Westfield Group Annual Report 2011

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Customer Visits Grow to 548 Million

ASX Announcement 18 February 2020 FULL YEAR FUNDS FROM OPERATIONS OF 25.42c PER SECURITY UP 3.2% (PRO FORMA BASIS); ANNUAL CUSTOMER VISITS GROW TO 548 MILLION Scentre Group (ASX: SCG) today released its results for the 12 months to 31 December 2019, with Funds From Operations (“FFO”) of $1.345 billion, in line with forecast. On a per security basis FFO was 25.42 cents, up 0.7% or 3.2% on a pro forma basis adjusting for the transactions1 completed during 2019. Distribution for the 12-month period was 22.60 cents per security, up 2.0% and in line with forecast. Operating Earnings – the Group’s FFO excluding Project Income – was $1.287 billion for the 12-month period, up 1.0% per security or 3.6% on a pro forma basis. Scentre Group CEO Peter Allen said: “We are creating the places more people choose to come, more often, for longer. “Our strategic focus on the customer and curation of our offer to continually meet their changing expectations and preferences has delivered these pleasing results. “Our 42 Westfield Living Centres are each strategically located in highly urbanised areas with strong population growth and density. “The strength of our portfolio combined with our leading operating platform has seen annual customer visits grow to more than 548 million. This is an increase of more than 12 million visits. “We have seen strong demand continue from our retail and brand partners with portfolio occupancy at 99.3%. During the year we introduced 344 new brands and 279 existing brands grew their store network with us. -

RGS-IBG and AGI Response to Mayor Draft Transport Strategy

Consultation Response Mayor of London draft Transport Strategy Mayor of London/ Greater London Authority Consultation Date: 29 September 2017 Introduction The Royal Geographical Society (with the Institute of British Geographers) is the UK's learned society and professional body for geography, founded in 1830. We are dedicated to the development and promotion of geographical knowledge, together with its application to the challenges facing society and the environment. The Association for Geographic Information (AGI) is the membership organisation for the UK geospatial industry. The AGI exists to promote the knowledge and use of Geographic Information for the betterment of governance, commerce and the citizen. The AGI represent the interests of the UK's Geographic Information industry; a wide-ranging group of public and private sector organisations, suppliers of geographic information/ geospatial software, hardware, data and services, consultants, academics and interested individuals. The RGS-IBG and the AGI are responding jointly to this consultation to further a shared vision and mission to ensure that geography and geographic information is recognised as an important enabler to the world of big data that surrounds us in the digital economy, and is used more widely across the public, private and third sectors. Our submission has been developed in consultation with the RGS Transport Geography, Economic Geography, Geographies of Health and Wellbeing, Planning and Environmental and Urban Geography Research Groups and with AGI London and the AGI Environmental, Asset Management and Land and Property Special Interest Groups. We welcome this opportunity to provide our views on the draft Transport Strategy. Key Message Geography is a key determinant of transport and transport networks, therefore using robust locational intelligence can enable smarter and more efficient transport networks, infrastructure and services to be delivered. -

21,134 Sq Ft

21,134 SQ FT RARE URBAN WAREHOUSE UNIT UNDERGOING FULL REFURBISHMENT UNIT 4 AVAILABLE TO OCCUPY JUNE 2021 IN PRIME LONDON LOCATION SEGRO.com/ParkCanningTown WELL-PLACED FOR ACCESS TO PORTS CITY OF LONDON CANARY WHARF Unit 4 at SEGRO Park Canning Town provides 21,134 sq ft (1,963 sq m) of A12/A102 rare urban warehouse space in one of London’s most premium and well- connected city logistics parks. A406 NORTH CIRCULAR RD Here’s why a variety of businesses have already set up shop and called SEGRO Park Canning Town home: UNIT 4 A13 An enviable location in the heart Within walking distance of three Zone A406 NORTH CIRCULAR RD and bustle of East London 2/3 tube stations, making it an ideal location for workers on the estate A key location for London centric M25 J30 customers, SEGRO Park Canning With convenient links to London Town’s proximity to Canary Wharf Gateway and Tilbury Port, SEGRO Park and beyond makes it ideal for serving Canning Town provides direct access CANNING TOWN STATION a London market to the city’s large shipping network. STAR LANE STATION CLOSE PROXIMITY TO THE CITY IN THE HEART OF EAST LONDON BOREHAMWOOD ENFIELD WATFORD BARNET Unit 4 is undergoing a complete M1 A1 STAPLEFORD M11 ABBOTTS 4 refurbishment which will enhance A10 M25 2 NORTHWOOD EDGWARE employee wellbeing, exceed sustainability WOODFORD F U LLY standards and introduce new tech REFURBISHED 4 HARROW A12 innovations and solutions to create 1 A1 ROMFORD 1 a more holistic working environment. WEMBLEY HOLLOWAY STRATFORD A40 DAGENHAM A10 BARKING HAYES GREENFORD A13 -

Travel Tips United Kingdom

Travel Tips United Kingdom City Guide London London is the largest city in the United Kingdom and a leader in global finance, fashion, commerce and education. It has a population of 8.17 million people and is located in south-eastern part of Great Britain and lies along the banks of the River Thames. London dates back 2 millennia to Roman times when it was a northern outpost of the Roman Empire. Airports London has two major international airports, and the city is easily reached from both of them. Heathrow (LHR) Heathrow located 15 miles west of London and there are a wide variety of transportation options to bring you to the city center. The Underground is the cheapest option with a one way ticket costing at most £6 (US$9.5). It takes close to an hour to reach most destinations within central London. The Heathrow Express train is the fastest option and will bring you to Paddington station in between 15 and 20 min. It costs £34 (US$53) for a return ticket. If your destination is not in the Paddington area, the Underground may end up taking less time overall. Various bus companies operate to and from London, and prices usually average about £12 (US$19) for a return ticket. There are several coaches that operate to outlying areas such as Oxford if London is not your final destination. There is a taxi queue in front of the arrivals gate, and private “Mini-Cabs” can be ordered ahead of time. It usually costs between £50-100 (US$75-$155). -

Seele Project Map London

projects in london Current and completed seele-projects, you may visit in and around London. Madame Toussauds 01 36 37 41 Royal Albert Hall 39 40 42 Victoria & Albert Museum 13 British Museum 12 Buckingham Palace 38 Houses of Parliament 11 27 31 34 16 07 08 02 21 46 23 14 Westminster Abbey 17 26 28 22 06 09 18 15 19 25 29 32 London Eye 03 20 24 St Paul's Cathedral 33 43 30 44 Imperial War Museum 05 Tower of London 35 45 04 10 projects in london Current and completed seele-projects, you may visit in and around London. 01 Hendon Quadrangle (university) 10 Wimbledon No. 1 Court (tennis stadium) 19 Unilever House (office building) 28 19 – 31 Moorgate (office building) 36 intu Watford (shopping centre) 45 Cutty Sark (museum) steel-and-glass roof, lift enclosure, post-and-beam construction, atrium, glass fibre construction, unitised façade made out of steel-and-glass gridshell roof steel-and-glass enclosure of the gallery and staircase balustrades balustrades, door systems glazed west façade, roofing stone, glass and aluminium www.watford-shopping.co.uk hull www.mdx.ac.uk www.wimbledon.com www.unilever.com reception open to the public Watford High Street (Train) www.rmg.co.uk/cutty-sark Hendon Central Wimbledon Park reception open to the public Moorgate / Bank 210 Queen St, Watford Cutty Sark The Burroughs Church Rd, Wimbledon City Thameslink 19 – 31 Moorgate King William Walk / Greenwich se-austria / 2005 se-austria / 2019 seele GmbH / 2007 100 Victoria Embankment se-austria / 2002 se-austria / 2018 se-austria / 2012 02 Westfield (shopping -

The Bay Area-Silicon Valley and Australia an Expanding Trans-Pacific Partnership

The Bay Area-Silicon Valley and Australia An Expanding Trans-Pacific Partnership December 2020 Acknowledgments This report was developed in partnership with the Odette Hampton, Trade and Investment Commissioner American Chamber of Commerce in Australia, with and Deputy Consul General, Australian Trade and support from Cisco, Google, Lendlease, Salesforce, Investment Commission (Austrade) Telstra, University of Technology Sydney, and Wipro. Joe Hockey, Founding Partner and President, Bondi Development of the project was led by Sean Randolph, Partners, Australian Ambassador to the US, 2016–2020 Senior Director at the Bay Area Council Economic Institute. Neils Erich, a consultant to the Institute, Vikas Jain, Asia-Pacific Business Head for Engineering, was co-author. The Institute wishes to thank April Construction and Mining, Wipro Palmerlee, Chief Executive Officer of the American Claire Johnston, Managing Director, Google Chamber of Commerce in Australia, for her support Development Ventures, Lendlease throughout this effort and the following individuals for Joe Kaesshaefer, Trade and Investment Commissioner– their valuable input: USA, Department of Industry, New South Wales Jeff Bleich, Chief Legal Officer, Cruise, US Ambassador Michael Kapel, Trade and Investment Commissioner to to Australia 2009–2013 the Americas in San Francisco, Government of Victoria Michael Blumenstein, Associate Dean, Research Damian Kassabgi, Executive Vice President, Public Strategy and Management, Faculty of Engineering Policy and Communications, Afterpay and -

Ngs Super Portfolio Holdings Disclosure

NGS SUPER PORTFOLIO HOLDINGS DISCLOSURE BALANCED - INCOME Effective date: 31 DEC 2020 AUSTRALIAN SHARES A2 MILK COMPANY LTD ABACUS PROPERTY GROUP AINSWORTH GAME TECHNOLOGY LIMITED ALTIUM ALUMINA LIMITED AMCOR PLC AMP LIMITED AMPOL LIMITED ANSELL LIMITED APA GROUP APPEN LTD ARB CORPORATION LIMITED ARISTOCRAT LEISURE LIMITED ASALEO CARE LTD ATLAS ARTERIA AUSNET SERVICES LIMITED AUSTRALIA AND NEW ZEALAND BANKING GROUP LIMITED AUSTRALIAN VINTAGE LTD BELLEVUE GOLD LIMITED BHP GROUP LTD BRAMBLES LIMITED BWP TRUST CAPRAL LIMITED CASH CHALLENGER LIMITED CHARTER HALL GROUP CHARTER HALL RETAIL REIT CHORUS LIMITED Issued by NGS Super Pty Limited ABN 46 003 491 487 AFSL No 233 154 the trustee of NGS Super ABN 73 549 180 515 ngssuper.com.au 1300 133 177 NGS SUPER – PORTFOLIO HOLDINGS DISCLOSURE 1 BALANCED - INCOME Effective date: 31 DEC 2020 CLEANAWAY WASTE MANAGEMENT LTD COCA-COLA AMATIL LIMITED COLES GROUP LTD COMMONWEALTH BANK OF AUSTRALIA CONTACT ENERGY LIMITED CROWN RESORTS LIMITED CSL LIMITED CSR LIMITED DERIVATIVES DOMINO'S PIZZA ENTERPRISES LIMITED ELDERS LIMITED EVENT HOSPITALITY & ENTERTAINMENT LTD EVOLUTION MINING LIMITED FAR LTD FISHER & PAYKEL HEALTHCARE CORPORATION LIMITED FLETCHER BUILDING LIMITED FLIGHT CENTRE TRAVEL GROUP LIMITED G.U.D. HOLDINGS LIMITED G8 EDUCATION LIMITED GOODMAN GROUP HARVEY NORMAN HOLDINGS LTD HEALIUS LIMITED HOME CONSORTIUM HT&E LTD IGO LIMITED IMPEDIMED LIMITED INCITEC PIVOT LIMITED INGHAMS GROUP LTD INSURANCE AUSTRALIA GROUP LIMITED IPH LTD JAMES HARDIE INDUSTRIES PLC JB HI-FI LIMITED KATHMANDU HOLDINGS LIMITED -

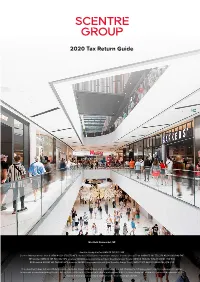

2020 Tax Return Guide

2020 Tax Return Guide Westfield Newmarket, NZ — Scentre Group Limited ABN 66 001 671 496 Scentre Management Limited ABN 41 001 670 579 AFS Licence 230329 as responsible entity of Scentre Group Trust 1 ABN 55 191 750 378 ARSN 090 849 746 RE1 Limited ABN 80 145 743 862 AFS Licence 380202 as responsible entity of Scentre Group Trust 2 ABN 66 744 282 872 ARSN 146 934 536 RE2 Limited ABN 41 145 744 065 AFS Licence 380203 as responsible entity of Scentre Group Trust 3 ABN 11 517 229 138 ARSN 146 934 652 This document does not constitute financial product or investment advice, and, in particular, it is not intended to influence you in making a decision in relation to financial products including Scentre Group Stapled Securities. You should obtain professional advice before taking any action in relation to this document, for example from your accountant, taxation or other professional adviser. About this Guide This 2020 Tax Return Guide (“Guide”) has been prepared to assist Australian resident individual securityholders to complete their 2020 Australian income tax return. This Guide provides general information Section 1 Important Information for only. Accordingly, this Guide should not be relied upon as taxation Australian Resident Individual advice. Each securityholder’s particular circumstances are different and we recommend you contact your accountant, taxation or other Securityholders Completing professional adviser for specific advice. a 2020 Tax Return This Tax Return Guide has two sections: General information - Scentre Group Scentre Group is a stapled group that comprises the following four Section 1 Provides information to assist entities: Australian resident individual - Scentre Group Limited (“SGL”) securityholders complete - Scentre Group Trust 1 (“SGT1”) their 2020 Australian income - Scentre Group Trust 2 (“SGT2”) tax return. -

Savills.Co.Uk/Retail Shaping Retail

Central London Retail savills.co.uk/retail Shaping Retail. Contents The Team 3 The Savills Approach 4 London 6 Crossrail 7 Track Record: Oxford Street 8 Track Record: Bond Street 10 Track Record: Old Spitalfields Market 12 Case Study: Nike Women’s Store 13 Track Record: APM Monaco 14 Case Study: Itsu 15 Bond Street 17 Dover Street and Albemarle Street 19 Mount Street and South Audley Street 21 South Molton Street 23 Conduit Street and Bruton Street 25 Regent Street 27 Oxford Street East 29 Oxford Street West 31 Marylebone High Street 33 Covent Garden: Neal Street 35 Covent Garden: Long Acre 37 Covent Garden: Seven Dials 39 Soho 41 King’s Road 43 Kensington High Street 45 Knightsbridge 47 Sloane Street and Sloane Square 49 South Kensington 51 Westbourne Grove 53 Spitalfields 55 Westfield Stratford 57 Westfield London 59 One Stop Shop 60 The Team Agency Lease Consultancy Anthony Selwyn Laura Salisbury-Jones Alan Spencer [email protected] [email protected] [email protected] +44 (0) 20 7758 3880 +44 (0) 20 7409 8830 +44 (0) 20 7758 3876 Peter Thomas Tiffany Luckett Paul Endicott [email protected] [email protected] [email protected] +44 (0) 20 7734 3443 +44 (0) 20 7758 3878 +44 (0) 20 7758 3879 Sam Foyle Benjamin Ashe Kristian Kendall [email protected] [email protected] [email protected] +44 (0) 20 7409 8171 +44 (0) 20 7758 3889 +44 (0) 20 7758 3881 Sarah Goldman James Fairley Daniel Aboud [email protected] [email protected] [email protected] +44 (0) 20 7758 3875 +44 (0) 20 7758 3877 +44 (0) 20 7758 3895 Oliver Green Claire Lakie [email protected] [email protected] +44 (0) 20 7758 3899 +44 (0) 20 7758 3896 Lance Marton Research [email protected] +44 (0) 20 7758 3884 Marie Hickey [email protected] +44 (0) 20 3320 8288 For general enquiries: [email protected] 3 The Savills Approach Savills Central London Retail team is recognised as a market leader within the sector and we have extensive experience in Central London, leasing and asset management and Landlord & Tenant matters. -

2014 PRINT NAREIT Annual Report Layout 1

REITWay NAREIT’s Annual Report 2013 In Review & 2014 A Look Ahead National Association of Real Estate Investment Trusts® REITs: Building Dividends & Diversification® 2014 REITWay NAREIT’s Annual Report 2 To Our Members The past year was active for NAREIT as we Stock Exchange-Listed took the REIT story to all of our industry’s REIT Capital Offerings, 2013 audiences. This 2014 issue of REITWay: IPOs NAREIT’S Annual Report re-caps some of what Secured and we accomplished on the REIT industry’s behalf Unsecured Debt $5.71 billion during the year. $30.74 billion Policy & Politics Secondary Total: In the Policy and Politics area, we began the Equity year with a highly effective Washington $40.51 billion $76.96 billion Leadership Forum. Our industry’s leaders climbed Capitol Hill to provide legislators and their staffs with a better understanding of the REIT investment proposition, including its history, the REITs in today’s mortgage finance marketplace, to the impact of important functions REITs play in investment portfolios, their rising interest rates on REIT total returns. We also continued to channeling of capital to the real estate industry, and their role upgrade and expand our REIT.com online platform and our other creating jobs and economic growth. digital properties. Over the course of the year, our Policy & Politics team provided Additionally, we conducted a full schedule of successful constructive input to the ongoing discussion on tax reform, conference events for our members, including our major including input to the House Ways and Means Committee and investor conferences, REITWeek and REITWorld. -

Presentation of the Group PDF 603KB

2 Universal Registration Document 2020 / UNIBAIL-RODAMCO-WESTFIELD Presentation of the Group Presentation of the Group 1.1 KEY FACTS 3 1.2 HISTORY 4 1.3 STRATEGY AND BUSINESS MODEL 6 1.4 BUSINESS OVERVIEW 12 Business segments 12 Portfolio breakdown 13 Development pipeline 15 CHAPTER 1.5 PORTFOLIO 16 1.5.1 France: Shopping Centres 16 1.5.2 France: Convention & Exhibition 18 1.5.3 France: Offices 19 1.5.4 Central Europe: Shopping Centres 20 1.5.5 Central Europe: Offices 21 1.5.6 Spain: Shopping Centres 21 1.5.7 Spain: Offices 21 1.5.8 Nordics: Shopping Centres 22 1.5.9 Nordics: Offices 22 1.5.10 Austria: Shopping Centres 23 1.5.11 Austria: Offices 23 1.5.12 Germany: Shopping Centres 24 1.5.13 Germany: Offices 24 1.5.14 The Netherlands: Shopping Centres 25 1.5.15 The Netherlands: Offices 25 1.5.16 United States: Shopping Centres 26 1.5.17 United States: Offices 28 1.5.18 United Kingdom: Shopping Centres 29 1.5.19 United Kingdom: Offices 29 1.6 OVERVIEW OF VALUATION REPORTS PREPARED BY UNIBAIL-RODAMCO-WESTFIELD’S INDEPENDENT EXTERNAL APPRAISERS FOR EUROPEAN ASSETS 30 1.7 OVERVIEW OF VALUATION REPORTS PREPARED BY UNIBAIL-RODAMCO-WESTFIELD’S INDEPENDENT EXTERNAL APPRAISERS FOR AMERICAN ASSETS 32 1.8 STRUCTURE 34 1.9 SIMPLIFIED GROUP ORGANISATIONAL CHART 35 Universal Registration Document 2020 / UNIBAIL-RODAMCO-WESTFIELD 3 Presentation of the Group Key facts 1.1 KEY FACTS 1. 87 16 OFFICES & OTHERS SHOPPING CENTRES BUILDINGS(1) 10 80% CONVENTION & EXHIBITION COLLECTION RATE(3) VENUES(2) 247 ~3,100 COVID-19 ESG INITIATIVES EMPLOYEES €1,790 Mn €7.28 ADJUSTED RECURRING NET RENTAL INCOME EARNINGS PER SHARE €2.3 Bn €56.3 Bn DISPOSALS(4) GROSS MARKET VALUE €166.8 €4.4 Bn EPRA NET REINSTATEMENT PIPELINE VALUE PER SHARE (1) Only standalone offices > 10,000 sqm and offices affixed to a shopping centre > 15,000 sqm, including La Vaguada offices. -

2019 Insurance Fact Book

2019 Insurance Fact Book TO THE READER Imagine a world without insurance. Some might say, “So what?” or “Yes to that!” when reading the sentence above. And that’s understandable, given that often the best experience one can have with insurance is not to receive the benefits of the product at all, after a disaster or other loss. And others—who already have some understanding or even appreciation for insurance—might say it provides protection against financial aspects of a premature death, injury, loss of property, loss of earning power, legal liability or other unexpected expenses. All that is true. We are the financial first responders. But there is so much more. Insurance drives economic growth. It provides stability against risks. It encourages resilience. Recent disasters have demonstrated the vital role the industry plays in recovery—and that without insurance, the impact on individuals, businesses and communities can be devastating. As insurers, we know that even with all that we protect now, the coverage gap is still too big. We want to close that gap. That desire is reflected in changes to this year’s Insurance Information Institute (I.I.I.)Insurance Fact Book. We have added new information on coastal storm surge risk and hail as well as reinsurance and the growing problem of marijuana and impaired driving. We have updated the section on litigiousness to include tort costs and compensation by state, and assignment of benefits litigation, a growing problem in Florida. As always, the book provides valuable information on: • World and U.S. catastrophes • Property/casualty and life/health insurance results and investments • Personal expenditures on auto and homeowners insurance • Major types of insurance losses, including vehicle accidents, homeowners claims, crime and workplace accidents • State auto insurance laws The I.I.I.