The Difference 2017 Outlook Welcome the Difference 17 Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Na Fianna Nuacht

Na Fianna Nuacht Senior Camogie Team In Championship Final Following last Sunday’s fantastic semi-final win over St Vincents, our Senior Camogie team play St Judes in Division 1 Championship on Final, this Sunday at 3.30pm in St Peregrines and they’re looking for you your support. This is Na Fianna's second Senior Camogie Championship final appearance in two years, and it’s great to be back again. Camogie has gone through a very strong revival in Na Fianna in recent times with playing numbers at all levels increasing year on year. Na Fianna has four adult teams in Championship reflecting the strong growth of Camogie in the club. One would have to go back to the days of twelve a-side Camogie to find a time when Na Fianna last fielded four competitive adult teams. Sunday’s Senior squad and their success in getting to another Championship final is a tribute to this unique set of players who have played together and played for each other over the last while. The team has had a few retirees and injuries from last year's finalists so as a result it is a much younger team. The squad is a very good mix of established players and young players at the very start of their adult playing career. Special credit and thanks goes to Senior Management team of Brendan Skehan, Fiona Greene, Darragh Muleady, David Hughes, Fran Gray, Dee Quinn and Austin Rock who have worked tirelessly with this group of players. All in Na Fianna wish the Ladies and the management team the very best of luck Na Fianna Nuacht 19ú Deireadh Fómhair 2018 1 Na Fianna Nuacht Weekend Fixtures Our AFL8’s play Peregrines in Blanchardstown IT this Friday at 8pm. -

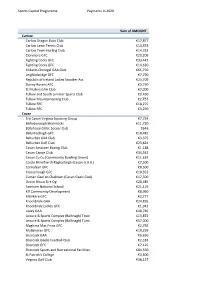

Sports Capital Programme Payments in 2020 Sum of AMOUNT Carlow

Sports Capital Programme Payments in 2020 Sum of AMOUNT Carlow Carlow Dragon Boat Club €17,877 Carlow Lawn Tennis Club €14,353 Carlow Town Hurling Club €14,332 Clonmore GFC €23,209 Fighting Cocks GFC €33,442 Fighting Cocks GFC €14,620 Kildavin Clonegal GAA Club €61,750 Leighlinbridge GFC €7,790 Republic of Ireland Ladies Snooker Ass €23,709 Slaney Rovers AFC €3,750 St Mullins GAA Club €7,000 Tullow and South Leinster Sports Club €9,430 Tullow Mountaineering Club €2,757 Tullow RFC €18,275 Tullow RFC €3,250 Cavan 3rd Cavan Virginia Scouting Group €7,754 Bailieborough Shamrocks €11,720 Ballyhaise Celtic Soccer Club €646 Ballymachugh GFC €10,481 Belturbet GAA Club €3,375 Belturbet Golf Club €23,824 Cavan Amatuer Boxing Club €1,188 Cavan Canoe Club €34,542 Cavan Co Co (Community Bowling Green) €11,624 Coiste Bhreifne Uí Raghaillaigh (Cavan G.A.A.) €7,500 Cornafean GFC €8,500 Crosserlough GFC €10,352 Cuman Gael an Chabhain (Cavan Gaels GAA) €17,500 Droim Dhuin Eire Og €20,485 Farnham National School €21,119 Kill Community Development €8,960 Killinkere GFC €2,777 Knockbride GAA €24,835 Knockbride Ladies GFC €1,942 Lavey GAA €48,785 Leisure & Sports Complex (Ballinagh) Trust €13,872 Leisure & Sports Complex (Ballinagh) Turst €57,000 Maghera Mac Finns GFC €2,792 Mullahoran GFC €10,259 Shercock GAA €6,650 Shercock Gaelic Football Club €2,183 Shercock GFC €7,125 Shercock Sports and Recreational Facilities €84,550 St Patrick's College €3,500 Virginia Golf Club €38,127 Sports Capital Programme Payments in 2020 Virginia Kayak Club €9,633 Cavan Castlerahan -

549033 DC Fixture Book 2011.Indd

EOLAIRE CAMÓGAÍOCHTA 2011 CAMOGIE DIRECTORY 2011 1 Visit www.dublincamogie.ie for latest news and photos Visit www.dublincamogie.ie for latest news and photos 1 BEST WISHES TO ALL From OZO 24/7 COLLECT & RECYCLE OZO are one of Dublin’s largest waste management providers with over 6,000 Commercial & Domestic Customers in Dublin alone. We are a Dublin owned company based in Inchicore and we are in operation since 1978. We have over 30 trucks doing waste collections in the following areas: If you are interested in getting a quotation from OZO for waste disposal please call our sales team on 01-6160610 or email: [email protected] OZO SUPPLY AND COLLECT: • ALL SIZE WHEELIE BINS – DOMESTIC & COMMERCIAL (240litre-1100litre) • GENERAL WASTE, MIXED RECYCLING WASTE, GLASS BOTTLE WASTE, HAZARDOUS WASTE, ELECTRONIC WASTE, COMPOST WASTE OZO SUPPLY SKIPS TO COMMERCIAL & DOMESTIC CUSTOMERS WE HAVE ALL DIFFERENT SIZES – MIDI, STANDARD, LARGE, ROLL ON, ROLL OFF OZO ALSO COLLECT CARDBOARD & PLASTIC BALES FROM COMMERCIAL SITES OZO ARE PROUD SPONSORS & SUPPORTERS OF DUBLIN CAMOGIE Dublin Camogie Fixtures Book 2011 Contents: Focal ón gCathaoirleach ................................................................................. 2 Management Committee & County Team Management ................................ 3 Club Contact Lists........................................................................................... 7 Minor Board Guidelines ............................................................................... 49 Under 8 Rules .............................................................................................. -

Na Fianna Nuacht

Na Fianna Nuacht Club Lotto This week’s Na Fianna Club Lotto winning numbers were; 2 12 17 27 No jackpot winner. Four Match 3 winners, each winning €35 – Richard Currie, Tom Ryan, Finola Grahan and Kay Clifford c/o Vinny Lucky Pick winners, each getting €15 were; Niall Ó Ceallacháin, Philip Hannon, Catherine Reymonde c/o Vinny, Dee Maher and Phyllis Carroll. Next Jackpot: €6,000, please support. Members’ Subscriptions Members are reminded that subscriptions for the current year became due and payable immediately following the Club’s AGM last October. All GAA Registrations were submitted on 1st April as per regulation, and any member whose membership was unpaid on that date was not included in this Registration as per Club policy. The consequences of this are that unregistered players are no longer insured to play or train and do so at their own risk. In addition, teams playing unregistered players could be adjudged an illegal team and suffer the loss of points and even elimination from competitions. Members’ subs can be paid in the bar on Wednesday nights between 6.30pm and 9pm and again on Saturday mornings from 9am to 11am. Payments by card, cheque and cash will be accepted. Subscriptions can also be paid at the club office, Mon to Fri, 9am to 1pm. Na Fianna Golf Society Na Fianna Golf Society’s next outing will be to Luttrellstown on Monday 16th June. Tee time reserved from 2.30-4pm, new members always welcome, please contact Ciaran Gray for timesheet 0872269133. Na Fianna Nuacht 6ú Meitheamh 2014 1 Na Fianna Nuacht Weekend Action League hurling this weekend when tomorrow, Saturday 7th June at 6.30pm our Senior hurlers play O’Tooles away and Inters play Kevins in Mobhi Road. -

Secretary's Report 2019 for Agm 19

SECRETARY'S REPORT 2019 FOR AGM 19 September 2019 Cumann Lúthchleas Gael Na Fianna Cruinniú Cinn Bhliana 2019 Áras Na Fianna Clár (a) Adoption of Standing Orders (b) President's Address (c) Minutes of AGM 20 September 2018 (d) Secretary's Report (i) Juvenile Chairman Presentation (ii) Adult Games Chairman Presentation (e) Treasurer's Report (i) Auditors Report (ii) Subs Report (f) Chairman's Address (g) Appointment of Tellers (h) Motion and Election of Officers (i) Motions and Recommendations (j) Any Other Business Page 2 of 49 Standing Orders for Annual General Meeting The proposer of the motion or an amendment thereto, may speak for five minutes but no longer. A person speaking to a motion or amendment shall not exceed three minutes. The proposer of a motion or amendment may speak a second time for five minutes before a vote is taken, but no other person may speak a second time to any motion or amendment. The Chairman shall, at any time he considers that a matter has been sufficiently discussed, call on a proposer to reply, after which a vote must be taken. A person may, with the consent of the Chairman, move ‘that the question now be put after which, when the proposer has spoken a vote must be taken. Page 3 of 49 TUARASCÁIL AN RÚNAÍ 2019 I feel like I blinked and here we are again. Another GAA year done...hard to believe, yet our Club has been very busy since the last AGM and a lot has happened on and off the pitch. To begin the Secretary’s report, I think it would be very fitting of me to recognise and show appreciation to the Club officers that come together every third Tuesday to thrash out requirements, resources, strategy, planning and process. -

Na Fianna Nuacht 270919

Na Fianna Nuacht Football Championship Weekend Preview Following on from our opening encounters against St Sylvester’s and Kilmacud Crokes our Senior Footballers look forward to their final group game of the Dublin Senior Football Club Championship against Ballymun Kickham’s in Parnell Park this Friday at 8.15pm with the aforementioned teams in the group playing directly beforehand. A victory against St Sylvester’s and a subsequent defeat at the hands of Kilmacud Crokes means that the stakes couldn’t be any higher at this stage, from our perspective, with a win for us an absolute requirement in order to progress to the quarter finals stage. A draw would be insufficient as in those circumstances Ballymun Kickhams would progress by virtue of holding a superior point’s difference. While the upcoming match undoubtedly is going to be an intense challenge given the quality of the opposition we will be facing, minds are clearly focused on the task in hand and players and management are all acutely conscious of the level of performance that will be required in order to prevail. While there were certainly positive elements to our performance in the previous group match against Kilmacud Crokes equally there were certain areas that provided scope for improvement and hopefully the players focus and hard work since then will bear fruit in that regard with the achievement of a victory on Friday night. Given that our final two league matches have been deferred we have relied on challenge matches to complete preparations for Friday’s match but in the final analysis what is required now is a Na Fianna Nuacht 27ú Meán Fómhair 2019 1 Na Fianna Nuacht high quality performance to put us in a position to win the game and progress to the knock out stages of the competition. -

Na Fianna Nuacht

Na Fianna Nuacht Weekend Action Best of luck to our Senior and Inter hulers in league on Saturday at 6.30pm. Seniors host neighbours St Vincents in Mobhi Road and Inters travel to Sean Moore Park to play Clanna Gael Fontenoy. Full fixture list on website, best of luck to all teams, all support welcome. Na Fianna’s Dubs Sunday’s big game is the much awaited clash of Dublin and Meath in the Leinster SFC final and best of luck to Jonny Cooper, Tomás Brady, Niall McGovern and Dublin’s footballers. The teams meet in the Leinster final for a third successive year, with Dublin having won the last two. Dublin are bidding for a fourth successive Leinster title and a ninth in ten years. Good luck also to Dublin’s Minor footballers including Na Fianna’s Aaron Byrne, Jack Carey, Cathal Doran, Al Fitzgerald, Ian Jesson, Eoghan McHugh, Eoin Murchan and Glen O’Reilly, in their Leinster final against Kildare on Sunday. Best of luck to Arlene Cushen, Alva Egan, Bláithín McQuillan, Elaine O’Meara and Dublin’s Senior Camogie team in tomorrow’s Championship Group 1 match against Wexford in Parnell Park at 2.30pm. Good luck to Dublin’s Premier Junior Camogie team including including Gráinne Ryan, Ellen Keatley and Cliona McCullough in tomorrow’s Championship match against Down in Portaferry. Good luck to Dublin Minor Ladies footballers, including injured vice captain Na Fianna’s Fiona Tuite in tomorrow’s All-Ireland semi-final against Galway in Birr at 2pm. Na Fianna – Your Pre & Post Match Venue With fantastic specials in the bar and carvery, Na Fianna is the best pre and post-match venue this Sunday. -

Celebrations

10 DUBLIN GAZETTE CITY 1 March 2018 EVENTS No matter what’s happening in your area, Dublin Gazette’s far-ranging photographers have all the events and angles covered Celebrations Special guest on the night, Uachtaran Cumann Luthchleas Gael John Horan, receiving a presentation from Paddy King, president, CLG Na Fianna to mark his appointment as Uachtaran Martin Quilty receiving Na Fianna Club Person of The Year award Jimmy Gray presents Na Fianna Hall Of Fame award to Pat Sullivan from Cormac O Donnchu, chairman, CLG Na Fianna Na Fianna’s Senior 2 Footballers, intermediate championship winners 2017 Na Fianna delight HUGE crowd came along to the onship winning teams (Senior 2 Foot- special guest, Uachtaran Tofa Cumann Bonnington Hotel, Drumcondra ballers, U21A Hurling and Football, Luthchleas Gael John Horan, and to Arecently for Na Fianna’s celebra- Minor A hurling and football, Junior E MC Gavin Duffy. tory dinner dance, with a night to hurling and Senior 7 Camogie), with Rounding out the memorable remember that recognised the tremen- the night also paying tribute to a num- night, former club barman Pat Sul- dous achievements of all Na Fianna ber of Na Fianna’s inter-county award livan was inducted into Na Fianna’s teams in the past year. winners, while top Na Fianna players Hall of Fame, while club stalwart More than 550 people were present were also celebrated. Martin Quilty was awarded Club to salute Na Fianna’s seven champi- A big thanks was given to the night’s Person of the Year.. -

Grid Export Data

Sports Capital and Equipment Programme all organisations registered March 2021 Organisation Name County 4th Carlow Leighlinbrige Scout Group Carlow All Star Sporting and Recreation Ltd Carlow Ardattin Athletic Club Carlow Asca GFC Carlow Askea Karate CLub Carlow Askea Sports Ltd Carlow Bagenalstown AFC Carlow BAGENALSTOWN ATHLETIC CLUB Carlow Bagenalstown Community Games Carlow Bagenalstown Cricket Club Carlow Bagenalstown Family Resource Centre Ltd Carlow Bagenalstown Karate Club Carlow Bagenalstown Pitch & Putt Club Carlow Bagenalstown Swimming Club Carlow Ballinabranna GAA Club Carlow Ballinkillen Hurling Club Carlow Ballinkillen Lorum Community Centre Club Carlow Ballon GAA Club Carlow Ballon Hall Committee Limited Carlow Ballon Karate Club Carlow Ballymurphy Celtic AFC Carlow Ballymurphy Hall Ltd Carlow Ballymurphy Indoor Soccer Club Carlow Barrow Valley Riding Club Carlow Bennekerry N.S Carlow Bigstone Community Centre Carlow Borris Golf Club Carlow Borris Tidy Towns Association Ltd Carlow Borris/St. Mullins Community Games Carlow Burrin Celtic F.C. Carlow Carlow & District Juveniles League Carlow Carlow Basketball Club Carlow Carlow Carsports Club CLG Carlow CARLOW COUNTY COUNCIL Carlow Carlow Cricket Club Carlow Carlow Dragon Boat Club Carlow Carlow Golf Club Carlow Carlow Gymnastics Club Carlow Carlow Hockey Club Carlow Carlow Karate Club Carlow Carlow Kickboxing Club Carlow Carlow Lawn Tennis Club Carlow Carlow Road Cycling Club Carlow Carlow Rowing Club Carlow Carlow Scot's Church Carlow Carlow Special Olympics Club Carlow Carlow -

And Residential Tenancies Act 2016 Inspector's

S. 4(1) of Planning and Development (Housing) and Residential Tenancies Act 2016 Inspector’s Report ABP-305173-19 Strategic Housing Development Construction of 118 build-to-rent no. apartments and associated site works. Location Site bounded by South Link Road (N27), Rockboro Road and Gasworks Road, Cork Planning Authority Cork City Council Applicant Seamus and Evelyn Scally Prescribed Bodies An Taisce The Heritage Council Department of Culture, Heritage and the Gaeltacht Irish Water Transport Infrastructure Ireland ABP-305173-19 Inspector’s Report Page 1 of 57 Bord Gais/Gas Networks Ireland Irish Aviation Authority Health and Safety Authority Observer(s) 18 submissions received- see Appendix A Date of Site Inspection(s) 05th November 2019 Inspector Lorraine Dockery ABP-305173-19 Inspector’s Report Page 2 of 57 1.0 Introduction This is an assessment of a proposed strategic housing development submitted to the An Bord Pleanála under section 4(1) of the Planning and Development (Housing) and Residential Tenancies Act 2016. 2.0 Site Location and Description 2.1. The Inspector’s Report of ABP-304245-19 gives the following description of the site and its surroundings: ‘The site is located in the centre of Cork City adjacent to the South City Link Road, a dual carriageway with the designation N27. The eastern portion of the site bounds the Rockboro Road behind a high stone wall. The southern boundary of the site is adjacent to the side and rear gardens of dwellings. The northern boundary of the site abuts a petrol filling station and the western boundary abuts the South City Link Road. -

An Inspiring Office Development Trinity Quarter Provided a Unique Opportunity to Design a Landmark Building in Cork City Centre

an inspiring office development Trinity Quarter provided a unique opportunity to design a landmark building in Cork city centre. Critical to the success of the building is the contribution it makes to the immediate surrounds and the larger Cork city centre. Close consideration of the urban grain, the location on the River Lee, the rich history of the area, and the architectural heritage surrounding this extraordinary location, all influenced and contributed to the design objectives of the development. Although contemporary in architectural language, the strong vertical proportions of the façade elements compliment the historic buildings and the urban grain of the surrounding architectural conservation area. From entering the building through the naturally lit main atrium space to the wide open views over the city and River Lee, the building exploits all possible benefits of its unique location and lets occupants enjoy the high tech environment of the office and retail spaces in a sun lit and natural environment. The atrium, the landscaped external courtyard as well as open landscaped roof terraces also provide occupants with ample space for informal collaboration and respite. RKD Architects are very enthusiastic about the success of the development and believe that Trinity Quarter will provide unsurpassed quality office space for the discerning tenant. Johan Wilken Director RKD Architects an inspiring office development t t 2 iRelanD’S MOST inSPiRing OFFiCe DevelopmenT 3 www.trinityquarter.com Spacious, sustainable and truly inspirational, Trinity Quarter is a new world-class office development, strategically located in the heart of Cork’s dynamic city centre. Providing corporate occupiers with the valuable opportunity to establish their operation in the midst of a thriving commercial quarter, Trinity Quarter is a unique city centre offering unlike any other currently on the market. -

Unique Retail Opportunities in the Heart of Cork City Because Your Business Deserves a Landmark Location…

UNIQUE RETAIL OPPORTUNITIES IN THE HEART OF CORK CITY BECAUSE YOUR BUSINESS DESERVES A LANDMARK location… From concept through to Like a beacon of light over- By locating in The Elysian, completion, The Elysian looking a city striding with all the advantages of being heralds a new dawn in Irish confidence into the 21st century, part of a high-profile, landmark architecture, a new confidence The Elysian hints at the face of development will be yours to in city development and a new Cork to come. It represents the enjoy — as well as proximity to scale of imagination when it first groundbreaking step in a Patrick Street and the entire comes to creating outstanding planned redevelopment that city-centre, easy access by residential, retail and commercial will transform the docklands road, extensive secure parking spaces in the heart of a thriving area of the city, bringing new and of course the growth urban environment. energy, vibrancy and life to the potential associated with a entire region. newly emerging part of the city. THE ELYSIAN. UNIQUE RETAIL OPPORTUNITIES IN THE HEART OF CORK CITY. THE LOCATION AND SURROUNDINGS SOuth LinK RoaD south MALL PaRK anD RIDE OLIVER PLunKEtt MERchant’S QuaY to coRK aiRPORT TERMinus stREET shoPPinG CEntRE anD WEst coRK citY HALL caR PARK citY HALL LAPP’S QuaY ALBERT RoaD PatRicK’S stREET CLARion HotEL BUS STATION to DubLin / WatERFORD RoaDS anD LittLE isLanD / JacK LYnch tunnEL THE DETAILS GROUND FLOOR ALBERT STREET ALBERT STREET PROXIMITY TO MAIN SHOPPING PRECINCT CAFÉ / RESTAURANT OPPORTUNITY SERVICE YARD OFFICES 6 ALBERT STREET PORT LANE 1 CAR PARK UNIT 1 RETAIL OPPORTUNITY.