Americas Banks Americas Banks Banking on Technology the Shareholder Benefits of a Digital Future

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

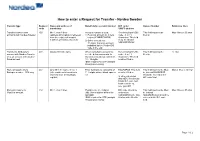

How to Enter a Request for Transfer - Nordea Sweden

How to enter a Request for Transfer - Nordea Sweden Transfer type Request Name and address of Beneficiary’s account number BIC code / Name of banker Reference lines code beneficiary SWIFT address Transfer between own 400 Min 1, max 4 lines Account number is used: Receiving bank’s BIC This field must not be Max 4 lines x 35 char accounts with Nordea Sweden (address information is retrieved 1) Personal account no = pers code - 8 or 11 filled in from the register of account reg no (YYMMDDXXXX) characters. This field numbers of Nordea, Sweden) 2) Other account nos = must be filled in 11 digits. Currency account NDEASESSXXX indicated by the 3-letter ISO code in the end Transfer to third party’s 401 Always fill in the name When using bank account no., Receiving bank’s BIC This field must not be 12 char account with Nordea Sweden see the below comments. In code - 8 or 11 filled in or to an account with another Sweden account nos consist of characters. This field Swedish bank 10 - 15 digits. must be filled in IBAN required for STP (straight through processing) Domestic payments to 402 Only fill in the name in line 1 Enter bankgiro no consisting of BGABSESS. This field This field must not be filled Max 4 lines x 35 char Bankgiro number - SEK only (other address information is 7 - 8 digits without blank spaces must be filled in. in. Instead BGABSESS retrieved from the Bankgiro etc should be entered in the register) In other currencies BIC code field than SEK: Receivning banks BIC code and bank account no. -

Chronology, 1963–89

Chronology, 1963–89 This chronology covers key political and economic developments in the quarter century that saw the transformation of the Euromarkets into the world’s foremost financial markets. It also identifies milestones in the evolu- tion of Orion; transactions mentioned are those which were the first or the largest of their type or otherwise noteworthy. The tables and graphs present key financial and economic data of the era. Details of Orion’s financial his- tory are to be found in Appendix IV. Abbreviations: Chase (Chase Manhattan Bank), Royal (Royal Bank of Canada), NatPro (National Provincial Bank), Westminster (Westminster Bank), NatWest (National Westminster Bank), WestLB (Westdeutsche Landesbank Girozentrale), Mitsubishi (Mitsubishi Bank) and Orion (for Orion Bank, Orion Termbank, Orion Royal Bank and subsidiaries). Under Orion financings: ‘loans’ are syndicated loans, NIFs, RUFs etc.; ‘bonds’ are public issues, private placements, FRNs, FRCDs and other secu- rities, lead managed, co-managed, managed or advised by Orion. New loan transactions and new bond transactions are intended to show the range of Orion’s client base and refer to clients not previously mentioned. The word ‘subsequently’ in brackets indicates subsequent transactions of the same type and for the same client. Transaction amounts expressed in US dollars some- times include non-dollar transactions, converted at the prevailing rates of exchange. 1963 Global events Feb Canadian Conservative government falls. Apr Lester Pearson Premier. Mar China and Pakistan settle border dispute. May Jomo Kenyatta Premier of Kenya. Organization of African Unity formed, after widespread decolonization. Jun Election of Pope Paul VI. Aug Test Ban Take Your Partners Treaty. -

Svenska Handelsbanken AB

OFFERING CIRCULAR Svenska Handelsbanken AB (publ) (Incorporated as a public limited liability banking company in The Kingdom of Sweden) U.S.$50,000,000,000 Euro Medium Term Note Programme for the issue of Notes with a minimum maturity of one month On 26th June, 1992 Svenska Handelsbanken AB (publ) (the “Issuer” or the “Bank”) entered into a U.S.$1,500,000,000 Euro Medium Term Note Programme (the “Programme”) and issued an offering circular on that date describing the Programme. This Offering Circular supersedes any previous offering circular and supplements therein prepared in connection with the Programme. Any Notes (as defined below) issued under the Programme on or after the date of this Offering Circular are issued subject to the provisions described herein. This does not affect any Notes already in issue. Under the Programme, the Bank may from time to time issue Notes (the “Notes”), which expression shall include Notes (i) issued on a senior preferred basis as described in Condition 3 (“Senior Preferred Notes”), (ii) issued on a senior non-preferred basis as described in Condition 4 (“Senior Non-Preferred Notes”), (iii) issued on a subordinated basis and which rank on any voluntary or involuntary liquidation (Sw. likvidation) or bankruptcy (Sw. konkurs) of the Bank as described in Condition 5 (“Subordinated Notes”) and (iv) issued on a subordinated basis with no fixed maturity and which rank on any voluntary or involuntary liquidation (Sw. likvidation) or bankruptcy (Sw. konkurs) of the Bank as described in Condition 6 (“Additional Tier 1 Notes”). The Outstanding Principal Amount (as defined in Condition 2) of each Series (as defined below) of Additional Tier 1 Notes will be subject to Write Down (as defined in Condition 2) if the Common Equity Tier 1 Capital Ratio (as defined in Condition 2) of the Bank and/or the Handelsbanken Group (as defined Condition 2) is less than the relevant Trigger Level (as defined in Condition 2). -

2Q21 GS Earnings Release

Second Quarter 2021 Earnings Results Media Relations: Andrea Williams 212-902-5400 Investor Relations: Carey Halio 212-902-0300 The Goldman Sachs Group, Inc. 200 West Street | New York, NY 10282 Second Quarter 2021 Earnings Results Goldman Sachs Reports Second Quarter Earnings Per Common Share of $15.02 and Increases the Quarterly Dividend to $2.00 Per Common Share “Our second quarter performance and record revenues for the first half of the year demonstrate the strength of our client franchise and our continued progress on our strategic priorities. While the economic recovery is underway, our clients and communities still face challenges in overcoming the pandemic. But, as always, I am proud of the dedication and resilience of our people, who have worked tirelessly to help our clients navigate the ever-changing market environment.” - David M. Solomon, Chairman and Chief Executive Officer Financial Summary Net Revenues Net Earnings EPS 2Q $15.39 billion 2Q $5.49 billion 2Q $15.02 2Q YTD $33.09 billion 2Q YTD $12.32 billion 2Q YTD $33.64 Annualized ROE1 Annualized ROTE1 Book Value Per Share 2Q 23.7% 2Q 25.1% 2Q $264.90 2Q YTD 27.3% 2Q YTD 28.9% YTD Growth 12.2% NEW YORK, July 13, 2021 – The Goldman Sachs Group, Inc. (NYSE: GS) today reported net revenues of $15.39 billion and net earnings of $5.49 billion for the second quarter ended June 30, 2021. Net revenues were $33.09 billion and net earnings were $12.32 billion for the first half of 2021. Diluted earnings per common share (EPS) was $15.02 for the second quarter of 2021 compared with $0.53 for the second quarter of 2020 and $18.60 for the first quarter of 2021, and was $33.64 for the first half of 2021 compared with $3.66 for the first half of 2020. -

Blackstone, Goldman Lead $1.25B Bet on City Offices

July 26, 2021 Link to Article Blackstone, Goldman lead $1.25B bet on city offices Blackstone Group Inc. and Goldman Sachs Group Inc. are leading financing for the $1.25 billion redevelopment of a 19th-century warehouse on Manhattan’s west side into a 21st-century office complex. The financing marks the largest construction deal so far this year in Manhattan, according to a statement Friday by L&L Holding Co. and Columbia Property Trust, developers of the Terminal Warehouse, which occupies an entire block in the West Chelsea neighborhood. The project is moving ahead without a major tenant at an uncertain time for New York’s office market. The city has a record amount of space available, and employees have been slow to return from pandemic work-from-home arrangements. Terminal Warehouse is south of Hudson Yards, where new skyscrapers have drawn major financial and technology tenants. “Our ability to secure financing in this current environment is both a testament to the merits of this project as well as a show of the investment community’s continued faith in the future of New York City’s economy,” Robert Lapidus, L&L’s chief investment officer, said in the statement. Blackstone’s real estate debt platform led the financing, with Goldman and KKR & Co. participating in $974 million of senior debt. Oaktree Capital Management led $274 million in junior mezzanine financing in partnership with Paramount Group. “This property is rich in history and we are excited to be part of another high-quality office addition to the growing Hudson Yards and broader west side area of Manhattan,” Michael Eglit, managing director in Blackstone’s Real Estate Debt Strategies group, said in an email. -

Interim Report January – September 2020 Q3

Interim Report January – September 2020 Q3 Financial summary Third quarter First nine months • Net sales amounted to EUR 27k (0) • Net sales amounted to EUR 126k (21k) • Operating loss (EBIT) increased to EUR 4,790k • Operating loss (EBIT) increased to EUR 7,291k (748k) driven by listing costs (3,490k) driven by listing costs • Loss after tax amounted to EUR 4,730k (815k) • Loss after tax amounted to EUR 7,127k (3,602k) • Basic and diluted loss per Class A share amounted to EUR 0.10 (0.02) • Basic and diluted loss per Class A share amounted to EUR 0.16 (0.08) • Liquid funds as at end of the period amounted to EUR 90.5m • Cash flow from operating activities amounted to EUR -1,824k (-3,014k) • No interest-bearing debt at end of the period Figures within parentheses refer to the preceding year. Significant events • Enlisted Inselspital Bern, the largest In the third quarter of 2020 university hospital in Switzerland, to be the lead hospital in our upcoming RefluxStop™ • Completed listing on Nasdaq First North Premier Growth Market raising SEK 1.1 Registry clinical trial to be focused primarily billion, with trading of Implantica's Swedish in Germany and Switzerland. Depository Receipts commencing on September 21, 2020. The offering was After the end of the period substantially oversubscribed. • Exercised overallotment option raising an additional SEK 165 million. • Increased our shareholder base with highly reputable shareholders such as Swedbank • Implantica’s RefluxStop™ trial showed Robur Ny Teknik, Handelsbanken Fonder, exceptional three-year follow-up results. TIN Fonder, Skandia and Nordea Investment None of the 47 patients in the study were in Management. -

DTC Participant Alphabetical Listing June 2019.Xlsx

DTC PARTICPANT REPORT (Alphabetical Sort ) Month Ending - June 30, 2019 PARTICIPANT ACCOUNT NAME NUMBER ABN AMRO CLEARING CHICAGO LLC 0695 ABN AMRO SECURITIES (USA) LLC 0349 ABN AMRO SECURITIES (USA) LLC/A/C#2 7571 ABN AMRO SECURITIES (USA) LLC/REPO 7590 ABN AMRO SECURITIES (USA) LLC/ABN AMRO BANK NV REPO 7591 ALPINE SECURITIES CORPORATION 8072 AMALGAMATED BANK 2352 AMALGAMATED BANK OF CHICAGO 2567 AMHERST PIERPONT SECURITIES LLC 0413 AMERICAN ENTERPRISE INVESTMENT SERVICES INC. 0756 AMERICAN ENTERPRISE INVESTMENT SERVICES INC./CONDUIT 7260 APEX CLEARING CORPORATION 0158 APEX CLEARING CORPORATION/APEX CLEARING STOCK LOAN 8308 ARCHIPELAGO SECURITIES, L.L.C. 0436 ARCOLA SECURITIES, INC. 0166 ASCENSUS TRUST COMPANY 2563 ASSOCIATED BANK, N.A. 2257 ASSOCIATED BANK, N.A./ASSOCIATED TRUST COMPANY/IPA 1620 B. RILEY FBR, INC 9186 BANCA IMI SECURITIES CORP. 0136 BANK OF AMERICA, NATIONAL ASSOCIATION 2236 BANK OF AMERICA, NA/GWIM TRUST OPERATIONS 0955 BANK OF AMERICA/LASALLE BANK NA/IPA, DTC #1581 1581 BANK OF AMERICA NA/CLIENT ASSETS 2251 BANK OF CHINA, NEW YORK BRANCH 2555 BANK OF CHINA NEW YORK BRANCH/CLIENT CUSTODY 2656 BANK OF MONTREAL, CHICAGO BRANCH 2309 BANKERS' BANK 2557 BARCLAYS BANK PLC NEW YORK BRANCH 7263 BARCLAYS BANK PLC NEW YORK BRANCH/BARCLAYS BANK PLC-LNBR 8455 BARCLAYS CAPITAL INC. 5101 BARCLAYS CAPITAL INC./LE 0229 BB&T SECURITIES, LLC 0702 BBVA SECURITIES INC. 2786 BETHESDA SECURITIES, LLC 8860 # DTCC Confidential (Yellow) DTC PARTICPANT REPORT (Alphabetical Sort ) Month Ending - June 30, 2019 PARTICIPANT ACCOUNT NAME NUMBER BGC FINANCIAL, L.P. 0537 BGC FINANCIAL L.P./BGC BROKERS L.P. 5271 BLOOMBERG TRADEBOOK LLC 7001 BMO CAPITAL MARKETS CORP. -

Joanne Choi Joins Lazard Asset Management As Chief Marketing Officer

JOANNE CHOI JOINS LAZARD ASSET MANAGEMENT AS CHIEF MARKETING OFFICER NEW YORK, July 19, 2021 – Lazard Asset Management (LAM) announced today that Joanne Choi has joined the firm as a Managing Director and Chief Marketing Officer, effective immediately. Based in New York, Ms. Choi joins from Goldman Sachs Asset Management, where she was Head of Global Marketing. Ms. Choi is responsible for the firm‘s marketing efforts and brand strategy across its global Asset Management client base. She will drive commercial opportunities through strategic marketing communications programs. She will also partner closely with distribution to promote LAM’s investment solutions and insights, and oversee marketing operations to enhance client engagement opportunities. “With the evolving complexity of global capital markets and the growing diversity of our investment solutions, our marketing efforts require a heightened level of expertise, nimbleness and creativity,” said Nathan Paul, Chief Business Officer, LAM. “Joanne not only has the relevant experience, but she understands the intricacies of our business and ways to position our strategies to best meet the needs of our clients.” “This is a rare opportunity to further strengthen and develop a well-established, global brand,” said Joanne Choi, Chief Marketing Officer, LAM. “I am drawn to the culture and client-led approach of Lazard Asset Management and am looking forward to working with the team to enhance the client experience, with a clear focus on lead and revenue generation.” Prior to joining LAM, Ms. Choi served 18 years with Goldman Sachs Asset Management, where she held a number of high-profile global marketing roles, including Head of Americas Marketing and Head of Americas Institutional Marketing. -

Wealth Management in a Mobile-First Era

Wealth Management In A Mobile-First Era How To Turn Robo Savers Into Robo Investors 14 December 2016 By: Mark Schwanhausser A growing number of so-called robo investment firms, fintech innovators, and bank partnerships is rushing to refine a cost-effective business model for investment services in a digital-first era. The challenges are numerous, starting with how to tempt today’s affluent Gen X, Baby Boomer, and female investors to try untested upstarts while also grooming tomorrow’s Gen Y banking customers who aren’t yet rich. The outcome will be shaped by how well financial institutions incorporate robo capabilities in three categories: digital banking insights, robo advising and investing, and personalized “robo writing.” Together, these services and players can build on Javelin’s Financial Journey Model, usher in new ways to coach customers, simplify investment decisions, counter anxiety in volatile times — and put banks and credit unions in a strong position when customers are ready to invest. Key questions discussed in this report: How can financial institutions use robo services to provide cost-effective investment services and groom customers to become eventual wealth management clients? What is the forecast for the potential market for Gen Y, Gen X, and Baby Boomer investors? Can banks and credit unions compete to provide robo services profitably? How should an FI prioritize investments to deliver insights in digital banking, robo advising and investing, and personalized information? Companies Mentioned: Acorns, Amazon (Echo), AssetBuilder, -

Effective May 07, 2021

CASH & BANKING LPL Financial Insured Cash Account (ICA): Current Priority Bank List Retail Accounts Effective May 07, 2021 ABOUT THE PRIORITY BANK LIST (PBL) The Priority Bank List is a list of available Banks into which your funds may be deposited and is available from your financial advisor and on lplfinancial.lpl.com/disclosures. The Banks appear in columns by state or region. In the column under your applicable state or region are multiple Banks in the order in which your funds will be allocated. The last banks on the list are “Excess Banks” and are noted as such. For all other banks on the PBL except these Excess Banks, LPL Financial as your agent will ensure that your ICA sweep deposits do not exceed the $250,000 (or $500,000 for joint accounts) FDIC-defined ownership category limits. For the Excess Banks, your funds may be deposited without consideration of the $250,000 and $500,000 limits. However, this will only be done when there is insufficient capacity in other Banks on the PBL to take your assets and not break through the $250,000 and $500,000 limits and is meant to be temporary in nature. You may not change the order of the Banks on the PBL. However, you may, at any time, designate a Bank as ineligible to receive your funds. This will result in your funds not being deposited into this bank or if already there, we will remove your funds from that Bank and designate the Bank as ineligible to receive future deposits. Unless you direct us to place your funds in a different investment, your funds from eliminated Banks will be deposited at the first available Bank set forth on the Priority Bank List, as amended by you. -

Important Notice National Securities Clearing Corporation

Important Notice National Securities Clearing Corporation A#: 8973 P&S #: 8546 Date: 03/05/2021 To: ALL PARTICIPANTS OPERATIONS PARTNER/OFFICER; MANAGER P&S DEPARTMENT; CASHIER; Attention: ACATS PARTICIPANTS; FUND/SERV PARTICIPANTS; MUNICIPAL BOND COMPARISON PARTICIPANTS From: ACCOUNT ADMINISTRATION Subject: CHANGES IN THE LIST OF PARTICIPANTS • The following firms will retire from all services, as detailed below: Last Trade Date, March 03, 2021 Preste Capital Partners S.A. No. 1156 Last Trade Date, March 05, 2021 Cary Street Partners, LLC No. 6487 Last Trade Date, March 09, 2021 Galloway Capital Management LTD. No. 3434 Veritas Independent Partners, LLC No. 4416 Last Trade Date, March 10, 2021 Ultimus Fund Distributors, LLC/Ryan Labs Funds No. 3183 • The following firm will begin participation in the MF Profile service, as detailed below: First Trade Date, March 08, 2021: Quasar Distributors, LLC/Locorr Investment Trust No. 5569 • The following firm will begin participation in the Omni/SERV Activity & Position service, as detailed below: First Trade Date, March 08, 2021: Goldman, Sachs & Co. LLC/Goldman Sachs International Fund No. 6570 DTCC offers enhanced access to all important notices via a Web-based subscription service. The notification system leverages RSS Newsfeeds, providing significant benefits including real-time updates and customizable delivery. To learn more and to set up your own DTCC RSS alerts, visit http://www.dtcc.com/rss-feeds.aspx. DTCC Public (White) • The following firm will change its OTC Symbol, as detailed below: Effective First Trade Date, March 15, 2021: From: Interactive Brokers LLC No. 0017 OTC Alpha Identifier: IBKR To: Interactive Brokers LLC No. -

MIT 15.S08 S20 Class 9: Trading & Capital Markets

FinTech: Shaping the Financial World April 29, 2020 1 Class 9: Overview • Online Brokerage • Robinhood & Zero Commission Trading • Robo Advisors • Capital Markets FinTech Startups • Crypto Exchanges, Lending & Decentralized Finance 2 Class 9: Readings • 'How Robinhood Changed an Industry' John Divine, US News • 'Charles Schwab and the New Broker Wars' Daren Fonda, Bloomberg • 'Robo-Advisors: Product vs. Platform' Henry O’Brien, The Startup 3 Class 9: Study Questions • How did online brokers emerge during an earlier stage of FinTech development? How were Robinhood and this era’s FinTech startups able to further disrupt the brokerage world? • How are Robo Advisors transforming the provision of retail asset management services? How has Big Finance - incumbent asset managers and banks - reacted? • What are FinTech trends and applications affecting trading, asset management & capital market infrastructure? 4 Online Brokerage Company Landscape • Retail Brokers: Charles Schwab / TD Ameritrade (1971) – 12M each, E*TRADE (1982) – 5.2M, Firstrade (1985), Interactive Brokers (1978) – 0.8M, LBMZ Zacks Trade (1978), Monex TradeStation (1999 / 1982) • Asset Managers: Fidelity (1946), Vanguard (1975) • Banks: JP Morgan You Invest (1871 / 2018), Merrill Edge (1914 / 2010), Ally Invest (1919 / 2016) 4M • FinTech Startups: Freetrade (2016), Public (2017), Robinhood (2013) - 10M, Stash (2015) – 3.5M, Tastyworks (2017), Upstox (2012), Webull (2017) 5 Mobile Trading – App Comparison © Reink Media Group LLC. All rights reserved. This content is excluded from