Vontobel Fund - European Equity

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Factset-Top Ten-0521.Xlsm

Pax International Sustainable Economy Fund USD 7/31/2021 Port. Ending Market Value Portfolio Weight ASML Holding NV 34,391,879.94 4.3 Roche Holding Ltd 28,162,840.25 3.5 Novo Nordisk A/S Class B 17,719,993.74 2.2 SAP SE 17,154,858.23 2.1 AstraZeneca PLC 15,759,939.73 2.0 Unilever PLC 13,234,315.16 1.7 Commonwealth Bank of Australia 13,046,820.57 1.6 L'Oreal SA 10,415,009.32 1.3 Schneider Electric SE 10,269,506.68 1.3 GlaxoSmithKline plc 9,942,271.59 1.2 Allianz SE 9,890,811.85 1.2 Hong Kong Exchanges & Clearing Ltd. 9,477,680.83 1.2 Lonza Group AG 9,369,993.95 1.2 RELX PLC 9,269,729.12 1.2 BNP Paribas SA Class A 8,824,299.39 1.1 Takeda Pharmaceutical Co. Ltd. 8,557,780.88 1.1 Air Liquide SA 8,445,618.28 1.1 KDDI Corporation 7,560,223.63 0.9 Recruit Holdings Co., Ltd. 7,424,282.72 0.9 HOYA CORPORATION 7,295,471.27 0.9 ABB Ltd. 7,293,350.84 0.9 BASF SE 7,257,816.71 0.9 Tokyo Electron Ltd. 7,049,583.59 0.9 Munich Reinsurance Company 7,019,776.96 0.9 ASSA ABLOY AB Class B 6,982,707.69 0.9 Vestas Wind Systems A/S 6,965,518.08 0.9 Merck KGaA 6,868,081.50 0.9 Iberdrola SA 6,581,084.07 0.8 Compagnie Generale des Etablissements Michelin SCA 6,555,056.14 0.8 Straumann Holding AG 6,480,282.66 0.8 Atlas Copco AB Class B 6,194,910.19 0.8 Deutsche Boerse AG 6,186,305.10 0.8 UPM-Kymmene Oyj 5,956,283.07 0.7 Deutsche Post AG 5,851,177.11 0.7 Enel SpA 5,808,234.13 0.7 AXA SA 5,790,969.55 0.7 Nintendo Co., Ltd. -

Common Stocks — 104.5%

Eaton Vance Tax-Advantaged Global Dividend Income Fund January 31, 2021 PORTFOLIO OF INVESTMENTS (Unaudited) Common Stocks — 104.5% Security Shares Value Aerospace & Defense — 0.8% Safran S.A.(1) 98,721 $ 12,409,977 $ 12,409,977 Banks — 6.7% Bank of New York Mellon Corp. (The) 518,654 $ 20,657,989 Citigroup, Inc. 301,884 17,506,253 HDFC Bank, Ltd.(1) 512,073 9,775,702 ING Groep NV(1) 1,676,061 14,902,461 Japan Post Bank Co., Ltd. 445,438 3,851,696 Mitsubishi UFJ Financial Group, Inc. 2,506,237 11,317,609 Mizuho Financial Group, Inc. 292,522 3,856,120 Sumitomo Mitsui Financial Group, Inc. 186,747 5,801,916 Wells Fargo & Co. 341,979 10,218,332 $ 97,888,078 Beverages — 1.0% Diageo PLC 378,117 $ 15,180,328 $ 15,180,328 Biotechnology — 1.2% CSL, Ltd. 82,845 $ 17,175,550 $ 17,175,550 Building Products — 0.9% Assa Abloy AB, Class B 509,607 $ 12,603,485 $ 12,603,485 Chemicals — 0.7% Sika AG 38,393 $ 10,447,185 $ 10,447,185 Construction & Engineering — 0.0% Abengoa S.A., Class A(1)(2) 311,491 $ 0 Abengoa S.A., Class B(1)(2) 3,220,895 0 $0 Construction Materials — 0.9% CRH PLC 332,889 $ 13,660,033 $ 13,660,033 Consumer Finance — 0.6% Capital One Financial Corp. 79,722 $ 8,311,816 $ 8,311,816 1 Security Shares Value Diversified Financial Services — 2.5% Berkshire Hathaway, Inc., Class B(1) 101,853 $ 23,209,243 ORIX Corp. -

COMMON STOCKS - 97.05% Argentina - 1.72% (A)

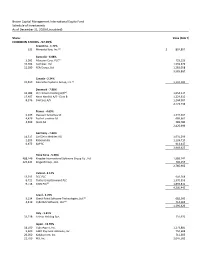

Yeah Brown Capital Management International Equity Fund Schedule of Investments As of December 31, 2020 (Unaudited) Shares Value (Note 1) COMMON STOCKS - 97.05% Argentina - 1.72% (a) 533 MercadoLibre, Inc. $ 892,892 Australia - 6.88% (a) 3,092 Atlassian Corp. PLC 723,126 10,704 Cochlear, Ltd. 1,559,676 11,180 REA Group, Ltd. 1,283,058 3,565,860 Canada - 2.24% (a) 19,819 Descartes Systems Group, Inc. 1,159,183 Denmark - 7.96% (a) 16,089 Chr Hansen Holding A/S 1,654,217 17,487 Novo Nordisk A/S - Class B 1,224,612 8,376 SimCorp A/S 1,244,907 4,123,736 France - 4.69% 6,639 Dassault Systemes SE 1,347,557 4,426 EssilorLuxottica SA 689,662 4,699 Ipsen SA 389,780 2,426,999 Germany - 7.66% 14,517 Carl Zeiss Meditec AG 1,931,296 1,209 Rational AG 1,124,710 6,975 SAP SE 913,617 3,969,623 Hong Kong - 5.38% 488,146 Kingdee International Software Group Co., Ltd. 1,989,747 123,443 Kingsoft Corp., Ltd. 796,155 2,785,902 Ireland - 8.12% 13,293 DCC PLC 941,268 6,721 Flutter Entertainment PLC 1,370,359 (a) 9,718 ICON PLC 1,894,816 4,206,443 Israel - 2.70% (a) 5,134 Check Point Software Technologies, Ltd. 682,360 (a) 4,419 CyberArk Software, Ltd. 714,066 1,396,426 Italy - 1.41% 33,718 Azimut Holding SpA 731,970 Japan - 13.70% 18,500 CyberAgent, Inc. 1,273,885 5,600 GMO Payment Gateway, Inc. -

Annex 1: Parker Review Survey Results As at 2 November 2020

Annex 1: Parker Review survey results as at 2 November 2020 The data included in this table is a representation of the survey results as at 2 November 2020, which were self-declared by the FTSE 100 companies. As at March 2021, a further seven FTSE 100 companies have appointed directors from a minority ethnic group, effective in the early months of this year. These companies have been identified through an * in the table below. 3 3 4 4 2 2 Company Company 1 1 (source: BoardEx) Met Not Met Did Not Submit Data Respond Not Did Met Not Met Did Not Submit Data Respond Not Did 1 Admiral Group PLC a 27 Hargreaves Lansdown PLC a 2 Anglo American PLC a 28 Hikma Pharmaceuticals PLC a 3 Antofagasta PLC a 29 HSBC Holdings PLC a InterContinental Hotels 30 a 4 AstraZeneca PLC a Group PLC 5 Avast PLC a 31 Intermediate Capital Group PLC a 6 Aveva PLC a 32 Intertek Group PLC a 7 B&M European Value Retail S.A. a 33 J Sainsbury PLC a 8 Barclays PLC a 34 Johnson Matthey PLC a 9 Barratt Developments PLC a 35 Kingfisher PLC a 10 Berkeley Group Holdings PLC a 36 Legal & General Group PLC a 11 BHP Group PLC a 37 Lloyds Banking Group PLC a 12 BP PLC a 38 Melrose Industries PLC a 13 British American Tobacco PLC a 39 Mondi PLC a 14 British Land Company PLC a 40 National Grid PLC a 15 BT Group PLC a 41 NatWest Group PLC a 16 Bunzl PLC a 42 Ocado Group PLC a 17 Burberry Group PLC a 43 Pearson PLC a 18 Coca-Cola HBC AG a 44 Pennon Group PLC a 19 Compass Group PLC a 45 Phoenix Group Holdings PLC a 20 Diageo PLC a 46 Polymetal International PLC a 21 Experian PLC a 47 -

DCC Plc Annual Report and Accounts 2019

DCC plc Annual Report and Accounts 2019 WorldReginfo - 47739327-57d6-4662-9440-8b5adb4dd3e6 DCC is a leading international sales, marketing and support services group with a clear focus on performance and growth, which operates across four divisions: LPG, Retail & Oil, Technology and Healthcare. DCC is an ambitious and entrepreneurial business operating in 17 countries, supplying products and services used by millions of people every day. Building strong routes to market, driving for results, focusing on cash conversion and generating superior sustainable returns on capital employed enable the Group to reinvest in its business, creating value for its stakeholders. DCC plc is listed on the London Stock Exchange and is a constituent of the FTSE 100. LPG Retail & Oil Technology Healthcare Page 42 Page 48 Page 54 Page 60 Strategic Report Governance Financial Statements ii DCC at a Glance 73 Chairman’s Introduction 124 Statement of Directors’ 1 Highlights of the Year 74 Board of Directors Responsibilities 2 Strategy 76 Group Management Team 125 Independent Auditor’s Report 4 Business Model 77 Corporate Governance Statement 129 Financial Statements 6 Chairman’s Statement 84 Nomination and Governance 8 Chief Executive’s Review Committee Report Supplementary Information 88 Audit Committee Report 10 Key Performance Indicators 210 Principal Subsidiaries, Joint Ventures 14 Risk Report 93 Remuneration Report and Associates 21 Financial Review 119 Report of the Directors 214 Shareholder Information 30 Strategy in Action 216 Corporate Information 42 -

FTF Franklin UK Equity Income Fund August 31, 2021

FTF - FTF Franklin UK Equity Income Fund August 31, 2021 FTF - FTF Franklin UK Equity August 31, 2021 Income Fund Portfolio Holdings The following portfolio data for the Franklin Templeton funds is made available to the public under our Portfolio Holdings Release Policy and is "as of" the date indicated. This portfolio data should not be relied upon as a complete listing of a fund's holdings (or of a fund's top holdings) as information on particular holdings may be withheld if it is in the fund's interest to do so. Additionally, foreign currency forwards are not included in the portfolio data. Instead, the net market value of all currency forward contracts is included in cash and other net assets of the fund. Further, portfolio holdings data of over-the-counter derivative investments such as Credit Default Swaps, Interest Rate Swaps or other Swap contracts list only the name of counterparty to the derivative contract, not the details of the derivative. Complete portfolio data can be found in the semi- and annual financial statements of the fund. Security Security Shares/ Market % of Coupon Maturity Identifier Name Positions Held Value TNA Rate Date 0673123 ASSOCIATED BRITISH FOODS PLC 795,000 £15,741,000 1.75% N/A N/A 0989529 ASTRAZENECA PLC 526,000 £44,783,640 4.98% N/A N/A 0263494 BAE SYSTEMS PLC 2,560,000 £14,551,040 1.62% N/A N/A BH0P3Z9 BHP GROUP PLC 927,000 £20,927,025 2.33% N/A N/A B3FLWH9 BODYCOTE PLC 1,340,000 £12,924,300 1.44% N/A N/A 0798059 BP PLC 10,175,000 £30,214,662 3.36% N/A N/A 0176581 BREWIN DOLPHIN HOLDINGS PLC 3,442,000 -

FTF - FTF Franklin UK Rising Dividends Fund August 31, 2021

FTF - FTF Franklin UK Rising Dividends Fund August 31, 2021 FTF - FTF Franklin UK Rising August 31, 2021 Dividends Fund Portfolio Holdings The following portfolio data for the Franklin Templeton funds is made available to the public under our Portfolio Holdings Release Policy and is "as of" the date indicated. This portfolio data should not be relied upon as a complete listing of a fund's holdings (or of a fund's top holdings) as information on particular holdings may be withheld if it is in the fund's interest to do so. Additionally, foreign currency forwards are not included in the portfolio data. Instead, the net market value of all currency forward contracts is included in cash and other net assets of the fund. Further, portfolio holdings data of over-the-counter derivative investments such as Credit Default Swaps, Interest Rate Swaps or other Swap contracts list only the name of counterparty to the derivative contract, not the details of the derivative. Complete portfolio data can be found in the semi- and annual financial statements of the fund. Security Security Shares/ Market % of Coupon Maturity Identifier Name Positions Held Value TNA Rate Date 0673123 ASSOCIATED BRITISH FOODS PLC 155,000 £3,069,000 2.01% N/A N/A 0989529 ASTRAZENECA PLC 84,000 £7,151,760 4.68% N/A N/A 0263494 BAE SYSTEMS PLC 575,000 £3,268,300 2.14% N/A N/A BYQ0JC6 BEAZLEY PLC 680,000 £2,662,200 1.74% N/A N/A 3314775 BLOOMSBURY PUBLISHING PLC 660,000 £2,329,800 1.52% N/A N/A B3FLWH9 BODYCOTE PLC 275,000 £2,652,375 1.74% N/A N/A 0176581 BREWIN DOLPHIN HOLDINGS -

20100107 Trading Notice Functional 0221

Trading Notice - 0221 Date: 7th January 2010 Priority: Notification Bulletin Subject: Chi-X launches services in Irish stocks with EMCF N.V. on 22 nd January 2010 Sent from: Trading Operations Message: Chi-X Europe Ltd (Chi-X) is pleased to announce the addition of the Irish market segment to its EMCF cleared stock universe. The following ISEQ 20 stocks will be available to trade from Friday 22nd January 2010: Chi-X Bloomberg Name UMTF RIC Chi-X RIC Bloomberg Code ISIN Allied Irish Banks PLC AIBi ALBK.I ALBKi.CHI ALBK ID ALBK IX IE0000197834 Aryzta AG YZAi ARYN.I ARYNi.CHI YZA ID YZA IX CH0043238366 Bank of Ireland BIRi BKIR.I BKIRi.CHI BKIR ID BKIR IX IE0030606259 C&C Group PLC GCCi GCC.I GCCi.CHI GCC ID GCC IX IE00B010DT83 CRH PLC CRGi CRH.I CRHi.CHI CRH ID CRH IX IE0001827041 DCC PLC DCCi DCC.I DCCi.CHI DCC ID DCC IX IE0002424939 Dragon Oil PLC DRSi DGO.I DGOi.CHI DGO ID DGO IX IE0000590798 Elan Corporation PLC DRXi ELN.I ELNi.CHI ELN ID ELN IX IE0003072950 F.B.D Holdings PLC EG7i FBD.I FBDi.CHI FBD ID FBD IX IE0003290289 Glanbia PLC GL9i GL9.I GL9i.CHI GLB ID GLB IX IE0000669501 Grafton Group PLC GN5i GRF_u.I GRF_ui.CHI GN5 ID GN5 IX IE00B00MZ448 Greencore Group PLC GCGi GNC.I GNCi.CHI GNC ID GNC IX IE0003864109 Independent News & Media PLC IPDi INME.I INMEi.CHI INM ID INWS IX IE0004614818 Irish Life & Permanent PLC ILBi IPM.I IPMi.CHI IPM ID IPM IX IE0004678656 Kerry Group PLC KRZi KYGa.I KYGai.CHI KYG ID KYG IX IE0004906560 Kingspan Group PLC KRXi KSP.I KSPi.CHI KSP ID KSP IX IE0004927939 Paddy Power PLSi PAP.I PAPi.CHI PWL ID PWL IX IE0002588105 Ryanair Holdings PLC RY4Bi RYA.I RYAi.CHI RYA ID RYA IX IE00B1GKF381 Smurfit Kappa Group PLC SK3i SKG.I SKGi.CHI SKG ID SKG IX IE00B1RR8406 United Drug PLC UN6Ai UDG.I UDGi.CHI UDG ID UDG IX IE0033024807 Current Trading Participants who require access to the above market segment are required to complete, sign and return the Access to Markets form to Chi-X Compliance. -

Agenda Item 4B-02 Attachment 2

Attachment 2, Page 1 of 5 CalPERS 2013 Northern Ireland Report CalPERS Holdings of Non-US Companies with Operations in Northern Ireland as of December 31, 2013 Equity Exposure Fixed Income Exposure Company Name Country Number of shares Market Value Par Value Market Value Total Market Value 3I GROUP PLC United Kingdom 2,574,784 $ 16,422,524.30 $ 16,422,524.30 Abertis Infraestructuras, S.A. Spain 1,593,291 $ 35,456,913.79 $ 35,456,913.79 Adecco S.A. Switzerland 496,749 $ 39,433,833.03 $ 39,433,833.03 Aer Lingus Group PLC Ireland 690,822 $ 1,220,358.65 $ 1,220,358.65 AGF Management Limited Canada 473,502 $ 5,913,761.45 $ 5,913,761.45 Akzo Nobel N.V. Netherlands 913,438 $ 70,913,548.72 $ 70,913,548.72 Allianz SE Germany 1,688,214 $ 303,229,768.85 $ 303,229,768.85 Anglo American PLC United Kingdom 7,998,118 $ 174,864,659.74 $ 174,864,659.74 AON PLC United Kingdom 884,243 $ 74,179,145.27 $ 74,179,145.27 ASSOCIATED BRITISH FOODS PLC United Kingdom 942,014 $ 38,147,125.08 $ 38,147,125.08 AstraZeneca PLC United Kingdom 4,953,597 $ 293,321,909.59 $ 293,321,909.59 ATOS S.A. France 268,961 $ 24,382,739.52 $ 24,382,739.52 AVIVA PLC United Kingdom 10,790,113 $ 80,366,392.33 $ 80,366,392.33 Axa SA France 7,018,874 $ 195,464,125.84 28,000,000 $ 28,389,999.68 $ 223,854,125.52 AYALA CORPORATION Philippines 609,480 $ 7,113,403.71 $ 7,113,403.71 BABCOCK INTERNATIONAL GROUP PLC United Kingdom 1,071,215 $ 24,040,391.35 $ 24,040,391.35 Banco Santander, S.A. -

COMMON STOCKS - 95.94% Australia - 4.43% (A)

Yeah Brown Capital Management International Equity Fund Schedule of Investments As of June 30, 2020 (Unaudited) Shares Value (Note 1) COMMON STOCKS - 95.94% Australia - 4.43% (a) 483 Atlassian Corp. PLC $ 87,070 7,426 Cochlear, Ltd. 968,203 5,944 REA Group, Ltd. 442,518 1,497,791 Canada - 1.89% (a) 12,124 Descartes Systems Group, Inc. 640,046 Denmark - 7.16% 9,068 Chr Hansen Holding A/S 935,170 15,091 Novo Nordisk A/S - Class B 977,018 4,724 SimCorp A/S 509,259 2,421,447 France - 6.31% 7,521 Dassault Systemes SE 1,297,890 (a) 3,819 EssilorLuxottica SA 490,204 4,055 Ipsen SA 344,644 2,132,738 Germany - 9.22% (a) 12,528 Carl Zeiss Meditec AG 1,221,722 1,034 Rational AG 578,988 9,410 SAP SE 1,314,321 3,115,031 Hong Kong - 6.00% 611,146 Kingdee International Software Group Co., Ltd. 1,420,922 130,443 Kingsoft Corp., Ltd. 606,731 2,027,653 Ireland - 9.27% 11,472 DCC PLC 956,663 (a) 5,800 Flutter Entertainment PLC 762,404 (a) 8,387 ICON PLC 1,412,874 3,131,941 Israel - 2.34% (a) 4,998 Check Point Software Technologies, Ltd. 536,935 (a) 2,564 CyberArk Software, Ltd. 254,528 791,463 Italy - 1.47% 29,099 Azimut Holding SpA 497,254 Japan - 12.81% 16,000 CyberAgent, Inc. 783,885 4,500 GMO Payment Gateway, Inc. 468,442 17,000 Kakaku.com, Inc. 429,664 24,300 M3, Inc. -

Agenda Item 4B

CalPERS 2012 Northern Ireland Report CalPERS Holdings of Non‐U.S. Companies with Operations in Northern Ireland as of December 31, 2012 Attachment 2, Page 1 of 5 Equity Exposure Fixed Income Exposure MacBride Catholic Protestant Company Name Country Agreement Underrepresentation Underrepresentation Number of shares Market Value Par Value Market Value Total Market Value 3i Group PLC United Kingdom Unknown No Yes 2,493,405 $ 8,803,185 $ 8,803,185 Abertis Infraestructuras SA Spain Unknown No No 1,314,151 $ 21,518,606 $ 21,518,606 Adecco SA Switzerland Unknown No Yes 506,864 $ 26,601,569 $ 26,601,569 Aer Lingus Group PLC Ireland Unknown No Yes 628,117 $ 915,061 $ 915,061 AGF Management Limited Canada Unknown Unknown Unknown 415,302 $ 4,137,587 $ 4,137,587 Akzo Nobel NV Netherlands Unknown No No 889,444 $ 58,333,136 $ 58,333,136 Allianz SE Germany Yes No No 1,588,478 $ 219,477,379 $ 219,477,379 Anglo American PLC United Kingdom Unknown Unknown Unknown 4,248,153 $ 130,787,828 500,000 $ 549,660 $ 131,337,488 Aon PLC United Kingdom Yes Yes No 897,247 $ 49,886,933 $ 49,886,933 Associated British Foods plc United Kingdom Yes Yes Yes 1,024,685 $ 26,050,396 $ 26,050,396 AstraZeneca PLC United Kingdom Unknown No Yes 4,338,354 $ 205,177,886 $ 205,177,886 ATOS S.A. France Unknown Unknown Unknown 292,332 $ 20,372,803 $ 20,372,803 Aviva plc United Kingdom Unknown No No 10,904,172 $ 66,113,284 $ 66,113,284 Axa SA France Unknown No Yes 9,924,754 $ 174,682,056 28,000,000 $ 28,520,000 $ 203,202,056 Ayala Corporation Philippines Unknown No Yes 533,454 $ 6,716,486 $ 6,716,486 Babcock International Group PLC United Kingdom Unknown Unknown Unknown 1,080,538 $ 16,958,191 $ 16,958,191 Banco Santander, S.A. -

Annual Report and Accounts 2019

HSBC UK Bank plc Annual Report and Accounts 2019 Contents Presentation of information Page This document comprises the Annual Report and Accounts 2019 Strategic report for HSBC UK Bank plc (‘the bank’) and its subsidiaries (together Key financial metrics 2 ‘HSBC UK’ or ‘the group’). ’We’, ‘us’ and ‘our’ refer to HSBC UK About us 3 Bank plc together with its subsidiaries. It contains the Strategic Report, the Report of the Directors, the Statement of Directors’ Our strategy 4 Responsibilities and Financial Statements, together with the How we do business 5 Independent Auditors’ Report, as required by the UK Companies Key performance indicators 9 Act 2006. References to ‘HSBC Group’ or ‘the Group’ within this Financial summary 10 document mean HSBC Holdings plc together with its subsidiaries. Risk overview 16 Report of the Directors HSBC UK is exempt from publishing information required by The Risk 17 Capital Requirements Country-by-Country Reporting Regulations Capital 52 2013, as this information is published by its ultimate parent, HSBC Corporate governance report 54 Holdings plc. This information will be available in June 2020 on the Disclosure of information to the auditors and Statement of Directors’ Group's website: www.hsbc.com. Responsibilities 60 Pillar 3 disclosures for HSBC UK are also available on Independent auditors’ Report 61 www.hsbc.com, under Investor Relations. Financial statements All narrative disclosures, tables and graphs within the Strategic Financial statements 70 Report and Report of the Directors are unaudited unless otherwise Notes on the financial statements 78 stated. Our reporting currency is £ sterling. Unless otherwise specified, all $ symbols represent US dollars.