Summary Financial Report (PDF: 6709KB)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Services for Ex-Offenders and Discharged Prisoners

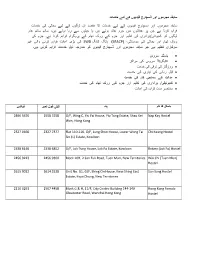

ﺳﺎﺑﻘہ ﻣﺟرﻣوں اور ڈﺳﭼﺎرج ﻗﯾدﯾوں ﮐﮯ ﻟﺋﮯ ﺧدﻣﺎت ﺳﺎﺑﻘہ ﻣﺠﺮﻣﻮں اور دﺳﭽﺎرج ﻗﯿﺪﯾﻮں ﮐﮯ ﻟﯿﮯ ﺧﺪﻣﺎت ﮐﺎ ﻣﻘﺼﺪ ان ﻟﻮﮔﻮں ﮐﮯ ﻟﯿﮯ ﺑﺤﺎﻟﯽ ﮐﯽ ﺧﺪﻣﺎت ﻓﺮاﮨﻢ ﮐﺮﻧﺎ ﮨﮯ ﺟﻦ ﭘﺮ ﻋﺪاﻟﺘﻮں ﻣﯿﮟ ﺟﺮم ﻋﺎﺋﺪ ﮨﻮﺋﮯ ﮨﯿﮟ ﯾﺎ ﺟﯿﻠﻮں ﺳﮯ رﮨﺎ ﮨﻮﺋﮯ ﮨﯿﮟ، ﺳﺎﺗﮭ ﺳﺎﺗﮭ ﻋﺎم ﻟﻮﮔﻮں ﮐﻮ ﮐﻤﯿﻮﻧﮣﯽ/ﺑﺮادری ﮐﯽ ﺗﻌﻠﯿﻢ اور ﺟﺮم ﮐﮯ روک ﺗﮭﺎم ﮐﮯ ﭘﺮوﮔﺮام ﻓﺮاﮨﻢ ﮐﺮﻧﺎ ﮨﮯ۔ ﺟﺮم ﮐﯽ روک ﺗﮭﺎم اور ﺑﺤﺎﻟﯽ ﮐﯽ ﺳﻮﺳﺎﺋﮣﯽ، (SRACP) ﮨﺎﻧﮓ ﮐﺎﻧﮓ SWD ﮐﯽ ﺑﮍی اﻋﺎﻧﺖ ﻓﺮاﮨﻢ ﮐﺮﻧﯽ واﻟﯽ ﻏﯿﺮ ﺳﺮﮐﺎری ﺗﻨﻈﯿﻢ ﮨﮯ ﺟﻮ ﺳﺎﺑﻘہ ﻣﺠﺮﻣﻮں اور ڈﺳﭽﺎرج ﻗﯿﺪﯾﻮں ﮐﻮ ﻣﻨﺪرﺟہ ذﯾﻞ ﺧﺪﻣﺎت ﻓﺮاﮨﻢ ﮐﺮﺗﯽ ﮨﮯ۔ • ﮨﺎﺳﮣﻞ ﺳﺮوس • اﻧﮣﯿﮕﺮﯾﮣﮉ ﺳﺮوس ﮐﯽ ﻣﺮاﮐﺰ • روزﮔﺎر ﮐﯽ ﺗرﻗﯽ ﮐﯽ ﺧدﻣت • ﻗﺒﻞ رﮨﺎﺋﯽ ﮐﯽ ﺗﯿﺎری ﮐﯽ ﺧﺪﻣﺖ • ﻋﺪاﻟﺖ ﮐﮯ ﺳﻤﺎﺟﯽ ﮐﺎم ﮐﯽ ﺧﺪﻣﺖ • ﮐﻤﯿﻮﻧﯿﮣﯽ/ ﺑﺮاداری ﮐﯽ ﺗﻌﻠﯿﻢ اور ﺟﺮم ﮐﮯ روک ﺗﮭﺎم ﮐﯽ ﺧﺪﻣﺖ • ﻣﺧﺗﺻر ﻣدت ﮐراﯾہ ﮐﯽ اﻋﺎﻧت ﮨﺎﺳﮣﻞ ﮐﺎ ﻧﺎم ﭘﺘہ ﮢﯿﻠﯽ ﻓﻮن ﻧﻤﺒﺮ ﻓﯿﮑﺲ 2896 5676 2558 3258 G/F, Wing C, Yiu Fai House, Yiu Tung Estate, Shau Kei Nap Kay Hostel Wan, Hong Kong 2327 0666 2327 7377 Flat 110-116, G/F, Lung Shun House, Lower Wong Tai Chi Keung Hostel Sin (1) Estate, Kowloon 2338 6146 2338 6852 G/F, Lok Tung House, Lok Fu Estate, Kowloon Rotary (Lok Fu) Hostel 2456 9223 2456 9300 Block 10H, 2 San Fuk Road, Tuen Mun, New Territories Wai Chi (Tuen Mun) Hostel 2615 9032 2614 2528 Unit No. G1, G/F, Shing On House, Kwai Shing East Sun Sang Hostel Estate, Kwai Chung, New Territories 2110 0291 2507 4458 Block G & H, 11/F, City Centre Building 144-149 Hong Kong Female Gloucester Road, Wanchai Hong Kong Hostel اﻧﮣﯿﮕﺮﯾﮣﮉ ﺳﺮوس ﮐﯽ ﻣﺮاﮐﺰ ﮐﯽ ﻓﮩﺮﺳﺖ ﻣﺮﮐﺰ ﮐﺎ ﻧﺎم ﭘﺘہ ﮢﯿﻠﯽ ﻓﻮن ﻧﻤﺒﺮ ﻓﯿﮑﺲ Hong Kong Integrated Service Centre for Social Rehabilitation & G/F, Li Chit Garden,1 Li Chit Street, Wanchai, Hong Community Support 2865 6448 2866 7867 Kong - Hong Kong Revival Hub Kowloon East Integrated Service Centre for Social Rehabilitation & 2321 7900 2352 3398 Unit Nos. -

Kwun Tong District(Open in New Window)

District : Kwun Tong Recommended District Council Constituency Areas +/- % of Population Estimated Quota Code Recommended Name Boundary Description Major Estates/Areas Population (17,194) J01 Kwun Tong Central 13,115 -23.72% N Ngau Tau Kok Road 1. YUE MAN CENTRE NE Hip Wo Street, Hong Ning Road Mut Wah Street, Tung Ming Street Yee On Street E Hip Wo Street, King Yip Lane King Yip Street, Kwun Tong Road SE King Yip Street S District Boundary SW Part of the Harbour Southwest of Hoi Bun Road, District Boundary W Cheung Yip Street, District Boundary NW Sheung Yee Road J1 District : Kwun Tong Recommended District Council Constituency Areas +/- % of Population Estimated Quota Code Recommended Name Boundary Description Major Estates/Areas Population (17,194) J02 Kowloon Bay 14,286 -16.91% N Kai Lok Street, Kai Shun Road 1. TELFORD GARDENS Wang Chiu Road NE Kwun Tong Road E Kwun Tong Road SE Kwun Tong Road, Sheung Yee Road S Sheung Yee Road SW District Boundary W Kai Fuk Road NW Cargo Circuit J03 Kai Yip 14,949 -13.06% N Kwun Tong Road 1. KAI TAI COURT 2. KAI YIP ESTATE NE Kwun Tong Road E Kai Lok Street, Kai Yip Road SE Kai Lok Street S Kai Lok Street, Kai Shun Road Wang Chiu Road SW Kai Shun Road, Wang Kwong Road W Cargo Circuit, Eastern Road Kai Yan Street NW Wang Chiu Road J2 District : Kwun Tong Recommended District Council Constituency Areas +/- % of Population Estimated Quota Code Recommended Name Boundary Description Major Estates/Areas Population (17,194) J04 Lai Ching 17,386 +1.12% N Choi Hung Road, Prince Edward Road East 1. -

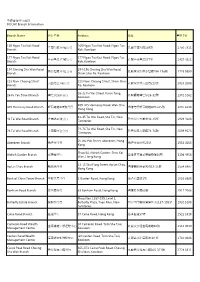

中銀香港分行資料BOCHK Branch Information Branch Name 分行名稱

中銀香港分行資料 BOCHK Branch Information Branch Name 分行名稱 Address 地址 電話 Tel 169 Ngau Tau Kok Road 169 Ngau Tau Kok Road, Ngau Tau 牛頭角道169號分行 九龍牛頭角道169號 2750 7311 Branch Kok, Kowloon 177 Ngau Tau Kok Road 177 Ngau Tau Kok Road, Ngau Tau 牛頭角道177號分行 九龍牛頭角道177號 2927 4321 Branch Kok, Kowloon 194 Cheung Sha Wan Road 194-196 Cheung Sha Wan Road, 長沙灣道194號分行 九龍深水埗長沙灣道194-196號 2728 9389 Branch Sham Shui Po, Kowloon 223 Nam Cheong Street 223 Nam Cheong Street, Sham Shui 南昌街223號分行 九龍深水埗南昌街223號 2928 2088 Branch Po, Kowloon 26-32 Fu Yan Street, Kwun Tong, 26 Fu Yan Street Branch 輔仁街26號分行 九龍觀塘輔仁街26-32號 2342 5262 Kowloon 409-415 Hennessy Road, Wan Chai, 409 Hennessy Road Branch 軒尼詩道409號分行 香港灣仔軒尼詩道409-415號 2835 6118 Hong Kong 41-45 Tai Wai Road, Sha Tin, New 41 Tai Wai Road Branch 大圍道41號分行 新界沙田大圍道41-45號 2929 4288 Territories 74-76 Tai Wai Road, Sha Tin, New 74 Tai Wai Road Branch 大圍道74號分行 新界沙田大圍道74-76號 2699 9523 Territories 25 Wu Pak Street, Aberdeen, Hong Aberdeen Branch 香港仔分行 香港仔湖北街25號 2553 4165 Kong Shop 58, Aldrich Garden, Shau Kei Aldrich Garden Branch 愛蝶灣分行 香港筲箕灣愛蝶灣商舖58號 3196 4956 Wan, Hong Kong 13-15 Wai Fung Street, Ap Lei Chau, Ap Lei Chau Branch 鴨脷洲分行 香港鴨脷洲惠風街13-15號 2554 6487 Hong Kong Bank of China Tower Branch 中銀大廈分行 1 Garden Road, Hong Kong 香港花園道1號 2826 6888 Bonham Road Branch 般含道分行 63 Bonham Road, Hong Kong 香港般含道63號 2517 7066 Shop Nos. L187-195, Level 1, Butterfly Estate Branch 蝴蝶邨分行 Butterfly Plaza, Tuen Mun, New 新界屯門蝴蝶廣場地下L187-195號 2920 5188 Territories Caine Road Branch 堅道分行 57 Caine Road, Hong Kong 香港堅道57號 2521 3318 Cameron Road Wealth 30 Cameron -

Hong Kong Public Opinion Program of Hong Kong Public Opinion Research Institute

Hong Kong Public Opinion Program of Hong Kong Public Opinion Research Institute PopPanel Research Report No. 21 cum Community Democracy Project Research Report No. 18 cum Community Health Project Research Report No. 14 Survey Date: 7 May to 12 May 2020 Release Date: 13 May 2020 Copyright of this report was generated by the Hong Kong Public Opinion Program (HKPOP) and opened to the world. HKPOP proactively promotes open data, open technology and the free flow of ideas, knowledge and information. The predecessor of HKPOP was the Public Opinion Programme at The University of Hong Kong (HKUPOP). “POP” in this publication may refer to HKPOP or HKUPOP as the case may be. 1 HKPOP Community Health Project Report No. 14 Research Background Initiated by the Hong Kong Public Opinion Research Institute (HKPORI), the “Community Integration through Cooperation and Democracy, CICD” Project (or the “Community Democracy Project”) aims to provide a means for Hongkongers to re-integrate ourselves through mutual respect, rational deliberations, civilized discussions, personal empathy, social integration, and when needed, resolution of conflicts through democratic means. It is the rebuilding of our Hong Kong society starting from the community level following the spirit of science and democracy. For details, please visit: https://www.pori.hk/cicd. The surveys of Community Democracy (CD) Project officially started on 3 January 2020, targeting members of “HKPOP Panel” established by HKPORI in July 2019, including “Hong Kong People Representative Panel” (Probability-based Panel) and “Hong Kong People Volunteer Panel” (Non-probability-based Panel). This report also represents Report No. 21 under HKPOP Panel survey series, as well as Report No. -

Wong Tai Sin District Celebration Events Calendar

Celebration Events for the 20th Anniversary of the Establishment of the HKSAR Wong Tai Sin District Celebration Events Calendar Date/Time Name of Event Description Venue Organiser(s) Enquiry 14/1/2017 Wong Tai Sin Basketball To enhance the youngsters’ Morse Park Sports Wong Tai Sin District 3143 1142 10:30 – 17:00 Reunification Cup in sense of belonging to the Centre Office; Celebration of the 20th community and to celebrate the Wong Tai Sin Youth Email: Anniversary of the 20th Anniversary of the Development [email protected] Establishment of the Establishment of the HKSAR Network HKSAR with residents from different sectors in Wong Tai Sin district through this basketball tournament 11/2/2017 Commendation To commend the WTS Youth Wong Tai Sin Wong Tai Sin District 3143 1142 14:00 – 17:00 Ceremony for Wong Tai Pioneers with outstanding Temple Court Office; Sin Youth Pioneers cum performance and to celebrate Wong Tai Sin Youth Email: Drama Show in the 20th Anniversary of the Development [email protected] Celebration of the 20th Establishment of the HKSAR by a Network Anniversary of the drama performance Establishment of the HKSAR Celebration Events for the 20th Anniversary of the Establishment of the HKSAR Wong Tai Sin District Celebration Events Calendar Date/Time Name of Event Description Venue Organiser(s) Enquiry 13/2/2017 & Wong Tai Sin Soccer To build up the youngsters’ Lok Fu Recreation Wong Tai Sin District 3143 1142 16/2/2017 Reunification Cup in sense of pride and to celebrate Ground (Artificial Office; 18:30 – 21:30 Celebration -

Badminton Tournament Planner YONEX German Open Matches of Wednesday 02/03/2016

YONEX German Open Matches of Wednesday 02/03/2016 Date City, Country Website 01 - 06 Mar 2016 Mulheim an der Ruhr, GER http://www.german-open-badminton.de/home.html Time Event Court Round Team 1 Team 2 09:00 WD R32 Emilie Juul Moller+Cecilie Sentow (DEN) (NED) Samantha Barning+Iris Tabeling 09:00 MD R32 Matijs Dierickx+Freek Golinski (BEL) (JPN) Takeshi Kamura+Keigo Sonoda 09:00 WS Court 2 R32 Pai Yu Po (TPE) (JPN) Sayaka Sato[8] 09:15 WD R32 Huang Yaqiong+Tang Jinhua (CHN) (FRA) Marie Batomene+Emilie Lefel 09:15 WS Court 1 - TV R32 Lindaweni Fanetri (INA) (TPE) Hsu Ya Ching 09:45 WS R32 Maria Ulitina (UKR) (HKG) Yip Pui Yin 09:45 WD R32 Go Ah Ra+Yoo Hae Won (KOR) (TPE) Hsieh Pei Chen+Wu Ti Jung 09:45 MD Court 2 R32 Wang Yilyu+Zhang Wen (CHN) (KOR) Ko Sung Hyun+Shin Baek Cheol[6] 10:00 WD Court 1 - TV R32 Jongkolphan Kititharakul+Rawinda Prajongjai (THA) (FRA) Audrey Fontaine+Anne Tran 10:00 WS R32 Kirsty Gilmour (SCO) (JPN) Aya Ohori 10:30 WS Court 2 R32 Yui Hashimoto (JPN) (BEL) Lianne Tan 10:30 MD R32 Adam Cwalina+Przemyslaw Wacha (POL) (SWE) Richard Eidestedt+Nico Ruponen 10:30 WD R32 Nadia Fankhauser+Sannatasah Saniru (SUI/MAS) (KOR) Chang Ye Na+Lee So Hee[6] 10:45 WS R32 Minatsu Mitani (JPN) (KOR) Sung Ji Hyun[3] 10:45 MD Court 1 - TV R32 Puavaranukroh Dechapol+Kedren Kittinupong (THA) (RUS) Vladimir Ivanov+Ivan Sozonov[8] 11:15 WS R32 Maria Febe Kusumastuti (INA) (THA) Busanan Ongbumrungphan 11:15 WD R32 Heather Olver+Lauren Smith (ENG) (SWE) Clara Nistad+Emma Wengberg 11:15 MD Court 2 R32 Liao Min Chun+Tseng Min Hao (TPE) (FRA) -

A Data Compression Algorithm Based on Adaptive Huffman Code for Wireless Sensor Networks

2011 Fourth International Conference on Intelligent Computation Technology and Automation (ICICTA 2011) Shenzhen, China 28 – 29 March 2011 Volume 1 Pages 1-618 IEEE Catalog Number: CFP1188E-PRT ISBN: 978-1-61284-289-9 1/4 2011 Fourth International Conference on Intelligent Computation Technology and Automation ICICTA 2011 Table of Contents Volume - 1 Preface - Volume 1.....................................................................................................................................................xxv Conference Committees - Volume 1.......................................................................................................................xxvi Reviewers - Volume 1.............................................................................................................................................xxviii Session 1: Advanced Comptation Theory and Applications A Data Compression Algorithm Based on Adaptive Huffman Code for Wireless Sensor Networks .............................................................................................................................................................3 Mo Yuanbin, Qiu Yubing, Liu Jizhong, and Ling Yanxia A Genetic Algorithm for Solving Weak Nonlinear Bilevel Programming Problems ....................................................7 Yulan Xiao and Hecheng Li A Layering Learning Routing Algorithm of WSNs Based on ADS Approach ............................................................10 Wang Zhaoqing and Zhong Sheng A Load Distribution Optimization among -

Electoral Affairs Commission Report

i ABBREVIATIONS Amendment Regulation to Electoral Affairs Commission (Electoral Procedure) Cap 541F (District Councils) (Amendment) Regulation 2007 Amendment Regulation to Particulars Relating to Candidates on Ballot Papers Cap 541M (Legislative Council) (Amendment) Regulation 2007 Amendment Regulation to Electoral Affairs Commission (Financial Assistance for Cap 541N Legislative Council Elections) (Application and Payment Procedure) (Amendment) Regulation 2007 APIs announcements in public interest APRO, APROs Assistant Presiding Officer, Assistant Presiding Officers ARO, AROs Assistant Returning Officer, Assistant Returning Officers Cap, Caps Chapter of the Laws of Hong Kong, Chapters of the Laws of Hong Kong CAS Civil Aid Service CC Complaints Centre CCC Central Command Centre CCm Complaints Committee CE Chief Executive CEO Chief Electoral Officer CMAB Constitutional and Mainland Affairs Bureau (the former Constitutional and Affairs Bureau) D of J Department of Justice DC, DCs District Council, District Councils DCCA, DCCAs DC constituency area, DC constituency areas DCO District Councils Ordinance (Cap 547) ii DO, DOs District Officer, District Officers DPRO, DPROs Deputy Presiding Officer, Deputy Presiding Officers EAC or the Commission Electoral Affairs Commission EAC (EP) (DC) Reg Electoral Affairs Commission (Electoral Procedure) (District Councils) Regulation (Cap 541F) EAC (FA) (APP) Reg Electoral Affairs Commission (Financial Assistance for Legislative Council Elections and District Council Elections) (Application and Payment -

Annex Compulsory Testing Notices Issued by the Secretary for Food

Annex Compulsory Testing Notices issued by the Secretary for Food and Health on December 30, 2020 Amended List of Specified Premises 1. Hibiscus House, Ma Tau Wai Estate, 9 Shing Tak Street, Kowloon City, Kowloon, Hong Kong 2. David Mansion, 93-103 Woosung Street, Yau Ma Tei, Kowloon, Hong Kong 3. Tung Hoi House, Tai Hang Tung Estate, 88 Tai Hang Tung Road, Shek Kip Mei, Kowloon, Hong Kong 4. Un Mun House, Un Chau Estate, 303 Un Chau Street, Sham Shui Po, Kowloon, Hong Kong 5. Fu Wen House, Fu Cheong Estate, 19 Sai Chuen Road, Sham Shui Po, Kowloon, Hong Kong 6. Cherry House, So Uk Estate, 380 Po On Road, Sham Shui Po, Kowloon, Hong Kong 7. Tao Tak House, Lei Cheng Uk Estate, 10 Fat Tseung Street, Sham Shui Po, Kowloon, Hong Kong 8. Scenic Court, 451-461 Shun Ning Road, Sham Shui Po, Kowloon, Hong Kong 9. Block 11, Rhythm Garden, 242 Choi Hung Road, Wong Tai Sin, Kowloon, Hong Kong 10. Chi Siu House, Choi Wan (I) Estate, 45 Clear Water Bay Road, Wong Tai Sin, Kowloon, Hong Kong 11. Sau Man House, Choi Wan (I) Estate, 45 Clear Water Bay Road, Wong Tai Sin, Kowloon, Hong Kong 12. Kai Fai House, Choi Wan (II) Estate, 55 Clear Water Bay Road, Wong Tai Sin, Kowloon, Hong Kong 13. Ching Yuk House, Tsz Ching Estate, 80 Tsz Wan Shan Road, Wong Tai Sin, Kowloon, Hong Kong 14. Ching Tai House, Tsz Ching Estate, 80 Tsz Wan Shan Road, Wong Tai Sin, Kowloon, Hong Kong 15. -

Register of Public Payphone

Register of Public Payphone Operator Kiosk ID Street Locality District Region HGC HCL-0007 Chater Road Outside Statue Square Central and HK Western HGC HCL-0010 Chater Road Outside Statue Square Central and HK Western HGC HCL-0024 Des Voeux Road Central Outside Wheelock House Central and HK Western HKT HKT-2338 Caine Road Outside Albron Court Central and HK Western HKT HKT-1488 Caine Road Outside Ho Shing House, near Central - Mid-Levels Central and HK Escalators Western HKT HKT-1052 Caine Road Outside Long Mansion Central and HK Western HKT HKT-1090 Charter Garden Near Court of Final Appeal Central and HK Western HKT HKT-1042 Chater Road Outside St George's Building, near Exit F, MTR's Central Central and HK Station Western HKT HKT-1031 Chater Road Outside Statue Square Central and HK Western HKT HKT-1076 Chater Road Outside Statue Square Central and HK Western HKT HKT-1050 Chater Road Outside Statue Square, near Bus Stop Central and HK Western HKT HKT-1062 Chater Road Outside Statue Square, near Court of Final Appeal Central and HK Western HKT HKT-1072 Chater Road Outside Statue Square, near Court of Final Appeal Central and HK Western HKT HKT-2321 Chater Road Outside Statue Square, near Prince's Building Central and HK Western HKT HKT-2322 Chater Road Outside Statue Square, near Prince's Building Central and HK Western HKT HKT-2323 Chater Road Outside Statue Square, near Prince's Building Central and HK Western HKT HKT-2337 Conduit Road Outside Elegant Garden Central and HK Western HKT HKT-1914 Connaught Road Central Outside Shun Tak -

126 Chapter 19 SWD – Central and Islands 4/F, Harbour Building 2852

SWD – Central and Islands 4/F, Harbour Building 2852-3137 Integrated Family 38 Pier Road, Central Service Centre Hong Kong SWD – High Street G/F, Sai Ying Pun 2857-6867 Integrated Family Community Complex Service Centre 2 High Street, Sai Ying Pun Hong Kong SWD – Aberdeen Unit 2, G/F, Pik Long House 2875-8685 Integrated Family Shek Pai Wan Estate Service Centre Aberdeen, Hong Kong The Hong Kong Catholic G/F, La Maison Du Nord 2810-1105 Marriage Advisory Council 12 North Street – Grace and Joy Integrated Kennedy Town, Hong Kong Family Service Centre 126 Chapter 19 Caritas – Hong Kong – 3/F & 5/F, Caritas Jockey Club 2555-1993 Caritas Integrated Family Aberdeen Social Centre Service Centre – Aberdeen 20 Tin Wan Street (Tin Wan / Pokfulam) Aberdeen, Hong Kong The Neighbourhood 1/F, Carpark 1 3141-7107 Advice-Action Council Yat Tung Estate, Tung Chung – The Neighbourhood Lantau Island Advice-Action Council Tung Chung Integrated Services Centre Hong Kong Sheng Kung Shop 201, 2/F 2525-1929 Hui Welfare Council Fu Tung Shopping Centre Limited – Hong Kong Fu Tung Estate Sheng Kung Hui Tung Tung Chung, Lantau Island Chung Integrated Services SWD – Causeway Bay 2/F, Causeway Bay 2895-5159 Integrated Family Community Centre Service Centre 7 Fook Yum Road North Point, Hong Kong SWD – Quarry Bay 2/F & 3/F, The Hong Kong 2562-4783 Integrated Family Federation of Youth Groups Service Centre Building, 21 Pak Fuk Road North Point, Hong Kong SWD – Chai Wan (West) Level 4, Government Office 2569-3855 Integrated Family New Jade Garden Service Centre 233 Chai -

2013 New Frontiers for Greater Opportunities

2013 Annual Report Exploring New Frontiers f or Greater Opportunities BOC Hong Kong (Holdings) Limited BOC Hong Kong Annual Report 2013 Annual Report 52/F Bank of China Tower, 1 Garden Road, Hong Kong Website: www.bochk.com OUR VISION TO BE YOUR PREMIER BANK OUR MISSION OUR CORE VALUES Build Social Responsibility customer satisfaction and provide quality We care for and contribute to our communities and professional service Performance Be environmentally friendly for our better future Offer We measure results and reward achievement rewarding career opportunities and As a good corporate citizen, we do not use cultivate staff commitment Integrity lamination as normally adopted by the industry We uphold trustworthiness and business ethics in this report. Instead, we use varnishing, an Create environmentally friendly technique. The whole report values and deliver superior returns to Respect is also printed on recyclable and elemental chlorine shareholders We cherish every individual free paper. This demonstrates our efforts in working for the betterment of our future generations. Innovation Combining the initials of mission and We encourage creativity core values, we have Teamwork BOC SPIRIT We work together to succeed TdA – concept and design www.tda.com.hk Contents BOC Hong Kong (Holdings) Limited (“the Company”) was incorporated in Hong Kong on 12 September 2001 Financial Highlights 2 to hold the entire equity interest in Bank of China (Hong Kong) Limited (“BOCHK”), its principal operating subsidiary. Five-Year Financial Summary 3 Bank of China Limited holds a substantial part of its interests in the shares of the Company through BOC Hong Kong (BVI) Limited, an indirect wholly-owned Chairman’s Statement 6 subsidiary of Bank of China Limited.