Pdf, (Accessed at 10.05.2014)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Orta Gediz Havzasında (Salihli-Turgutlu) Tarımsal Amaçlı Bölgelendirme Yöntemi İle Organik Tarım Alanlarının Belirlenmesi , Ü

Orta Gediz Havzasında (Salihli-Turgutlu) Tarımsal Amaçlı Bölgelendirme Yöntemi İle Organik Tarım Alanlarının Belirlenmesi , Ü. Erdal1, Ö. Sökmen2, M.Kirami Ölgen3 2Uluslararası Tarımsal Araştırma ve Eğitim Merkezi Menemen İzmir 1Ege Üniversitesi, Coğrafya Bölümü, 35100 Bornova İzmir ÖZET Bu çalışmada CBS yardımıyla Orta Gediz Havzası’nda yer şekilleri, toprak, iklim ve verimlilik kriterlerine bağlı olarak bitki yetiştiriciliği açısından tarımsal amaçlı ekolojik bölgelerin (zonların) ve organik yetiştiriciliğe uygun olan tarımsal alanların belirlenmesi amaçlanmıştır. Bu amaç için farklı veri setlerinden oluşan bir veritabanı tasarlanmıştır. Tasarlanan veritabanı toprak, topografya, bitki örtüsü, iklim ve toprak örneklerinin kimyasal, fiziksel ve verimlilik analiz sonuçları katmanlarından oluşturulmuştur. Ardından her bir katmanın değerlendirilmesinde ağırlıklı puan analizi kullanılmıştır. Öncelikli olarak bitki yetiştiriciliği açısından önemli olan özellikler saptanmış ve her birine önem derecesine göre etki katsayıları verilmiştir. Sonuç olarak her bir ağırlıklı değer toplanarak sınıflandırılmış ve agroekolojik bölgelerin haritası oluşturularak her zona uygun bitki çeşitleri belirlenmiştir. Orta Gediz Havzasında yaklaşık 17 000 ha alanda organik ve konvansiyonel tarım yapılan alanların organik madde miktarlarına ait haritalar oluşturulmuştur. Anahtar Sözcükler: Agroekolojik bölge (zon), CBS, organik tarım, bitki, organik madde 1. GİRİŞ Ekolojik bölgelendirme ister tarımsal amaçlı olsun, isterse başka bir amaç ( arazi toplulaştırması, -

Balıkesir Orman Bölge Müdürlüğü

BALIKESİR ORMAN BÖLGE MÜDÜRLÜĞÜ BALIKESİR İLİ DAHİLİNDEKİ ORMAN İŞLETME MÜDÜRLÜKLERİNDEKİ ORMAN YANGINLARI İLE MÜCADELLE HİZMETLERİNDE İSTİHTAM EDİLECEK GECİÇİ İŞCİLERE YAPILAN SÖZLÜ MÜLAKAT SINAVI DEĞERLENDİRME SINAV SONUÇ TUTANAĞI İŞLETME/FİDANLIK BÖLGE MÜDÜRLÜĞÜ POZİSYON ADI SOYADI ALDIĞI NOT DURUMU MÜDÜRLÜĞÜ BALIKESİR SINDIRGI BEDEN İŞÇİSİ MEHMET ŞENSÖZ 96 ASİL1 BALIKESİR SINDIRGI BEDEN İŞÇİSİ ADEM ORDU 92 ASİL2 BALIKESİR SINDIRGI BEDEN İŞÇİSİ SAMET YILMAZ 90 ASİL3 BALIKESİR SINDIRGI BEDEN İŞÇİSİ İLKER KUŞÇU 86 YEDEK1 BALIKESİR SINDIRGI BEDEN İŞÇİSİ HASAN ÇAKIR 80 YEDEK2 BALIKESİR SINDIRGI BEDEN İŞÇİSİ İSA ÇAKIR 76 YEDEK3 BALIKESİR FİDANLIK(DURSUNBEY) BEDEN İŞÇİSİ MEHMET GÜRLEN 90 ASİL1 BALIKESİR FİDANLIK(DURSUNBEY) BEDEN İŞÇİSİ MUSTAFA SEYHAN 80 YEDEK1 BALIKESİR FİDANLIK(SINDIRGI) BEDEN İŞÇİSİ MUSTAFA SERHAT GEZER 90 ASİL1 BALIKESİR FİDANLIK(SINDIRGI) BEDEN İŞÇİSİ YÜCEL ERMİŞ 80 YEDEK1 BALIKESİR BİGADİÇ BEDEN İŞÇİSİ İSA KUZU 100 ASİL1 BALIKESİR BİGADİÇ BEDEN İŞÇİSİ MAHMUT DEMİR 98 ASİL2 BALIKESİR BİGADİÇ BEDEN İŞÇİSİ HALİL İBRAHİM KANDEMİR 92 ASİL3 BALIKESİR BİGADİÇ BEDEN İŞÇİSİ GÖKHAN KARADAĞ 90 ASİL4 BALIKESİR BİGADİÇ BEDEN İŞÇİSİ ERAY ARIK 88 ASİL5 BALIKESİR BİGADİÇ BEDEN İŞÇİSİ SEDAT KARAHAN 86 YEDEK1 BALIKESİR BİGADİÇ BEDEN İŞÇİSİ İHSAN YETGİN 82 YEDEK2 BALIKESİR BİGADİÇ BEDEN İŞÇİSİ HASAN KEF 80 YEDEK3 BALIKESİR BİGADİÇ BEDEN İŞÇİSİ MEHMET AKAN 76 YEDEK4 BALIKESİR BİGADİÇ BEDEN İŞÇİSİ CENGİZ KABAKOĞLU 74 YEDEK5 BALIKESİR FİDANLIK(BALIKESİR) BEDEN İŞÇİSİ RAMAZAN TİPİ 100 ASİL1 BALIKESİR FİDANLIK(BALIKESİR) BEDEN İŞÇİSİ CİHAN -

Balıkesir Büyükşehir Belediye Tarihçesi 25 B

BALIKESİR BÜYÜKŞEHİR BELEDİYESİ FAALYET RAPORU balkesrbld Hususi İdareler ve Belediyeler, büyük kalkınma savaşımızda başarı hasılasını artıracak vazifeler almalı ve hususiyle hayat ucuzluğunu temin edecek, yerine göre tedbirler bulmalı ve salahiyetlerini tam kullanmalıdır. 1 Kasım 1937, Meclis Açılış Konuşmasından Ancak geleceği düşünebilen milletler, yaşamak ve ilerlemek imkanına kavuşurlar. Mustafa Kemal ATATÜRK Yerel yönetimler, demokrasinin temel oluşumu ve taşlarıdır. Demokratik belediyecilik anlayışı yanında, bir şehre ait olmanın bilincini geliştirmemiz, şehri bütün unsurlarıyla yaşayan canlı bir organizma gibi görmemiz gerekir. Yaşayan canlı bir organizma olarak şehrin sahiplerini, yani şehir halkını yönetim ve karar sürecinin en önemli unsuru olarak görmediğimiz müddetçe, demokratik bir belediyeciliği hayata geçirmemiz mümkün değildir. Recep Tayyip ERDOĞAN Türkiye Cumhuriyeti Cumhurbaşkanı Sevgili Balıkesirliler, Büyükşehir Belediye Başkanlığı görevine sizlerin takdir ve teveccühleriyle seçilmemizin üzerinden iki yıl geçti. Şehrimiz için aynı masa etrafında bir araya gelerek geleceği planladığımız, birlikte düşündüğümüz, birlikte çalıştığımız, güzel işlere imza attığımız iki yıl. Günlük hayatın içerisinde vatandaşlarımızın ihtiyaçlarını kesintisiz olarak giderebildiği, tüm eksiklikleri giderilmiş, her bir ilçesinin kendine has değerleriyle dünyaca kabul gördüğü, yaşamaktan gurur duyulan bir şehri inşa etme hedefiyle gece gündüz çalıştık, çalışmaya da devam ediyoruz. Yola çıkarken söz verdik, verdiğimiz sözleri birer birer yerine -

The Hellenistic Pottery and Small Finds of Kordon Tumulus at Kordon Köyü/Salihli (Manisa) 2001*

Baran Aydın The Hellenistic Pottery and Small Finds of Kordon Tumulus at Kordon Köyü/Salihli (Manisa) 2001* Introduction This paper aims to publish hellenistic finds from a tumulus grave in the territory of Sardis aided by publica- tions after 20011. Since little datable contexts are known for hellenistic pottery from Sardis2 it is helpful to present some useful contexts. Furthermore it is also intended to present new finds of known and unknown workshops as well as a unique wooden pyxis. Kordon Tumulus3 (fig. 1) is located 18 km east of Sardis and 1 km south of Kordon Köyü4. Its GPS coordinates are N 38° 26’ 50.5’’, E 28° 15’ 52.2’’ and in UTM System E610345 N4256211 (UTM zone 35) elv. 268 m. Since C. Foss5 draws the borders of Roman Sardis 15 km west till to Aureliopolis, 20 km north- east as far as Adala, 30 km east as far as Philadephia, it seems plausible to consider these Kordon finds as ›Sardian‹. It is worth mentioning that the Hellenistic pottery of Sardis has a close relationship to the pottery of Pergamum6. At the end of the field research it became clear that the tomb was built in the beginning of the 5th century BC by the Lydians and was re-used in the 2nd century BC as a family grave. The tomb’s form can be placed between ›Group P‹ and ›Group R‹ according to R. Dinç’s classification for Lydian tumuli7. * For abbreviations additional to those published in <http://www.oeai.at/publik/autoren.html> see the end of this contribution. -

Ad Soyad Hizmet Puanı Eski Görev İlçesi Görev Yeri Branşı Atandığı

BALIKESİR İL MİLLÎ EĞİTİM MÜDÜRLÜĞÜ ÖĞRETMENLERİN 2021 YILI İL İÇİ İSTEĞE BAĞLI YER DEĞİŞTİRME SONUÇ LİSTESİ (Yer Değiştirme Sonuç Listesi bilgilendirme amaçlıdır. Gerekli kontroller yapıldıktan ve Valilik Oluru alındıktan sonra sonuçlar kesinlik kazanacaktır.) Hizmet Eski Görev Ad Soyad Görev Yeri Branşı Atandığı İlçe Atandığı Kurum Sıra No Puanı İlçesi 1 ASLI KOÇ 121 SAVAŞTEPE Necip Fazıl Kısakürek Anadolu Lisesi Almanca ALTIEYLÜL Balıkesir Cumhuriyet Anadolu Lisesi 2 TUĞBA GÜLER 87 ERDEK Erdek Anadolu Lisesi Almanca BANDIRMA Kemal Pireci Anadolu Lisesi 3 SEMRA YÜCEL 462 MARMARA Marmara Çok Programlı Anadolu Lisesi Beden Eğitimi MARMARA Marmara Halk Eğitimi Merkezi Burhaniye Ticaret Odası Özel Eğitim Uygulama Okulu 4 MURAT AKTEPE 416 BURHANİYE Beden Eğitimi BURHANİYE Burhaniye Atatürk Mesleki ve Teknik Anadolu Lisesi III. Kademe 5 MEHMET TUNCAY DEMİRCAN 267 BANDIRMA Edincik Recep Gencer Mesleki ve Teknik Anadolu Lisesi Beden Eğitimi BANDIRMA Fatih Ortaokulu 6 RAMAZAN YAZGAN 267 İVRİNDİ Şehit Turan Kurt Ortaokulu Beden Eğitimi DURSUNBEY Akbaşlar Ortaokulu 7 GÜLŞAH ERTAN 241 BANDIRMA Bandırma Atatürk Özel Eğitim Ortaokulu Beden Eğitimi BANDIRMA Aksakal Umut Akkaya Ortaokulu 8 SEMİH ÖZKARAL 185 SINDIRGI Yüreğil Ortaokulu Beden Eğitimi İVRİNDİ Soğanbükü Müdafa-i Hukuk Ortaokulu 9 AHMET BİRGÜN 121 MARMARA Avşa Ortaokulu Beden Eğitimi ERDEK Karşıyaka Çok Programlı Anadolu Lisesi 10 BÜŞRA İLDAN 87 EDREMİT Yolören Esin Akpınar Ortaokulu Beden Eğitimi İVRİNDİ KAYAPA ORTAOKULU 11 AYKUT ÖZKAN 82 SINDIRGI Gölcük Ortaokulu Beden Eğitimi SINDIRGI Sındırgı Makbule Efe Anadolu Lisesi 12 SİNAN ÖNAL 177 GÖNEN Buğdaylı Ortaokulu Bilişim Teknolojileri BURHANİYE Şehit Mustafa Serin Ortaokulu 13 NURETTİN YORULMAZ 138 SINDIRGI Sındırgı Mesleki ve Teknik Anadolu Lisesi Bilişim Teknolojileri SINDIRGI Cumhuriyet Ortaokulu 14 EYLÜL ESİNBAY 113 SAVAŞTEPE Necip Fazıl Kısakürek Anadolu Lisesi Bilişim Teknolojileri SUSURLUK Susurluk Anadolu Lisesi 15 HAKAN ERDEMLİ 397 MANYAS Manyas Anadolu Lisesi Biyoloji BANDIRMA Bandırma Anadolu Lisesi 16 İBRAHİM COŞKUN 395 ALTIEYLÜL 100. -

Logistic Atlas

BALIKESİR Logistic Atlas Balıkesir is the New Favorite for Investments with Developing Transportation Network On the junction of East-West and North-South connection roads, Balıkesir is a candidate for being the logistics center of Turkey. Recent highways and ongoing highway investments, projected railroad and port projects are making Balıkesir the door of Turkey to the world. These projects will make Balıkesir a bridge between metropoles and other provinces, as well as contributing to inter-province commercial activities. Marmara YALOVA Erdek Bandırma BİLECİK Gönen Manyas BURSA ÇANAKKALE Susurluk Balya Karesi Kepsut Edremit Havran Altıeylül İvrindi Dursunbey Bigadiç Savaştepe Gömeç Burhaniye KÜTAHYA Ayvalık Sındırgı MANİSA İZMİR UŞAK 2 Balıkesir on the Road to Become a Logistics Base Geographic location of Balıkesir and its close proximity to centers such as İstanbul, Bursa, İzmir increases the growth potential of the province. Being an alternative region in industry sector moves Balıkesir rapidly into becoming a logistics base. İSTANBUL TEKİRDAĞ 132 km ÇANAKKALE 190 km 90 km 115 km Bandırma 240 km 165 km 110 km 200 km BURSA 100 km 150 km BALIKESİR 140 km MANİSA 40 km İZMİR 3 Connection Roads to Neighboring Provinces Social, economic and logistic relations between provinces have been improved by increasing the length of the total divided roads connecting Balıkesir to neighboring provinces. Divided road construction works on the 220 km-highway connecting Balıkesir to Çanakkale has been completed and the road has been commissioned. Transportation infrastructure of 225 km Kütahya – Balıkesir divided road has been improved. Furthermore, transportation to Bursa, İzmir and Manisa provinces that are neighboring Balıkesir is provided with divided roads. -

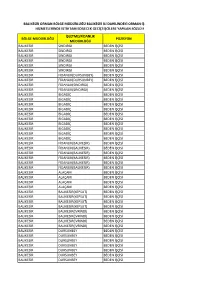

Balikesir Orman Bölge Müdürlüğü Balikesir Ili Dahilindeki Orman Iş Hizmetlerinde Istihtam Edilecek Geciçi Işcilere Yapilan Sözlü M

BALIKESİR ORMAN BÖLGE MÜDÜRLÜĞÜ BALIKESİR İLİ DAHİLİNDEKİ ORMAN İŞ HİZMETLERİNDE İSTİHTAM EDİLECEK GECİÇİ İŞCİLERE YAPILAN SÖZLÜ M İŞLETME/FİDANLIK BÖLGE MÜDÜRLÜĞÜ POZİSYON MÜDÜRLÜĞÜ BALIKESİR SINDIRGI BEDEN İŞÇİSİ BALIKESİR SINDIRGI BEDEN İŞÇİSİ BALIKESİR SINDIRGI BEDEN İŞÇİSİ BALIKESİR SINDIRGI BEDEN İŞÇİSİ BALIKESİR SINDIRGI BEDEN İŞÇİSİ BALIKESİR SINDIRGI BEDEN İŞÇİSİ BALIKESİRFİDANLIK(DURSUNBEY) BEDEN İŞÇİSİ BALIKESİRFİDANLIK(DURSUNBEY) BEDEN İŞÇİSİ BALIKESİRFİDANLIK(SINDIRGI) BEDEN İŞÇİSİ BALIKESİRFİDANLIK(SINDIRGI) BEDEN İŞÇİSİ BALIKESİRBİGADİÇ BEDEN İŞÇİSİ BALIKESİRBİGADİÇ BEDEN İŞÇİSİ BALIKESİRBİGADİÇ BEDEN İŞÇİSİ BALIKESİRBİGADİÇ BEDEN İŞÇİSİ BALIKESİRBİGADİÇ BEDEN İŞÇİSİ BALIKESİRBİGADİÇ BEDEN İŞÇİSİ BALIKESİRBİGADİÇ BEDEN İŞÇİSİ BALIKESİRBİGADİÇ BEDEN İŞÇİSİ BALIKESİRBİGADİÇ BEDEN İŞÇİSİ BALIKESİRBİGADİÇ BEDEN İŞÇİSİ BALIKESİRFİDANLIK(BALIKESİR) BEDEN İŞÇİSİ BALIKESİRFİDANLIK(BALIKESİR) BEDEN İŞÇİSİ BALIKESİRFİDANLIK(BALIKESİR) BEDEN İŞÇİSİ BALIKESİRFİDANLIK(BALIKESİR) BEDEN İŞÇİSİ BALIKESİRFİDANLIK(BALIKESİR) BEDEN İŞÇİSİ BALIKESİRFİDANLIK(BALIKESİR) BEDEN İŞÇİSİ BALIKESİR ALAÇAM BEDEN İŞÇİSİ BALIKESİR ALAÇAM BEDEN İŞÇİSİ BALIKESİR ALAÇAM BEDEN İŞÇİSİ BALIKESİR ALAÇAM BEDEN İŞÇİSİ BALIKESİR BALIKESİR(KEPSUT) BEDEN İŞÇİSİ BALIKESİR BALIKESİR(KEPSUT) BEDEN İŞÇİSİ BALIKESİR BALIKESİR(KEPSUT) BEDEN İŞÇİSİ BALIKESİR BALIKESİR(KEPSUT) BEDEN İŞÇİSİ BALIKESİR BALIKESİR(İVRİNDİ) BEDEN İŞÇİSİ BALIKESİR BALIKESİR(İVRİNDİ) BEDEN İŞÇİSİ BALIKESİR BALIKESİR(İVRİNDİ) BEDEN İŞÇİSİ BALIKESİR BALIKESİR(İVRİNDİ) BEDEN İŞÇİSİ BALIKESİR DURSUNBEY -

Balıkesir Logistic Atlas

www.gmka.gov.tr Balıkesir is the New Favorite for Investments with Developing Transportation Network On the junction of East-West and North-South connection roads, Balıkesir is a candidate for being the logistics center of Turkey. Recent highways and ongoing highway investments, projected railroad and port projects are making Balıkesir the door of Turkey to the world. These projects will make Balıkesir a bridge between metropoles and other provinces, as well as contributing to inter-province commercial activities. Marmara YALOVA Erdek Bandırma BİLECİK Gönen Manyas BURSA ÇANAKKALE Susurluk Balya Karesi Kepsut Edremit Havran Altıeylül İvrindi Dursunbey Bigadiç Savaştepe Gömeç Burhaniye KÜTAHYA Ayvalık Sındırgı MANİSA İZMİR UŞAK 2 Balıkesir on the Road to Become a Logistics Base Geographic location of Balıkesir and its close proximity to centers such as İstanbul, Bursa, İzmir increases the growth potential of the province. Being an alternative region in industry sector moves Balıkesir rapidly into becoming a logistics base. İSTANBUL TEKİRDAĞ 132 km ÇANAKKALE 190 km 90 km 115 km Bandırma 240 km 165 km 110 km 200 km BURSA 100 km 150 km BALIKESİR 140 km MANİSA 40 km İZMİR 3 Connection Roads to Neighboring Provinces Social, economic and logistics relations between provinces have been improved by increasing the length of the total divided roads connecting Balıkesir to neighboring provinces. Divided road construction works on the 220 km-highway connecting Balıkesir to Çanakkale has been completed and the road has been commissioned. Transportation infrastructure of 225 km Kütahya – Balıkesir divided road has been improved. Furthermore, transportation to Bursa, İzmir and Manisa provinces that are neighboring Balıkesir is provided with divided roads. -

Turkey Raisin Annual Turkey Raisin Annual 2010

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: 8/19/2010 Turkey Raisin Annual Turkey Raisin Annual 2010 Approved By: Rachel Nelson Prepared By: Samet Serttas Report Highlights: Post revised the MY 2009 raisin production estimate to 260,000 MT, and MY 2010 production is forecasted at 240,000 MT. Production dropped in MY 2010 due to cold weather and frost in March. The harvest has just started in some regions and is expected to finish in September. Executive Summary: Turkish raisin production reached a record 310,000 MT in MY 2008 and decreased to 260,000 MT in MY 2009. In the early forecast of MY 2009 production was forecasted at 280,000 but due to late rainfall in September, production was just 260,000 MT. MY 2010 production is forecasted at 240,000 MT. MY 2008 exports reached 285,000 MT and MY 2009 exports reached 192,000 MT as of July. MY 2009 total exports are estimated at 220,000 MT. A forecast for low production levels in MY 2010 will decrease MY 2010 exports to 205,000 MT. The demand for grapes by the wine industry is expected to increase in MY 2010. This demand will slightly decrease raisin production in MY 2010. Commodities: Grapes, Table, Fresh Raisins Production: Grapes are grown throughout Turkey. Seedless grapes, virtually all of which are „Vitis viniserae L , constitute about 40 percent of Turkey‟s total grape crop and are grown only in Aegean part of Turkey. -

Balikesir Ili 2018 Yili Çevre Durum Raporu

TÜRKİYE CUMHURİYETİ BALIKESİR VALİLİĞİ ÇEVRE VE ŞEHİRCİLİK İL MÜDÜRLÜĞÜ BALIKESİR İLİ 2018 YILI ÇEVRE DURUM RAPORU HAZIRLAYAN: BALIKESİR ÇEVRE VE ŞEHİRCİLİK İL MÜDÜRLÜĞÜ BALIKESİR Mayıs 2019 (REVİZE) i BALIKESİR 2018 ÇEVRE DURUM RAPORU ÖNSÖZ Tüm canlılar yeryüzüne geldiği andan itibaren önce çevresini tanır zamanla çevre ile etkileşime geçer. İnsanoğlu yüzyıllar boyunca doğayı sınırsız bir kaynak olarak görmüş, onu hor kullanmış, kirletmiş ve çevre sorunlarının ortaya çıkmasına neden olmuştur. Bir tarafta hızla artan nüfus olgusu diğer tarafta ise tükenmekte olan doğal kaynakların varlığı insanlık için yeni çözüm arayışlarını zorunlu kılmıştır. Bu çerçevede ortaya koyulan çözüm, doğal kaynakların tamamen tüketilmeden, gelecek nesillere de aktarılmasının sağlanması olarak özetlenebilecek olan sürdürülebilir kalkınma anlayışıdır. Bu anlayış, özünde insana önem veren, mevcut nüfusun ekonomik ve toplumsal ihtiyaçlarının karşılanması için gerekli çaba sırasında gelecek kuşakların da ihtiyaçlarını gözeterek doğal ve kültürel kaynakların özenli bir biçimde tüketilmesini öngören sürdürülebilir kalkınma kavramını ortaya çıkarmıştır. Doğal kaynakların sınırlı olduğu ve tükenebileceği gerçeği karşısında çevrenin korunması ve bu durumun süreklilik arz etmesi kaçınılmaz olmaktadır. Günümüzde Sanayileşme, Hızlı ve Düzensiz Kentleşme ve Nüfus kaynaklı çevre sorunları ortaya çıkmış, bu sorunların ortadan kaldırılabilmesi için önemli ölçüde kaynak ayrılmaya başlanılmıştır. Çevre sorunları dünyada olduğu gibi ülkemizde de her geçen gün etkisini artırmakta, -

Design of Blood Supply Chain and Application to Marmara Region in Turkey

EJERS, European Journal of Engineering Research and Science Vol. 4, No. 3, March 2019 Design of Blood Supply Chain and Application to Marmara Region in Turkey Liban Ali Mohamed, Osman Yazicioglu, and Oguz Borat and is in a diastolic phase when it stops. It takes about a Abstract—Blood transfusion is needed due to operations, minute for the blood to circulate through the cardiovascular diseases or accidents. Millions of people's health depends on system and pumping oxygenated blood into the body. The the success of their blood transfusion. Planning and sinus node provides electrical stimuli to contract heart and management is required to supply blood, test against diseases, produce blood products, store t hem and transport them to pump blood. The power of the heart can be calculated by hospitals. A blood supply chain network design such as Blood multiplying the flow by pressure. Turbulent blood flow Donation Centers (CBM), Regional Blood Centers (RBC), through the vessels can be heard as a soft ticking while Destruction Centers (DM), and hospitals are addressed. To measuring blood pressure; this sounds are known as formulate the problem, the General Algebraic Modeling Korotkoff sounds. Although there are 5 recognized System (GAMS) software was applied to the Mixed Integer Korotkoff sounds only 2 are normally recorded. The first Model. When the number of RBC in Marmara region decreased from 3 to 2, opening and transportation costs sound heard indicates systolic pressure and last sound is increased to $5.37 million. When the number of RBCs recorded as diastolic pressure. Cardiac output is the increased from 3 to 4, opening and transportation costs measurement of blood flow rate from the heart through the decreased to $3.94 million. -

Wheat Landraces in Farmers' Fields in Turkey. National Survey, Collection

WHEAT LANDRACES IN FARMERS’ FIELDS IN TURKEY NATIONAL SURVEY, COLLECTION ©FAО/ Mustafa Kan Mustafa ©FAО/ AND CONSERVATION, 2009-2014 ©FAО/ Mustafa Kan Mustafa ©FAО/ Kan Mustafa ©FAО/ ©FAО/ Mustafa Kan Mustafa ©FAО/ Alexey Morgounov ©FAO/ WHEAT LANDRACES IN FARMERS’ FIELDS IN TURKEY NATIONAL SURVEY, COLLECTION AND CONSERVATION, 2009-2014 Mustafa KAN, Murat KÜÇÜKÇONGAR, Mesut KESER, Alexey MORGOUNOV, Hafiz MUMINJANOV, Fatih ÖZDEMIR, Calvin QUALSET FOOD AND AGRICULTURE ORGANIZATION OF THE UNITED NATIONS Ankara, 2015 Citation: FAO, 2015. Wheat Landraces in Farmers’ Fields in Turkey: National Survey, Collection, and Conservation, 2009-2014, by Mustafa Kan, Murat Küçükçongar, Mesut Keser, Alexey Morgounov, Hafiz Muminjanov, Fatih Özdemir, Calvin Qualset The designations employed and the presentation of material in this information product do not imply the expression of any opinion whatsoever on the part of the Food and Agriculture Organization of the United Nations (FAO) concerning the legal or development status of any country, territory, city or area or of its authorities, or concerning the delimitation of its frontiers or boundaries. The mention of specific companies or products of manufacturers, whether or not these have been patented, does not imply that these have been endorsed or recommended by FAO in preference to others of a similar nature that are not mentioned. The views expressed in this information product are those of the author(s) and do not necessarily reflect the views or policies of FAO. ISBN: 978-92-5-109048-0 © FAO, 2015