(Always) See Scotland: Adjusting the Welsh Block Grant After Tax Devolution

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

House of Commons Welsh Affairs Committee

House of Commons Welsh Affairs Committee S4C Written evidence - web List of written evidence 1 URDD 3 2 Hugh Evans 5 3 Ron Jones 6 4 Dr Simon Brooks 14 5 The Writers Guild of Great Britain 18 6 Mabon ap Gwynfor 23 7 Welsh Language Board 28 8 Ofcom 34 9 Professor Thomas P O’Malley, Aberystwth University 60 10 Tinopolis 64 11 Institute of Welsh Affairs 69 12 NUJ Parliamentary Group 76 13 Plaim Cymru 77 14 Welsh Language Society 85 15 NUJ and Bectu 94 16 DCMS 98 17 PACT 103 18 TAC 113 19 BBC 126 20 Mercator Institute for Media, Languages and Culture 132 21 Mr S.G. Jones 138 22 Alun Ffred Jones AM, Welsh Assembly Government 139 23 Celebrating Our Language 144 24 Peter Edwards and Huw Walters 146 2 Written evidence submitted by Urdd Gobaith Cymru In the opinion of Urdd Gobaith Cymru, Wales’ largest children and young people’s organisation with 50,000 members under the age of 25: • The provision of good-quality Welsh language programmes is fundamental to establishing a linguistic context for those who speak Welsh and who wish to learn it. • It is vital that this is funded to the necessary level. • A good partnership already exists between S4C and the Urdd, but the Urdd would be happy to co-operate and work with S4C to identify further opportunities for collaboration to offer opportunities for children and young people, thus developing new audiences. • We believe that decisions about the development of S4C should be made in Wales. -

Radio Multiplex Licence Variation Request Form

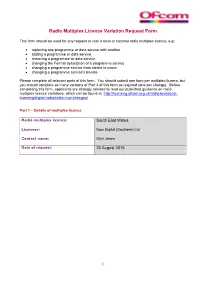

Radio Multiplex Licence Variation Request Form This form should be used for any request to vary a local or national radio multiplex licence, e.g: replacing one programme or data service with another adding a programme or data service removing a programme or data service changing the Format description of a programme service changing a programme service from stereo to mono changing a programme service's bit-rate Please complete all relevant parts of this form. You should submit one form per multiplex licence, but you should complete as many versions of Part 3 of this form as required (one per change). Before completing this form, applicants are strongly advised to read our published guidance on radio multiplex licence variations, which can be found at: http://licensing.ofcom.org.uk/radio-broadcast- licensing/digital-radio/radio-mux-changes/ Part 1 – Details of multiplex licence Radio multiplex licence: South East Wales Licensee: Now Digital (Southern) Ltd Contact name: Glyn Jones Date of request: 25 August 2016 1 Part 2 – Summary of multiplex line-up before and after proposed change(s) Existing line-up of programme services Proposed line-up of programme services Service name and Bit-rate Stereo/ Stereo/ short-form description (kbps)/ Mono Mono Coding (H or F) BBC Radio Wales 128 F J/S BBC Radio Wales 128 F J/S BBC Radio Cymru 128 F J/S BBC Radio Cymru 128 F J/S Heart Wales 128 F J/S Heart Wales 128 F J/S Smooth S.Wales 128 F J/S Smooth S.Wales 128 F J/S Capital S.Wales 128 F J/S Capital S.Wales 128 F J/S Bridge FM 80 F Mono Bridge FM 80 F Mono Nation Radio 112 F J/S Nation Radio 112 F J/S Nation Gold 80 F Mono Dragon Radio 80 F Mono Any additional information/notes: The multiplex also has an EPG (8kbps) Part 3 – Details of proposed change For each proposed change you wish to make to your licence, please answer the following question and then complete the relevant sections of the rest of the application form. -

Enterprise Search & BI from Clearview for Villages Housing Keystone's Component Accounting with Midland Heart Wales

issue 39 | may 2014 | www.housing-technology.com | £6.95 Grampian Housing goes virtual Keystone’s component EDM at Port of Leith with with Castle Computer Services accounting with Midland Heart Invu Page 27 Page 04 Page 30 Enterprise search & BI from Feature article: SMAC your Optevia wins Dynamics CRM Clearview for Villages Housing IT up deal at A2Dominion Page 30 Page 18 Page 15 Trident deploys CGFirst Readers’ letters - risk management Peaks & Plains’ approach to Board Portal on iPads and big data in housing arrears Page 22 Page 28 Page 06 Kypera delivers full suite to 1st Touch launches self-service Wales & West’s free wi-fi with Atrium Homes app Meraki & BT Page 03 Page 10 Page 20 © The Intelligent Business Company 2014. Housing Technology is published by The Intelligent Business Company. Reproduction of any material, in whole or in part, is strictly forbidden without the prior consent of the publisher. 0402 || housing technology | housing management www.housing-technology.com Editor’s Notes Building homes with technology can increase the number of residents that The pressure on social housing stock is they can support through having fewer unused relentless, with most housing providers doing bedrooms among their properties. what they can to build new properties and Many housing providers are well-positioned make best use of their existing properties to to turn their existing in-house services into maximise the number of residents they can commercial propositions that they can sell to accommodate, with particular pressure on other housing providers and local authorities, those operating in the main cities. -

Global-GMG Merger Inquiry: Appendices and Glossary

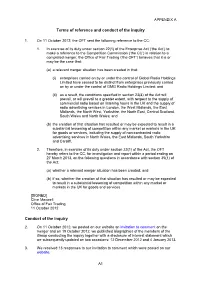

APPENDIX A Terms of reference and conduct of the inquiry 1. On 11 October 2012, the OFT sent the following reference to the CC: 1. In exercise of its duty under section 22(1) of the Enterprise Act (‘the Act’) to make a reference to the Competition Commission (‘the CC’) in relation to a completed merger, the Office of Fair Trading (‘the OFT’) believes that it is or may be the case that: (a) a relevant merger situation has been created in that: (i) enterprises carried on by or under the control of Global Radio Holdings Limited have ceased to be distinct from enterprises previously carried on by or under the control of GMG Radio Holdings Limited; and (ii) as a result, the conditions specified in section 23(4) of the Act will prevail, or will prevail to a greater extent, with respect to the supply of commercial radio based on listening hours in the UK and the supply of radio advertising services in London, the West Midlands, the East Midlands, the North West, Yorkshire, the North East, Central Scotland, South Wales and North Wales; and (b) the creation of that situation has resulted or may be expected to result in a substantial lessening of competition within any market or markets in the UK for goods or services, including the supply of non-contracted radio advertising services in North Wales, the East Midlands, South Yorkshire and Cardiff. 2. Therefore, in exercise of its duty under section 22(1) of the Act, the OFT hereby refers to the CC, for investigation and report within a period ending on 27 March 2013, on the following questions in accordance with section 35(1) of the Act: (a) whether a relevant merger situation has been created; and (b) if so, whether the creation of that situation has resulted or may be expected to result in a substantial lessening of competition within any market or markets in the UK for goods and services. -

A History of the Welsh English Dialect in Fiction

_________________________________________________________________________Swansea University E-Theses A History of the Welsh English Dialect in Fiction Jones, Benjamin A. How to cite: _________________________________________________________________________ Jones, Benjamin A. (2018) A History of the Welsh English Dialect in Fiction. Doctoral thesis, Swansea University. http://cronfa.swan.ac.uk/Record/cronfa44723 Use policy: _________________________________________________________________________ This item is brought to you by Swansea University. Any person downloading material is agreeing to abide by the terms of the repository licence: copies of full text items may be used or reproduced in any format or medium, without prior permission for personal research or study, educational or non-commercial purposes only. The copyright for any work remains with the original author unless otherwise specified. The full-text must not be sold in any format or medium without the formal permission of the copyright holder. Permission for multiple reproductions should be obtained from the original author. Authors are personally responsible for adhering to copyright and publisher restrictions when uploading content to the repository. Please link to the metadata record in the Swansea University repository, Cronfa (link given in the citation reference above.) http://www.swansea.ac.uk/library/researchsupport/ris-support/ A history of the Welsh English dialect in fiction Benjamin Alexander Jones Submitted to Swansea University in fulfilment of the requirements -

2016-17 Annual Report and Accounts

Welsh Centre for International Affairs 2016-2017 Annual Report Clockwise from top: Visitors to the Weeping Window Poppies at Caernarfon Castle; Wales for Peace film project, #MoreinCommon event at the Temple of Peace, Ballet Nimba at the International Development Summit; Caernarfon Peace Trail; Winners of 2016 Wales Schools Debating Championships – Cardiff1 Sixth Form College Our vision, mission and values The Welsh Centre for International Affairs' vision is that everyone in Wales contributes to creating a fair and peaceful world. To achieve this, our mission is to inspire learning and action on global issues. The WCIA believes: That everyone has a contribution to make through active global citizenship In the principles of human rights, international law, peace, tolerance and international cooperation promoted by the United Nations In the power of education, positive engagement and dialogue between individuals and organisations as means to work towards those principles That sustainability is a vital part of all efforts to ensure a safer and more secure world for future generations In the importance of fair treatment of individuals, transparency and accountability in all its affairs 2 Hub Cymru Africa Wales for Peace Contents Contributing to our Strategic Aims 6 Hub Cymru Africa 10 Wales for Peace 13 Education, events and volunteering 16 Temple of Peace – developing the ‘venue with a heart’ 19 Education Financial review 2016-17 21 Events Our partners and funders 24 Volunteering Statement of Trustees’ Responsibilities 27 Financial Statements for the year ended 31 March 2017 for the Welsh Centre for International Affairs 28 3 Message from the Chair 2016 was a momentous year in world affairs. -

(Public Pack)Agenda Dogfen I/Ar Gyfer Pwyllgor Diwylliant, Y Gymraeg a Chyfathrebu, 26/04/2018 09:00

------------------------Pecyn dogfennau cyhoeddus ------------------------ Agenda - Pwyllgor Diwylliant, y Gymraeg a Chyfathrebu Lleoliad: I gael rhagor o wybodaeth cysylltwch a: Ystafell Bwyllgora 2 - Y Senedd Steve George Dyddiad: Dydd Iau, 26 Ebrill 2018 Clerc y Pwyllgor Amser: 09.00 0300 200 6565 [email protected] ------ 1 Cyflwyniad, ymddiheuriadau, dirprwyon a datgan buddiannau 2 Radio yng Nghymru: Sesiwn dystiolaeth 5 (09:00 - 10:00) (Tudalennau 1 - 45) Marc Webber, Uwch Ddarlithydd mewn Newyddiaduraeth a'r Cyfryngau Martin Mumford, Rheolwr Gyfarwyddwr yn Nation Broadcasting Ltd Mel Booth, Rheolwr Gyfarwyddwr Cymru, Global Radio Neil Sloan, Pennaeth Rhaglenni, Communicorp UK 3 Radio yng Nghymru: Sesiwn dystiolaeth 6 (10:00 - 11:15) (Tudalennau 46 - 49) Dafydd Elis-Thomas, y Gweinidog Diwylliant, Twristiaeth a Chwaraeon Hywel Owen, Arweinydd Tîm Polisi'r Cyfryngau, Llywodraeth Cymru Egwyl (11:15 - 11:30) 4 Radio yng Nghymru: Sesiwn dystiolaeth 7 (11:30 - 12:15) Euros Lewis, Ysgrifennydd Cymdeithas Gydweithredol Radio Beca Lowri Jones, Arweinydd Tîm Cymell a Hwyluso, Radio Beca 5 Cynnig o dan Reol Sefydlog 17.42 i benderfynu gwahardd y cyhoedd o'r cyfarfod ar gyfer y busnes a ganlyn: 6 Ystyried y dystiolaeth (12:15 - 12:30) Eitem 2 Mae cyfyngiadau ar y ddogfen hon Tudalen y pecyn 1 Cynulliad Cenedlaethol Cymru / National Assembly for Wales Pwyllgor Diwylliant, y Gymraeg a Chyfathrebu / The Culture, Welsh Language and Communications Committee Radio yng Nghymru / Radio in Wales CWLC(5) RADIO02 Ymateb gan Marc Webber / Evidence from Marc Webber Enclosed is my submission to your forthcoming inquiry into the radio industry in Wales. It is a subject which I have had a long-standing interest in, from my very first job as a reporter on Cardiff's Red Dragon Radio to my role today as a Senior Lecturer in Multimedia Journalism at the University of Northampton. -

QUARTERLY SUMMARY of RADIO LISTENING Survey Period Ending 30Th March 2014

QUARTERLY SUMMARY OF RADIO LISTENING Survey Period Ending 30th March 2014 PART 1 - UNITED KINGDOM (INCLUDING CHANNEL ISLANDS AND ISLE OF MAN) Adults aged 15 and over: population 53,205,000 Survey Weekly Reach Average Hours Total Hours Share in Period '000 % per head per listener '000 TSA % All Radio Q 48063 90 19.5 21.5 1035333 100.0 All BBC Radio Q 35314 66 10.7 16.1 568166 54.9 All BBC Radio 15-44 Q 15408 60 6.7 11.1 171370 40.8 All BBC Radio 45+ Q 19906 72 14.4 19.9 396796 64.5 All BBC Network Radio1 Q 32262 61 9.1 15.0 482606 46.6 BBC Local Radio Q 9263 17 1.6 9.2 85559 8.3 All Commercial Radio Q 34078 64 8.2 12.8 434769 42.0 All Commercial Radio 15-44 Q 18546 72 9.0 12.4 230430 54.9 All Commercial Radio 45+ Q 15532 56 7.4 13.2 204340 33.2 All National Commercial1 Q 16586 31 2.4 7.7 127651 12.3 All Local Commercial (National TSA) Q 27246 51 5.8 11.3 307119 29.7 Other Radio Q 3891 7 0.6 8.3 32398 3.1 Source: RAJAR/Ipsos MORI/RSMB 1 See note on back cover. For survey periods and other definitions please see back cover. Embargoed until 00.01 am Enquiries to: RAJAR, 6th floor, 55 New Oxford St, London WC1A 1BS 15th May 2014 Telephone: 020 7395 0630 Facsimile: 020 7395 0631 e mail: [email protected] Internet: www.rajar.co.uk ©Rajar 2014. -

Welsh Edition

BUMPER GAZETTE WELSH EDITION Y GAZETTE MAWR RHIFYN CYMREIG Cefnogwch y Ddraig… Siaradwch Gymraeg! Thank you to the Welsh Ambassadors for creating this bumper edition of the school Gazette to highlight the initiatives linking Bilingualism and Cwricwlwm Cymreig at St Joseph’s which they and the Welsh Department have been involved with this year. …DIOLCH! ! Introduction - Cyflwyniad As St Joseph’s is an English Medium Secondary School in Wales, we feel that it is very important that we try to use Welsh as much as we can within our school community. As we are on the border of England and Wales, we live in a mainly English speaking area. This means that it is not always easy to practise using Welsh especially since recently there has been a decline in the number of people using Welsh in this area. In the last ten years the number of Welsh speakers in the County of Wrexham has decreased by 1.7% (2001-2011 census), making us feel that we need to do something about this. The Welsh Assembly Government has a target of a million Welsh speakers in Wales by the year 2050, and here at St Joseph’s we are doing as much as possible to help to reach this target and support bilingualism. Over the course of this year, the Welsh ambassadors have done as much as they can to introduce more Welsh into day-to-day life at school. The pupils and staff have all been involved and the majority of them have said that they have benefited from our work. -

Tafwyl Evaluation Background

TAFWYL EVALUATION BACKGROUND Tafwyl is an annual festival celebrating the Welsh language, arts and culture. It was established in 2006 as part of the core work of Menter Caerdydd and this year it celebrated its 15th anniversary in a form rather different to its original format. Tafwyl is an integral part of the wider work of Menter Caerdydd - a charity that promotes and extends the social use of the Welsh language in Cardiff, with the ambition that Welsh plays a central role in life in the capital. Tafwyl’s Main Aims are to: 1. raise the profile of the Welsh language in Cardiff; 2. strengthen the position of the Welsh language in the community; 3. introduce the language and culture to a new audience. It’s a free event, open to all – both Welsh and non-Welsh speakers – and appeals particularly to families, as well as attracting people of all ages and backgrounds. In light of another challenging year of COVID-19 restrictions, and following the success of the 2020 Digital Tafwyl Festival, Menter Caerdydd announced in February this year that the festival would again take the form of a digital event, streamed live from its home in Cardiff Castle. PILOT TEST EVENT As restrictions began to be lifted, the Welsh Government announced that a number of pilot test events would be held to create a robust and safe strategy to allow the arts and live music industry to reopen. With Tafwyl on the shortlist of pilot test events, the team set about planning processes which could be implemented quickly when the green light came to enable the festival to invite an audience of 500 to Tafwyl. -

Reinvention of Welsh Canals +

the welsh + Mererid Hopwood Owain Glyndwˆr and the Welsh dream Adam Price Devolution in reverse Peter Hain Case for the Severn Barrage Jon Owen Jones Costs of Wales’ newest quango Kevin Brennan Rise of the Twitter generation Stephanie Matthews Statins scandal Reinvention of David Reynolds Schools trapped in time warp Helen Birtwhistle Welsh canals Health and social care gap Alison Taylor Still lost in care Trevor Fishlock Magic of the movies Peter Stead Swans fly high www.iwa.org.uk | Winter 2012 | No. 48 | £8.99 The Institute of Welsh Affairs gratefully acknowledges funding support from the Joseph Rowntree Charitable Trust, the Esmée Fairbairn Foundation and the Waterloo Foundation. The following organisations are corporate members: Public Sector Private Sector Voluntary Sector • Aberystwyth University • ABACA Limited • Aberdare & District Chamber • ACAS Wales • Arden Kitt Associates Ltd of Trade & Commerce • Bangor University • Association of Chartered Certified • Alcohol Concern Cymru • BBC Cymru Wales Accountants (ACCA) • Cardiff & Co • Cardiff & Vale College / Coleg Caerdydd • Beaufort Research Ltd • Cartrefi Cymru a’r Fro • BT • Cartrefi Cymunedol Community • Cardiff School of Management • Castell Howell Foods Housing Cymru • Cardiff University • CBI Wales • Cynnal Cymru - Sustain Wales • Cardiff University (CAIRD) • Constructing Excellence in Wales • Cynon Taf Community Housing Group • Cardiff University Library • Core • Disability Wales • Centre for Regeneration Excellence Wales • D S Smith Recycling • EVAD Trust (CREW) • Elan -

2015-16 Annual Report and Accounts

Welsh Centre for International Affairs 2015-2016 Annual Report Clockwise from top: WAGE teacher seminar, Hub Cymru Africa Health Conference, Lindsey Hilsum (Channel 4) at media event, 16-18 year- olds at Mock COP21 conference in the Senedd, WW1 picture, WAGE teacher training 1 Our vision, mission and values The Welsh Centre for International Affairs' vision is that everyone in Wales contributes to creating a fair and peaceful world. To achieve this, our mission is to inspire learning and action on global issues. The WCIA believes: That everyone has a contribution to make through active global citizenship In the principles of human rights, international law, peace, tolerance and international cooperation promoted by the United Nations In the power of education, positive engagement and dialogue between individuals and organisations as means to work towards those principles That sustainability is a vital part of all efforts to ensure a safer and more secure world for future generations In the importance of fair treatment of individuals, transparency and accountability in all its affairs 2 Hub Cymru Africa 10 Wales for Peace 13 Contents Contributing to our Strategic Aims 6 Hub Cymru Africa 10 Wales for Peace 13 Education, events and volunteering 16 Temple of Peace 19 Financial review 2015-16 20 Education Our partners and funders 22 Events Partners during 2015-16 26 Volunteering Statement of Trustees’ Responsibilities 27 Financial Statements for the year ended 31 March 2016 for the Welsh Centre for International Affairs 28 16 3 Message from the Chair The 2015-16 annual report covers the first full year of the WCIA’s work as a larger, more ambitious and even more inclusive charity.