View Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Download the Development Showcase Here

THE DEVELOPMENT SHOWCASE WELCOME ondon is one of the most popular capital in the past year, CBRE has continued global cities, home to over eight million to provide exceptional advice and innovative L residents from all over the world. The solutions to clients, housebuilders and English language, convenient time zone, developers, maintaining our strong track world-class education system, diverse culture record of matching buyers and tenants with and eclectic mix of lifestyles, make London their ideal homes. one of the most exciting places to call home and also the ideal place to invest in. Regeneration in London is on a scale like no other, with many previously neglected With four world heritage sites, eight spacious areas being transformed into thriving new royal parks and over 200 museums and communities and public realms, creating galleries, London acts as a cultural hub for jobs and economic growth. This large- both its residents and the 19 million visitors scale investment into regeneration and it receives every year. The London economy, placemaking is contributing to the exciting including financial services, life sciences and constant evolution of the capital that and many of the world’s best advisory we are witnessing and is a crucial reason as firms not only attract people from all over to why people are still choosing to invest in the world to study and work here, but also London real estate. London’s regeneration contribute towards the robust UK economy plan will be enhanced further when the that stands strong throughout uncertainty. It Elizabeth Line (previously Crossrail) will is no surprise that the property market has open in December, reducing journey times mirrored this resilience in the past few years. -

Annual Report 2007 Download PDF 504.15 KB

Delivering profitable growth Annual Report and Financial Statements 2007 CONTENTS PERFORMANCE “Galliford Try has had an excellent year. We have delivered significant profit growth across all our businesses, Highlights 01 our recent acquisitions are performing The Group 02 ahead of expectations, and we are Chairman’s Statement 03 confident that our strategy will continue Business Review 04 to deliver sustainable growth and Divisional Reviews 06 increased shareholder value.” Financial Results 11 Corporate Responsibility 14 Greg Fitzgerald Corporate and Social Responsibility Report 16 Chief Executive DIRECTORS AND GOVERNANCE Directors and Executive Board 20 Directors’ Report 22 Corporate Governance Report 24 Remuneration Report 28 FINANCIALS Independent Auditors’ Report – Group 34 Consolidated Income Statement 35 Consolidated Statement of Recognised Income and Expense 36 Consolidated Balance Sheet 37 Consolidated Cash Flow Statement 38 Notes to the Consolidated Financial Statements 39 Independent Auditors’ Report – Company 72 Company Balance Sheet 73 Notes to the Company Financial Statements 74 Five-Year Record 82 Contacts 83 Shareholder Information 84 HIGHLIGHTS For the year ended 30 June 2007 • Results ahead of expectations from Morrison Construction and REVENUE Chartdale Homes in the first full year following acquisition. +65% • Good performance from Linden Homes since acquisition; integration going well with synergies exceeding forecast. • Year end net debt of £99 million, representing gearing of 32 per cent, £1,410 m significantly better than expectations. • Current construction order book maintained at £2.1 billion. PROFIT BEFORE TAX • Record housebuilding completions of 1,526 units and landbank +75% of 11,200 plots. Encouraging sales during the summer period with current sales in hand of £323 million. -

Keep Calm and Carillion – the Company’S Pension Schemes Are More Secure Than They Look

Keep Calm and Carillion – The Company’s Pension Schemes Are More Secure than They Look Safeguarding the Carillion pension empire The company we came to know as Carillion was created in July 1999, following a demerger from Tarmac, through which it acquired a number of huge UK employers, including Mowlem and Alfred McAlpine. This gave the new company immediate responsibility for 13 defined benefit pension schemes. Almost two decades later, 27,500 people First Actuarial’s Catherine Lockyer continue to have benefits in schemes reliant on Carillion as sponsor, with close to half of sheds light on the doom and gloom these already receiving their pensions. surrounding Carillion’s pension schemes Commentators were not slow to point to The recent collapse of the construction and public problems with Carillion’s pension schemes. services contractor, Carillion plc, sent shockwaves The Guardian reported that MPs were through the British economy. accusing the company of trying to wriggle out of its pension obligations, for example. When the news broke in January, the future looked And The Economist asked whether pension uncertain for the company’s 20,000 UK employees. protection was still viable, referring to ‘a big And as industrialists took the measure of the hole’. All in all, the future of these schemes consequences for the country, other questions looked deeply uncertain, and this can only quickly emerged. have added to the anxieties of Carillion’s employees and pensioners. How would the Government deal with the huge infrastructure projects that Carillion had failed to The fantastic news, however, is that all of complete? Who would manage the maintenance Carillion’s pension scheme members have and service of hundreds of hospitals, schools and the security of the Pension Protection Fund homes? And as for the thousands of smaller (PPF). -

![J Jarvis & Sons Ltd V Blue Circle Dartford Estates Ltd [2007]](https://docslib.b-cdn.net/cover/2296/j-jarvis-sons-ltd-v-blue-circle-dartford-estates-ltd-2007-322296.webp)

J Jarvis & Sons Ltd V Blue Circle Dartford Estates Ltd [2007]

J Jarvis & Sons Ltd v Blue Circle Dartford Estates Ltd [2007] APP.L.R. 05/14 JUDGMENT : MR JUSTICE JACKSON: TCC. 14th May 2007 1. This judgment is in seven parts, namely, Part 1 "Introduction"; Part 2 "The Facts"; Part 3 "The Present Proceedings"; Part 4 "The Law"; Part 5 "The Application for an Injunction"; Part 6 "Jarvis's Challenges to the Interim Award"; and Part 7 "Conclusion". Part 1: Introduction 2. This is an action brought by a main contractor in order to prevent the continuance of an arbitration. The contractor seeks to achieve that result either by means of an injunction or, alternatively, by challenging an Interim Award of the Arbitrator. This litigation has been infused with some urgency because it was launched just fifteen days before the date fixed for the start of arbitration hearing. 3. J Jarvis & Sons Limited is claimant in these proceedings and defendant in the arbitration. Prior to 18th February 1997, the name of this company was J Jarvis & Sons plc. I shall refer to the company as "Jarvis". Jarvis is the subsidiary company of Jarvis plc. Blue Circle Dartford Estates Limited is defendant in these proceedings and claimant in the arbitration. I shall refer to this party as "Blue Circle". Blue Circle is a subsidiary company of Blue Circle Industries plc. The solicitors for the parties will feature occasionally in the narrative. Squire & Co are solicitors for Jarvis. Howrey LLP are solicitors for Blue Circle. 4. I turn now to other companies which will feature in the narrative of events. GEFCO (UK) Limited are forwarding agents. -

Minutes of Meeting

Minutes of Meeting VGB-Technical Committee: Generation and Technology VGB-Technical Group: PGMON Power Generation Maintenance Optimisation Netzwork 61st Meeting on 14 October 2020; Onlinemeeting Participants: Andrejkowic Milan CEZ Basus Martin CEZ Hoffmann Martin CEZ Krempasky Jakub CEZ Krickis Otto Latvenergo Le Bris Yves EDF Martin Conor ESB Meinke Sebastian Vattenfall Tereso Bruno EDP Wels Henk DNV GL Wolbers Patrick DNV GL VGB Secretariat: Göhring Sven VGB Agenda Welcome (Henk Wels) TOP 1: Use of parts from decommissioned coal-fired power plants Milan Andrejkovic, CEZ TOP 2: CCGT eHGPI Martin Hoffman, CEZ TOP 3: Siemens SGT-800 gas turbine’s upgrade process, related technical issues and preliminary results Otto Krickis, Latvenergo TOP 4: Diag Engine, a new monitoring solution for reciprocating engines Yves Le Bris, EDF TOP 5: RAM prediction for a district heating station consisting of aux boilers and a buffer Henk Wels, Dekra TOP 6: Ancillary Services Market: ESB CCGT Plant Flexibility Improvements Conor Martin, ESB TOP 7: Statistical analysis of VGB Forced Unavailability data on cycling CCGTs Henk Wels, Dekra TOP 8: The new VGB-Workspace Sven Göhring, VGB TOP 9: Place and date of next venue TOP 1: Use of parts from decommissioned coal-fired power plants Milan Andrejkovič & Martin Bašus, CEZ The introductory part of the presentation summarizes current information on CEZ Group's strategy and economic development in the Czech Republic in relation to the energy market, significantly affected by the Covid-19 pandemic. The history pf the power plant Prunerov 1 was presented. It was commissioned in 1967- 1968. The first reconstruction was taken in 1985-1988. -

Press Release

Press Release 1 October 2012 A contract worth around €410 million for Alstom Alstom awarded contract to supply and service equipment for new gas-fired power station at Carrington, United Kingdom Alstom Thermal Power will supply the electromechanical equipment for the new Carrington Power gas-fired power station, located near Manchester, United Kingdom, and will also be responsible for maintenance of this equipment. The contract has been signed in consortium with Duro Felguera, a Spanish company specialising in the execution of power plants, which will be in charge of the erection of the new power plant for Carrington Power Limited. The total contract value is approximately €640 million, with Alstom’s share being around €410 million. The contract is effective immediately and will be booked in the second quarter of the 2012/13 financial year. The 880 MW power plant will be built under an Engineering, Procurement and Construction (EPC) contract. Duro Felguera will be responsible for construction and site management. Alstom’s scope includes the supply of two GT26 gas turbines and other key components, including the steam turbine, heat recovery steam generator (HRSG) and turbogenerator. Additionally, Alstom has been awarded a long-term service agreement valid for 16 years to maintain this equipment once it enters commercial operation. Scheduled for completion in 2016, the power station will be capable of providing enough power for around a million homes. The station will be located on the site of the old Carrington power station in Trafford, next to the Manchester Shipping Canal and the River Mersey. Up to 600 people will be employed at the peak of construction. -

Industry Background

Appendix 2.2: Industry background Contents Page Introduction ................................................................................................................ 1 Evolution of major market participants ....................................................................... 1 The Six Large Energy Firms ....................................................................................... 3 Gas producers other than Centrica .......................................................................... 35 Mid-tier independent generator company profiles .................................................... 35 The mid-tier energy suppliers ................................................................................... 40 Introduction 1. This appendix contains information about the following participants in the energy market in Great Britain (GB): (a) The Six Large Energy Firms – Centrica, EDF Energy, E.ON, RWE, Scottish Power (Iberdrola), and SSE. (b) The mid-tier electricity generators – Drax, ENGIE (formerly GDF Suez), Intergen and ESB International. (c) The mid-tier energy suppliers – Co-operative (Co-op) Energy, First Utility, Ovo Energy and Utility Warehouse. Evolution of major market participants 2. Below is a chart showing the development of retail supply businesses of the Six Large Energy Firms: A2.2-1 Figure 1: Development of the UK retail supply businesses of the Six Large Energy Firms Pre-liberalisation Liberalisation 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 -

IL Combo Ndx V2

file IL COMBO v2 for PDF.doc updated 13-12-2006 THE INDUSTRIAL LOCOMOTIVE The Quarterly Journal of THE INDUSTRIAL LOCOMOTIVE SOCIETY COMBINED INDEX of Volumes 1 to 7 1976 – 1996 IL No.1 to No.79 PROVISIONAL EDITION www.industrial-loco.org.uk IL COMBO v2 for PDF.doc updated 13-12-2006 INTRODUCTION and ACKNOWLEDGEMENTS This “Combo Index” has been assembled by combining the contents of the separate indexes originally created, for each individual volume, over a period of almost 30 years by a number of different people each using different approaches and methods. The first three volume indexes were produced on typewriters, though subsequent issues were produced by computers, and happily digital files had been preserved for these apart from one section of one index. It has therefore been necessary to create digital versions of 3 original indexes using “Optical Character Recognition” (OCR), which has not proved easy due to the relatively poor print, and extremely small text (font) size, of some of the indexes in particular. Thus the OCR results have required extensive proof-reading. Very fortunately, a team of volunteers to assist in the project was recruited from the membership of the Society, and grateful thanks are undoubtedly due to the major players in this exercise – Paul Burkhalter, John Hill, John Hutchings, Frank Jux, John Maddox and Robin Simmonds – with a special thankyou to Russell Wear, current Editor of "IL" and Chairman of the Society, who has both helped and given encouragement to the project in a myraid of different ways. None of this would have been possible but for the efforts of those who compiled the original individual indexes – Frank Jux, Ian Lloyd, (the late) James Lowe, John Scotford, and John Wood – and to the volume index print preparers such as Roger Hateley, who set a new level of presentation which is standing the test of time. -

Modified UK National Implementation Measures for Phase III of the EU Emissions Trading System

Modified UK National Implementation Measures for Phase III of the EU Emissions Trading System As submitted to the European Commission in April 2012 following the first stage of their scrutiny process This document has been issued by the Department of Energy and Climate Change, together with the Devolved Administrations for Northern Ireland, Scotland and Wales. April 2012 UK’s National Implementation Measures submission – April 2012 Modified UK National Implementation Measures for Phase III of the EU Emissions Trading System As submitted to the European Commission in April 2012 following the first stage of their scrutiny process On 12 December 2011, the UK submitted to the European Commission the UK’s National Implementation Measures (NIMs), containing the preliminary levels of free allocation of allowances to installations under Phase III of the EU Emissions Trading System (2013-2020), in accordance with Article 11 of the revised ETS Directive (2009/29/EC). In response to queries raised by the European Commission during the first stage of their assessment of the UK’s NIMs, the UK has made a small number of modifications to its NIMs. This includes the introduction of preliminary levels of free allocation for four additional installations and amendments to the preliminary free allocation levels of seven installations that were included in the original NIMs submission. The operators of the installations affected have been informed directly of these changes. The allocations are not final at this stage as the Commission’s NIMs scrutiny process is ongoing. Only when all installation-level allocations for an EU Member State have been approved will that Member State’s NIMs and the preliminary levels of allocation be accepted. -

Completed Acquisition by Interserve Plc of the Facilities Management Business of Rentokil Initial Plc (Initial Facilities)

Completed acquisition by Interserve plc of the facilities management business of Rentokil Initial plc (Initial Facilities) ME/6432-14 The CMA’s decision on clearance under section 33(1) given on 29 May 2014. Full text of the decision published on 11 June 2014. Please note that the square brackets indicate figures or text which have been deleted or replaced in ranges at the request of the parties for reasons of commercial confidentiality. Summary 1. On 18 March 2014, Interserve plc (Interserve) acquired the facilities management (FM) business (Initial Facilities) of Rentokil Initial plc (Rentokil) through the purchase of a combination of shares and assets. The Competition and Markets Authority (CMA) considers that the parties have ceased to be distinct and that the turnover test in section 23(1)(b) of the Enterprise Act 2002 (the Act) is met. The CMA therefore believes that it is or may be the case that a relevant merger situation has been created. 2. The parties notified the completed merger to the Office of Fair Trading (OFT)1 on 31 March 2014. The administrative deadline for the CMA to make a decision on whether or not to refer the merger to a phase II investigation is 29 May 2014. 3. The parties overlapped in the provision of FM services in the UK. The CMA analysed the effects of the merger on the provision of FM services in the UK as a whole, and also taking into account the information received by it on how competition varies across certain segments and geographies. 1 The Competition and Markets Authority (CMA) was established on 1 October 2013. -

One Blackfriars Is Indicative Only

THE SOUTH CONTENTS � BANK London is a world-class city with an 06 RESTAURANTS unrivalled position as a business and financial centre, leading the way in arts 14 BARS and culture, architecture and heritage. 20 ARTS & CULTURE The capital has always embraced change and has celebrated its international connections 32 HEART OF THE SOUTH BANK through the centuries, shaping its global status 34 SHOPPING which was showcased in unforgettable style at The London 2012 Summer Olympics. 38 LUXURY HOTELS The South Bank is creating a new focus for the 44 EDUCATION capital. Southwark has a rich history and the presence of Guy’s and St Thomas’ teaching 46 TRANSPORT hospitals and the academic excellence of King’s College London have brought international 48 LOCAL BUSINESSES MAP recognition to the borough for the past 150 years. The cultural cluster of theatres, galleries, museums and The Shard have driven the latest transformation. First-class restaurants, bars and cafés are bringing a new vibrant nightlife to the district. Companies and businesses such as News Corporation are moving from Wapping; the FT is established next to Southwark Bridge; RBS, Lloyds and leading law firms such as Norton Rose and Lawrence Graham, plus accountancy practices PWC and Ernst & Young are all established on the South Bank. Computer generated image of One Blackfriars is indicative only. UNIQUE � DINING LOCAL GASTRONOMY The South Bank has become renowned for its exciting, BOROUGH MARKET OXO TOWER BRASSERIE ROAST cosmopolitan restaurants and bars, with numerous artisan and -

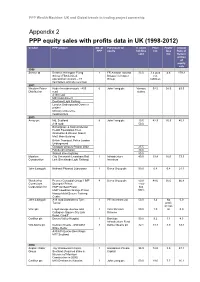

Appendix 2 PPP Equity Sales with Profits Data in UK (1998-2012)

PPP Wealth Machine: UK and Global trends in trading project ownership Appendix 2 PPP equity sales with profits data in UK (1998-2012) Vendor PPP project No. of Purchaser of % share Price Profit/ Annual PPP equity holding £m loss Rate of sold £m Return at time of equity sale 1998 Serco Ltd Defence Helicopter Flying 1 FR Aviation Ltd and 33.0 3.4 plus 4.6 179.3 School (FBS Limited, Bristow Helicopter net operational contract – 47 Group liabilities helicopters and site services) 2001 Western Power Hyder Investments plc - A55 6 John Laing plc Various 92.5 58.5 63.3 Distribution road stakes A130 road M40 road project Dockland Light Railway London Underground Connect project Ministry of Defence headquarters 2003 Amey plc M6, Scotland 8 John Laing plc 19.5 42.9 25.9 45.2 A19 road 50.0 Birmingham & Solihull Mental Health Foundation Trust (Erdington & Winson Green) MoD Main Building British Transport Police London Underground Glasgow schools-Project 2002 25.5 Edinburgh schools 30.0 Walsall street lighting 50.0 Mowlem City Greenwich Lewisham Rail 1 Infrastructure 40.0 19.4 16.0 73.3 Construction Link (Docklands Light Railway) Investors John Laing plc National Physical Laboratory 1 Serco Group plc 50.0 0.8 0.4 21.1 Wackenhut Premier Custodial Group: HMP 4 Serco Group plc 50.0 48.6 35.0 66.8 Corrections Dovegate Prison - now Corporation Inc HMP Ashfield Prison has HMP Lowdham Grange Prison 100% Hassockfield Secure Training Centre John Laing plc A19 road Dishforth to Tyne 1 PFI Investors Ltd 50.0 3.4 No 0.0 Tunnel profit or loss Vinci plc Lloyd George