MININING 05 051 4 >=500 BETUL (M.P.) 440001 11 38 LAND COLMINCE LINE 0 480442 KOLMINCE LAND 05 089 1 >=500 OFFICE,MOARI INK SCAPE WORK 12 44 OFFICE COAL MINES Bijuri OFFICE COAL COAL MINES 05 051 1 >=500 SECL BILASPUR MINES SECL BILASPUR Korja Coliery Bijuri 484440 13 38 W.C.L. Dist. Chhindwara COL MINING 05 051 4 >=500 480559 14 22 SHIWALIK BETRIES PANCHDERIYA TARCH FACTORY 06 259 2 >=500 PVT. LTD. 453551 15 33 S.S.E.C.N. WEST Katni S.S.E.C.N. RIPERING OF 10 454 1 >=500 RAILWAY KATNI WEST RAILWAY MALGADI DEEBBE KATNI Nill 483501 16 44 Jhiriya U.G.Koyla Dumarkachar Jhiriya CAOL SUPPLY WORK 06 239 4 >=500 khadan U.G.Koyla khadan Dumarkachar 484446 17 23 CENTURY YARN SATRATI 451228 CENTURY YARN 06 141 4 >=500 18 21 ret spean pithampur 454775 DHAGA PRODUCTS 06 131 4 >=500 19 21 hdfe FEBRICATION PITHAMPUR 454775 FEBRICATION 06 141 2 >=500 20 29 INSUTATOR ILE. -

Iv Iv Iii Iii I I Ii Ii V V Vi Vii Vii Vi

ROAD NETWORK OF MADHYA PRADESH PINHAT LEGEND 3-6 ATER KOSAD AMBAHA PRATAPPUR 2-10 ITAWA RD. 2-2 PRITHVIPURA PORSA SUNARPURA 2 DIMANI 3-2 PAWAI 2-4 FUF NATIONAL HIGHWAY 2 JAWASA 3-1 3-3 2-7 SINHONIYA 19 BHIND HARICHA GORMI CHOURELA RD. 15 2-3 2-11 11 NEW DECLARED NATIONAL HIGHWAY MORENA 92 KANAWAR LAWAN TEHARA 2-1 UMARI BAGCHINI MEHGAON 2-9 GOHAD 2-8 TEHARGUR VICHAULA KOHAR GONAHARDASPURA BHAROLI NATIONAL HIGHWAY Declared In Principle 3-8 NOORABAD 2 3-4 3-5RITHORAKALA BARASO 3-10 SHANICHARA SUMABALI GWALIOR RD. KAROLI 3-13 19 2 JOURA MAHARAJPURA GATA 2-6 S- 1 1-22 AMAYAN MIHONA STATE HIGHWAY KAILARASH MAU 2 SEMAI 12 BASOTA GWALIOR 15 SABALGARH PURANI JAIL 1-8 2-3 Gopalpur 1 Murar RANGAWA 3-11 LAHAR 23 3-12 PAHARGARH 1-3 NEW DECLARED STATE HIGHWAY TIGRA 1-6 1-1 1-18 LASHKAR 1-17 MOHANPUR 1-2BEHAT DANDAKHIRAK SINGPUR SEONDA SYAMPUR TENTRA 4-8 2 1-21 4-1 DEVGARH 5-5 45 PANIHAR 1-4 4-10 1-19 GIJORA 5-4 VIJAYPUR BHAGUAPURA 2-12 MDR (BOT TOLL+ANNUITY) BHANWARPURA CHOURAI NADIGAON JIGANIYA IKLOD GHATIGON MAKODA 1-5 4-2 JANGIPUR DABOH 1-7 KHOJIPURA 1-13 1-16 1-14 IV RAMESHWAR MOHANA ARON CHINOR PICHHOR MDR (ADB IV) INDARGARH MDR- 17 1-9 6 1-20 PATAI LANCH5-3 KARAHIYA CHHIMAK1-15 PALI UMARI DABARA S- 2 DHOBANI RANIGHATI 1-23 5-8 1-10 5-7 MANPUR 1-12 1 4-6 7-11 MDR (PWD) 23 GOWARDHAN GORAGHAT 45 HARSI DHORIYA 3 1-11 KHURAI BHITARWAR TEKNA CHITOLI 7-12 75 7-16 SANWADA 19 1 SHEOPUR 7-2 PAWAYA MDR- 16 7-6 GOPALPUR MAGRONI BHANDER BAIRAD AINCHWADA 5-6 KHATOLI PREMSAR 11 BARGAWAN State Capital 4-3 6 7-8 DATIAV 5-2 8 6 7-17 NARWAR 4-5 2 KAMAD 4-9 BILWARA 5-1 UNNAV 7-13 IV CHIRGAON District Headquarter 4-7 JHIRI 7-7 7-5 GORAS 6 POHARI AMOLPATHA SANDARI AWDA SATANWADA 12 KARAHAL 7-18 8 23 SHIVPURI KARERA JHANSI 34-12 UTTARPRADESH BORDER CHECK POST 24 Nos. -

Total - 512 Fathers/ Pump Details of Solar Name of Installation Company S

Total - 512 Fathers/ Pump Details of Solar Name Of Installation Company S. No. Husband Village Block Tahshil District Capacity (in Type of Beneficiary Capacity Date Name Name Wp) Pump 1 2 3 4 5 6 7 8 9 10 11 12 Dynamech Kishan Lal Bala Prsasd Pariyat 1 Panagar Panagar Jabalpur 3000 Wp DC Sub. 3 HP DC 07/12/2017 Electropower Upadhya Upadhya Mangva Pvt.Ltd. Ram Dynamech Bharat Lal Gandhi 2 Naresh Sihora Sihora Jabalpur 3000 Wp DC Sub. 3 HP DC 10/12/2017 Electropower Patel Gram Patel Pvt.Ltd. Dynamech Tej Bahadur Jeet Lal Gaurha 3 Manjholi poda Jabalpur 3000 Wp DC Sub. 3 HP DC 12/12/2017 Electropower Mourya Mourya Bhitoni Pvt.Ltd. Kamlesh Dynamech 4 Kumar D N saxena Narayanpur Jabalpur Jabalpur Jabalpur 3000 Wp DC Sub. 3 HP DC 21/12/2017 Electropower Saxena Pvt.Ltd. Satya Dynamech 5 Vijay Jaggi Prakash Umariya Jabalpur Jabalpur Jabalpur 3000 Wp DC Sub. 3 HP DC 28/11/2017 Electropower Jaggi Pvt.Ltd. Dynamech Jimal 6 Rabiya Bee Chargava Chargava Shahpura Jabalpur 3000 Wp DC Sub. 3 HP DC 21/12/2017 Electropower Ahmad Pvt.Ltd. Dynamech Santaram Siya ram 7 Kaladehi Jabalpur Jabalpur Jabalpur 3000 Wp DC Sub. 3 HP DC 08/02/2018 Electropower Chouksey Chouksey Pvt.Ltd. Dynamech Ram lal 8 Pritam Lal Bargawa Sihora Sihora Jabalpur 3000 Wp DC Sub. 3 HP DC 26/02/2018 Electropower Haldar Pvt.Ltd. Dynamech Ram Prasad Baarelal Badiya 9 Panagar Panagar Jabalpur 3000 Wp DC Sub. 3 HP DC 12/02/2018 Electropower Patel Patel Kheda Pvt.Ltd. -

Kundam Patan Sihora Bargi RURAL VACCINATION CENTERS Kundam

RURAL VACCINATION CENTERS SR.N SR.N BLOCK NAME VACCINATION CENTERS BLOCK NAME VACCINATION CENTERS O. O. 1 CHC Shahpura 66 SHC Jhirmila 2 PHC Belkheda 67 SHC pipariya Bagharaji 3 PHC Chargawa 68 SHC Badkur 4 SHC Sihoda 69 PHC Imali 5 SHC Jamuniya 70 Kundam SHC Soopawara 6 SHC SaheJpur 71 SHC Jamgavn 7 SHC Dharampura 72 SHC Makhrar 8 SHC Kohla 73 SHC Mohni 9 SHC Mnakedi 74 SHC Chourai 10 SHC Nichi 75 CHC Patan 11 SHC Sukha 76 PHC Katangi 12 SHC Kishronda 77 PHC Boriya 13 Shahpura SHC Chaprat 78 SHC Sarond 14 SHC Cheerapodi 79 SHC Bineki 15 SHC Umariya 80 SHC Badoda chhedi 16 SHC Bheeroghat 81 SHC Belkheda 17 SHC Bilpathar 82 SHC Kunwarpur 18 SHC Nayanagar 83 Patan SHC Thana 19 SHC Sunwara 84 SHC Murrai 20 SHC Barmaan 85 SHC Nunsar 21 SHC Gubhra kala 86 SHC Kakrehta 22 SHC Bilpathar 87 SHC Chattarpur 23 SHC Bheeta 88 SHC Sakra 24 SHC Billha 89 SHC Kaimori 25 SHC Bijori 90 SHC Katra Belkheda 26 CHC Majholi 91 SHC Gadaghat 27 PHC Indrana 92 SHC Kusali Luhari 28 SHC Talad 93 CH Sihora 29 SHC Sihoda 94 PHC Gosalpur 30 SHC Khand 95 PHC Khitola 31 SHC Amgawa devri 96 PHC Majhagwa 32 SHC Pola 97 SHC Mosam 33 SHC Devri Rajwai 98 SHC Darolikla 34 Majholi SHC Ponda 99 SHC Ramkhiriya 35 SHC Darshni 100 SHC Jughari 36 SHC Umariya dhirha 101 Sihora SHC Bela 37 SHC Bargi 102 SHC Ghandigram 38 SHC Badkhera 103 SHC Dharmpura 39 SHC Dinari khamariya 104 SHC Madha 40 SHC Hardua kalan 105 SHC Agariya 41 SHC Shajpura 106 SHC Phanwani 42 SHC Kanjai 107 SHC Makura 43 SHC Khinni 108 SHC Budhari 44 CHC Panagar 109 SHC Kumhi 45 PHC Sonpur 110 PHC Bargi 46 PHC Belkhadu -

Jabalpur District Madhya Pradesh

JABALPUR DISTRICT MADHYA PRADESH Ministry of Water Resources Central Ground Water Board North Central Region BHOPAL 2013 JABALPUR DISTRICT AT A GLANCE S.No. Items Statistics 1 General Information i) Geographical Area 5655.34 Km2 ii) Administrative Division Number of Tehsil 4/7 Number of Panchayat/ Villages 542/1458 iii) Population 2460714 iv) Average Annual Rainfall 1279.50 mm 2. Geomorphology 1. Major Physiographic Units i) Vindhyan track ii) South eastern plateau iii) Bhitri Ganj range 2. Major Drainage i) Narmada river and its tributaries ii) Chhoti Mahanadi & its tributary 3. Land use (Km2) a) Forest Area 777 b) Net area sown 2738 c) Gross croped area 3718 4. Major Soil Types 1. Loamy to sandy loamy 2. medium black and deep black 5. Principal Crops Paddy,Maize,wheat,Mustard,Arhar etc. 6. Irrigation By Different Sources No. Area irrigated Km2 Dug Wells 8010 261 Tube wells/Bore wells 8832 815 Tanks/Ponds 36 1 Canals 56 940 Other sources 853 161 Net Irrigation Area 1174 Gross Irrigated Area 1332 7. Number of Ground Water Monitoring Wells of CGWB (As on 31.03.2013) Number of Dug Wells 19 No. Piezometers 07 8. Predominant Geological Formations Recent : Alluium, Gondwana, Vidhyan. 9. Hydrogeology Major Water Bearing Formation Alluvium joint & fractured Granite and Sand stone Pre monsoon depth to water level during 2012 0.37 to 10.20 mbgl Post monsoon depth to water level during 2012 2.30 to 16.80 mbgl Long term water level trend in 10 years (2003- Fall 0.02-0.2 m/year (Pre-monsoon) 2013) Rise 0.01-0.14 m/year (Pre-monsoon) 0.34-1.36 m/year (Post- monsoon) 10. -

Sq.Km.) Phuphkalan Total Population – 72 627 (In Thousand) Gormi Bhind Districts – 51 Akoda of MADHYA PRADESH Morena Mehgaon Tehsil – 367

74°10'0"E 75°11'0"E 76°12'0"E 77°13'0"E 78°14'0"E 79°15'0"E 80°16'0"E 81°17'0"E 82°18'0"E FACTS OF MADHYA PRADESH SH 2 UV UVS H URBAN LOCAL BODY MAP Ambah 2 Porsa Geographical Area – 308 (Thousand Sq.Km.) Phuphkalan Total Population – 72 627 (In Thousand) Gormi Bhind Districts – 51 Akoda OF MADHYA PRADESH Morena Mehgaon Tehsil – 367 UV S UV H S Bhind Blocks – 313 Gohad H 2 1 Jhundpura 9 ULB WISE AREA (Sq.Km) Joura Tribal Blocks – 89 Kailaras S.No. ULB Name Area(SQ.KM) S.No. ULB Name Area(SQ.KM) S.No. ULB Name Area(SQ.KM) Mihona Town (Census 2011) – 476 1 Agar 5.29 101 Dhamnod 13.10 201 Majholi 3.03 Mau 2 Ajaygarh 6.03 102 Dhamnod 14.40 202 Makdon 14.90 Sabalgarh 3 Akoda 1.28 103 Dhanpuri 20.90 203 Maksi 11.20 Gwalior Total Villages – 54903 4 Akodia 10.30 104 Dhar 24.80 204 Malanjkhand 81.20 N 23 Morena 5 Alampur 6.45 105 Dharampuri 4.26 205 Malhargarh 1.08 H Lahar S N " 6 Alirajpur 23.80 106 Dindori 10.30 206 Manasa 8.43 Nagar Nigam (July, 2015) – 16 UV " 7 Alot 3.57 107 Dongar Parasia 5.72 207 Manawar 9.57 Seondha 0 8 Amanganj 5.47 108 Gadarwara 18.50 208 Mandav 25.20 ' 9 Amarkantak 47.20 109 Gairatganj 12.70 209 Mandideep 56.80 0 Nagar Palika – 98 ' 0 10 Amarpatan 5.09 110 Ganj Basoda 6.58 210 Mandla 3.10 0 ° 11 Amarwara 11.80 111 Garhakota 3.32 211 Mandla 2.67 Vijaypur 9 12 Ambah 3.43 112 Garhi Malhera 20.00 212 Mandleshwar 1.09 1 Nagar Parishad – 272 ° H 6 Bilaua 13 Amla 4.81 113 Garoth 10.70 213 Mandsaur 34.50 Gwalior S 14 Anjad 8.17 114 Gohad 12.80 214 Mangawan 9.73 UV Daboh 6 2 15 Antari 5.49 115 Gormi 2.69 215 Manpur 4.25 Gram -

Service Electors Voter List

FINAL ELECTORAL ROLL - 2021 STATE - (S12) MADHYA PRADESH No., Name and Reservation Status of Assembly Constituency: 95-PATAN(GEN) Last Part No., Name and Reservation Status of Parliamentary Service Constituency in which the Assembly Constituency is located: 13-JABALPUR(GEN) Electors 1. DETAILS OF REVISION Year of Revision : 2021 Type of Revision : Special Summary Revision Qualifying Date :01/01/2021 Date of Final Publication: 15/01/2021 2. SUMMARY OF SERVICE ELECTORS A) NUMBER OF ELECTORS 1. Classified by Type of Service Name of Service No. of Electors Members Wives Total A) Defence Services 187 3 190 B) Armed Police Force 0 0 0 C) Foreign Service 0 0 0 Total in Part (A+B+C) 187 3 190 2. Classified by Type of Roll Roll Type Roll Identification No. of Electors Members Wives Total I Original Mother roll Integrated Basic roll of revision 187 3 190 2021 II Additions Supplement 1 After Draft publication, 2021 0 0 0 List Sub Total: 0 0 0 III Deletions Supplement 1 After Draft publication, 2021 0 0 0 List Sub Total: 0 0 0 Net Electors in the Roll after (I + II - III) 187 3 190 B) NUMBER OF CORRECTIONS/MODIFICATION Roll Type Roll Identification No. of Electors Supplement 1 After Draft publication, 2021 0 Total: 0 Elector Type: M = Member, W = Wife Page 1 Final Electoral Roll, 2021 of Assembly Constituency 95-PATAN (GEN), (S12) MADHYA PRADESH A . Defence Services Sl.No Name of Elector Elector Rank Husband's Address of Record House Address Type Sl.No. Officer/Commanding Officer for despatch of Ballot Paper (1) (2) (3) (4) (5) (6) (7) Assam Rifles -

Telephone Directory of Delivery Points in Madhya Pradesh

Telephone Directory of Delivery Points in Madhya Pradesh June 2015 Supported by MPTAST 2 Index: S.no. Topic Page Number Bhopal Division 3 -13 1a District Bhopal 4 1b District Betul 5-6 1c District Hoshangabad 7 1d District Harda 8 1e District Raisen 9 1f District Rajgarh 10 1g District Sehore 11-12 1h District Vidisha 13 Indore Division 14-25 2a Alirajpur 15 2b Barwani 16-17 2c Burhanpur 18 2d Dhar 19 2e Indore 20 2f Jhabua 21 2g Khandwa 22-23 2h Khargone 24-25 Ujjain Division 26-34 3a Agar 27 3b Dewas 28 3c Mandsaur 29 3d Neemuch 30 3e Ratlam 31 3f Shajapur 32 3f Ujjain 33-34 Gwalior Division 35-44 4a Ashoknagar 36 4b Bhind 37 4c Datia 38 4d Guna 39 4e Gwalior 40 4f Morena 41 4g Sheopur 42 4h Shivpuri 43-44 Sagar Division 45-55 5a Damoh 46-47 3 5b Chhattarpur 48-49 5c Panna 50-51 5d Sagar 52-53 5e Tikamgarh 54-55 Jabalpur Division 56-70 6a Balaghat 57-58 6b Chindwara 59-60 6c Dindori 61 6d Jabalpur 62-63 6e Katni 64-65 6f Mandla 66-67 6g Narsinghpur 68 6h Seoni 69-70 Rewa Division 71-80 7a Anuppur 72 7b Rewa 73 7c Satna 74-75 7d Shahdol 76-77 7e Sidhi 78 7f Singrauli 79 7g Umaria 80 4 BHOPAL DIVISION MR N BH D GL R SO P DT A SV P TK M NM C AK N CT P RWA GU N PA N ST N S DH MD S SG L SJ P RJ G VD S SA G DM H KT N UM R SD L RT M UJ N BPL RS N JBP SE H J BA NS P DD R AN P ID R DH R DW S HS B MD L AL R HA R SN I KN D CD W BR W KR G BT L BL G BH P 5 6 District Bhopal Delivery Type of Level of Land Line Facility S.No District Contact no.