(Public Pack)Agenda Document For

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Leicester City Council Overview & Scrutiny Handbook

Leicester City Council Overview & Scrutiny Handbook Publication Agreed at Overview Select Committee of 22/09/12 Introduction by Chair of Overview Select Committee I want scrutiny to be as effective as possible in Leicester City Council and this Handbook will help to achieve that. It is designed to help all those involved in scrutiny. To do this we have tried to pull together in one place all of the current information about scrutiny. It contains advice, guidance, and the rules and regulations governing how scrutiny works. For me scrutiny has three main purposes: holding the City Mayor to account, holding the council and other organisations to account and generating ideas and policy. These functions are important in ensuring that the Council is run democratically by involving all members and providing the primary checks and balances on the power of the City Mayor and his cabinet. Scrutiny Commissions will look at the expenditure, administration and policy of the cabinet portfolio they cover. All members should be involved in scrutiny. Members of Scrutiny Committees will involve themselves and contribute to the work of their committee. Executive members will attend, answer questions, explain decisions and policy and the strategy they are pursuing. Officers will attend and be prepared to brief members and answer questions about finance, administration and policy. The spirit of scrutiny should be that of genuine enquiry in our efforts to improve the council and the city for all its citizens. Scrutiny should be conducted without fear of consequences or promise of favour. I hope this handbook will be useful in helping us in our scrutiny work Ross Willmott Chair Overview Select Committee “When the people fear the government, there is tyranny. -

Title 42 Point Poppins Semi Bold

Onstreet Residential Chargepoint Scheme Successful Applicants 18 / 19 Broadhembury Parish Council Buckinghamshire County Council Cardiff City Council Coventry City Council Cranbrook and Sissinghurst Parish Council Dundee City Council East Lindsey District Council East Lothian Council Lambeth Council Lancaster City Council Liverpool City Council London borough of Waltham Forest Luton Borough Council Nottingham City Council Portsmouth City Council South Norfolk Council South Tyneside Council ORCS resources 1 Stirling Council Tadley Town Council Welwyn Parish Council West Berkshire Council West Lindsey District Council West Suffolk Councils ORCS resources 2 19 / 20 Barnsley Council Boston Borough Council Breckland and South Holland Council Brent Council Brighton Council Calderdale Council Canterbury City Council Carmarthenshire County Council Cheshire West and Chester Borough Council Chichester District Council Coventry City Council Derbyshire County Council Dundee City Council East Lothian Council East Riding of Yorkshire Essex County Council Great Yarmouth Borough Council Gwent County Borough Council Halton Borough Council Hovingham Parish Council Isle of Wight ORCS resources 3 Kettering Borough Council Leicester City Council London Borough of Bexley London Borough of Camden London Borough of Hammersmith and Fulham London Borough of Harrow London Borough of Islington North Norfolk Portsmouth City Council Powys County Council Reading Borough Council Richmond Council South Kesteven District Council South Tyneside Council Swansea Council -

Leicester's Green Infrastructure Strategy

LEICESTER GREEN INFRASTRUCTURE STRATEGY 2015-2025 EVIDENCE BASE, ACTIONS AND OPPORTUNITIES 1 | P a g e FOREWORD This framework sets out the strategic vision for our green sites in Leicester and the ways in which they can be created, managed and maintained to provide maximum benefits to the people who live, work or visit Leicester. The actions are supported by an evidence base of data and information which recognise and prioritise key areas where resources can be focussed to develop high quality green infrastructure (GI) into our new and existing communities. By placing the framework within the planning system it is possible to provide the key tools needed to secure these areas and design them to provide multi- functional green space. Improvements to established green space and creating new sites to surround built development will provide an accessible and natural green network. These areas will be capable of supporting a range of functions which include landscaping/public amenity, recreation, flood control, safer access routes, cooler areas to combat predicted climate change and places for wildlife. These functions give rise to a range of environmental and quality of life benefits which include providing attractive and distinctive places to live, work and play; improving public health, facilitating access and encouraging sustainable transport as well as offering an environment to support wildlife. Placing a monetary value on these benefits is difficult, but many have potential to deliver significant economic value by increasing the attractiveness of a neighbourhood for businesses and employers, encouraging tourism and associated revenue, reducing health care costs and maintenance or clean-up costs from flooding. -

Pharmaceutical Needs Assessment Project Team Leicester City Council, Leicestershire County Council, Rutland County Council

APPENDIX 1 PHARMACEUTICAL NEEDS ASSESSMENT PROJECT TEAM LEICESTER CITY COUNCIL, LEICESTERSHIRE COUNTY COUNCIL, RUTLAND COUNTY COUNCIL TERMS OF REFERENCE Purpose: The Pharmaceutical Needs Assessment (PNA) is a legal duty of the Health and Wellbeing Board (HWB) and each HWB will need to publish its own revised PNA for its area by 1st April 2015. The purpose of this project team is to identify opportunities to work together across Leicester, Leicestershire and Rutland to jointly develop PNA across the three HWBs and to identify areas where there are key benefits to working together. The team will set the timetable for the development of the PNA, agree the format and content of the PNA and ensure that each PNA fulfils statutory duties around consultation for the PNA. The team will be a task and finish group, meeting between March 2014 and March 2015. Key responsibilities: To oversee the PNA process across the three Health and Wellbeing Board areas To ensure that the development of the PNA meets the statutory duties of the HWBs To support the three HWBs in the development of their PNAs by working collaboratively across the LLR area to ensure that the evidence base is effective and joined up to better support NHS England, CCGs and Local Authoritys in their commissioning decisions To ensure active engagement from all stakeholders To communicate to a wider audience how the PNA is being developed To ensure that the PNA addresses issues of provision and identifies need To map current provision of pharmaceutical services To identify any gaps in pharmaceutical provision To map any future provision Governance: The three Health and Wellbeing Boards are each responsible for ensuring that there is a PNA for its area. -

Leicestershire and Rutland a Guide to Care and Independent Living Summer 2018 Leaving Hospital What’S Next? NHS Continuing Healthcare Who’S Eligible? FREE Guide

OPTIONS Leicestershire and Rutland A guide to care and independent living Summer 2018 Leaving hospital What’s next? NHS continuing healthcare Who’s eligible? FREE guide CONTRIBUTORS: Age UK Leicester Shire and Rutland Leicester City Council Leicestershire County Council Leicestershire Partnership NHS Trust SOCIAL CARE NHS Choices 10 Rutland County Council University Hospitals of tips Leicester NHS Trust PROFESSIONAL HOME CARE WITH CONFIDENCE & TRUST Crystal Home Care is a non-medical home care Our Clients We are dedicated to serving our clients and agency owned and operated by a multi-talented and We ensure our clients are shown and given the communities with exemplary care services through our multi-specialist team. respect they deserve. professional, caring and experienced healthcare staff. We provide unique, affordable and professional care We offer personal care and comfort to elders Our Team services to a wide range of people in their homes and who are:- We select our resource on the basis of compassion, community in order to help them live independently. • In need of assistance with daily living activities reliability and experience, all our care workers are fully We understand the importance of being in control of • Living alone • Disabled or wheelchair bound trained and security checked. your life and care, so we design our services to support • Recovering from surgery or illness When choosing a homecare service, one consideration your personal choices at every stage by providing Our objective is to meet our clients expectations stands above all, the quality of care workers who will personal care 24/7 dependent on every individual needs by building a care worker-client relationship through be by your side, that’s why we go the extra distance to whether it be home, in a nursing home or in hospital. -

Title, Initial, Surname

Christopher Margetts My ref: 101003286971 Date: 14 July 2017 Sent by email: [email protected] Dear Mr Margetts Your request under the Freedom of Information Act 2000 Thank you for your information access request which we received on 24 June 2017. Please find enclosed the Council’s response to your request. We hope that this fully satisfies your enquiry, but should you require further information at any time please feel free to submit a new request. Cornwall Council is committed to open and transparent government and provides information to members of the public about all aspects of the authority. We deal with over 4000 requests for information each year. We estimate that the cost to Cornwall Council of dealing with each request ranges between £150 and £350 to administer. You may be able to find the information by checking previous responses using www.cornwall.gov.uk/default.aspx?page=24586 or checking the Council’s website at www.cornwall.gov.uk. Most of the information that we provide in response to Freedom of Information requests will be subject to copyright protection. In most cases the copyright will be owned by Cornwall Council. The copyright in other information may be owned by another person or organisation, as indicated in the information itself. Konsel Kernow Cornwall Council, County Hall Truro, TR1 3AY Tel: 0300 1234 100 www.cornwall.gov.uk You are free to use any information supplied for your own use, including for non- commercial research purposes. The information may also be used for the purposes of news reporting. -

Sustainable Homes for People… Creating a Great Place to Live

LEICESTER Sustainable homes for people… creating a great place to live MARKETING BROCHURE foreword by LEICESTER CITY MAYOR Ashton Green is seen as the most innovative and sustainable new development in Leicester in more than 30 years and will enable substantial progress towards delivering the 20,000 new homes needed in the City over the next 20 years. Ashton Green will make a significant contribution towards delivering quality new homes in Leicester and raising its profile as the place to do business in the East Midlands. The site has the potential to deliver the highest quality of built environment whilst protecting and enhancing the natural surroundings in this part of the city. In addition to much needed new homes, this major development will bring employment land opportunities with new jobs, economic, regeneration and social benefits for the wider community. Leicester City Council will retain influence and direction over the future development as land owner and local planning authority to ensure the long term delivery of the Ashton Green vision of a sustainable new community. With an outline planning permission, infrastructure delivery plan and phasing strategy already in place, the Council is now bringing the site forward for development. Expressions of interest are being invited from developers with the commitment to bring forward a first parcel of high quality new homes from early 2015 and further commercial development opportunities will follow later. This is a unique, exciting and challenging development opportunity and we very much look forward to working with the most creative and innovative partners within the development industry to bring forward the Ashton Green vision. -

Annex a MHCLG Counter Fraud Fund Successful Bids

Annex A MHCLG Counter Fraud Fund Successful Bids Lead authority Name of bid Funding allocated (£) Barnsley Metropolitan Borough Establishment of a Corporate Fraud Team within 118,600 Council Internal Audit Bedford Borough Council Tenancy Fraud and Council Tax Fraud 146,370 Birmingham City Council Fraud and Error- Continuous Monitoring and Detection 105,050 Brighton & Hove City Council Blue Badge Misuse: Detect, Enforce & Educate 183,000 Cambridgeshire County Council/ The Development of a Regional Multi-Organisational 329,200 Northamptonshire County Counter-Fraud Operation Council Cotswold District Council The Gloucestershire-Oxfordshire Counter Fraud “Data 403,000 Gateway” Croydon Council Tackling "Health Tourism" and those with "No 77,430 Recourse to Public Funds" fraud Doncaster Metropolitan Borough Fraud Awareness improvements and Data Matching 98,294 Council (Doncaster and Rotherham) Durham County Council Procurement Fraud Partnership Pilot 51,350 East Lindsey District Council East Coast Business Rates Assurance Function 125,820 East Riding of Yorkshire Council Humber Data Intelligence Hub 129,425 Eastbourne Borough Council Fighting Fraud in East Sussex 365,000 Erewash Borough Council Derbyshire Joint Fraud Initiative 698,000 Hampshire County Council Integrating Fraud Risk Assessment and Data Analysis 71,500 Hertfordshire County Council Shared Anti-Fraud Service in Hertfordshire 366,000 Huntingdonshire District Council Cambridgeshire Anti-Fraud Network 335,100 Kent County Council Kent Intelligence Network (KIN) 480,080 Leeds City Council Competition Damages Recovery Unit 750,000 Leicester City Council Tackling Insurance Fraud- the way forward 310,173 Leicester City Council Leicester, Leicestershire and Rutland Intelligence Hub 470,109 Lincolnshire County Council Lincolnshire Fraud Partnership 200,000 London Borough of Barking & Holistic approach to the use of an Accredited Financial 64,152 Dagenham Investigator to detect, prevent and investigate fraud. -

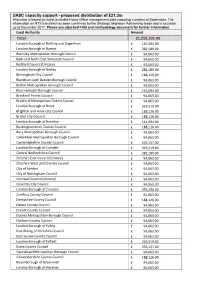

UASC Capacity Support - Proposed Distribution of £21.3M Allocation Is Based on Latest Available Home Office Management Data Capturing Numbers at September

UASC capacity support - proposed distribution of £21.3m Allocation is based on latest available Home Office management data capturing numbers at September. The information on NTS transfers has been confirmed by the Strategic Migration Partnership leads and is accurate up to December 2017. Please see attached FAQ and methodology document for further information. Local Authority Amount Total 21,258,203.00 London Borough of Barking and Dagenham £ 141,094.00 London Borough of Barnet £ 282,189.00 Barnsley Metropolitan Borough Council £ 94,063.00 Bath and North East Somerset Council £ 94,063.00 Bedford Council (Unitary) £ 94,063.00 London Borough of Bexley £ 282,189.00 Birmingham City Council £ 188,126.00 Blackburn with Darwen Borough Council £ 94,063.00 Bolton Metropolitan Borough Council £ 94,063.00 Bournemouth Borough Council £ 141,094.00 Bracknell Forest Council £ 94,063.00 Bradford Metropolitan District Council £ 94,063.00 London Borough of Brent £ 329,219.00 Brighton and Hove City Council £ 188,126.00 Bristol City Council £ 188,126.00 London Borough of Bromley £ 141,094.00 Buckinghamshire County Council £ 188,126.00 Bury Metropolitan Borough Council £ 94,063.00 Calderdale Metropolitan Borough Council £ 94,063.00 Cambridgeshire County Council £ 235,157.00 London Borough of Camden £ 329,219.00 Central Bedfordshire Council £ 282,189.00 Cheshire East Council (Unitary) £ 94,063.00 Cheshire West and Chester Council £ 94,063.00 City of London £ 94,063.00 City of Nottingham Council £ 94,063.00 Cornwall Council (Unitary) £ 94,063.00 Coventry City -

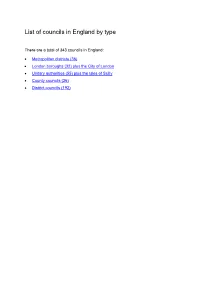

List of Councils in England by Type

List of councils in England by type There are a total of 343 councils in England: • Metropolitan districts (36) • London boroughs (32) plus the City of London • Unitary authorities (55) plus the Isles of Scilly • County councils (26) • District councils (192) Metropolitan districts (36) 1. Barnsley Borough Council 19. Rochdale Borough Council 2. Birmingham City Council 20. Rotherham Borough Council 3. Bolton Borough Council 21. South Tyneside Borough Council 4. Bradford City Council 22. Salford City Council 5. Bury Borough Council 23. Sandwell Borough Council 6. Calderdale Borough Council 24. Sefton Borough Council 7. Coventry City Council 25. Sheffield City Council 8. Doncaster Borough Council 26. Solihull Borough Council 9. Dudley Borough Council 27. St Helens Borough Council 10. Gateshead Borough Council 28. Stockport Borough Council 11. Kirklees Borough Council 29. Sunderland City Council 12. Knowsley Borough Council 30. Tameside Borough Council 13. Leeds City Council 31. Trafford Borough Council 14. Liverpool City Council 32. Wakefield City Council 15. Manchester City Council 33. Walsall Borough Council 16. North Tyneside Borough Council 34. Wigan Borough Council 17. Newcastle Upon Tyne City Council 35. Wirral Borough Council 18. Oldham Borough Council 36. Wolverhampton City Council London boroughs (32) 1. Barking and Dagenham 17. Hounslow 2. Barnet 18. Islington 3. Bexley 19. Kensington and Chelsea 4. Brent 20. Kingston upon Thames 5. Bromley 21. Lambeth 6. Camden 22. Lewisham 7. Croyd on 23. Merton 8. Ealing 24. Newham 9. Enfield 25. Redbridge 10. Greenwich 26. Richmond upon Thames 11. Hackney 27. Southwark 12. Hammersmith and Fulham 28. Sutton 13. Haringey 29. Tower Hamlets 14. -

Leicester, Leicestershire and Rutland Police and Crime Panel

Leicester, Leicestershire and Rutland Police and Crime Panel Constitution INDEX PART 1 - Terms of Reference page 2. PART 2 - Panel Arrangements page 5. PART 3 - Rules of Procedure page 10. PART 4 - Making a Complaint about the Police and Crime Commissioner or Deputy Police and Crime Commissioner page 27. PART 5 - Role of the Police and Crime Commissioner page 33. SCHEDULES page 35. 1 PART 1 TERMS OF REFERENCE 2 1. TERMS OF REFERENCE Introduction The Leicester, Leicestershire and Rutland Police and Crime Panel will publicly scrutinise the actions and decisions of the Police and Crime Commissioner (PCC) in the context of relevant sections of the Police Reform and Social Responsibility Act 2011, with a view to supporting and challenging the PCC in the effective exercise of his or her functions, acting as a critical friend. References in this document to the ‘PCP’ are references to the Police and Crime Panel. Terms of Reference (as agreed by all relevant local authorities) The Police and Crime Panel will be a joint Committee of Blaby District Council, Charnwood Borough Council, Harborough District Council, Hinckley and Bosworth Borough Council, Leicester City Council, Leicestershire County Council, Melton Borough Council, North West Leicestershire District Council, Rutland County Council and Oadby and Wigston Borough Council. To enable it to effectively scrutinise and support the Police and Crime Commissioner in the exercise of his or her functions, the PCP will: Review and report/make recommendations to the PCC in respect of his/her draft -

1 Leicester, Leicestershire and Rutland Child Death Overview Panel

Leicester, Leicestershire and Rutland Child Death Overview Panel (CDOP) CDOP Arrangements Overview The Leicester, Leicestershire and Rutland CDOP has been set up by Child Death Review (CDR) Partners (Leicester City Council, Leicestershire County Council, Rutland Council, Leicester City CCG, West Leicestershire CCG, and East Leicestershire and Rutland CCG) to review the deaths of children under the requirements of the Children Act, 2004 and Working Together to Safeguard Children, 2018. Purpose The purpose of the Leicester, Leicestershire and Rutland CDOP is to undertake a review of all child deaths (excluding both those babies who are stillborn and planned terminations of pregnancy carried out within the law) up to the age of 18 years, normally resident in Leicester, Leicestershire and Rutland, irrespective of the place of their death. The Leicester, Leicestershire and Rutland CDOP will adhere to the statutory guidance: Child Death Review Statutory and Operational Guidance (England) 2018: https://www.gov.uk/government/publications/child-death-review-statutory-and- operational-guidance-england. CDOP Responsibilities To collect and collate information about each child death, seeking relevant information from professionals and, where appropriate, family members; To analyse the information obtained, including the report from the Child Death Review Manager (CDRM), in order to confirm or clarify the cause of death, to determine any contributory factors, and to identify learning arising from the child death review process that may prevent future