Chapter Iv Land Revenue

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2019071371.Pdf

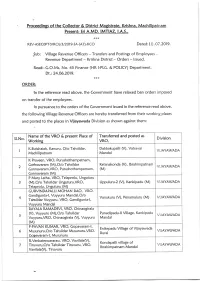

.:€ ' Proceedings of the Collector & District Magistrate. Krishna, Machilipatnam Present: Sri A.MD. lMTlAZ, 1.A.5.. >kJ.* REV-A5ECoPT(VRO)/3 /2o1s-sA-(A7)-KCo Dated: l0 .07.2019. Sub: Village Revenue Officers - Transfers and Postings of Employees - Revenue Department - Krishna District - Orders - lssued. Read:- 6.O.Ms, No. 45 Finance (HR l-P16. & POLICY) Department, Dt.:24.06.2019. ,( :k )k ORDER: {n the reference read above, the Government have relaxed ban orders imposed on transfer of the employees. ln pursuance to the orders of the Government issued in the reference read above, the following Village Revenue Officers are hereby transferred from their working places and posted to the places in Vijayawada Division as shown against them: :' Name of the VRO & present Place of Transferred and posted as 5l.No. Division Working VRO, K.Butchaiah, Kanuru, O/o Tahsildar, Dabbakupalli (V), Vatsavai I VIJAYAWADA Machilipatnam Mandal K Praveen, VRO, Purushothampatnam, 6arlnavaram (M),O/o Tahsildar Ketanakonda (V), lbrahimpatnam 2 VIJAYAWADA Gannavaram,VRO, Purushothampatnam, (M) Gannavaram (M) P Mary Latha, VRO, Telaprolu, Unguturu 3 (M),O/o Tahsildar Unguturu,VRO, Uppuluru-2 (V), Kankipadu (M) VIJAYAWADA Telaprolu, Unguturu (M) GURVINDAPALLI MOHAN RAO, VRO, 6andigunta-1, Vuyyuru Mandal,O/o 4 Vanukuru (V), Penamaluru (M) VIJAYAWADA TaLxildar Vuyyuru, VRO, Gandigunta-1, Vuwuru Mandal RAYALA RAMADEVI, VRO, Chinaogirala (V), Vuyyuru (M),O/o Tahsildar Punadipadu-ll Village, Kankipadu 5 VIJAYAWADA Vuyyuru,VRO, Chinaogirala (V), Vuyyuru Mandal (M) P-PAVAN KUMAR, VRO, Gopavaram-|, Enikepadu Village of Vijayawada 6 Musunuru,O/o Tahsildar Musunuru,VRO, VIJAYAWADA Rural Gopavaram-|, Musunuru VRO, Vavi lala (V), R.Venkateswararao, Kondapallivillage of 7 Tiruvuru,O/o Tahsildar Tiruvuru, VRO, VIJAYAWADA lbrahimpatnam Mandal Vavilala(V), Tiruvuru M.fhantibabu, VRO, Pamidimukkala,O/o Northvalluru I of Thotlavalluru 8 Tahsildar Pamidimukkala.VRO. -

District Survey Report - 2018

District Survey Report - 2018 4 DEPARTMENT OF MINES AND GEOLOGY Government of Andhra Pradesh DISTRICT SURVEY REPORT - KRISHNA DISTRICT Prepared by ANDHRA PRADESH SPACE APPLICATIONS CENTRE (APSAC) ITE & C Department, Govt. of Andhra Pradesh 2018 i District Survey Report - 2018 ACKNOWLEDGEMENTS APSAC wishes to place on record its sincere thanks to Sri. B.Sreedhar IAS, Secretary to Government (Mines) and the Director, Department of Mines and Geology, Govt. of Andhra Pradesh for entrusting the work for preparation of District Survey Reports of Andhra Pradesh. The team gratefully acknowledge the help of the Commissioner, Horticulture Department, Govt. of Andhra Pradesh and the Director, Directorate of Economics and Statistics, Planning Department, Govt. of Andhra Pradesh for providing valuable statistical data and literature. The project team is also thankful to all the Joint Directors, Deputy Directors, Assistant Directors and the staff of Mines and Geology Department for their overall support and guidance during the execution of this work. Also sincere thanks are due to the scientific staff of APSAC who has generated all the thematic maps. VICE CHAIRMAN APSAC ii District Survey Report - 2018 Contents Page Acknowledgements List of Figures List of Tables 1 Salient Features of Krishna District 1 1.1 Administrative Setup 1 1.2 Drainage 2 1.2a Kolleru Lake- A eco-sensitive zone 4 1.3 Climate and Rainfall 4 1.4 Transport and Communications 9 1.5 Population and Literacy 10 1.6 Important Places 11 1.6a Places of Tourist Interest 11 1.6b Places of -

Krishna District Machilipatnam Ph-223602 Krishna District Cell-9885395597 12

11. SRI KOMPELLA GOPAL MACHILIPATNAM RICE MILL,SARPANCH VARI STREET BUTTAI PETA 1. SRI KALAPU GOPALAKRISHNA MURTHY MACHILIPATNAM D NO-5/323-1 ,JAVVARUPET KRISHNA DISTRICT MACHILIPATNAM PH-223602 KRISHNA DISTRICT CELL-9885395597 12. SRI GHANTASALA VENKATA SUBBA RAO PH - 08672 227602 , 220663 PANJA SIDE STREET,KENNADI ROAD RAMANAIDU PET 2. SRI KALAPU LAKSHMI SATYANARAYANA MACHILIPATNAM CIRCLE PETA , MACHILIPATNAM KRISHNA DISTRICT KRISHNA DISTRICT PH-229600 CELL-9440317352 , 08672 225478 13. SRI GAMINI SRINIVAS 3. SRI KALAPU GANESH KOTESWARARAO PANJA SIDE STREET,KENNADI ROAD D NO-5/323-1 ,JAVVARUPET RAMANAIDU PET MACHILIPATNAM MACHILIPATNAM KRISHNA DISTRICT KRISHNA DISTRICT PH, 08672 227602 PH-229600 4. SRI KALAPU PRASAD RAO 14. SRI VEERAMALLU GOPAL MANGALI VAARI STREET ENGLISH PALEM CENTRE CIRCLE PETA , MACHILIPATNAM MACHILIPATNAM KRISHNA DISTRICT KRISHNA DISTRICT CELL- 9440107161 PH-226852 5. SRI KALAPU DURGA NAGA 15. SRI VEERAMALLU SRINIVASARAO MALLESWARARAO D NO-22/85-1 ,BACHU PET MANGALI VAARI STREET MACHILIPATNAM CIRCLE PETA , MACHILIPATNAM KRISHNA DISTRICT KRISHNA DISTRICT CELL-9948264551 6. SRI KALAPU PURNACHANDRARAO 16. SRI KUKUNURU GOPAL (BABURAO) D NO-22-85 , ,BACHU PET OPP TO;-NARASIMHASWAMY TEMPLE MACHILIPATNAM, KRISHNA DISTRICT JALAL PET ;,MACHILIPATNAM KRISHNA DISTRICT 17. SRI YADAVALLY MURALI CELL-9290625731 D NO -7 /221 – 3 ,PADMAPRIYA BULDINGS KANYAKA RICE MILL ROAD, GODUGUPET, 7. SRI KALAPU SANKARA SOMAIAH MACHILIPATNAM KENNADI ROAD,JAVVARUPET KRISHNA DISTRICT MACHILIPATNAM CELL-9848263624 KRISHNA DISTRICT CELL-9966632242 18. SRI PENDYALA GANESH BABU PARASUPETA 8. SRI VEERAMALLU NAGAKRISHNATEJA MACHILIPATNAM KRISHNA DISTRICT 9. SRI DEVAGANUGALA VENKATA SATYA PH-251763 SUBRAMANYAM RICE MILL,SARPANCH VARI STREET 19. SRI GHANTASALA NAGARAJU BUTTAI PETA, MACHILIPATNAM PLAT NO 17 ,NGO’S COLONY KRISHNA DISTRICT PARASUPETA, CHILAKALAPUDI PH-223602 MACHILIPATNAM KRISHNA DISTRICT 10. -

Assessment of Ground Water Quality Using Water Quality Index

International Journal of Innovative Research in Advanced Engineering (IJIRAE) ISSN: 2349-2163 Issue 3, Volume 2 (March 2015) www.ijirae.com ASSESSMENT OF GROUND WATER QUALITY USING WATER QUALITY INDEX K. Sundara Kumar1*, Ch. Satish Kumar2, K. Hari Prrasad3, B. Rajesh4, R. Sivaram Prasad5 , T. Venkatesh6 1Associate Professor and Head, Department of Civil Engineering,2-6 Final B.Tech., Civil, Usha Rama College of Engineering & Technology, Telaprolu, Krishna District, Andhra Pradesh, India. ABSTRACT-- Ground water is one of the important fresh water resources available for human consumption. Early people recognized the importance of water from a quantity view point. However assessment of the quality of ground water is essential for improving its potability. In this project work we have estimated the water quality of Bapulapadu Mandal which is located 10km away from the Gannavaram airport on east coast of Krishna district of Andhra Pradesh, India. Water quality is tested for about 10 physico-chemical parameters of 90 water samples collected from various locations of 27 villages from Bapulapadu Mandal. The ground water samples are collected manually from the bore wells which were approximately equally distributed all over 27 villages of Bapulapadu Mandal. The samples were analyzed using MULTI- PARAMETER TEST KIT, which provide quick and easy water quality testing in the field. The combined effect of all there parameters was expressed in terms of WATER QUALITY INDEX. Bapulapadu Mandal map has been collected and analyzed. The data base obtained from water quality testing is used as attribute data base for preparation of thematic maps showing the spatial distribution of various water quality parameters. -

Meos & MIS Co-Ordinators

List of MEOs, MIS Co-orfinators of MRC Centers in AP Sl no District Mandal Name Designation Mobile No Email ID Remarks 1 2 3 4 5 6 7 8 1 Adilabad Adilabad Jayasheela MEO 7382621422 [email protected] 2 Adilabad Adilabad D.Manjula MIS Co-Ordinator 9492609240 [email protected] 3 Adilabad ASIFABAD V.Laxmaiah MEO 9440992903 [email protected] 4 Adilabad ASIFABAD G.Santosh Kumar MIS Co-Ordinator 9866400525 [email protected] [email protected] 5 Adilabad Bazarhathnoor M.Prahlad MEO(FAC) 9440010906 n 6 Adilabad Bazarhathnoor C.Sharath MISCo-Ord 9640283334 7 Adilabad BEJJUR D.SOMIAH MEO FAC 9440036215 [email protected] MIS CO- 8 Adilabad BEJJUR CH.SUMALATHA 9440718097 [email protected] ORDINATOR 9 Adilabad Bellampally D.Sridhar Swamy M.E.O 7386461279 [email protected] 10 Adilabad Bellampally L.Srinivas MIS CO Ordinator 9441426311 [email protected] 11 Adilabad Bhainsa J.Dayanand MEO 7382621360 [email protected] 12 Adilabad Bhainsa Hari Prasad.Agolam MIS Co-ordinator 9703648880 [email protected] 13 Adilabad Bheemini K.Ganga Singh M.E.O 9440038948 [email protected] 14 Adilabad Bheemini P.Sridar M.I.S 9949294049 [email protected] 15 Adilabad Boath A.Bhumareedy M.E.O 9493340234 [email protected] 16 Adilabad Boath M.Prasad MIS CO Ordinator 7382305575 17 Adilabad CHENNUR C.MALLA REDDY MEO 7382621363 [email protected] MIS- 18 Adilabad CHENNUR CH.LAVANYA 9652666194 [email protected] COORDINATOR 19 Adilabad Dahegoan Venkata Swamy MEO 7382621364 [email protected] 20 -

Hand Book of Statistics 2018 Krishna District

HAND BOOK OF STATISTICS 2018 KRISHNA DISTRICT Compiled by CHIeF PlANNINg OFFICeR KRISHNA, MACHIlIPATNAM Sri B.LAKSHMIKANTHAM, I.A.S., Collector & District Magistrate Krishna District P R E F A C E I am glad that the Hand Book of Statistics 2018 of Krishna District with statistical dataof various departments for the year 2017-18 is being released. The statistical data in respect of various schemes being implemented by the departmentsin the district are compiled in a systematic manner so as to reflect the progress made under various sectors during the year. The sector wise progress is depicted in sector – wise tables apart from Mandal - wise data. I am confident that the publication will be of immense utility as a reference book to general public and Government and Non-Governmental agencies in general as well as Administrators, Planners, Research Scholars, Funding agencies, Banks and Non-Profit Institutions. I am thankful to all the District Officers and the Heads of Institutions for extendingtheirco-operation by furnishing the information to this Hand Book. I appreciate the efforts made by Sri T.Hima Prabhakar Raju, Chief Planning Officer (FAC), Krishna District and their Staff in collection and compilation of data in bringing out this publication. Any suggestions aimed at improvement of Hand Book are most welcome and maybe sent to the Chief Planning Officer, Krishna District at Machilipatnam Date: Station: Machilipatnam OFFICERS AND STAFF ASSOCIATED WITH THE PUBLICATION 1. SRI T.HIMA PRABHAKARA RAJU : CHIEF PLANNINg OFFICER 2. SRI M.SATYANARAYANA : STATISTICAL OFFICER 3. SRI M.ANAND KUMAR : DEPUTY STATISTICAL OFFICER, COMPILED AND COMPUTERIzED * * * DISTRICT PROFILE :: KRISHNA DISTRICT GENERAL AND PHYSICAL FEATURES Krishna District with its district head quarters at Machilipatnam is the coastal district of Andhra Pradesh. -

Krishna District Annual Report

Krishna District Annual Report 1st April 2018 to 31st March 2019 CONTENTS FOREWORD FROM THE DISTRICT PRESIDENT SRI SATHYA SAI SEVA ORGANISATIONS – AN INTRODUCTION WINGS OF THE ORGANISATIONS ADMINISTRATION OF THE ORGANISATION THE 9 POINT CODE OF CONDUCT AND 10 PRINCIPLES SRI SATHYA SAI SEVA ORGANISATIONS, [KRISHNA DISTRICT] BRIEF HISTORY DIVINE VISIT OVERVIEW SAI CENTRES ACTIVITIES OFFICE BEARERS SPECIFIC SERVICE PROJECTS OR INITIATIVES IMPORTANT EVENTS OR CONFERENCES GLIMPSES OF ACTIVITIES This report is dedicated at the Lotus Feet of our Lord and Master Bhagavan Sri Sathya Sai Baba Foreword from the District President SaiRam, I offer my heartfull salutations at the lotus fee of our beloved Sarvadevatateeta Swaroopa Bhagavan Sri Sari Sathya Sai Baba Varu. The elder and chosen devotees of Krishna District were very fortunate enough in having recognized Bala Baba as God Incarnated. Swamy blessed nearly seven or eight places and devotee’s residences in Krishna Distrct. Swamy, we on behalf of thousands of devotees of Krishna District offer our salutations to you for blessing all of us to be an active member’s of esteemed organisation named after you and blessed by you. Swamy how fortunate we are when you have created a lingam and named it as Premalingam and given to Vijayawada Samithi for daily abhishekam and declared whosoever taken the abhisheka jalam will get rid of any disease whatsoever. Swamy long back during darshan time you hve enlighted all of us to concentrate on the followup of any activity in any wing by asking “machines teesukunnavallandaru bagunnaraa”. After hearing this we have been taking continuous steps for follow up whether it is medical seva, DJP or any educational activity. -

Slno DISTRICT COD E DISTRICT NAME MANDAL CODE

Secretariat Master Report For KRISHNA DISTRICT_COD DISTRICT_ MANDAL SECRETAR slno MANDAL_NAME SECRETARIAT_NAME E NAME _CODE IAT_CODE 1 106 KRISHNA 1519 10690667 MADHAVARAM 2 106 KRISHNA 1519 10690665 KRISHNARAOPALEM 3 106 KRISHNA 1519 10690661 GOLLAMANDLA 4 106 KRISHNA 1519 10690659 A.KONDURUTHANDA 5 106 KRISHNA 1519 10690660 CHEEMALAPADU 6 106 KRISHNA 1519 10690668 POLLOSETTIPADI 7 106 KRISHNA 1519 10690662 KHAMBHAMPADU1 A.KONDURU 8 106 KRISHNA 1519 10690658 A.KONDURU 9 106 KRISHNA 1519 10690669 RAMCHANDRAPURAM 10 106 KRISHNA 1519 10690670 REPUDI 11 106 KRISHNA 1519 10690664 KODURU 12 106 KRISHNA 1519 10690666 KUMMARIKUNTLA 13 106 KRISHNA 1519 10690663 KHAMBHAMPADU2 14 106 KRISHNA 1519 10690671 VALLAMPATLA 15 106 KRISHNA 1509 10690457 ADAVINEKKALAM1 16 106 KRISHNA 1509 10690468 KOTHAEDARA 17 106 KRISHNA 1509 10690475 VATTIGUDIPADU 18 106 KRISHNA 1509 10690459 AGIRIPALLI1 19 106 KRISHNA 1509 10690463 CHOPPARMETLA 20 106 KRISHNA 1509 10690473 SURAVRAM 21 106 KRISHNA 1509 10690460 AGIRIPALLI2 22 106 KRISHNA 1509 10690474 VADLAMANU 23 106 KRISHNA 1509 10690467 KANASANAPALLI 24 106 KRISHNA 1509 AGIRIPALLI 10690462 CHINNAAGIRIPALLI 25 106 KRISHNA 1509 10690466 EDULAGUDEM 26 106 KRISHNA 1509 10690464 EDARA1 27 106 KRISHNA 1509 10690465 EDARA2 28 106 KRISHNA 1509 10690469 KRISHNAVARUM 29 106 KRISHNA 1509 10690472 S.A.PETA 30 106 KRISHNA 1509 10690458 ADAVINEKKALAM2 31 106 KRISHNA 1509 10690461 BODDANAPALLI 32 106 KRISHNA 1509 10690470 NARASINGAPALEM 33 106 KRISHNA 1509 10690471 NUGONDAPALLI 34 106 KRISHNA 1497 10690267 ASWARAPALEM 35 106 KRISHNA -

Pran Details of 0512-Nuzvid Empcode Name Ddocode

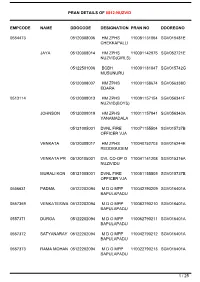

PRAN DETAILS OF 0512-NUZVID EMPCODE NAME DDOCODE DESIGNATION PRAN NO DDOREGNO 0554473 05120308006 HM ZPHS 110081131064 SGV015481E CHEKKAPALLI JAYA 05120308014 HM ZPHS 110001142975 SGV052721E NUZVID(GIRLS) 05122501006 BCBH 110001181047 SGV015742G MUSUNURU 05120308007 HM ZPHS 110001158674 SGV056338C EDARA 0513114 05120308013 HM ZPHS 110091157154 SGV056341F NUZVID(BOYS) JOHNSON 05120308019 HM ZPHS 110011157841 SGV056343A YANAMADALA 05121005001 DVNL FIRE 110071155504 SGV015737B OFFICER VJA VENKATA 05120308017 HM ZPHS 110040752703 SGV016244E REDDIGUDEM VENKATA PR 05120105001 DVL CO-OP O 110041141208 SGV015316A NUZIVIDU MURALI KON 05121005001 DVNL FIRE 110051155505 SGV015737B OFFICER VJA 0556631 PADMA 05122202094 M D O MPP 110042790209 SGV016401A BAPULAPADU 0557369 VENKATESWA 05122202094 M D O MPP 110082790210 SGV016401A BAPULAPADU 0557371 DURGA 05122202094 M D O MPP 110062790211 SGV016401A BAPULAPADU 0557372 SATYANARAY 05122202094 M D O MPP 110042790212 SGV016401A BAPULAPADU 0557373 RAMA MOHAN 05122202094 M D O MPP 110022790213 SGV016401A BAPULAPADU 1 / 25 0513124 05120308013 HM ZPHS 110071157155 SGV056341F NUZVID(BOYS) 0519893 GIRIJA 05120308013 HM ZPHS 110051157156 SGV056341F NUZVID(BOYS) 0558040 HARA DURGA 05122202094 M D O MPP 110002790214 SGV016401A BAPULAPADU SUNDARARAO 05120105001 DVL CO-OP O 110081141058 SGV015316A NUZIVIDU 0511234 SIVALEELA 05122202097 M E O 110061131972 SGV052718B AGIRIPALLI MUMTAZ 05122202097 M E O 110041131973 SGV052718B AGIRIPALLI KIRAN 05120105001 DVL CO-OP O 110061141059 SGV015316A NUZIVIDU RAVI 05120105001 -

List of Aadhaar Enrolment Centres in Krishna District

List of Aadhaar Enrolment Centres in Krishna District For latest information, please visit https://appointments.uidai.gov.in/easearch.aspx 1. Registrar : Information Technology & Communication Department Address : Patamata, Patamata, Krishna, Vijayawada (urban), Vijayawada (Urban), Andhra Pradesh - 520010 Permanent Last 30 days Enrolments : 23 Updates : 309 Last Update Date : 01/08/2019 2. Registrar : Information Technology & Communication Department Address : NVK MTM, Cattle Yard, Machilipatnam, Krishna, Machilipatnam, Machilipatnam, Andhra Pradesh - 521001 Permanent Last 30 days Enrolments : 0 Updates : 1 Last Update Date : 31/07/2019 3. Registrar : Information Technology & Communication Department Address : POORNODAYA ESEVA, 3-347 NEAR RAAVI CHETTU OLD SBI ROAD VUYYURU, Krishna, Vuyyuru, Vuyyuru, Andhra Pradesh - 521165 Permanent Last 30 days Enrolments : 69 Updates : 441 Last Update Date : 29/07/2019 4. Registrar : Information Technology & Communication Department Address : POORNODAYA ESEVA, VUYYURU, Krishna, Vuyyuru, Vuyyuru, Andhra Pradesh - 521165 Permanent Last 30 days Enrolments : 9 Updates : 58 Last Update Date : 02/08/2019 5. Registrar : Information Technology & Communication Department Address : Sri Sai Communications, L H Reddy Complex, Mylavaram, Krishna dt, Krishna, Mylavaram, Mylavaram, Andhra Pradesh - 521230 Permanent Last 30 days Enrolments : 162 Updates : 700 Last Update Date : 01/08/2019 6. Registrar : Information Technology & Communication Department Address : Sri Sai Communication, L H Reddy Complex, Mylavaram, Krishna dt, AP, Krishna, Mylavaram, Mylavaram, Andhra Pradesh - 521230 Permanent Last 30 days Enrolments : 16 Updates : 43 Last Update Date : 01/08/2019 7. Registrar : Information Technology & Communication Department Address : om prime computers, main road movva, Krishna, Movva, Movva, Andhra Pradesh - 521135 Permanent Last 30 days Enrolments : 0 Updates : 0 Last Update Date : 28/07/2019 8. -

Andhra Medi Pharma India Pvt. Ltd. Sy.No

ANDHRA MEDI PHARMA INDIA PVT. LTD. SY.NO. 263, VEERAVALLI VILLAGE, BAPULAPADU MANDAL, KRISHNA DISTRICT, ANDHRA PRADESH FORM I Project No. 0418‐21‐01 April 2018 STUDIES AND DOCUMENTATION BY Andhra Medi Pharma India Pvt. Ltd. TEAM Labs and Consultants Door No.40‐25‐35/1, Opposite Kesava Towers, B‐115‐117 & 509, Annapurna Block, Patamatalanka, Asramam street, Vijayawada, Aditya Enclave, Ameerpet, Andhra Pradesh – 520 010 Hyderabad‐500 038. Phone: +91 98664 72222 Phone: 040‐23748 555/23748616, E‐mail ID: [email protected] Telefax: 040‐23748666 SUBMITTED TO MINISTRY OF ENVIRONMENT, FORESTS AND CLIMATE CHANGE GOVERNMENT OF INDIA INDIRA PARYAVARAN BHAWAN, JOR BAGH ROAD, NEW DELHI APPENDIX – I (See Paragraph – 6) FORM I I) Basic Information S.No. Item Details 1 Name of the Project/s Andhra Medi Pharma India Private Limited 2 S. No in the Schedule 5 (f) ‐ A category (Synthetic Organic Chemicals) 3 Proposed capacity/area/length/tonnage to be Area Existing: 5 acres handled/command area/lease area/number Existing Capacity : 43.5 TPM of wells to be drilled S.No Name of Product Capacity (TPM) Phase I 1 Glucosamine Hydrochloride 30 2 Chondroitin Sulphate Sodium 3 Total Phase I 33 Phase II 1 Losartan Potassium 3 2 Pantoprazole Sodium 0.5 3 Topiramate 3 4 Rabeprazole Sodium 0.5 5 Valsartan 0.5 6 Levetiracetam 3 Total Phase II 10.5 Grand Total (Phase I + Phase II) 43.5 After Expansion: 186 TPM S.No Name of Product Capacity (TPM) Group ‐ A 1 Glucosamine Hydrochloride 186 Total Group ‐ A 186 Group ‐ B 1 Glucosamine Hydrochloride 30 2 Chondroitin Sulphate Sodium 3 3 Losartan Potassium 3 4 Pantoprazole Sodium 0.5 5 Topiramate 3 6 Rabeprazole Sodium 0.5 7 Valsartan 0.5 8 Levetiracetam 3 Total Group ‐ B 43.5 Note: Any one group will be manufactured at any point of time on campaign basis. -

Andhra Pradesh 28 Guntur 548 Phirangipuram 5072 113 Thalluru

State Name State District Name District Sub District Name Sub Village/Town Name Village/To Code Code District wn Code Code Andhra Pradesh 28 Guntur 548 Phirangipuram 5072 113 Thalluru 590214 Andhra Pradesh 28 Guntur 548 Pedakurapadu 5057 75-Tyallur 590010 Andhra Pradesh 28 Guntur 548 Vemuru 5087 Abbanagudavalli 590410 Andhra Pradesh 28 Guntur 548 Thullur 5053 Abbarajupalem 589963 Andhra Pradesh 28 Guntur 548 Sattenapalle 5058 Abburu 590029 Andhra Pradesh 28 Krishna 547 Pamarru 5028 Addada 589575 Andhra Pradesh 28 Guntur 548 Bhattiprolu 5089 Addepalli 590425 Andhra Pradesh 28 Krishna 547 Agiripalle 5005 Adivinekkalam 589117 Andhra Pradesh 28 Krishna 547 Nandigama 4993 Adiviravulapadu 588876 Andhra Pradesh 28 Guntur 548 Pedakakani 5075 Agatha Varappadu 590253 Andhra Pradesh 28 Krishna 547 Pamidimukkala 5026 Aginiparru 589547 Andhra Pradesh 28 Krishna 547 Agiripalle 5005 Agiripalle 589111 Andhra Pradesh 28 Krishna 547 Pamarru 5028 Ainampudi 589578 Andhra Pradesh 28 Guntur 548 Thullur 5053 Ainavolu 589968 Andhra Pradesh 28 Krishna 547 Gannavaram 5012 Ajjampudi 589249 Andhra Pradesh 28 Krishna 547 Vuyyuru 5027 Akunuru 589561 Andhra Pradesh 28 Guntur 548 Tsundur 5085 Alapadu 590385 Andhra Pradesh 28 Krishna 547 Gannavaram 5012 Allapuram 589247 Andhra Pradesh 28 Krishna 547 Gudivada 5021 Allidoddi 589463 Andhra Pradesh 28 Krishna 547 Veerullapadu 4994 Alluru 588909 Andhra Pradesh 28 Krishna 547 Vatsavai 4990 Allurupadu 588826 Andhra Pradesh 28 Guntur 548 Atchampet 5050 Ambadipudi 589919 Andhra Pradesh 28 Krishna 547 Vijayawada (Rural) 5011 Ambapuram