Overview of the Spanish Gas Market in Year 2005

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Cyberbullying Analysis in Intercultural Educational Environments Using Binary Logistic Regressions

future internet Article Cyberbullying Analysis in Intercultural Educational Environments Using Binary Logistic Regressions José Manuel Ortiz-Marcos 1 , María Tomé-Fernández 2,* and Christian Fernández-Leyva 1 1 Department of Research Methods and Diagnosis in Education, Faculty of Education Sciences, University of Granada, 18071 Granada, Spain; [email protected] (J.M.O.-M.); [email protected] (C.F.-L.) 2 Department of Research Methods and Diagnosis in Education, Faculty of Education and Sports Sciences, University of Granada, 52071 Melilla, Spain * Correspondence: [email protected] Abstract: The goal of this study is to analyze how religion, ethnic group, and race influence the likelihood of becoming either a cybervictim or cyberbully in intercultural educational environments. In the research, 755 students in secondary education were analyzed in the south of Spain through the Cyberbullying Scale for students with Cultural and Religious Diversity (CSCRD). The analyses were carried out using the Statistical Package SPSS and the STATA software. The results obtained from the Kruskal–Wallis H test showed significant differences according to these aspects, for both the cybervictim and cyberbully parameters. The results stemming from binary logistic regressions confirmed such differences and regarded those students who belong to the Muslim religion, the gypsy ethnic group and the Asian race as being more likely to become cybervictims. Furthermore, these analyses showed that Gypsy and Asian students were also more likely to be cyberbullies than other groups. The main conclusions state that minority groups are more likely to suffer cyberbullying in intercultural educational environments, and that students from these groups are also more likely to become cyberbullies. -

Autonomous Community of Andalucia (PDF 210K)

LIST OF ATTORNEYS AUTONOMOUS COMMUNITY OF ANDALUCIA While every effort has been made to include only the names of persons with favorable reputations, the Embassy of the United States of America in Madrid assumes no responsibility for the professional ability or integrity of persons or firms whose names appear in the following list. Complaints should initially be addressed to the COLEGIO DE ABOGADOS (Bar Association) in the city involved. If you wish, you may also send a copy of the complaint to the Embassy. The names are arranged alphabetically within cities. The order in which they appear has no other significance. The Embassy reserves the right to add, restrict or amend this list as necessary. PROVINCE OF CADIZ LEGAL CONNECT - www.legalconnect.es Point of Contact: Carolina Leon Address: Avda. de Andalucia, 8, 4ºC, 11008 Cádiz E-Mail: [email protected] Phone: +34 674 227 907 Practice Areas: Civil Law: Corporate, Family and Immigration; Contract Law; Business Law and International Law, Investment Law. Languages: Spanish and English CASADO RUIZ, JAIME - www.jaimecasado.com Point of Contact: Jaime Casado Address: C/ Francia, s/n, Edificio Europa, 4ª-1, 11011 Cádiz Also offices in Seville and Huelva E-Mail: [email protected] Phone: +34 954 281 614 Practice Areas: Commercial, Civil, Labor, Maritime, Real Estate, Family, Probate Languages: English, Spanish, French, and German CITY OF JEREZ KONSELL ABOGADOS Y ASESORES, S.L. - www.konsell.es Point of Contact: Jose Manuel Diaz Montes Address: Calle Porvera, 6-8, 1ª A, 11403 Jerez de la Frontera, Cádiz E-Mail: [email protected] Phone: +34 956 33 00 83 / +34 638 765 528 Practice Areas: - Contracts drafting and negotiation both in Civil & Commercial Law - International and Local Taxation. -

Archaeological Finds in the Deepest Anthropogenic Stratum at 3 Concepción Street in the City of Huelva, Spain*

doi: 10.2143/AWE.16.0.3214933 AWE 16 (2017) 1-61 ARCHAEOLOGICAL FINDS IN THE DEEPEST ANTHROPOGENIC STRATUM AT 3 CONCEPCIÓN STREET IN THE CITY OF HUELVA, SPAIN* F. G ONZÁLEZ DE CANALES, L. SERRANO PICHARDO (†), J. LLOMPART GÓMEZ, M. GARCÍA FERNÁNDEZ, J. RAMON TORRES, A.J. DOMÍNGUEZ MONEDERO AND A. MONTAÑO JUSTO** Abstract Finds from the occupation layer under the water table at 3 Concepción St, in the historic centre of the city of Huelva, Spain, confirm the early development of an important Phoeni- cian emporion, already revealed by pottery and craft and industrial activities in the nearby plot at 7–13 Méndez Núñez St/12 Las Monjas Sq. As well as vessels of Phoenician and local tradition, some Greek Geometric and a significant Sardinian representation have been docu- mented. Whereas the oldest Phoenician pottery in Méndez Núñez St/Las Monjas Sq. was broadly dated to ca. 900 BC, the characteristics of a Tyre jug type 9 (in Bikai’s classification) from 3 Concepción St point more strongly to the 10th century BC. Against the background of the finds in the deepest anthropogenic sub-phreatic stratum at 7–13 Méndez Núñez St/12 Las Monjas Sq. (hereinafter MN/PM) in the historic centre of Huelva,1 we are now presenting the new corresponding finds, just 43 m away, at 3 Concepción St (hereinafter C3) (Fig. 1). The archaeological inter- vention took place in two phases between May 2009 and September 2010. SOME GEOLOGICAL AND STRATIGRAPHIC CONSIDERATIONS The old Huelva habitat spread out from a higher elevation, configured by a cluster of hillocks (cabezos), towards a lower brackish marsh on the estuary of the Tinto and Odiel rivers. -

The Impact of Phoenician and Greek Expansion on the Early Iron Age

Ok%lkVlht a, ol a- Pk- c-i--t-S- 'L. ST COPY AVAILA L Variable print quality 3C7 BIBLIOGRAPHY Abbreviations used AJA American Journal of Archaeology AEArq Archivo Espanol de Arqueologia BASOR Bulletin of the American School of Oriental Rese arch Bonner Jb Bonner JahrbUcher BRGK Bericht der R8misch-Germanischen Kommission BSA Annual of the British School at Athens CAH Cambridge Ancient History CNA Congreso Nacional de Arqueologia II Madrid 1951 x Mahon 1967 x]: Merida 1968 XII -Jaen 1971 XIII Huelva 1973 Exc. Arq. en Espana Excavaciones Arqueolo'gicas en Espana FbS Fundberichte aus Schwaben Jb RGZM Jahrbucfi des Rbmisch-Germaniscfien Zentraimuseums Mainz JCS Journal of Cuneiform Studies JHS Journal of Hellenic Studies JNES Journal of Near Eastern Studies MDOG Mitteilungen der Deutschen Orient-Gesellschaft MH Madrider Mitteilungen NAH Noticario Arqueologico Hispanico PBSR Papers of the British School at Rome PEQ Palestine Exploration Quarterly PPS Proceedings of the Prehistoric Society SCE Swedish Cyprus Expedition SUP Symposium Internacional de Prehistoria Peninsular, V Jerez de la Frontera 1968: Tartessos y sus Problemas, Publicaciones Eventuales 13 SPP Symposium de Prehistoria Peninsular VI Palma de Mallorca 1972 Trab. de Preh. Trabajos de Prehistoria 8L \ t 4. ADCOCK FE 1926 The reform of the Athenian State; CAH IV, 'Ch. II, IV and'V, 36-45 ALBRIGHT WF 1941 New light on the early history of Phoenician colonisation, BASOR 83, (Oct. ) 14-22 1942 ArchaeologX and*the Religion of Israel, Baltimore 1958 Was the age of Solomon without monumental art? Eretz-Israel V, lff 1961 The role of the Canaanites in the history of civilization in WRIGHT GE ed. -

Calendario Migraciones

Calendario campañas agrícolas nacionales 2019 ENERO FEBRERO MARZO CAMPAÑA PROVINCIA CAMPAÑA PROVINCIA CAMPAÑA PROVINCIA Aceituna Córdoba, Jaén, Cítricos Córdoba, Sevilla, Tarragona, Cítricos Tarragona, Alicante, produc.aceite Granada, Badajoz, Alicante, Castellón, Valencia, Castellón, Huelva, Málaga, Toledo, Ciudad Real Murcia, Sevilla, Málaga Valencia, Murcia P.Subtropicales Granada, Málaga Fresa y Berrys Huelva Hortofrutícola Almería, Valencia, Fresa y Berrys Huelva Alicante, Murcia Hortofrutícola Almería, Alicante, Murcia, Hortofrutícola Almería, Alicante, Valencia Plátano Las Palmas, Tenerife Murcia Tomate Las Palmas, Tenerife Tomate Las Palmas, Tenerife Fresa y Berrys Huelva ABRIL MAYO JUNIO CAMPAÑA PROVINCIA CAMPAÑA PROVINCIA CAMPAÑA PROVINCIA Cítricos Córdoba, Sevilla, Cereza Cáceres, Aragón Ajo Córdoba, Albacete, Tarragona, Alicante, Cuenca, Ciudad Real Huelva, Castellón, Ajo Albacete, Cuenca, Ciudad Real Valencia Cereza Cáceres Fruta dulce Lleida, Badajoz, Sevilla, Aragón, Fresa y Berrys Huelva Murcia Fruta Dulce Lleida, Badajoz, Sevilla, Aragón, Murcia Fresa y Berrys Huelva Hortofrutícola Almería, Alicante, Fresa y Berrys Huelva Hortofrutícola Almería, Barcelona Murcia, Valencia Melón y Sandía Castilla La Mancha Hortofrutícola Almería Plátano Las Palmas, Tenerife Calendario campañas agrícolas nacionales 2019 JULIO AGOSTO SEPTIEMBRE CAMPAÑA PROVINCIA CAMPAÑA PROVINCIA CAMPAÑA PROVINCIA Fresa plantación Ávila Ajo Albacete, Ciudad Real, Fruta dulce Aragón, Lleida Cuenca Fruta dulce Aragón, Lleida, Alicante Vendimia Barcelona, Tarragona -

Presentación De Powerpoint

Best Practice Policy Guidelines for Small Scale LNG; Truck Loading Group of Experts on Gas Luis. I Parada 22nd April 2016 - Geneva Program Focus UNECE 1. New Uses of LNG, including small scale: . Bringing gas to remote areas (remote gas services) . Use of LNG as a transport fuel. 2. Regulatory needs: . Implement regulation to facilitate the use of natural gas and LNG. Norms and standards for LNG 3. Advantages of gas and LNG in mitigating climate change. 2 Advantanges of Natural Gas UNECE 1. Environmental benefits of natural gas • Reducing emissions (CO2, NOx, SOx) • Reduce local pollution, air quality for citizens • Considered by EU as alternative fuel 2. Truckloading Services I. Distribution market – Remote areas not being connected to gas grid for both industrial and domestic usage; II. Transport sector – Parties considering using LNG III. Power generation & Industrial customers- small power plants used for peak shaving where these are still supplied with fuel oil or industrial customers who may consider this a more feasible option. 3 Truck Loading in the UN ECE UNECE Truck loading Development from import terminals in the UNECE Region Truck Loading Development in the UN ECE region Regasification Terminals in the US Regasification Terminals in the US Canaport Everett Golden PassCameron LNG Freeport LNG Cove Point Canaport Elba Island Everett Golden PassCameron LNG Freeport LNG Gulf LNGCove Point Lake Charles Sabine Pass Elba Island Gulf LNG Lake Charles Regasification Terminals Sabine Pass Regasification Terminalsin Europe inGrain EuropeLNG -

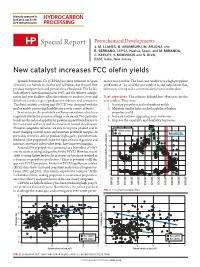

New Catalyst Increases FCC Olefin Yields

Originally appeared in: April 2014, pgs 63-66. Used with permission. Petrochemical Developments Special Report J. M. LLANES, B. ARAMBURU, M. ARJONA and E. SERRANO, CEPSA, Huelva, Spain; and M. MIRANDA, C. KEELEY, V. KOMVOKIS and S. RIVA, BASF, Iselin, New Jersey New catalyst increases FCC olefin yields Spanish Petroleum Co. (CEPSA) has three refineries in Spain mance was possible. The base case catalyst was a high propylene (Tenerife, La Rábida in Huelva and Gibraltar–San Roque) that yield catalyst.3 To see if the new catalyst would outperform this, produce transport fuels and petrochemical feedstock. The La Rá- laboratory testing and a commercial trial were undertaken. bida refinery started operations in 1967, and the refinery configu- ration and port facilities allow the refinery to produce, store and Trial objectives. The refinery defined four objectives for the distribute a wide range of products for industry and consumers. new catalyst. They were: The fluid catalytic cracking unit (FCCU) was designed with the 1. Increase propylene and isobutylene yields goal to enable processing flexibility for a wide variety of feeds.a 2. Maintain similar light cracked naphtha at higher In recent years, the profitability of European refineries has been propylene yield negatively affected by a number of large-scale trends. Two particular 3. Increase bottoms upgrading and conversion trends are the reduced appetite for gasoline imports from Europe to 4. Improve the capability and flexibility to process the East Coast of the US and the movement toward dieselization. 100 However, adaptable refineries are able to improve product mix to 90 Furfural extracts meet changing societal needs and maintain profitable margins. -

FACTSHEET 2021/2022 INSTITUTIONAL DETAILS Name of University University of Huelva

FACTSHEET 2021/2022 INSTITUTIONAL DETAILS Name of University University of Huelva Erasmus Code E HUELVA 01 Web Address http://www.uhu.es/english/ International Office International Office. Pavilion 13, Juan Agustín de Mora. Campus El Carmen, Huelva. Postal Address Avenida. Fuerzas Armadas, s/n Campus El Carmen. 21007. Huelva, Spain. Email [email protected] | [email protected] Telephone (+34) 959 21 82 37 | (+34) 959 21 94 94 Facebook Address International Students - University of Huelva - Spain WHO WE ARE Contact Person Function Contact Data Mª Teresa Aceytuno Director of the [email protected] Pérez International Office Juan José Gómez Boullosa Incoming [email protected] Exchange/Erasmus+ Coordinator Claire Martin Responsible for Inter- [email protected] institutional Agreements Mariluz Capelo Álvarez CEIMAR Incoming [email protected] Students Campus El Carmen Tel.: (+34) 959 21 94 94 [email protected] Avda. 3 de marzo, s/n 21007 - Huelva Fax: (+34) 959 21 93 59 www.uhu.es/english/ Raquel Pérez Cuadrado Internships [email protected] CALENDAR Fall 2021 Spring 2022 (September-February) (February-June) Nomination Deadline June 15th, 2021 November 15th, 2021 Application Deadline July 1st, 2021 November 30th, 2021 Welcome Week * September 27th – October February 7th - 11th, 2022 1st , 2021 Summer School June 28th – July 16th Spanish intensive August 30th – September language course * 24th 2021 Beginning of Classes * October 1st , 2021 February 15th, 2022 End of Exams * February 12th, 2022 June 30th, 2022 *Dates to be confirmed. For further information, please check: General Calendar http://www.uhu.es/estudios/calendario/calendario.htm NOMINATION / APPLICATION PROCEDURES Complete Application For further information, please check the following link: Instructions http://www.uhu.es/english/ Nomination/Application 1. -

Municipal and Autonomous Community Elections of 22 May 2011

31 March 2011 Municipal and Autonomous Community elections of 22 May 2011 35,381,270 voters will be able to vote in the elections of 22 May The electoral census will be available for query from 4 to 11 April Next 22 May 2011, a total of 34,567,304 voters will be able to vote in the municipal elections. 19,328,936 voters will be able to participate in the Autonomous Community elections that will be held in 13 Autonomous Communities, and 114,584 in the elections to the Assemblies of the autonomous cities of Ceuta and Melilla. Elections Residents in Spain Residents abroad Foreign Spaniards nationals Municipal 34,093,730 473,574 -- Autonomous Community 18,629,554 -- 699,382 Assemblies of Ceuta and Melilla 108,695 174 5,715 According to article 2.3 of the Electoral Law, in order to be able to vote in the municipal elections, it is necessary to be registered in the electoral census of residents in Spain. Electoral census querying The electoral census will be available for query from 4 to 11 April, at the municipal councils, and also in the provincial delegations of the Electoral Census Office. Spanish voters residing abroad may verify their registration data on these same dates at their respective consulates. Queries at the municipal councils may be made through electronic means, after the interested party identifies him or herself, or alternatively, through the posted voting lists, if said electronic means are not available. The claims period, if any error or omission is observed regarding the data contained in the electoral census, will elapse from 4 to 11 April. -

As Andalusia

THE SPANISH OF ANDALUSIA Perhaps no other dialect zone of Spain has received as much attention--from scholars and in the popular press--as Andalusia. The pronunciation of Andalusian Spanish is so unmistakable as to constitute the most widely-employed dialect stereotype in literature and popular culture. Historical linguists debate the reasons for the drastic differences between Andalusian and Castilian varieties, variously attributing the dialect differentiation to Arab/Mozarab influence, repopulation from northwestern Spain, and linguistic drift. Nearly all theories of the formation of Latin American Spanish stress the heavy Andalusian contribution, most noticeable in the phonetics of Caribbean and coastal (northwestern) South American dialects, but found in more attenuated fashion throughout the Americas. The distinctive Andalusian subculture, at once joyful and mournful, but always proud of its heritage, has done much to promote the notion of andalucismo within Spain. The most extreme position is that andaluz is a regional Ibero- Romance language, similar to Leonese, Aragonese, Galician, or Catalan. Objectively, there is little to recommend this stance, since for all intents and purposes Andalusian is a phonetic accent superimposed on a pan-Castilian grammatical base, with only the expected amount of regional lexical differences. There is not a single grammatical feature (e.g. verb cojugation, use of preposition, syntactic pattern) which separates Andalusian from Castilian. At the vernacular level, Andalusian Spanish contains most of the features of castellano vulgar. The full reality of Andalusian Spanish is, inevitably, much greater than the sum of its parts, and regardless of the indisputable genealogical ties between andaluz and castellano, Andalusian speech deserves study as one of the most striking forms of Peninsular Spanish expression. -

FACTSHEET 2021/2022 INSTITUTIONAL DETAILS Name of University University of Huelva

FACTSHEET 2021/2022 INSTITUTIONAL DETAILS Name of University University of Huelva Erasmus Code E HUELVA 01 Web Address http://www.uhu.es/english/ International Office International Office. Pavilion 13, Juan Agustín de Mora. Campus El Carmen, Huelva. Postal Address Avenida. Fuerzas Armadas, s/n Campus El Carmen. 21007. Huelva, Spain. Email [email protected] | [email protected] Telephone (+34) 959 21 82 37 | (+34) 959 21 94 94 Facebook Address International Students - University of Huelva - Spain WHO WE ARE Contact Person Function Contact Data Mª Teresa Aceytuno Director of the [email protected] Pérez International Office Juan José Gómez Boullosa Incoming [email protected] Exchange/Erasmus+ Coordinator Claire Martin Responsible for Inter- [email protected] institutional Agreements Mariluz Capelo Álvarez CEIMAR Incoming [email protected] Students Campus El Carmen Tel.: (+34) 959 21 94 94 [email protected] Avda. 3 de marzo, s/n 21007 - Huelva Fax: (+34) 959 21 93 59 www.uhu.es/english/ Raquel Pérez Cuadrado Internships [email protected] CALENDAR Fall 2021 Spring 2022 (September-February) (February-June) Nomination Deadline June 15th, 2021 November 15th, 2021 Application Deadline July 1st, 2021 November 30th, 2021 Welcome Week September 20th – 24th, February 7th - 11th, 2022 2021 Summer School June 28th – July 16th Spanish intensive August 30th – September language course 24th 2021 Beginning of Classes September 27th, 2021 February 14th, 2022 End of Exams February 11th, 2022 July 1st, 2022 For further information, please check: General Calendar http://www.uhu.es/estudios/calendario/calendario.htm NOMINATION / APPLICATION PROCEDURES Complete Application For further information, please check the following link: Instructions http://www.uhu.es/english/ Nomination/Application 1. -

Huelva Is Situated Between the Airports of Faro in Portugal and Seville

Getting to Huelva Huelva is situated between the airports of Faro in Portugal and Seville. The distance is about the same but there are more frequent connections from Seville. If you travel to Faro, you can take the bus to Huelva from Faro central bus station. There are two buses daily. The times below are local times: Depart Faro 8:20 Arrival Huelva 11:45 Depart Faro 15:30 Arrival Huelva 19:00 Depart Huelva 08:45 Arrival Faro 10:10 Depart Huelva 17:30 Arrival Faro 18:55 Faro-Huelva: http://www.damas-sa.es/index.php/rutas-y-horarios/ Faro Airport to Faro Bus Station: http://www.algarve-tourist.com/Faro/Faro- airport-to-Faro.html If you fly to Seville, there are buses every hour from Seville (Plaza de Armas Bus station) to Huelva and the journey takes about an hour and 15 minutes. To get to the Plaza de Armas Bus Station, you can take the airport bus to the city center If you prefer train you can take it at Santa Justa Train Station reachable through the airport bus to the city center. There are three daily trains to Huelva at 10.00, 17.00 and 20.50 and three trains back to Seville at 6.55, 15.00 and 19.00. The journey takes about an hour and a half. Airport bus to city center: https://www.sevilla-airport.com/en/getting_there.php). Bus Seville-Huelva: http://www.damas-sa.es/index.php/rutas-y-horarios/ Train Seville-Huelva: http://www.renfe.com/viajeros/index.html If you fly to Madrid, there are two direct trains to Huelva departing from Atocha Station at 16.20 and 18.05 (back to Madrid at 8.00).