2013 New Frontiers for Greater Opportunities

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Services for Ex-Offenders and Discharged Prisoners

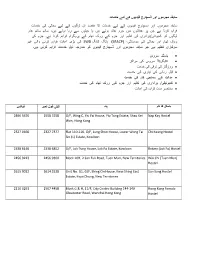

ﺳﺎﺑﻘہ ﻣﺟرﻣوں اور ڈﺳﭼﺎرج ﻗﯾدﯾوں ﮐﮯ ﻟﺋﮯ ﺧدﻣﺎت ﺳﺎﺑﻘہ ﻣﺠﺮﻣﻮں اور دﺳﭽﺎرج ﻗﯿﺪﯾﻮں ﮐﮯ ﻟﯿﮯ ﺧﺪﻣﺎت ﮐﺎ ﻣﻘﺼﺪ ان ﻟﻮﮔﻮں ﮐﮯ ﻟﯿﮯ ﺑﺤﺎﻟﯽ ﮐﯽ ﺧﺪﻣﺎت ﻓﺮاﮨﻢ ﮐﺮﻧﺎ ﮨﮯ ﺟﻦ ﭘﺮ ﻋﺪاﻟﺘﻮں ﻣﯿﮟ ﺟﺮم ﻋﺎﺋﺪ ﮨﻮﺋﮯ ﮨﯿﮟ ﯾﺎ ﺟﯿﻠﻮں ﺳﮯ رﮨﺎ ﮨﻮﺋﮯ ﮨﯿﮟ، ﺳﺎﺗﮭ ﺳﺎﺗﮭ ﻋﺎم ﻟﻮﮔﻮں ﮐﻮ ﮐﻤﯿﻮﻧﮣﯽ/ﺑﺮادری ﮐﯽ ﺗﻌﻠﯿﻢ اور ﺟﺮم ﮐﮯ روک ﺗﮭﺎم ﮐﮯ ﭘﺮوﮔﺮام ﻓﺮاﮨﻢ ﮐﺮﻧﺎ ﮨﮯ۔ ﺟﺮم ﮐﯽ روک ﺗﮭﺎم اور ﺑﺤﺎﻟﯽ ﮐﯽ ﺳﻮﺳﺎﺋﮣﯽ، (SRACP) ﮨﺎﻧﮓ ﮐﺎﻧﮓ SWD ﮐﯽ ﺑﮍی اﻋﺎﻧﺖ ﻓﺮاﮨﻢ ﮐﺮﻧﯽ واﻟﯽ ﻏﯿﺮ ﺳﺮﮐﺎری ﺗﻨﻈﯿﻢ ﮨﮯ ﺟﻮ ﺳﺎﺑﻘہ ﻣﺠﺮﻣﻮں اور ڈﺳﭽﺎرج ﻗﯿﺪﯾﻮں ﮐﻮ ﻣﻨﺪرﺟہ ذﯾﻞ ﺧﺪﻣﺎت ﻓﺮاﮨﻢ ﮐﺮﺗﯽ ﮨﮯ۔ • ﮨﺎﺳﮣﻞ ﺳﺮوس • اﻧﮣﯿﮕﺮﯾﮣﮉ ﺳﺮوس ﮐﯽ ﻣﺮاﮐﺰ • روزﮔﺎر ﮐﯽ ﺗرﻗﯽ ﮐﯽ ﺧدﻣت • ﻗﺒﻞ رﮨﺎﺋﯽ ﮐﯽ ﺗﯿﺎری ﮐﯽ ﺧﺪﻣﺖ • ﻋﺪاﻟﺖ ﮐﮯ ﺳﻤﺎﺟﯽ ﮐﺎم ﮐﯽ ﺧﺪﻣﺖ • ﮐﻤﯿﻮﻧﯿﮣﯽ/ ﺑﺮاداری ﮐﯽ ﺗﻌﻠﯿﻢ اور ﺟﺮم ﮐﮯ روک ﺗﮭﺎم ﮐﯽ ﺧﺪﻣﺖ • ﻣﺧﺗﺻر ﻣدت ﮐراﯾہ ﮐﯽ اﻋﺎﻧت ﮨﺎﺳﮣﻞ ﮐﺎ ﻧﺎم ﭘﺘہ ﮢﯿﻠﯽ ﻓﻮن ﻧﻤﺒﺮ ﻓﯿﮑﺲ 2896 5676 2558 3258 G/F, Wing C, Yiu Fai House, Yiu Tung Estate, Shau Kei Nap Kay Hostel Wan, Hong Kong 2327 0666 2327 7377 Flat 110-116, G/F, Lung Shun House, Lower Wong Tai Chi Keung Hostel Sin (1) Estate, Kowloon 2338 6146 2338 6852 G/F, Lok Tung House, Lok Fu Estate, Kowloon Rotary (Lok Fu) Hostel 2456 9223 2456 9300 Block 10H, 2 San Fuk Road, Tuen Mun, New Territories Wai Chi (Tuen Mun) Hostel 2615 9032 2614 2528 Unit No. G1, G/F, Shing On House, Kwai Shing East Sun Sang Hostel Estate, Kwai Chung, New Territories 2110 0291 2507 4458 Block G & H, 11/F, City Centre Building 144-149 Hong Kong Female Gloucester Road, Wanchai Hong Kong Hostel اﻧﮣﯿﮕﺮﯾﮣﮉ ﺳﺮوس ﮐﯽ ﻣﺮاﮐﺰ ﮐﯽ ﻓﮩﺮﺳﺖ ﻣﺮﮐﺰ ﮐﺎ ﻧﺎم ﭘﺘہ ﮢﯿﻠﯽ ﻓﻮن ﻧﻤﺒﺮ ﻓﯿﮑﺲ Hong Kong Integrated Service Centre for Social Rehabilitation & G/F, Li Chit Garden,1 Li Chit Street, Wanchai, Hong Community Support 2865 6448 2866 7867 Kong - Hong Kong Revival Hub Kowloon East Integrated Service Centre for Social Rehabilitation & 2321 7900 2352 3398 Unit Nos. -

中銀香港分行資料BOCHK Branch Information Branch Name 分行名稱

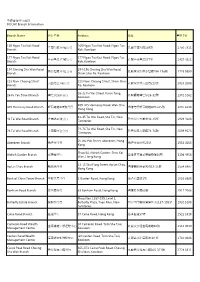

中銀香港分行資料 BOCHK Branch Information Branch Name 分行名稱 Address 地址 電話 Tel 169 Ngau Tau Kok Road 169 Ngau Tau Kok Road, Ngau Tau 牛頭角道169號分行 九龍牛頭角道169號 2750 7311 Branch Kok, Kowloon 177 Ngau Tau Kok Road 177 Ngau Tau Kok Road, Ngau Tau 牛頭角道177號分行 九龍牛頭角道177號 2927 4321 Branch Kok, Kowloon 194 Cheung Sha Wan Road 194-196 Cheung Sha Wan Road, 長沙灣道194號分行 九龍深水埗長沙灣道194-196號 2728 9389 Branch Sham Shui Po, Kowloon 223 Nam Cheong Street 223 Nam Cheong Street, Sham Shui 南昌街223號分行 九龍深水埗南昌街223號 2928 2088 Branch Po, Kowloon 26-32 Fu Yan Street, Kwun Tong, 26 Fu Yan Street Branch 輔仁街26號分行 九龍觀塘輔仁街26-32號 2342 5262 Kowloon 409-415 Hennessy Road, Wan Chai, 409 Hennessy Road Branch 軒尼詩道409號分行 香港灣仔軒尼詩道409-415號 2835 6118 Hong Kong 41-45 Tai Wai Road, Sha Tin, New 41 Tai Wai Road Branch 大圍道41號分行 新界沙田大圍道41-45號 2929 4288 Territories 74-76 Tai Wai Road, Sha Tin, New 74 Tai Wai Road Branch 大圍道74號分行 新界沙田大圍道74-76號 2699 9523 Territories 25 Wu Pak Street, Aberdeen, Hong Aberdeen Branch 香港仔分行 香港仔湖北街25號 2553 4165 Kong Shop 58, Aldrich Garden, Shau Kei Aldrich Garden Branch 愛蝶灣分行 香港筲箕灣愛蝶灣商舖58號 3196 4956 Wan, Hong Kong 13-15 Wai Fung Street, Ap Lei Chau, Ap Lei Chau Branch 鴨脷洲分行 香港鴨脷洲惠風街13-15號 2554 6487 Hong Kong Bank of China Tower Branch 中銀大廈分行 1 Garden Road, Hong Kong 香港花園道1號 2826 6888 Bonham Road Branch 般含道分行 63 Bonham Road, Hong Kong 香港般含道63號 2517 7066 Shop Nos. L187-195, Level 1, Butterfly Estate Branch 蝴蝶邨分行 Butterfly Plaza, Tuen Mun, New 新界屯門蝴蝶廣場地下L187-195號 2920 5188 Territories Caine Road Branch 堅道分行 57 Caine Road, Hong Kong 香港堅道57號 2521 3318 Cameron Road Wealth 30 Cameron -

Official Record of Proceedings

LEGISLATIVE COUNCIL ─ 3 November 2010 1399 OFFICIAL RECORD OF PROCEEDINGS Wednesday, 3 November 2010 The Council met at Eleven o'clock MEMBERS PRESENT: THE PRESIDENT THE HONOURABLE JASPER TSANG YOK-SING, G.B.S., J.P. THE HONOURABLE ALBERT HO CHUN-YAN IR DR THE HONOURABLE RAYMOND HO CHUNG-TAI, S.B.S., S.B.ST.J., J.P. THE HONOURABLE LEE CHEUK-YAN DR THE HONOURABLE DAVID LI KWOK-PO, G.B.M., G.B.S., J.P. THE HONOURABLE FRED LI WAH-MING, S.B.S., J.P. DR THE HONOURABLE MARGARET NG THE HONOURABLE JAMES TO KUN-SUN THE HONOURABLE CHEUNG MAN-KWONG THE HONOURABLE CHAN KAM-LAM, S.B.S., J.P. THE HONOURABLE MRS SOPHIE LEUNG LAU YAU-FUN, G.B.S., J.P. THE HONOURABLE LEUNG YIU-CHUNG DR THE HONOURABLE PHILIP WONG YU-HONG, G.B.S. 1400 LEGISLATIVE COUNCIL ─ 3 November 2010 THE HONOURABLE WONG YUNG-KAN, S.B.S., J.P. THE HONOURABLE LAU KONG-WAH, J.P. THE HONOURABLE LAU WONG-FAT, G.B.M., G.B.S., J.P. THE HONOURABLE MIRIAM LAU KIN-YEE, G.B.S., J.P. THE HONOURABLE EMILY LAU WAI-HING, J.P. THE HONOURABLE ANDREW CHENG KAR-FOO THE HONOURABLE TIMOTHY FOK TSUN-TING, G.B.S., J.P. THE HONOURABLE TAM YIU-CHUNG, G.B.S., J.P. THE HONOURABLE ABRAHAM SHEK LAI-HIM, S.B.S., J.P. THE HONOURABLE LI FUNG-YING, S.B.S., J.P. THE HONOURABLE TOMMY CHEUNG YU-YAN, S.B.S., J.P. THE HONOURABLE FREDERICK FUNG KIN-KEE, S.B.S., J.P. -

Bank of China Limited, Luxembourg Branch

http://www.oblible.com BANK OF CHINA (LUXEMBOURG) S.A. (incorporated with limited liability under the laws of Luxembourg) Issue of EUR 800,000,000 0.125 per cent. Notes due 2023 Guaranteed by Bank of China Limited, Luxembourg Branch under the U.S.$40,000,000,000 Medium Term Note Programme of Bank of China Limited ______________ These Listing Particulars (the “Listing Particulars”) are prepared in connection with the U.S.$40,000,000,000 Medium Term Note Programme (the “Programme”) established by Bank of China Limited (the “Bank”), and the EUR 800,000,000 0.125 per cent. Notes due 2023 (the “Notes”) to be issued by Bank of China (Luxembourg) S.A. (the “Issuer”) and unconditionally and irrevocably guaranteed by Bank of China Limited, Luxembourg Branch (the “Guarantor”) on 16 January 2020 under the Programme. The Offering Circular in respect of the Programme dated 4 April 2019 (the “Principal Offering Circular”) as supplemented by the supplemental offering circular dated 8 October 2019 (the “Supplement”) and the second supplemental offering circular dated 8 October 2019 (the “Second Supplement”, and together with the Principal Offering Circular and the Supplement, the “Offering Circular”), is set out in Annex A hereto and forms part of these Listing Particulars. Terms defined in the Offering Circular have the same meaning when used in these Listing Particulars. Pursuant to the Approval by the Enterprise Borrowing Foreign Debt Registration Certificate of [2019] (《企业借用外债备案登记证明》(发改办外资备 [[2019]51 号])) issued by the NDRC General Office on 24 January 2019 (the “NDRC Approval”), the Bank is not required to complete the pre-issuance registration in respect of the Notes with the NDRC as the Notes will be issued within the NDRC Approval. -

Prospectus E.Pdf

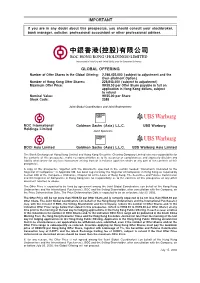

IMPORTANT If you are in any doubt about this prospectus, you should consult your stockbroker, bank manager, solicitor, professional accountant or other professional adviser. (Incorporated in Hong Kong with limited liability under the Companies Ordinance) GLOBAL OFFERING Number of Offer Shares in the Global Offering: 2,298,435,000 (subject to adjustment and the Over-allotment Option) Number of Hong Kong OÅer Shares: 229,843,500 (subject to adjustment) Maximum OÅer Price: HK$9.50 per OÅer Share payable in full on application in Hong Kong dollars, subject to refund Nominal Value: HK$5.00 per Share Stock Code: 2388 Joint Global Coordinators and Joint Bookrunners BOC International Goldman Sachs (Asia) L.L.C. UBS Warburg Holdings Limited Joint Sponsors BOCI Asia Limited Goldman Sachs (Asia) L.L.C. UBS Warburg Asia Limited The Stock Exchange of Hong Kong Limited and Hong Kong Securities Clearing Company Limited take no responsibility for the contents of this prospectus, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this prospectus. A copy of this prospectus, together with the documents speciÑed in the section headed ""Documents Delivered to the Registrar of Companies'' in Appendix VIII, has been registered by the Registrar of Companies in Hong Kong as required by Section 38D of the Companies Ordinance, Chapter 32 of the Laws of Hong Kong. The Securities and Futures Commission and the Registrar of Companies in Hong Kong take no responsibility as to the contents of this prospectus or any other document referred to above. -

Chiyu Banking Corporation Limited Or 2

DIRECT DEBIT AUTHORISATION 直接付款授權書 Application method: 申請方法: 1. Return this form to any branch of Chiyu Banking Corporation Limited or 2. Mail this form to “3/F, Bank of China Centre, 1. 將此表格交回任何一間集友銀行有限公司的分行 或 2. 郵寄表格至“西九龍海輝道 11 號奧海城 Olympian City, 11 Hoi Fai Road, West Kowloon, Hong Kong Attn: Autopay Section” or 3. Via Personal Internet Banking 中銀 中心 3 樓, 送:自動轉賬組”或 3.經個人網上銀行透過「雙重認証」辦理(毋需填寫此表格) with the use of two factor authentication (No need to fill in this form) Please write in BLOCK letters. 請以英文正楷填寫 Customer Information 客戶資料 My/Our Bank Name and Branch 本人/吾等之銀行及分行之名稱 Bank No.銀行編號 Branch No.分行編號 My/Our Account No.本人/吾等之賬戶號碼 Chiyu Banking Corporation Ltd My/Our Name(s) as recorded on Statement/Passbook 本人/吾等在結單/存摺上所紀錄之名稱 貨幣 Currency: Contact Tel No.聯絡電話號碼 HKD Please set up the following Direct Debit Authorisation Records marked with “” for me/us.請為本人(吾等)設立下列已選取 “” 號之直接付款授權紀錄。 Name of Party to be Credited (The Beneficiary) Account no. to be credited †Debtor’s Reference (Compulsory Field) †Limit for Each Payment †Expiry Date 到期日 收款方 (受益人) 收款賬戶號碼 債務人參考 (必須填寫) 每次付款之限額 (DD/MM/YY) (日/月/年) 港幣 HK$: HR21 Limited 012-737-10230564 1. I/We hereby authorise my/our above named Bank to effect transfers from my/our account to the above account in accordance with such instructions as my/our Bank may receive from the beneficiary and/or its banker and/or its banker’s correspondent from time to time provided always that the amount of any one such transfer shall not exceed the limit indicated above. -

Wong Tai Sin District Celebration Events Calendar

Celebration Events for the 20th Anniversary of the Establishment of the HKSAR Wong Tai Sin District Celebration Events Calendar Date/Time Name of Event Description Venue Organiser(s) Enquiry 14/1/2017 Wong Tai Sin Basketball To enhance the youngsters’ Morse Park Sports Wong Tai Sin District 3143 1142 10:30 – 17:00 Reunification Cup in sense of belonging to the Centre Office; Celebration of the 20th community and to celebrate the Wong Tai Sin Youth Email: Anniversary of the 20th Anniversary of the Development [email protected] Establishment of the Establishment of the HKSAR Network HKSAR with residents from different sectors in Wong Tai Sin district through this basketball tournament 11/2/2017 Commendation To commend the WTS Youth Wong Tai Sin Wong Tai Sin District 3143 1142 14:00 – 17:00 Ceremony for Wong Tai Pioneers with outstanding Temple Court Office; Sin Youth Pioneers cum performance and to celebrate Wong Tai Sin Youth Email: Drama Show in the 20th Anniversary of the Development [email protected] Celebration of the 20th Establishment of the HKSAR by a Network Anniversary of the drama performance Establishment of the HKSAR Celebration Events for the 20th Anniversary of the Establishment of the HKSAR Wong Tai Sin District Celebration Events Calendar Date/Time Name of Event Description Venue Organiser(s) Enquiry 13/2/2017 & Wong Tai Sin Soccer To build up the youngsters’ Lok Fu Recreation Wong Tai Sin District 3143 1142 16/2/2017 Reunification Cup in sense of pride and to celebrate Ground (Artificial Office; 18:30 – 21:30 Celebration -

Printed Version for Despatch to Shareholders (PDF: 9281KB)

Stock Code: 2388 BOC Hong Kong (Holdings) Limited Annual Report 2009 52/F Bank of China Tower, 1 Garden Road, Hong Kong Website: www.bochk.com Solid FOUNDatIONS for SUSTAINABLE GROWTH Annual Report 2009 Theme Hong Kong’s modern cityscape is complemented by its wealth of natural resources. The formation of these world-class rock and geological features takes hundred million of years. Hong Kong Geopark helps ensure that our future generations will be able to enjoy the legacy of these beautiful natural wonders. The Group takes great pleasure in pioneering the “Hong Kong Geopark Charity Green Walk”, a key focus of our Corporate Social Responsibility (CSR) programme in the year ahead. Our commitment to CSR is at the heart of our long-term competitiveness, enabling younger generations to enjoy the natural environment we are endowed with, and contributing to the sustainable development of the economy, society and environment as a whole. By embracing CSR, we reinforce our vision of becoming the premier bank of choice and creating greater value for our customers, shareholders and employees. OUR VISION TO BE YOUR PREMIER BANK OUR MISSION OUR CORE VALUES Build Social Responsibility customer satisfaction and provide quality We care for and contribute to our communities and professional service Performance Offer We measure results and reward achievement rewarding career opportunities and cultivate staff commitment Integrity We uphold trustworthiness and business ethics Create values and deliver superior returns to Respect shareholders We cherish every individual Innovation Combining the initials of mission and We encourage creativity core values, we have Teamwork BOC SPIRIT We work together to succeed Be environmentally friendly for our better future: As a good corporate citizen, we do not use lamination as normally adopted by the industry in our Annual Report 2009. -

Property Management Revenue from Property Management for 2003 Increased by 11.0% Over 2002 to HK$94 Million

032 Executive management’s report Property review This caused revenue from investment properties for the year of our properties further and establishing them as a to decline slightly by 1% over 2002 to HK$888 million. benchmark for the industry in Hong Kong. Our staff performed outstandingly during the period of SARS For Two IFC, the quality of the office building and its to ensure shoppers’safety and mitigate the effects of the management enabled MTR to attract tenants despite the outbreak on public confidence. We also supported tenants lingering cautious sentiment resulting from SARS, the war in through aggressive promotion campaigns, including an Iraq and the weak economy. Considerable effort was taken attractive rebate promotion. Within this context, we took full to explain to potential tenants, agents and the business advantage of the relaxation of travel restrictions on tourists community the merits of the building, which is ideally suited from Mainland China through proactive, tailor-made to the sophisticated needs of multi-national corporations. programmes, such as organising shopping tours, designed The decision by Swiss banking giant UBS to lease seven floors to bring high spending Mainland visitors to our shopping represented one of the largest and highest profile relocations centres. These programmes proved successful in boosting of an office tenant in Hong Kong in 2003. UBS joined a growing the business turnover of our tenants. list of leading institutions in the building, including the Hong The Total Quality Service Regime, our pioneering customer Kong Monetary Authority, reinforcing Two IFC’s position as the service enhancement programme, and our computerised building of choice for top-tier corporations. -

Tuenmun 20191018 E.Pdf

NOMINATIONS FOR THE 2019 DISTRICT COUNCIL ORDINARY ELECTION (NOMINATION PERIOD: 4 - 17 OCTOBER 2019) TUEN MUN DISTRICT As at 5pm, 17 October 2019 (Thursday) Constituency Constituency Name of Nominees Alias Gender Occupation Political Affiliation Date of Nomination Remarks Code (Surname First) L01 Tuen Mun Town Centre LAI Chun-wing Alfred M Legislative Councillor Assistant The Democratic Party 4/10/2019 L01 Tuen Mun Town Centre AU Chi-yuen M Civil Engineer 17/10/2019 L02 Siu Chi LAM Chung-hoi M Full Time District Councillor The Democratic Party 4/10/2019 L02 Siu Chi WONG Ka-leung M 14/10/2019 L03 On Ting FUNG Pui-yin M Community Officer FTU, DAB 4/10/2019 L03 On Ting KONG Fung-yi F ADPL 15/10/2019 L04 Siu Tsui YIP Man-pan M Member of Tuen Mun District Council DAB 4/10/2019 L04 Siu Tsui YAN Pui-lam M Illustrator Power for Democracy, Team Chu Hoi Dick of NTW 8/10/2019 L05 Yau Oi South LAM Kin-cheung M Community Organizer Labour Party 8/10/2019 L05 Yau Oi South TSANG Hin-hong M RSW, Full Time District Council Member DAB 9/10/2019 L06 Yau Oi North IP Chun-yuen M Solicitor DAB 4/10/2019 L06 Yau Oi North LAM Ming-yan M Community Organizer Labour Party 8/10/2019 L07 Tsui Hing POON Chi-kin M Community Officer Tuen Mun Community Network 4/10/2019 L07 Tsui Hing CHU Yiu-wah M District Councilor Roundtable 10/10/2019 L08 Shan King WONG Tan-ching M Registered Social Worker Tuen Mun Community Network 4/10/2019 L08 Shan King NG Dip-pui F Community Worker Independent Candidate 9/10/2019 L09 King Hing LAW Cheuk-yung M Social Worker Tuen Mun Community Network -

Minutes Of“Reduce, Recycle and Propoer Waste Management”For

CB(1) 1369/11-12(01) For discussion on 26 March 2012 LEGISLATIVE COUNCIL PANEL ON ENVIRONMENTAL AFFAIRS “REDUCE, RECYCLE AND PROPER WASTE MANAGEMENT”: (i) Progress of the Key Initiatives under the Waste Management Strategy (ii) 5177DR: Integrated Waste Management Facilities (IWMF) Phase 1 (iii) 5163DR: Northeast New Territories (NENT) landfill extension (v) 5164DR: Southeast New Territories (SENT) landfill extension (vi) 5165DR: West New Territories (WENT) landfill extension 1. PURPOSE 1.1 Hong Kong faces an imminent waste management problem as the three existing landfills would exhaust their design capacity one by one in the mid and end 2010s. In January 2011, the Government announced an action agenda on the implementation of initiatives that would help achieve a sustainable waste management solution for Hong Kong, using the Policy Framework for the Management of Municipal Solid Waste (2005-2014) (The MSW Policy Framework) as the basis. The action agenda listed concrete actions for resolving Hong Kong’s waste problem under a three-pronged approach that includes (i) strengthened actions to reduce wastes at source, (ii) introduction of modern technologies to upgrade our waste treatment capability, and (ii) timely extension of landfill, at a reduced scale with the implementation of (i) and (ii). This paper – (a) updates Members on the progress of waste reduction and recycling initiatives under the action agenda; 1 (b) seeks Members’ support for our proposals to – (i) upgrade 5177DR to Category A at an estimated cost of $14,960.1 million in money-of-the-day (MOD) prices (or $11,383.0 million in September 2011 prices); (ii) upgrade 5163DR to Category A at an estimated cost of $6,631.7 million in MOD prices (or $3,969.8 million in September 2011 prices); (iii) upgrade 5164DR to Category A at an estimated cost of $1,759.4 million in MOD prices (or $1,254.3 million in September 2011 prices); and (iv) upgrade part of 5165DR to Category A at an estimated cost of $33.4 million in MOD prices (or $26.1 million in September 2011 prices). -

Minutes of the First Meeting of the Traffic and Transport Committee Under the Yuen Long District Council in 2020

The minutes were confirmed on 12.3.2020 without amendment. Minutes of the First Meeting of the Traffic and Transport Committee under the Yuen Long District Council in 2020 Date : 23 January 2020 (Thursday) Time : 5:53 p.m. - 7:30 p.m. Venue : Conference Room, Yuen Long District Council, 13/F., Yuen Long Government Offices, 2 Kiu Lok Square, Yuen Long Present Time of Arrival Time of Withdrawal Members: Mr AU Kwok-kuen Beginning of the meeting 6:05 p.m. Mr CHAN King-lun, Kisslan Beginning of the meeting End of the meeting Ms CHAN Mei-lin Beginning of the meeting End of the meeting Mr CHAN Shu-fai Beginning of the meeting End of the meeting Ms CHAN Sze-nga Beginning of the meeting End of the meeting Mr CHEUNG Chi-yeung, Felix Beginning of the meeting End of the meeting Mr CHEUNG Sau-yin Beginning of the meeting End of the meeting Mr FONG Ho-hin Beginning of the meeting End of the meeting Mr HAU Man-kin Beginning of the meeting 6:35 p.m. Mr HO Wai-pan Beginning of the meeting 6:40 p.m. Mr HONG Chin-wah Beginning of the meeting End of the meeting Mr KWAN Chun-sang Beginning of the meeting 6:40 p.m. Mr KWOK Man-ho Beginning of the meeting End of the meeting Mr LAI Kwok-wing, Samuel Beginning of the meeting End of the meeting Ms LAI Po-wa Beginning of the meeting 6:00 p.m. Mr LAM Chun Beginning of the meeting 6:40 p.m.