Food Retailing

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Retail Sector on Long Island Overlooked… Undervalued… Essential!

The Retail Sector on Long Island Overlooked… Undervalued… Essential! A Preliminary Report from the Long Island Business Council May 2021 Long Island “ L I ” The Sign of Success 2 | The Retail Sector on Long Island: Overlooked, Undervalued, Essential! Long Island Business Council Mission Statement The Long Island Business Council (LIBC) is a collaborative organization working to advocate for and assist the business community and related stakeholders. LIBC will create an open dialogue with key stakeholder groups and individuals to foster solutions to regional and local economic challenges. LIBC will serve as a community-focused enterprise that will work with strategic partners in government, business, education, nonprofit and civic sectors to foster a vibrant business climate, sustainable economic growth and an inclusive and shared prosperity that advances business attraction, creation, retention and expansion; and enhances: • Access to relevant markets (local, regional, national, global); • Access to a qualified workforce (credentialed workforce; responsive education & training); • Access to business/economic resources; • Access to and expansion of the regional supply chain; • A culture of innovation; • Commitment to best practices and ethical operations; • Adaptability, resiliency and diversity of regional markets to respond to emerging trends; • Navigability of the regulatory environment; • Availability of supportive infrastructure; • An attractive regional quality of life © 2021 LONG ISLAND BUSINESS COUNCIL (516) 794-2510 [email protected] -

Acme Markets - Have Reserved the Hours of 7 A.M

Acme Markets - have reserved the hours of 7 a.m. to 9 a.m. Monday through Friday at all stores for senior citizens and other at-risk customers. There are three Acme locations in the Trenton area: Hamilton Square (953 Route 33), Yardville (4400 S. Broad St.) and Bordentown (260 Dunns Mill Road). Aldi - stores across the country will be open from 9 a.m. to 7 p.m. daily. Some stores may have limited hours to accommodate restocking and cleaning. Aldi has five locations in the Trenton area: Bordentown (262C Route 130), East Windsor (440 US Highway 130), Ewing (1650 N. Olden Ave.), Hamilton (2735 S. Broad Street) and Hamilton Square (1250 Route 33). All BJ’s Wholesale Club - locations are opening one hour early for members who are age 60 and older. People ages 60 and up can use a designated entrance, from 8-9 a.m. daily. BJ’s members can shop in-club, on BJs.com or through the BJ’s mobile app, as well as through its same-day delivery service. BJ’s has one location in Mercer County: 900 Marketplace Blvd., Hamilton. Phone: (609) 581-4501. Costco - (4100 Quakerbridge Road, Lawrence) is limiting the number of shoppers in its warehouses, and has asked shoppers and employees to practice social distancing. A queue forms outside the warehouse doors to control the crowd inside it. Costco has increased our protocols in sanitizing surfaces, including shopping cart handles, merchandise shelves, front-end belts and registers. Limits have been implemented on certain items. Shoppers 60 and older gain early access to Costco warehouses Tuesdays and Thursdays from 8 to 9 a.m. -

Chapter 3: Socioeconomic Conditions

Chapter 3: Socioeconomic Conditions A. INTRODUCTION This chapter analyzes whether the proposed actions would result in changes in residential and economic activity that would constitute significant adverse socioeconomic impacts as defined by the City Environmental Quality Review (CEQR) Technical Manual.1 The proposed actions would result in the redevelopment of an underutilized site with an approximately 214,000- square-foot (sf), 60-foot-tall commercial building currently anticipated to be a BJ’s Wholesale Club along with up to three other retail stores on the second level, 690 parking spaces, and approximately 2.4 acres of publicly accessible waterfront open space. The Brooklyn Bay Center site (“project site”) is located at 1752 Shore Parkway between Shore Parkway South to the east, Gravesend Bay (Lower New York Bay) to the west, and between the prolongation of 24th Avenue to the north and the prolongation of Bay 37th Street to the south. The objective of the socioeconomic conditions analysis is to determine if the introduction of the retail uses planned under the proposed actions would directly or indirectly impact population, housing stock, or economic activities in the local study area or in the larger retail trade area. Pursuant to the CEQR Technical Manual, significant impacts could occur if an action meets one or more of the following tests: (1) if the action would lead to the direct displacement of residents such that the socioeconomic profile of the neighborhood would be substantially altered; (2) if the action would lead to the displacement of substantial numbers of businesses or employees, or would displace a business that plays a critical role in the community; (3) if the action would result in substantial new development that is markedly different from existing uses in a neighborhood; (4) if the action would affect real estate market conditions not only on the site anticipated to be developed, but in a larger study area; or (5) if the action would have a significant adverse effect on economic conditions in a specific industry. -

Dynamics in a Mature Industry: Entry, Exit, and Growth of Big-Box Grocery Retailers

WORKING PAPERS Dynamics in a Mature Industry: Entry, Exit, and Growth of Big-Box Retailers Daniel Hanner Daniel Hosken Luke M. Olson Loren K. Smith WORKING PAPER NO. 308 September 2011 FTC Bureau of Economics working papers are preliminary materials circulated to stimulate discussion and critical comment. The analyses and conclusions set forth are those of the authors and do not necessarily reflect the views of other members of the Bureau of Economics, other Commission staff, or the Commission itself. Upon request, single copies of the paper will be provided. References in publications to FTC Bureau of Economics working papers by FTC economists (other than acknowledgment by a writer that he has access to such unpublished materials) should be cleared with the author to protect the tentative character of these papers. BUREAU OF ECONOMICS FEDERAL TRADE COMMISSION WASHINGTON, DC 20580 Dynamics in a Mature Industry: Entry, Exit, and Growth of Big-Box Grocery Retailers Daniel Hanner Daniel Hosken Luke M. Olson Loren K. Smith1 U.S. Federal Trade Commission September 15, 2011 Abstract This paper measures market dynamics within the U.S. grocery industry (defined as supermarket, supercenter and club retailers). We find that the composition of outlets changes substantially, roughly 7%, each year, and that store sizes have increased as the result of growth by supercenter and club retailers. We find significant changes in the relative position of brands in markets over time. These changes are largely the result of expansion (or contraction) by incumbents rather than entry or exit. There is little entry or exit, except by small firms. -

Economic News & Trends

ECONOMIC NEWS & TRENDS March 3, 2017 ECONOMIC NEWS & TRENDS This nonconfidential edition includes excerpts from articles, studies, and economic research. The content focuses on trends and news during the third and fourth quarters of 2016. This report may be forwarded to others in your agency, the local chamber, and in your community. CONTENTS FIGURES HIGHLIGHTS. PAGE 2 FIGURE 1. GDP CHANGES OVER QUARTERS (2013–2016), PAGE 3 Section 1. U.S. ECONOMY, PAGE 3 FIGURE 2. UNEMPLOYMENT FOR 4Q2016, PAGE 5 Section 2. U.S. AUTO REPORT, PAGE 7 TABLES Section 3. TEXAS ECONOMY, PAGE 7 TABLE 1. PERCENT CHANGES IN CPI FOR ALL URBAN CONSUMERS 2016, PAGE 4 Section 4. RETAIL AND E-COMMERCE SALES AND TRENDS, PAGE 9 TABLE 2. U.S. HOUSING MARKET INDICATORS FOR 4Q2016, PAGE 5 Section 5. RESTAURANT NEWS AND SUPERMARKET TRENDS, PAGE 10 TABLE 3. ESTIMATED QUARTERLY REVENUE FOR SELECTED SERVICES FOR EMPLOYER FIRMS, NOT SEASONALLY ADJUSTED FROM 3Q2016 TO Section 6. SELECTED REGIONAL REPORT, PAGE 12 4Q2016, PAGE 6 CLIENT TEAM, PAGE 12 TABLE 4. TEXAS HOUSING MARKET INDICATORS FOR 4Q2016, PAGE 8 TABLE 5. U.S RESTAURANT EXPANSION 2016, PAGE 11 For more information about MuniServices, visit: www.MuniServices.com or contact us at [email protected]. ECONOMIC NEWS & TRENDS March 3, 2017 HIGHLIGHTS U.S. GDP: Real gross domestic product (GDP) increased at U.S. median home sales price: In 4Q2016, the median asking an annual rate of 1.9 percent in 4Q2016, according to the sales price for vacant-for-sale units was $167,700. New “advance” estimate released by the Bureau of Economic vehicles: U.S. -

Schedule 14A

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 SCHEDULE 14A Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934 (Amendment No. __) Filed by the Registrant o Filed by a Party other than the Registrant ☑ Check the appropriate box: o Preliminary Proxy Statement o Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) o Definitive Proxy Statement o Definitive Additional Materials ☑ Soliciting Material Pursuant to ss. 240.14a-12 Target Corporation (Name of Registrant as Specified In Its Charter) Pershing Square, L.P. Pershing Square II, L.P. Pershing Square International, Ltd. Pershing Square IV Trade-Co, L.P. Pershing Square IV-I Trade-Co, L.P. Pershing Square International IV Trade-Co, Ltd. Pershing Square International IV-I Trade-Co, Ltd. William A. Ackman Michael L. Ashner James L. Donald Ronald J. Gilson Richard W. Vague (Name of Person(s) Filing Proxy Statement, if other than the Registrant) Payment of Filing Fee (check the appropriate box): ☑ No fee required. o Fee computed on table below per Exchange Act Rule 14a-6(i)(4) and 0-11. (1) Title of each class of securities to which transaction applies: (2) Aggregate number of securities to which transaction applies: (3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): (4) Proposed maximum aggregate value of transaction: (5) Total fee paid: o Fee paid previously with preliminary materials. -

MERGER ANTITRUST LAW Albertsons/Safeway Case Study

MERGER ANTITRUST LAW Albertsons/Safeway Case Study Fall 2020 Georgetown University Law Center Professor Dale Collins ALBERTSONS/SAFEWAY CASE STUDY Table of Contents The deal Safeway Inc. and AB Albertsons LLC, Press Release, Safeway and Albertsons Announce Definitive Merger Agreement (Mar. 6, 2014) .............. 4 The FTC settlement Fed. Trade Comm’n, FTC Requires Albertsons and Safeway to Sell 168 Stores as a Condition of Merger (Jan. 27, 2015) .................................... 11 Complaint, In re Cerberus Institutional Partners V, L.P., No. C-4504 (F.T.C. filed Jan. 27, 2015) (challenging Albertsons/Safeway) .................... 13 Agreement Containing Consent Order (Jan. 27, 2015) ................................. 24 Decision and Order (Jan. 27, 2015) (redacted public version) ...................... 32 Order To Maintain Assets (Jan. 27, 2015) (redacted public version) ............ 49 Analysis of Agreement Containing Consent Orders To Aid Public Comment (Nov. 15, 2012) ........................................................... 56 The Washington state settlement Complaint, Washington v. Cerberus Institutional Partners V, L.P., No. 2:15-cv-00147 (W.D. Wash. filed Jan. 30, 2015) ................................... 69 Agreed Motion for Endorsement of Consent Decree (Jan. 30, 2015) ........... 81 [Proposed] Consent Decree (Jan. 30, 2015) ............................................ 84 Exhibit A. FTC Order to Maintain Assets (omitted) ............................. 100 Exhibit B. FTC Order and Decision (omitted) ..................................... -

Small-Cap Research

October 27, 2015 Small-Cap Research Steven Ralston, CFA 312-265-9426 [email protected] /.scr .zacks.com 10 S. Riverside Plaza, Chicago, IL 60606 MamaMancini s Holdings (MMMB-OTCQB) MMMB: Relationship with QVC continues to expand OUTLOOK MamaMancini s Holdings is a growth company in the specialty food industry. Management is aggressively pursuing strategies to build the MamaMancini s brand and to drive sales growth through 1) the Current Recommendation Buy addition of new retail locations, 2) increasing the Prior Recommendation N/A number of shelf placements at each location and 3) Date of Last Change 01/04/2014 new product introductions. The relationship with QVC continues to strengthen. New product offerings being developed by the recently hired Chef Christopher Current Price (10/26/15) $0.65 Styler are expected to be available soon that will $2.50 Six- Month Target Price broaden MamaMancini s presence on this ecommerce platform. We maintain our Buy rating. SUMMARY DATA 52-Week High $2.10 Risk Level Above Average 52-Week Low $0.51 Type of Stock Small-Growth One-Year Return (%) -59.04 Industry Food-Misc. Beta 1.05 Average Daily Volume (shrs.) 4,683 ZACKS ESTIMATES Shares Outstanding (million) 26.1 Market Capitalization ($ mil.) $17.0 Revenue (changed to January FY during 2014) (in millions of $) Short Interest Ratio (days) N/A Q1 Q2 Q3 Q4 Year Institutional Ownership (%) 0 Insider Ownership (%) 52 (Apr) (Jul) (Oct) (Jan) (Jan) 2014 1.77 A 1.70 A 2.17 A 3.10 A 8.74 A Annual Cash Dividend $0.00 2015 2.58 A 2.25 A 3. -

Market Analysis for Grocery Retail Space in Forest Grove, Oregon

MARKET ANALYSIS FOR GROCERY RETAIL SPACE IN FOREST GROVE, OREGON PREPARED FOR THE CITY OF FOREST GROVE, FEBRUARY 2018 TABLE OF CONTENTS I. INTRODUCTION ............................................................................................................................................. 2 II. EXECUTIVE SUMMARY .................................................................................................................................. 2 III. TRADE AREA DEFINITION .............................................................................................................................. 4 IV. GROCERY MARKET OVERVIEW ...................................................................................................................... 5 THE PORTLAND METRO MARKET .............................................................................................................................. 5 METRO LOCATION PATTERNS ................................................................................................................................... 8 FOREST GROVE-CORNELIUS ................................................................................................................................... 15 V. SOCIO-ECONOMIC CONDITIONS .................................................................................................................. 19 POPULATION & HOUSEHOLDS ................................................................................................................................ 19 EMPLOYMENT & COMMUTING .............................................................................................................................. -

Express Scripts Prescription Form

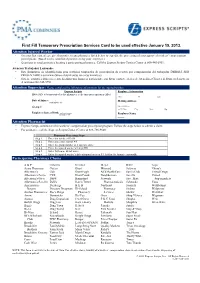

First Fill Temporary Prescription Services Card to be used effective January 15, 2013. Attention Injured Worker • On your first visit, please give this notice to any pharmacy listed below to expedite the processing of your approved workers’ compensation prescriptions. (Based on the established parameters by your employer.) • Questions or need assistance locating a participating pharmacy: Call the Express Scripts Contact Center at 800-945-5951. Atencion Trabajador Lesionado: • Este formulario de identificación para servicios temporales de prescripción de recetas por compensación del trabajador DEBERÁ SER PRESENTADO a su farmacéutico al surtir su(s) receta(s) inicial(es). • Si tiene cualquier duda o necesita localizar una farmacia participante, por favor contacte al área de Atención a Clientes de Express Scripts, en el teléfono 866-945-5951. Attention Supervisor: Please complete the following information for the injured worker. Express Scripts Employee Information ID #: SSN to be presented to the pharmacy at the time prescription is filled First M Last Date of Injury: / / Mailing Address MM/DD/CCYY Group #: Street Address or PO Box City State Zip Employee Date of Birth: / / Employer Name MM/DD/CCYY Attention Pharmacist • Express Scripts administers this workers’ compensation prescription program. Follow the steps below to submit a claim. • For assistance, call the Express Scripts Contact Center at 888-786-9640. Pharmacy Processing Steps Step 1 Enter bin number 003858 Step 2 Enter processor control A4 Step 3 Enter the group number as it -

Of Food Distribution Articles

Index of Food Distribution Articles This list of papers is presented in subject classi- Warehousing, Transportation and Physical fication form following the Super Market Institute infor- Distribution Management mation Service classifications for their monthly index The papers included are for proceedings issues of service. Food Distribution Research Conferences from 1962 and The following additions have been made to the SMI include all Food Distribution Journal Articles through classifications: 1972 including the October 1972 Proceedings Issue. Air Conditioning, Heating and Refrigeration Copies of all these issues are available through the Con sumeri sm and Providing Food for Poor Food Distribution Research Society, Inc. People A I ist of all of these publications is presented at Groups-Retail Cooperatives, Voluntaries, the end of the Index. Other Wholesalers, Franchises and Individual articles may be listed under more than Brokers one classification if the content is such as to concern Top Management and Research Management two or more classifications. SMI classification titles Training, Education and Getting Research for which no article appears were not included. Adapted Categories Used: Accounting and Controls Grocery Handling Advertising Groups - Retai I Cooperatives, Vo Iuntaries, Other Air Conditioning, Heating and Refrigeration Wholesalers, Franchises and Brokers Bakery Manufacturers and Manufacturer Supplier Relations Bantam, Convenience and Drive-In Markets Meat Brands Merchandising Buying, Ordering Procedures and Inventories Mergers Checkout Operations Nutriments Other Than Standard Foods Consumerism and Providing Food for Poor People Packaging Credit and Del ivery Personnel Administration Customer Behavior Patterns and Characteristics Prices and Price Spreads Custwnar Relations and Services Produce Dairy Products Public Relations Del icatessen Restaurants, Snack Bars, Etc. -

What Is the Marginal Effect of Entry? Evidence from A

What is the Marginal Effect of Entry? Evidence from a Natural Experiment in Liquor Licensure⇤ Gaston Illanes, Northwestern University† Sarah Moshary, University of Pennsylvania‡ August 26, 2017 Abstract We leverage a natural experiment in liquor licensure requirements to estimate the causal effect of entry on prices and sales volumes. When Washington state privatized liquor sales in 2012, it required retailer premises exceed 10,000ft2 in order to sell spirits. We exploit this discontinuity to overcome the endogeneity of entry to local demand conditions and firm unobservables. We find a 27 percentage point jump in entry at the licensure threshold and an 60% decline in entry for independent stores neighboring marginally-eligible potential entrants. While entry does not affect prices for individual products, we find it boosts liquor consumption, with an additional entrant increasing volume by 30% and product variety by 20%. However, these effects are limited to duopoly and triopoly markets, indicating the size-based entry restriction is a blunt instrument for reducing liquor externalities across the State. 1 Introduction This paper examines the competitive effects of firm entry by leveraging a natural experiment induced by Washington State’s 2012 deregulation of liquor sales. The interplay between entry and competition is central to policy-makers and correspondingly, has received considerable attention among Industrial Organization economists. A lengthy theoretical literature investigates how the number of competitors in a market affects ⇤This research was partially funded by the Center for the Study of Industrial Organization at Northwestern University, the George and Obie B. Schultz Dissertation Grant, and the Lynde and Harry Bradley Foundation.