Return of Private Foundation OMB No 1545-0052 Form 990 -PF Or Section 4947(A)(1) Nonexempt Charitable Trust ` Treated As a Private Foundation 2009 Note

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Fresh Perspective on the History of Hasidic Judaism

eSharp Issue 20: New Horizons A Fresh Perspective on the History of Hasidic Judaism Eva van Loenen (University of Southampton) Introduction In this article, I shall examine the history of Hasidic Judaism, a mystical,1 ultra-orthodox2 branch of Judaism, which values joyfully worshipping God’s presence in nature as highly as the strict observance of the laws of Torah3 and Talmud.4 In spite of being understudied, the history of Hasidic Judaism has divided historians until today. Indeed, Hasidic Jewish history is not one monolithic, clear-cut, straightforward chronicle. Rather, each scholar has created his own narrative and each one is as different as its author. While a brief introduction such as this cannot enter into all the myriad divergences and similarities between these stories, what I will attempt to do here is to incorporate and compare an array of different views in order to summarise the history of Hasidism and provide a more objective analysis, which has not yet been undertaken. Furthermore, my historical introduction in Hasidic Judaism will exemplify how mystical branches of mainstream religions might develop and shed light on an under-researched division of Judaism. The main focus of 1 Mystical movements strive for a personal experience of God or of his presence and values intuitive, spiritual insight or revelationary knowledge. The knowledge gained is generally ‘esoteric’ (‘within’ or hidden), leading to the term ‘esotericism’ as opposed to exoteric, based on the external reality which can be attested by anyone. 2 Ultra-orthodox Jews adhere most strictly to Jewish law as the holy word of God, delivered perfectly and completely to Moses on Mount Sinai. -

Stamford Hill.Pdf

This is an Accepted Manuscript of an article published by Taylor & Francis in Housing Studies on Volume 33, 2018. Schelling-Type Micro-Segregation in a Hassidic Enclave of Stamford-Hill Corresponding Author: Dr Shlomit Flint Ashery Email [email protected] Abstract This study examines how non-economic inter- and intra-group relationships are reflected in residential pattern, uses a mixed methods approach designed to overcome the principal weaknesses of existing data sources for understanding micro residential dynamics. Micro-macro qualitative and quantitative analysis of the infrastructure of residential dynamics offers a holistic understanding of urban spaces organised according to cultural codes. The case study, the Haredi community, is composed of sects, and residential preferences of the Haredi sect members are highly affected by the need to live among "friends" – other members of the same sect. Based on the independent residential records at the resolution of a single family and apartment that cover the period of 20 years the study examine residential dynamics in the Hassidic area of Stamford-Hill, reveal and analyse powerful Schelling-like mechanisms of residential segregation at the apartment, building and the near neighbourhood level. Taken together, these mechanisms are candidates for explaining the dynamics of residential segregation in the area during 1995-2015. Keywords Hassidic, Stamford-Hill, Segregation, Residential, London Acknowledgments This research was carried out under a Marie Curie Fellowship PIEF-GA-2012-328820 while based at Centre for Advanced Spatial Analysis (CASA) University College London (UCL). 1 1. Introduction The dynamics of social and ethnoreligious segregation, which form part of our urban landscape, are a central theme of housing studies. -

Mattos Chassidus on the Massei ~ Mattos Chassidus on the Parsha +

LIGHTS OF OUR RIGHTEOUS TZADDIKIM בעזרת ה ' יתבר A Tzaddik, or righteous person , makes everyone else appear righteous before Hashem by advocating for them and finding their merits. Kedushas Levi, Parshas Noach (Bereishis 7:1) MATTOS ~ MASSEI _ CHASSIDUS ON THE PARSHA + Dvar Torah – Mattos Keep Your Word The Torah states (30:3), “If a man takes a vow or swears an oath to G -d to establish a prohibition upon himself, he shall not violate his word; he shall fulfill whatever comes out of his mouth.” In relation to this passuk , the Midrash quotes from Tehillim (144:4), “Our days are like a fleeting shadow.” What is the connection? This can be explained, says Rav Levi Yitzchok, according to a Gemara ( Nedarim 10b), which states, “It is forbidden to say, ‘ Lashem korban , for G-d − an offering.’ Instead a person must say, ‘ Korban Lashem , an offering for G -d.’ Why? Because he may die before he says the word korban , and then he will have said the holy Name in vain.” In this light, we can understand the Midrash. The Torah states that a person makes “a vow to G-d.” This i s the exact language that must be used, mentioning the vow first. Why? Because “our days are like a fleeting shadow,” and there is always the possibility that he may die before he finishes his vow and he will have uttered the Name in vain. n Story The wood chopper had come to Ryczywohl from the nearby village in which he lived, hoping to find some kind of employment. -

Time to Dance” Proudly Brings You the Fourth Album in the Classic Series

עת רקוד • TIME TO DANCE 4 MARCHES, WALTZES AND HAKOFA NIGUNIM FROM THE SANZER AND BOBOVER DYNASTY Arranged and Conducted by Yisroel Lamm • Music by Neginah Orchestra Produced by Zalmen Leib Blau TIME TO DANCE — THE INNER SOUL OF CHASSIDIC MUSIC “Time to Dance” proudly brings you the fourth album in the classic series. As in the previous recordings, these are not well-known, popular tunes. Rather, these selections bring back the depth of feeling of a bygone era. They are as timely today as when they were originally composed by the Tzaddikim of Bobov, Sanz and Ropshitz. Sung at the Tischen and during the tefillos on Shabbos and Yom Tov, these nigunnim stir the listener’s soul to joy, to tears, and to strive for spiritual heights. The richness of tone, beautiful arrangement and symphonic sound are sure to please the most discriminat- ing ear, while pulling at the strings of the Jewish heart. Truly, this is a “Time to Dance” for us. This recording is being released in con- junction with the wedding of our dear children, ·Â ‰Á˘Â· ‰Ș¯ ‰Á˙Ô ‡·¯‰Ì ‡ÏÚʯ ¢È Ú·¢‚ ‰Îω ‰·˙Âω ‰Ó‰ÂÏω È¡ ˙ÁÈß È¡ ‰Ó‰ÂÏω ‰·˙Âω ‰Îω Ú·¢‚ ¢È ‡ÏÚʯ ‡·¯‰Ì ‰Á˙Ô Â‰È˜¯ ‰Á˘Â· ·Â ·˙ η„ ÓÁÂß ‰¯‰¢‚ ¯ß „„ ȇÓÙ‡ÏÒ˜È ˘ÏÈË¢‡ ȇÓÙ‡ÏÒ˜È „„ ¯ß ‰¯‰¢‚ ÓÁÂß Î·Â„ ·˙ Á˙Ô Î¢˜ ‡„Ó¢¯ ¯ß ˘ÏÓ‰ ÊÏÓÔ Ù¯ÈÚ„Ó‡Ô ÊˆÂ˜¢Ï ÓËÚ˜‡ ʈ˜¢Ï Ù¯ÈÚ„Ó‡Ô ÊÏÓÔ ˘ÏÓ‰ ¯ß ‡„Ó¢¯ ΢˜ Á˙Ô May the ‰ÂˆÓ Ï˘ ‰ÁÓ˘—together with the ‰ÁÓ˘ and inspiration provided by these recordings—bring the day closer when ‰„Â‰È È¯Ú· ÚÓ˘È „ÂÚ ‰ÏΠϘ Ô˙Á Ϙ ‰ÁÓ˘ Ϙ Ô¢˘ Ϙ ÌÈÏ˘Â¯È ˙ˆÂÁ·Â speedily in our days, ÔÓ‡Æ Â˙Èگ ‡ÈÂÏ· ·ÈÈÏ ÔÓÏÊ ¢ÈÂÓ‡ ‚ß Á˘ÂÔ¨ „ß ÏÒ„¯ Á¢ ÏÒ„¯ „ß Á˘ÂÔ¨ ‚ß ¢ÈÂÓ‡ Zalmen Leib Blau Ú˙ ¯˜Â„ Ú˙ ·‚Èß ÎÓÈÔ ÓÂÁ‰ ¢ÓÁ‰ ‡Â¯ Ïȉ„ÈÌ ‡Â¯ ¢ÓÁ‰ ÓÂÁ‰ ÎÓÈÔ • TIME TO DANCE 4 1. -

Form 990-PF ,, Return of Private Foundation

OMB No 1545-0052 Form 990-PF ,, Return of Private Foundation or Section 4947(a)(1) Nonexempt Charitable Trust Department of the Treasury Treated as a Private Foundation Intern al Revenue Serv ice Note: The organization may be able to use a copy of this return to satisfy state reporting rel 2004 For calendar year 2004 , or tax year beginning AUG 1, 2004 , and ending JUL 31 5 G Check all that apply 0 Initial return E:1 Final return Amended return Name of organization Use the IRS A Employer identification number label. Otherwise , HE FISHOFF FAMILY FOUNDATION 13-3076576 print Number and street (or P O box number if mail is not delivered to street add re ss) Room/suite B Telephone number ortype . 300 2C ROUTE 17 SOUTH 973-458-8070 See Specific City or town, state, and ZIP code C If exemption application Is pending , check here ► U Instructions OD I NJ 0 7 6 4 4 D 1. Foreign organizations, check here ► 2. Foreign organizations meeting the 85% test, ► H Check type of organization OX Section 501 (c)(3) exempt private foundation check here and attach computation Q Section 4947(a)(1) nonexempt charitable trust fl Other taxable private foundation E If private foundation status was terminated I Fair market value of all assets at end of year J Accounting method 0 Cash �X Accrual under section 507(b)(1)(A), check here ► 0 (from Part ll, col (c), line 16) 0 Other (specify) F If the foundation is in a 60-month terminat ion ► $ 7,183,307 . -

Form 990-PF Return of Private Foundation

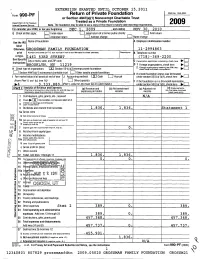

EXTENSION GRANTED UNTIL OCTOBER 15,2011 Return of Private Foundation OMB No 1545-0052 Form 990-PF a or Section 4947(a)(1) Nonexempt Charitable Trust Treated as a Private Foundation Department of the Treasury 2009 Internal Revenue Service Note. The foundation may be able to use a copy of this return to satisfy state reporting requirements. For calendar year 2009, or tax year beginning DEC 1, 200 9 , and ending NOV 30, 2010 G Check all that apply: Initial return 0 Initial return of a former public charity LJ Final return n Amended return n Address chance n Name chance of foundation A Employer identification number Use the IRS Name label Otherwise , ROSSMAN FAMILY FOUNDATION 11-2994863 print Number and street (or P O box number if mad is not delivered to street address) Room/suite B Telephone number ortype. 1461 53RD STREET ( 718 ) -369-2200 See Specific City or town, state, and ZIP code C If exem p tion app lication is p endin g , check here 10-E] Instructions 0 1 BROOKLYN , NY 11219 Foreign organizations, check here ► 2. Foreign aanizations meeting % test, H Check type of organization. ®Section 501(c)(3) exempt private foundation chec here nd att ch comp t atiooe5 Section 4947(a )( nonexem pt charitable trust 0 Other taxable private foundation 1 ) E If p rivate foundation status was terminated I Fair market value of all assets at end of year J Accounting method: ® Cash 0 Accrual under section 507(b)(1)(A), check here (from Part Il, co! (c), line 16) 0 Other (specify) F If the foundation is in a 60-month terminatio n $ 3 , 333 , 88 0 . -

Hasidic Judaism - Wikipedia, the Freevisited Encyclopedi Ona 1/6/2015 Page 1 of 19

Hasidic Judaism - Wikipedia, the freevisited encyclopedi ona 1/6/2015 Page 1 of 19 Hasidic Judaism From Wikipedia, the free encyclopedia Sephardic pronunciation: [ħasiˈdut]; Ashkenazic , תודיסח :Hasidic Judaism (from the Hebrew pronunciation: [χaˈsidus]), meaning "piety" (or "loving-kindness"), is a branch of Orthodox Judaism that promotes spirituality through the popularization and internalization of Jewish mysticism as the fundamental aspect of the faith. It was founded in 18th-century Eastern Europe by Rabbi Israel Baal Shem Tov as a reaction against overly legalistic Judaism. His example began the characteristic veneration of leadership in Hasidism as embodiments and intercessors of Divinity for the followers. [1] Contrary to this, Hasidic teachings cherished the sincerity and concealed holiness of the unlettered common folk, and their equality with the scholarly elite. The emphasis on the Immanent Divine presence in everything gave new value to prayer and deeds of kindness, alongside rabbinical supremacy of study, and replaced historical mystical (kabbalistic) and ethical (musar) asceticism and admonishment with Simcha, encouragement, and daily fervor.[2] Hasidism comprises part of contemporary Haredi Judaism, alongside the previous Talmudic Lithuanian-Yeshiva approach and the Sephardi and Mizrahi traditions. Its charismatic mysticism has inspired non-Orthodox Neo-Hasidic thinkers and influenced wider modern Jewish denominations, while its scholarly thought has interested contemporary academic study. Each Hasidic Jews praying in the Hasidic dynasty follows its own principles; thus, Hasidic Judaism is not one movement but a synagogue on Yom Kippur, by collection of separate groups with some commonality. There are approximately 30 larger Hasidic Maurycy Gottlieb groups, and several hundred smaller groups. Though there is no one version of Hasidism, individual Hasidic groups often share with each other underlying philosophy, worship practices, dress (borrowed from local cultures), and songs (borrowed from local cultures). -

Download Catalogue

F i n e Ju d a i C a . pr i n t e d bo o K s , ma n u s C r i p t s , au t o g r a p h Le t t e r s , gr a p h i C & Ce r e m o n i a L ar t K e s t e n b a u m & Co m p a n y We d n e s d a y , ma r C h 21s t , 2012 K e s t e n b a u m & Co m p a n y . Auctioneers of Rare Books, Manuscripts and Fine Art A Lot 275 Catalogue of F i n e Ju d a i C a . PRINTED BOOKS , MANUSCRI P TS , AUTOGRA P H LETTERS , GRA P HIC & CERE M ONIA L ART Featuring: Property from the Library of a New England Scholar ——— To be Offered for Sale by Auction, Wednesday, 21st March, 2012 at 3:00 pm precisely ——— Viewing Beforehand: Sunday, 18th March - 12:00 pm - 6:00 pm Monday, 19th March - 10:00 am - 6:00 pm Tuesday, 20th March - 10:00 am - 6:00 pm No Viewing on the Day of Sale This Sale may be referred to as: “Maymyo” Sale Number Fifty Four Illustrated Catalogues: $38 (US) * $45 (Overseas) KestenbauM & CoMpAny Auctioneers of Rare Books, Manuscripts and Fine Art . 242 West 30th street, 12th Floor, new york, NY 10001 • tel: 212 366-1197 • Fax: 212 366-1368 e-mail: [email protected] • World Wide Web site: www.Kestenbaum.net K e s t e n b a u m & Co m p a n y . -

Form 990-PF 2014

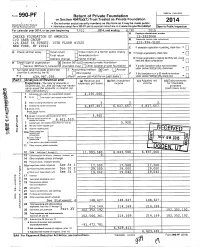

a -a OMB No 1545-0052 Form 990-PF Return of Private Foundation or Section 4947(a)(1) Trust Treated as Private Foundation 201 4 Do not enter social security numbers on this form as it may be made public. Department the ► of Treasury at www.irs.gov/form990pf. Internal Revenue Service ► Information about Form 990-PF and its separate instructions is to Public Inspection For calendar year 2014 , or tax year beginning 7/01 2014, and endin Employer identification number CHESED FOUNDATION OF AMERICA 13-3922068 C/O SABR GROUP Telephone number (see instructions) 126 EAST 56 STREET, 15TH FLOOR #1520 212-936-5100 NEW YORK, NY 10022 C If exemption application is pending, check here ► n public charity G Check all that apply Initial return Initial return of a former D 1 Foreign organizations , check here q Final return Amended return q Address change Name change 2 Foreign organizations meeting the 85% test, check here and attach com p utation H Check type of organization n Section 501 (c)(3) exempt private foundation Section 4947(a)(1) nonexemppl charitable trust Other taxable private foundation E If private foundation status was terminated q under section 507(b)(1)(A), check here I Fair market value of all assets at end of year J Accounting method Cash Accrual (from Part ll, column (c), line 16) q Other (specify) F If the foundation is in a 60-month termination q $ 439, 987, 095. (Part 1, column (d) must be on cash bas(s) under section 507(b)(1)(B), check here Part A na lysis O Revenue an d (a) Revenue and (b) Net investment (c) Adjusted net (d) Disbursements Expenses (The total of amounts in expenses per books income income for charitable columns (b), (c), and (d) may not neces- purposes sarily equal the amounts in column (a) (cash basis only) (see instructions) ) 1 Contribution^s' g1efts, grants , etc, received (attach schedule) 4 , 250 , 000. -

Succession in Contemporary Hasidism

1 Succession in Contemporary Hasidism Who Will Lead Us? ZADDIKIM OR REBBES When the modern Hasidic movement fi rst emerged in the late eight- eenth century, it was led mostly by charismatic men, commonly called zaddikim (loosely translated as the saintly or pious), who were them- selves the successors of ba’aley shem (wonder masters of the name of God or healers) and their counterparts, the maggidim (itinerant preach- ers).1 While the ba’aley shem were said to possess the mystical knowl- edge of Kabbalah that enabled them to invoke and in shaman-like fash- ion manipulate powerful, esoteric names of God in order to heal people, do battle with their demons, or liberate the human soul to unify itself with God, powers they used on behalf of those who believed in them, and while the maggidim were powerful preachers and magnetic orators who told tales and off ered parables or sermons that inspired their listen- ers, zaddikim had a combination of these qualities and more. With ba’aley shem they shared a knowledge of how to apply Kabbalah to the practical needs of their followers and to perform “miracles,” using their mystical powers ultimately to help their Hasidim (as these followers became known), and from the maggidim they took the power to inspire and attract with stories and teaching while inserting into these what their devotees took to be personal messages tailored just to them. With both, they shared the authority of charisma. Charisma, Max Weber explained, should be “applied to a certain quality of an individual personality by virtue of which he is set apart 1 HHeilmaneilman - WWhoho WillWill LeadLead Us.inddUs.indd 1 223/03/173/03/17 22:32:32 PPMM 2 | Succession in Contemporary Hasidism from ordinary men and treated as endowed with supernatural, superhu- man, or at least specifi cally exceptional powers or qualities.” 2 Whether the supernatural was an essential aspect of early Hasidism has been debated, but what is almost universally accepted is the idea that the men who became its leaders were viewed by their followers as extraordinary and exceptional. -

Tzadik Righteous One", Pl

Tzadik righteous one", pl. tzadikim [tsadi" , צדיק :Tzadik/Zadik/Sadiq [tsaˈdik] (Hebrew ,ṣadiqim) is a title in Judaism given to people considered righteous צדיקים [kimˈ such as Biblical figures and later spiritual masters. The root of the word ṣadiq, is ṣ-d- tzedek), which means "justice" or "righteousness". The feminine term for a צדק) q righteous person is tzadeikes/tzaddeket. Tzadik is also the root of the word tzedakah ('charity', literally 'righteousness'). The term tzadik "righteous", and its associated meanings, developed in Rabbinic thought from its Talmudic contrast with hasid ("pious" honorific), to its exploration in Ethical literature, and its esoteric spiritualisation in Kabbalah. Since the late 17th century, in Hasidic Judaism, the institution of the mystical tzadik as a divine channel assumed central importance, combining popularization of (hands- on) Jewish mysticism with social movement for the first time.[1] Adapting former Kabbalistic theosophical terminology, Hasidic thought internalised mystical Joseph interprets Pharaoh's Dream experience, emphasising deveikut attachment to its Rebbe leadership, who embody (Genesis 41:15–41). Of the Biblical and channel the Divine flow of blessing to the world.[2] figures in Judaism, Yosef is customarily called the Tzadik. Where the Patriarchs lived supernally as shepherds, the quality of righteousness contrasts most in Contents Joseph's holiness amidst foreign worldliness. In Kabbalah, Joseph Etymology embodies the Sephirah of Yesod, The nature of the Tzadik the lower descending -

Orm'99o-PF 2006

Return of Private Foundation OMB No 1545-0052 - orm'99O-PF or Section 4947 (a)(1) Nonexempt Charitable Trust Department of the Treasury Treated as a Private Foundation Internal Revenue Service Dn may be able to use a copy of this return to satisfy state rec 2006 For calendar year 2006 , or tax year beg innin g 11 / 01 , 2006 , and ending 10/31 / 2007 G Check all that app ly Initial return Final return Amended return Address change Name change Name of foundation A Employer identification number Use the IRS label. SSM FOUNDATION , INC. 06-1691147 Otherwise , Number and street (or P 0 box number if mail is not delivered to street address) Room/suite B Telephone number (see page 11 of print the instructions) or type. C/O MILLER, ELLIN COMPANY, LLP See Specific 750 LEXINGTON AVENUE - City or town, state, and ZIP code C If exemption application is Instructions . pending , check here . D I Foreign organizations, check here NEW YORK , NY 10022 2 Foreign organizations meeting the check here and attach H Check type of organization X Section 501 ( c 3 exempt private foundation co mp u ta tion I^ El Section 4947 ( a )( 1 ) nonexem pt charitable trust Other taxable p rivate foundation E If private foundation status was terminated I Fair market value of all assets at end J Accounting method Cash L_J Accrual X under section 507(b)(1)(A), check here . El of year (from Part ll, col (c), line El Other (specify) - - - - - - - - - - - - - - - - -- F If t h e f oun d ation is in a 60-month termination 16)10- $ (Part 1, column (d) must be on cash bas(s ) under section 507(b)( 1)(B), check here , 11111.