FACT BOOK Textron Inc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Security & Defence European

a 7.90 D European & Security ES & Defence 2/2018 International Security and Defence Journal COUNTRY FOCUS: MALAYSIA ISSN 1617-7983 • www.euro-sd.com • March 2018 Unmanned Maritime Systems Game Changer for EU Defence? Spain: Increasing Funds for Defence 25 member states established the ”Permanent Seven new programmes are to be scheduled Structured Cooperation“ (PESCO). for the next 15 years. Politics · Armed Forces · Procurement · Technology The backbone of every strong troop. Mercedes-Benz Defence Vehicles. When your mission is clear. When there’s no road for miles around. And when you need to give all you’ve got, your equipment needs to be the best. At times like these, we’re right by your side. Mercedes-Benz Defence Vehicles: armoured, highly capable off-road and logistics vehicles with payloads ranging from 0.5 to 110 t. Mobilising safety and efficiency: www.mercedes-benz.com/defence-vehicles Editorial The Balkans Are Losing Their Illusions At the beginning of the year, Bulgaria strategy”. If this were true, the authors took over the presidency of the European would have performed a particularly great Council. The six months in which a Mem- service by giving the term a new content. ber State exercises this honorary position, So far, it has been assumed that a strategy before passing on the baton to the next indicates how a goal should be achieved. capital city, are too short for course- However, this document offers only vague setting. Certainly, at least for a moment, hints. Instead, it lists once again what the President of the Council can put issues requirements applicants must fulfil in or- that are important to him on the agenda. -

WARNING: This Price List Is Protected by U. S. Copyright Law and Unfair and Deceptive Competition Laws

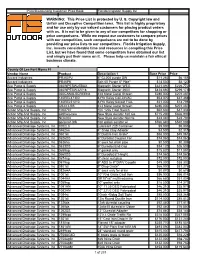

Price/Discounting Customer Price Book Florida Irrigation Supply Inc WARNING: This Price List is protected by U. S. Copyright law and Unfair and Deceptive Competition laws. This list is highly proprietary and for use only by our valued customers for placing product orders with us. It is not to be given to any of our competitors for shopping or price comparisons. While we expect our customers to compare prices with our competition, such comparisons are not to be done by providing our price lists to our competitors. Florida Irrigation Supply, Inc. invests considerable time and resources in compiling this Price List, but we have found that some competitors have obtained our list and simply put their name on it. Please help us maintain a fair ethical business climate. County Of Lee Fort Myers Fl Vendor Name Product Description 1 Base Price Price Accord Industries PR200PJ 6" CL200 purple SW $11.282 $6.155 Accord Industries PR40PK Sch 40 Purple 8" Pipe" $14.530 $8.120 Ace Pump & Supply 030WPESW25BAX Magnetic Starter WEG $321.890 $226.772 Ace Pump & Supply 030WPESW32V18 Magnetic Starter 460V $424.660 $299.173 Ace Pump & Supply 060CANALSCREEN4 4x4 Metal Canal Screen $286.000 $201.487 Ace Pump & Supply 140REL47300 8 Pin Relay Coil 24VAC $53.070 $37.388 Ace Pump & Supply 140REL51210 8 Pin Relay Socket F/UL $21.000 $14.795 Ace Pump & Supply CS4X3-SS 4x3 Metal Canal Screen $286.000 $201.487 Action Mfg And Supply, Inc 1002707 10ft 120v Float Switch $62.630 $47.336 Action Mfg And Supply, Inc a20hws-new New Style Aerator 160 Ga $715.200 $666.996 Action -

1C7duo6na 640331.Pdf

1 Table of Contents Common Items .......................................................................................................................................................................................................... 4 Services ....................................................................................................................................................................................................................... 6 Medical Equipment & Drugs .................................................................................................................................................................................... 7 Individual Item Descriptions .................................................................................................................................................................................. 7 Hand Weapons .......................................................................................................................................................................................................... 9 Armour....................................................................................................................................................................................................................... 10 Individual Item Descriptions ................................................................................................................................................................................ 10 Ranged Weapons .................................................................................................................................................................................................. -

2011 FACT BOOK Textron Inc

2011 FACT BOOK Textron Inc. is an $11.3 billion multi-industry company operating in 25 countries with approximately 32,000 employees. The company leverages its global network of aircraft, defense and intelligence, industrial and finance businesses to provide customers with innovative solutions and services. Textron is known around the world for its powerful brands such as Bell Helicopter, Cessna Aircraft, E-Z-GO, Greenlee, Jacobsen, Kautex, Lycoming, Textron Systems and Textron Financial Corporation. Textron Inc. consists of numerous subsidiaries and operating divisions. Please refer to the back cover for legal entity structure. KEY EXECUTIVES Scott C. Donnelly was named chief executive officer in December 2009 and chairman of the board in September 2010. Donnelly joined Textron as executive vice president and chief operating officer in June 2008 and was promoted to president in January 2009. Prior to joining Textron, Donnelly was president and CEO for General Electric (GE) Aviation. He also held various other management positions since joining GE in 1989. Scott C. Donnelly Scott A. Ernest John L. Garrison Jr. Frederick M. Strader Chairman and Cessna Aircraft Bell Helicopter Textron Systems Chief Executive Officer President and CEO President and CEO President and CEO Frank T. Connor joined Textron as executive vice president and chief financial officer in August 2009. Connor came to Textron after a 22-year career at Goldman, Sachs & Co. where, most recently, he was managing director and head of Telecom Investment Banking. Prior to that, he served as Goldman, Sachs & Co.’s chief operating officer of Telecom, Technology and Media Investment Banking. Frank T. Connor J. -

Soldier Systems Technology Roadmap

SOLDIER SYSTEMS TECHNOLOGY ROADMAP CAPSTONE REPORT AND ACTION PLAN SUPPORTING THE FUTURE SOLDIER SUPPORTING CANADIAN INDUSTRY SOLDIER SYSTEMS TECHNOLOGY ROADMAP CAPSTONE REPORT AND ACTION PLAN Abstract The Soldier Systems Technology Roadmap Capstone Report and Action Plan captures and summarizes the findings of the Development Phase of the Soldier Systems Technology Roadmap (2011–2025) (SSTRM) initiative. The SSTRM is a groundbreaking industry-government collaboration focused on enhancing the operational effectiveness of the future Canadian soldier and the competitiveness of Canadian industry through open innovation. Led by the Department of National Defence (DND)—with participation from Army and Materiel branches and Defence Research and Development Canada (DRDC)—and Industry Canada (IC), the initiative enjoys the strong support of the Canadian Association of Defence and Security Industries (CADSI) and of Technopôle Defence and Security (TDS). Applying roadmapping principles and processes to Canadian Forces soldier modernization efforts, the initiative involves industry and academia collaboratively in a comprehensive knowledge-sharing platform to articulate future needs and identify capability gaps, related challenges and potential technology solutions for the Canadian soldier of the future. The report includes an Action Plan that highlights the key R&D priorities identified by the soldier systems community of interest and makes recommendations for next steps in the initiative to encourage industry, academia and government collaboration -

Powerful Performance: Powerful Future

POWERFUL PERFORMANCE: POWERFUL FUTURE Fact Book 2007 Tex tron > www.textron.com Textron Inc. is a $13.2 billion multi-industry company operating in 34 countries with > NYSE: TXT approximately 44,000 employees. The company leverages its global network of aircraft, > 2007 Fortune 500 ranking: 194 industrial and finance businesses to provide customers with innovative solutions > Fortune Magazine’s America’s Most Admired and services. Textron is known around the world for its powerful brands such as Aerospace & Defense Company in 2008 Bell Helicopter, Cessna Aircraft Company, Jacobsen, Kautex, Lycoming, E-Z-GO, > Number of employees: 44,000 – 20 percent are Greenlee, Fluid & Power, Textron Systems and Textron Financial Corporation. outside the U.S. > Number of countries with manufacturing Textron Inc. consists of numerous subsidiaries and operating divisions. Please refer to back cover for operations: 20 legal entity structure. Textron is an Equal Opportunity Employer. Key Executives Financial Highlights (Dollars in millions except per share data) 2007 2006 Change Revenues $ 13,225 $ 11,490 15% International revenues % 39% XX% 39% — Segment profit 1 $ 1,640 $ 1,267 29% Income from continuing operations $ 915 $ 706 30% Total debt – Manufacturing group 2 $ 2,148 $ 1,800 19% Shareholders’ equity $ 3,507 $ 2,649 32% Common Share Data 3 Lewis B. Campbell Diluted EPS from continuing operations $ 3.59 $ 2.71 32% Chairman, President and Dividends per share $ 0.85 $ 0.78 9% Chief Executive Officer Diluted average common shares outstanding (in thousands) 254,826 260,444 (2)% Lewis Campbell was named CEO in July 1998 Key Performance Metrics ROIC 4 24.8% 16.8% — and appointed chairman in February 1999.