MAJOR TRANSACTIONS in the 1926 DECEMBER WHEAT FUTURE by J

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Writing Home from Around the World, 1926–1927

Writing Home from Around the World, 1926–1927 A keen and amused observer, Tom Johnson is an articulate and conscien- tious letter writer. The reader has the feeling he was writing for himself as much as his family as he makes sentences and paragraphs of his impressions of the world at the height of colonialism. By THOMAS H. JOHNSON Edited with an introduction by LAURA JOHNSON WATERMAN y father, Thomas H. Johnson, the writer of these letters, was born in 1902 on the Connecticut River Valley farm known as Stone Cliff, located one mile north of the vil- Mlage of Bradford. In 1926, upon his graduation from Williams College, Tom Johnson embarked on a world cruise that was to last the length of a school year—September to May. He had been invited to teach Eliza- bethan Drama and American Literature (subjects he soon found to be not particularly relevant) on the fi rst ever student travel experiment. This was launched on a large scale with over fi fty faculty and four hun- dred and fi fty students, one hundred and twenty of them women. A. J. McIntosh, president of the University Travel Association, saw this as an opportunity to combine formal education with travel, and orga- nized the adventure by reaching out to colleges across the country. The project became known as the Floating University and was considered . LAURA JOHNSON WATERMAN is the author of Losing the Garden (2005), a memoir of thirty years of homesteading in East Corinth, Vermont. She co-authored with her late husband, Guy Waterman, fi ve books on the history of climbing the moun- tains of the Northeast and related environmental issues, among them, Forest and Crag (1989), Backwoods Ethics (1993), and Wilderness Ethics (1993). -

Records of the Immigration and Naturalization Service, 1891-1957, Record Group 85 New Orleans, Louisiana Crew Lists of Vessels Arriving at New Orleans, LA, 1910-1945

Records of the Immigration and Naturalization Service, 1891-1957, Record Group 85 New Orleans, Louisiana Crew Lists of Vessels Arriving at New Orleans, LA, 1910-1945. T939. 311 rolls. (~A complete list of rolls has been added.) Roll Volumes Dates 1 1-3 January-June, 1910 2 4-5 July-October, 1910 3 6-7 November, 1910-February, 1911 4 8-9 March-June, 1911 5 10-11 July-October, 1911 6 12-13 November, 1911-February, 1912 7 14-15 March-June, 1912 8 16-17 July-October, 1912 9 18-19 November, 1912-February, 1913 10 20-21 March-June, 1913 11 22-23 July-October, 1913 12 24-25 November, 1913-February, 1914 13 26 March-April, 1914 14 27 May-June, 1914 15 28-29 July-October, 1914 16 30-31 November, 1914-February, 1915 17 32 March-April, 1915 18 33 May-June, 1915 19 34-35 July-October, 1915 20 36-37 November, 1915-February, 1916 21 38-39 March-June, 1916 22 40-41 July-October, 1916 23 42-43 November, 1916-February, 1917 24 44 March-April, 1917 25 45 May-June, 1917 26 46 July-August, 1917 27 47 September-October, 1917 28 48 November-December, 1917 29 49-50 Jan. 1-Mar. 15, 1918 30 51-53 Mar. 16-Apr. 30, 1918 31 56-59 June 1-Aug. 15, 1918 32 60-64 Aug. 16-0ct. 31, 1918 33 65-69 Nov. 1', 1918-Jan. 15, 1919 34 70-73 Jan. 16-Mar. 31, 1919 35 74-77 April-May, 1919 36 78-79 June-July, 1919 37 80-81 August-September, 1919 38 82-83 October-November, 1919 39 84-85 December, 1919-January, 1920 40 86-87 February-March, 1920 41 88-89 April-May, 1920 42 90 June, 1920 43 91 July, 1920 44 92 August, 1920 45 93 September, 1920 46 94 October, 1920 47 95-96 November, 1920 48 97-98 December, 1920 49 99-100 Jan. -

Official Gazette Colony and Protectorate of Kenya

THE OFFICIAL GAZETTE OF THE COLONY AND PROTECTORATE OF KENYA. Published under the Authority of His Excellency the Governor of the Colony and Protectorate of Kenya. [Vol. XXVL—No. 922] NATROBI, January 2, 1924. [Prices 50 Cenrs] Registered as a Newspaper ai the G. P. 0. Published every Wednesday. TABLE OF CONTENTS. PAGE Govt. Notice No, 1—Appointments ves vee ves .. wes vee 2 » 0 ’ 2—A. Bill intituled an Ordinance to Amend the Legislative Conncil Ordinance, 1919 ce Le . Lee . BA4 ” ” ” 3—A Bill intituled an Ordinance to Amend the Native Liquor Ordinance, 1921 wee vee a Lee vee 4 Proclamation No, 1—The Kenya and Uganda (Currency) Order, 1921... vee bee 4 Proclamation No. : 2—The Diseases of Animals Ordinance, 1906 . 5 Govt. Notice No. 4——-Public Health Ordinance, 1921—Notiee ... a vee wes 5 »»» 5-6—The Native Authority Ordinance, 1912—Appointments of Oficial Headmen bee Lee Le ves vee vee 3 Gen. Notices Nos. 1-11—Miscellaneeus Notices ... ve Lee i _ we 5H 2 THE OFFICIAL GAZETTE January 2, 1924. Government Notice No. 1. APPOINTMENTS. W. McHarpy, 0.B.E., M.A., to be Superintendent (Admin- 5. 18816 /930. istrative), Uganda Railway, with effect from Ist January, Guorce Eenest Scarrercoop, to be Accountant, Medical 1924. Department, with effect from the 24th July, 1923. _ A. G. Hicerns, to be Secretary to the Railway Council and CG. M. Bunsury, to be Senior District Engineer, Uganda Private Secretary to the General Manager, Uganda Rail- Railway, with effect from Ist January, 1924. way, with effect from Ist January, 1924. -

The Foreign Service Journal, December 1924

tHti AMERICAN FOREIGN SERVICE JOURNAL (Contributed by the Under Secretary of State, Hon. J. C. Grew) ON THE SCHEIDEGG, SWITZERLAND, 1924 Vol. I DECEMBER, 1924 No. 3 FEDERAL-AMERICAN NATIONAL BANK NOW IN COURSE OF CONSTRUCTION IN WASHINGTON, D. C. W. T. GALLIHER, Chairman of the Board JOHN POOLE, President RESOURCES OVER $13,000,000.00 FOREIGN S JOURNAL PUBLISHED MONTHLY BY THE AMERICAN POREIGN SERVICE ASSOCIATION VOL. I. No. 3 WASHINGTON, D. C. DECEMBER, 1924 The Presidential Election By GERHARD GADE 1916 1920 1924 N November 4 the people of the United State Rep. Dem. Rep. Dem. Rep. Dem. States elected Calvin Coolidge President Maryland 8 8 8 by a popular vote estimated at about Massachusetts . .. .. 18 18 18 18.000,000—2,000,000 more votes than President Michigan .. 15 15 15 Harding received in 1920, although the latter Minnesota .. 12 12 12 Mississippi 10 16 10 polled 22 more electoral votes than his successor. Missouri 18 18 is The popular vote in the last three elections was Montana 4 4 4 as follows: Nebraska 8 8 8 Nevada 3 3 3 1916 Woodrow Wilson 9,129,606 New Hampshire .. 4 4 4 Charles E. Hughes 8,538,221 New Jersey .. ii 14 14 1920 Warren G. Harding 16,152,200 New Mexico 3 3 3 James M. Cox 9,147,353 New York .. 45 45 45 1924 Calvin Coolidge 18,000,000* North Carolina . 12 ii ii John W. Davis 9,000,000* North Dakota .... S 5 5 Robert M. La Follette 4,000,000* Ohio 24 24 24 Oklahoma 10 10 10 * Estimated. -

Survey of Current Business June 1926

UNITED STATES mi DEPARTMENT OF COMMERCE ill WASHINGTON SURVEY OF CURRENT BUSINESS JUNE, 1926 No. 58 1'SW,,1 If.i COMPILED BY ' <i ^ BUREAU OF THE CENSUS BURJBAU OF FOREIGN AND DOMESTIC COMMERCE BUREAU OF STANDARDS IMPORTANT If OTICE In addition to figures given from Government sources, there are also incorporated for completeness of service figures from other sources generally accepted by the trades, the authority and responsibility for which are noted in the "Sources of Data" on pages 159-155 of ike February, 1926, issue Subscription price of the SURVEY OF CURRENT BUSINESS is $1.50 a year; single copies (monthly), 10 cents; semiannual issues, 25 cents. Foreign subscriptions, $2,25; single copies (monthly issues), including postage, 14 cents; semiannual issues, 36 cents. Subscription price of COMMERCE REPORTS is $4 a year; with the SURVBY, £5.50 t year. Make remittances only to Superintendent of Documents, Washington, D, C., by postal money order, express order, or Hew York draft Currency at sender's risk. Postage stamps or foreign money not accepted. WASHINGTON : GOVERNMENT P.RINTINQ OFFICE ! 1986 I INTRODUCTION THE SURVEY OF CURRENT BUSINESS is designed to per cent over the base period, while a relative number present each month a picture of the business situation of 80 means a decrease of 20 per cent from the base. oy setting forth the principal facts regarding the vari- Relative numbers may also be used to calculate the ous lines of trade ana industry. At semiannual inter- approximate percentage increase or decrease in a move- vals detailed tables are published giving, for each item, ment from one period to the next. -

Germany, Reparation Commission)

REPORTS OF INTERNATIONAL ARBITRAL AWARDS RECUEIL DES SENTENCES ARBITRALES Interpretation of London Agreement of August 9, 1924 (Germany, Reparation Commission) 24 March 1926, 29 January 1927, 29 May 1928 VOLUME II pp. 873-899 NATIONS UNIES - UNITED NATIONS Copyright (c) 2006 XXI a. INTERPRETATION OF LONDON "AGREEMENT OF AUGUST 9, 1924 *. PARTIES: Germany and Reparation Commission. SPECIAL AGREEMENT: Terms of submission contained in letter signed by Parties in Paris on August 28, 1925, in conformity with London Agree- ment of August 9, 1924. ARBITRATORS: Walter P. Cook (U.S.A.), President, Marc. Wallen- berg (Sweden), A. G. Kroller (Netherlands), Charles Rist (France), A. Mendelssohn Bartholdy (Germany). AWARD: The Hague, March 24, 1926. Social insurance funds in Alsace-Lorraine.—Social insurance funds in Upper Silesia.—Intention of a provision as a principle of interpretation.— Experts' report and countries not having accepted the report.—Baden Agreement of March 3, 1920.—Restitution in specie.—Spirit of a treaty.— Supply of coal to the S.S. Jupiter.—Transaction of private character. For bibliography, index and tables, see Volume III. 875 Special Agreement. AGREEMENT BETWEEN THE REPARATION COMMISSION AND THE GERMAN GOVERNMENT. Signed at London. August 9th, 1924. Ill (b) Any dispute which may arise between the Reparation Commission and the German Government with regard to the interpretation either of the present agreement and its schedules or of the experts' plan or of the •German legislation enacted in execution of that plan, shall be submitted to arbitration in accordance with the methods to be fixed and subject to the conditions to be determined by the London conference for questions of the interpretation of the experts' Dlan. -

Yesterday's News: Media Framing of Hitler's Early Years, 1923-1924

92 — The Elon Journal of Undergraduate Research in Communications, Vol. 6, No. 1 • Spring 2015 Yesterday’s News: Media Framing of Hitler’s Early Years, 1923-1924 Katherine Blunt Journalism and History Elon University Abstract This research used media framing theory to assess newspaper coverage of Hitler published in The New York Times, The Christian Science Monitor, and The Washington Post between 1923 and 1924. An analysis of about 200 articles revealed “credible” and “non-credible” frames relating to his political influence. Prior to Hitler’s trial for treason in 1924, the credible frame was slightly more prevalent. Following his subsequent conviction, the non-credible frame dominated coverage, with reports often presenting Hitler’s failure to over- throw the Bavarian government as evidence of his lack of political skill. This research provides insight into the way American media cover foreign leaders before and after a tipping point—one or more events that call into question their political efficacy. I. Introduction The resentment, suspicion, and chaos that defined global politics during the Great arW continued into the 1920s. Germany plunged into a state of political and economic turmoil following the ratification of the punitive Treaty of Versailles, and the Allies watched with trepidation as it struggled to make reparations pay- ments. The bill — equivalent to 33 billion dollars then and more than 400 billion dollars today — grew increas- ingly daunting as the value of the mark fell from 400 to the dollar in 1922 to 7,000 to the dollar at the start of 1923, when Bavaria witnessed the improbable rise of an Austrian-born artist-turned-politician who channeled German outrage into a nationalistic, anti-Semitic movement that came to be known as the Nazi Party.1 Ameri- can media outlets, intent on documenting the chaotic state of post-war Europe, took notice of Adolf Hitler as he attracted a following and, through their coverage, essentially introduced him to the American public. -

S Ubject L Ist N O. 44 of DOCUMENTS DISTRIBUTED to the MEMBERS of the COUNCIL DURING DECEMBER 1924

[DISTRIBUTED ,, e a g u e o f a t i o n s C. 5. MEMBERS OFT0TllE THE COUNCIL ] L N 1925- G en ev a , January 4 t h , 1925. S ubject L ist N o. 44 OF DOCUMENTS DISTRIBUTED TO THE MEMBERS OF THE COUNCIL DURING DECEMBER 1924. (Prepared by the Distribution Branch.) Armaments, Reduction 0! Arms, Private manufacture of and traffic in Convention concluded September 10, 1919 at St. Germain-en-Laye for the control of traffic in arms Convention to supersede Conference, May 1925, Geneva, to prepare A Report dated December 1924 by Czechoslovak Representative (M. Benes) and resolution adopted December 8, 1924 by 32nd Council Session, fixing May 4, 1925 as date for Admissions to League C. 801. 1924. IX Germany Letter dated December r 2, 1924 from German Government (M. Stresemann) forwarding copy Text (draft) subm itted July 1924 by Temporary of its memorandum to the Governments repre Mixed Commission, of sented on the Council with a view to the elucida Letter dated October 9, 1924 from Secretary- tion of certain problems connected with Germany's General to States Members and Non- co-operation with League, announcing its satis Members of the League quoting relative faction with the replies received, except with Assembly resolution, forwarding Tempo regard to Article 16 of Covenant, and submitting rary Mixed Commission's report (A. 16. detailed statement of its apprehensions with 1924) containing above-mentioned draft and regard to this article minutes of discussion of its Article 9, and the report of 3rd Commission to Assembly C. -

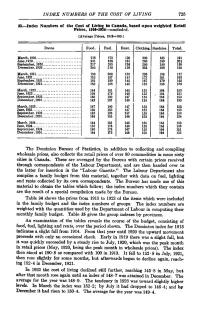

INDEX NUMBERS of the COST of LIVING 725 33.—Index Numbers of the Cost of Living in Canada, Based Upon Weighted Retail Prices

INDEX NUMBERS OF THE COST OF LIVING 725 33.—Index Numbers of the Cost of Living in Canada, based upon weighted Retail Prices, 1910-1934—concluded. (Average Prices, 1913=100.) Dates. Food. Fuel. Rent. Clothing. Sundries. Total. March, 1920 218 173 120 260 185 191 June,1920 231 186 133 260 190 201 September, 1920 217 285 136 260 190 199 December, 1920. 202 218 139 235 190 192 March, 1921 180 208 139 195 188 177 June,1921 152 197 143 173 181 163 September, 1921 161 189 145 167 170 162 December, 1921. 150 186 145 158 166 156 March, 1922 144 181 145 155 164 153 June, 1922 139 179 146 155 . 164 151 September, 1922. 140 190 147 155 164 153 December, 1922. 142 187 146 155 164 153 March, 1923 147 190 147 155 164 155 June,1923 139 182 147 155 164 152 September, 1923. 142 183 147 155 164 153 December, 1923. 146 185 146 155 164 154 March, 1924 144 181 146 155 164 153 June,1924 133 176 146 155 164 149 September, 1924. 140 176 147 155 164 151 December, 1924. 144 175 146 155 164 152 The Dominion Bureau of Statistics, in addition to collecting and compiling wholesale prices, also collects the retail prices of over 80 commodities in some sixty cities in Canada. These are averaged by the Bureau with certain prices received through correspondents of the Labour Department, and are then handed over to the latter for insertion in the "Labour Gazette." The Labour Department also compiles a family budget from this material, together with data on fuel, lighting and rents collected by its own correspondents. -

Economic Crises of Weimar Republic, 1923 & 1929 Block

LHS World History Name: Reading #1 Date: Economic Crises of Weimar Republic, 1923 & 1929 Block: Two economic events shattered the average German’s faith in the Weimar Republic. The first event was the hyperinflation crisis of 1923. The second event was the Great Depression that began in 1929. When in January 1923, France and Belgium occupied the Ruhr in response to Weimar’s announced policy of “non cooperation” Berlin countered by ordering passive resistance. In doing so, they paid the workers of Germany to not work. These became known as “resistance wages.” To pay the resistance wages, the presses began to print astronomical amounts of money. By December 1923, Germany was in the grips of a hyperinflation crisis unprecedented in the annals of western civilization. $1.00 cost 4 million RM (Reichmark). A woman might order a cup of coffee for 5000 RM and get a bill for 8000 RM an hour later. By December of 1923 90% of average family expenditure was going towards food. A massive crime wave swept the country. Child prostitution was off the charts as families sold their children for food, and precious metals disappeared off th of the streets. Germany collapsed into a full barter economy, reminiscent of 9 century Europe. Full economic collapse stared the government in the face. Though for years it has been claimed by historians that the hyperinflation crisis wiped out the German middle class, this was simply not the case. The inflation did not destroy the economic position of the middle class. Some like mortgage holders, debtors or businessmen who bought on installment payments gained; others such as investors or bondholders, lost. -

Representations of Gender and Age in the 1920S

JOURNALHirshbein / THEOF FAMILY FLAPPER HISTORY AND THE / January FOGY 2001 THE FLAPPER AND THE FOGY: REPRESENTATIONS OF GENDER AND AGE IN THE 1920S Laura Davidow Hirshbein In the 1920s in the United States, public attention was riveted on the antics of a new, rebellious younger generation. Although popular representations focused on youth in crisis, these representations emphasized comparisons between young and old. This article explores the public discussions about youth culture in the 1920s and how they helped to refine cultural categories of youth and old age. In addition, through gender-specific representations, social commentators worked out new definitions of masculinity, femininity, and the relationships between the sexes. Furthermore, the rhetorical conflict between generations of Americans helped to frame important contemporary questions about national identity. In the 1920s in the United States, public attention was riveted on the represented antics of a new, rebellious younger generation. Within the mass culture of the burgeoning magazine and movie industries, as well as the new medium of motion pictures and expansions in advertising, one of the hottest topics of the time was youth.1 Commenta- tors of the time wrote extensively on whether or not the younger generation was lead- ing society toward progress or toward destruction. But while the ostensible topic of these discussions was the behavior of young people, popular representations of youth in crisis depended on a constant series of comparisons between young and old. In this article, I explore the discussions of youth that appeared in popular magazines in the 1920s. I focus on the definitions of youth and old age that emerged from these public discussions, as well as the implications for gender standards and national iden- tity. -

Scrapbook Inventory

E COLLECTION, H. L. MENCKEN COLLECTION, ENOCH PRATT FREE LIBRARY Scrapbooks of Clipping Service Start and End Dates for Each Volume Volume 1 [sealed, must be consulted on microfilm] Volume 2 [sealed, must be consulted on microfilm] Volume 3 August 1919-November 1920 Volume 4 December 1920-November 1921 Volume 5 December 1921-June-1922 Volume 6 May 1922-January 1923 Volume 7 January 1923-August 1923 Volume 8 August 1923-February 1924 Volume 9 March 1924-November 1924 Volume 10 November 1924-April 1925 Volume 11 April 1925-September 1925 Volume 12 September 1925-December 1925 Volume 13 December 1925-February 1926 Volume 14 February 1926-September 1926 Volume 15 1926 various dates Volume 16 July 1926-October 1926 Volume 17 October 1926-December 1926 Volume 18 December 1926-February 1927 Volume 19 February 1927-March 1927 Volume 20 April 1927-June 1927 Volume 21 June 1927-August 1927 Volume 22 September 1927-October 1927 Volume 23 October 1927-November 1927 Volume 24 November 1927-February 1928 Volume 25 February 1928-April 1928 Volume 26 May 1928-July 1928 Volume 27 July 1928-December 1928 Volume 28 January 1929-April 1929 Volume 29 May 1929-November 1929 Volume 30 November 1929-February 1930 Volume 31 March 1930-April 1930 Volume 32 May 1930-August 1930 Volume 33 August 1930-August 1930. Volume 34 August 1930-August 1930 Volume 35 August 1930-August 1930 Volume 36 August 1930-August 1930 Volume 37 August 1930-September 1930 Volume 38 August 1930-September 1930 Volume 39 August 1930-September 1930 Volume 40 September 1930-October 1930 Volume