The Swiss Tax System –– Main Features of the Swiss Tax System

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Alarmierung Der Feuerwehren in Den Kantonen St.Gallen, Ap- Penzell Ausser- Rhoden Und Ap- Penzell Inner- Rhoden

Verteilt an Kommandos Alarmierung der Feuerwehren in den Kantonen St.Gallen, Ap- penzell Ausser- rhoden und Ap- penzell Inner- rhoden Analyse und Entscheid Bischof Daniel / AFS Pierre River / AAR Amt für Feuerschutz des Kantons St.Gallen Inhaltsverzeichnis Inhaltsverzeichnis ....................................................................................................................... 1 1 Management Summary ........................................................................................................ 3 1.1 Empfehlung zur Umsetzung / Ziellösung ............................................................................... 3 1.2 Abgrenzung ............................................................................................................................ 3 1.3 Betroffene Organisationen ..................................................................................................... 3 1.4 Ausgangslage Kanton St.Gallen ............................................................................................ 3 1.5 Ausgangslage der Kantone Appenzell Innerrhoden und Ausserrhoden ............................... 4 1.6 Gesetzliche Vorgaben ............................................................................................................ 4 1.6.1 Kanton St. Gallen ............................................................................................................... 4 1.6.2 Kanton Appenzell Ausserrhoden ........................................................................................ 4 1.6.3 -

A Tale of Minorities: Evidence on Religious Ethics and Entrepreneurship from Swiss Census Data

IZA DP No. 7976 A Tale of Minorities: Evidence on Religious Ethics and Entrepreneurship from Swiss Census Data Luca Nunziata Lorenzo Rocco February 2014 DISCUSSION PAPER SERIES Forschungsinstitut zur Zukunft der Arbeit Institute for the Study of Labor A Tale of Minorities: Evidence on Religious Ethics and Entrepreneurship from Swiss Census Data Luca Nunziata University of Padua and IZA Lorenzo Rocco University of Padua Discussion Paper No. 7976 February 2014 IZA P.O. Box 7240 53072 Bonn Germany Phone: +49-228-3894-0 Fax: +49-228-3894-180 E-mail: [email protected] Any opinions expressed here are those of the author(s) and not those of IZA. Research published in this series may include views on policy, but the institute itself takes no institutional policy positions. The IZA research network is committed to the IZA Guiding Principles of Research Integrity. The Institute for the Study of Labor (IZA) in Bonn is a local and virtual international research center and a place of communication between science, politics and business. IZA is an independent nonprofit organization supported by Deutsche Post Foundation. The center is associated with the University of Bonn and offers a stimulating research environment through its international network, workshops and conferences, data service, project support, research visits and doctoral program. IZA engages in (i) original and internationally competitive research in all fields of labor economics, (ii) development of policy concepts, and (iii) dissemination of research results and concepts to the interested public. IZA Discussion Papers often represent preliminary work and are circulated to encourage discussion. Citation of such a paper should account for its provisional character. -

Guide to the Canton of Lucerne

Languages: Albanian, Arabic, Bosnian / Serbian / Croatian, English, French, German, Italian, Polish, Portuguese, Spanish, Tamil, Tigrinya Sprache: Englisch Acknowledgements Edition: 2019 Publisher: Kanton Luzern Dienststelle Soziales und Gesellschaft Design: Rosenstar GmbH Copies printed: 1,800 Available from Guide to the Canton of Lucerne. Health – Social Services – Workplace: Dienststelle Soziales und Gesellschaft (DISG) Rösslimattstrasse 37 Postfach 3439 6002 Luzern 041 228 68 78 [email protected] www.disg.lu.ch › Publikationen Health Guide to Switzerland: www.migesplus.ch › Health information BBL, Vertrieb Bundes- publikationen 3003 Bern www.bundespublikationen. admin.ch Gesundheits- und Sozialdepartement Guide to the Canton of Lucerne Health Social Services Workplace Dienststelle Soziales und Gesellschaft disg.lu.ch Welcome to the Canton Advisory services of Lucerne An advisory service provides counsel- The «Guide to the Canton of Lucerne. ling from an expert; using such a Health – Social Services – Workplace» service is completely voluntary. These gives you information about cantonal services provide information and and regional services, health and support if you have questions that need social services, as well as information answers, problems to solve or obliga- on topics related to work and social tions to fulfil. security. For detailed information, please consult the relevant websites. If you require assistance or advice, please contact the appropriate agency directly. Some of the services described in this guide may have changed since publication. The guide does not claim to be complete. Further information about health services provided throughout Switzerland can be found in the «Health Guide to Switzerland». The «Guide to the Canton of Lucerne. Health – Social Services – Work- place» is closely linked to the «Health Guide to Switzerland» and you may find it helpful to cross-reference both guides. -

Route for Undergrounding the High- Voltage Transmission Line Between Mettlen and Samstagern

Zug Cantonal Building Authority, Spatial Planning Office Route for undergrounding the high- voltage transmission line between Mettlen and Samstagern 25.09.2021 Page 1 Route for undergrounding the high-voltage transmission line between Mettlen and Samstagern Client Facts Zug Cantonal Building Authority, Spatial Period 2015 - 2016 Planning Office Project Country Switzerland Perimeter length 28 kilometers Perimeter width 8 kilometers Examined 29 routing proposals The Canton of Zug would like to retain a long-term option for undergrounding a high-voltage (380/220kV), cross-cantonal transmission line. A specific route for the line is to be entered into the Zug Cantonal Development Plan so as to secure a long- term option on the project’s realization and to prevent any development that would prevent the project’s realization. The high-voltage (380/220kV) overhead transmission line that runs between the substations in Mettlen (Lucerne) and Benken/Grynau (St. Gallen) is a part of the Swiss national and European transmission grid. The transmission line passes through and depreciates residential areas in the Canton of Zug and also compromises the attractiveness of the landscape. In fact, landscapes that have been entered in the Swiss Federal Inventory of Landscapes and Natural Monuments (BLN) are affected to a considerable degree. The Canton of Zug is therefore determined to underground the transmission line as soon as the opportunity presents itself. Feasibility study to determine the best transmission route Working together with Axpo Netze AG, EBP has carried out a feasibility study to determine the most suitable transmission route for the project. The study’s aim was to identify and ascertain the technical, operational and zoning feasibility of possible routes for the transmission line, while ensuring environmental compatibility. -

Selected Information

Selected information SNB 120 Selected information 2002 1 Supervisory and executive bodies (as of 1 January 2003) Hansueli Raggenbass, Kesswil, National Councillor, Attorney-at-law, President Bank Council Philippe Pidoux, Lausanne, Attorney-at-law, Vice President (Term of office 1999–2003) Kurt Amsler, Neuhausen am Rheinfall, President of the Verband Schweizerischer Kantonalbanken (association of Swiss cantonal banks) The members elected by Käthi Bangerter, Aarberg, National Councillor, Chairwoman of the Board of Bangerter- the Annual General Meeting of Shareholders are marked Microtechnik AG with an asterisk (*). * Fritz Blaser, Reinach, Chairman of Schweizerischer Arbeitgeberverband (Swiss employers’ association) Pierre Darier, Cologny, partner of Lombard Odier Darier Hentsch & Cie, Banquiers Privés * Hugo Fasel, St Ursen, National Councillor, Chairman of Travail.Suisse Laurent Favarger, Develier, Director of Four électrique Delémont SA Ueli Forster, St Gallen, Chairman of the Swiss Business Federation (economiesuisse), Chairman of the Board of Forster Rohner Ltd * Hansjörg Frei, Mönchaltorf, Chairman of the Swiss Insurance Association (SIA), member of the extended Executive Board of Credit Suisse Financial Services * Brigitta M. Gadient, Chur, National Councillor, partner in a consulting firm for legal, organisational and strategy issues Serge Gaillard, Bolligen, Executive Secretary of the Swiss federation of trade unions Peter Galliker, Altishofen, entrepreneur, President of the Luzerner Kantonalbank Marion Gétaz, Cully, Member of the -

Canton of Basel-Stadt

Canton of Basel-Stadt Welcome. VARIED CITY OF THE ARTS Basel’s innumerable historical buildings form a picturesque setting for its vibrant cultural scene, which is surprisingly rich for THRIVING BUSINESS LOCATION CENTRE OF EUROPE, TRINATIONAL such a small canton: around 40 museums, AND COSMOPOLITAN some of them world-renowned, such as the Basel is Switzerland’s most dynamic busi- Fondation Beyeler and the Kunstmuseum ness centre. The city built its success on There is a point in Basel, in the Swiss Rhine Basel, the Theater Basel, where opera, the global achievements of its pharmaceut- Ports, where the borders of Switzerland, drama and ballet are performed, as well as ical and chemical companies. Roche, No- France and Germany meet. Basel works 25 smaller theatres, a musical stage, and vartis, Syngenta, Lonza Group, Clariant and closely together with its neighbours Ger- countless galleries and cinemas. The city others have raised Basel’s profile around many and France in the fields of educa- ranks with the European elite in the field of the world. Thanks to the extensive logis- tion, culture, transport and the environment. fine arts, and hosts the world’s leading con- tics know-how that has been established Residents of Basel enjoy the superb recre- temporary art fair, Art Basel. In addition to over the centuries, a number of leading in- ational opportunities in French Alsace as its prominent classical orchestras and over ternational logistics service providers are well as in Germany’s Black Forest. And the 1000 concerts per year, numerous high- also based here. Basel is a successful ex- trinational EuroAirport Basel-Mulhouse- profile events make Basel a veritable city hibition and congress city, profiting from an Freiburg is a key transport hub, linking the of the arts. -

Swiss Economy Cantonal Competitiveness Indicator 2019: Update Following the Swiss Tax Reform (STAF)

Swiss economy Cantonal Competitiveness Indicator 2019: Update following the Swiss tax reform (STAF) Chief Investment Office GWM | 23 May 2019 3:12 pm BST | Translation: 23 May 2019 Katharina Hofer, Economist, [email protected]; Matthias Holzhey, Economist, [email protected]; Maciej Skoczek, CFA, CAIA, Economist, [email protected] Cantonal Competitiveness Indicator 2019 Following the adoption of the tax reform (STAF) on 19 • 1 ZG 0 = rank change versus previous year 100.0 May 2019, the canton of Zug remains the most competitive 2 BS +1 90.6 canton, as in 2018. Basel-Stadt has overtaken the canton of 3 ZH - 1 90.1 Zurich. 4 VD +3 75.2 5 AG - 1 74.3 • The cantons of Appenzell Innerrhoden and Glarus boast the 6 NW +2 72.4 most attractive cost environments. The canton of Bern has 7 SZ - 2 71.3 lost some of its tax appeal. 8 LU - 2 71.2 9 BL 0 71.1 • The tax reform burdens cantons' finances to different 10 GE +1 69.8 extents. In the near term, the cantons of Geneva and Basel- 11 TG - 1 66.7 Stadt are likely to lose revenue from profit tax. 12 SH 0 66.1 13 FR +1 62.9 14 SG - 1 62.8 Following the approval of tax reforms (STAF) in a recent referendum, 15 OW +3 58.6 cantons now need to make changes to their profits taxes. Although 16 AR +1 57.3 some cantons announced considerable cuts to profit taxes prior to 17 SO - 1 55.8 18 GL +4 55.5 the voting, others were more reluctant. -

Clarity on Swiss Taxes 2019

Clarity on Swiss Taxes Playing to natural strengths 4 16 Corporate taxation Individual taxation Clarity on Swiss Taxes EDITORIAL Welcome Switzerland remains competitive on the global tax stage according to KPMG’s “Swiss Tax Report 2019”. This annual study analyzes corporate and individual tax rates in Switzerland and internationally, analyzing data to draw comparisons between locations. After a long and drawn-out reform process, the Swiss Federal Act on Tax Reform and AHV Financing (TRAF) is reaching the final stages of maturity. Some cantons have already responded by adjusting their corporate tax rates, and others are sure to follow in 2019 and 2020. These steps towards lower tax rates confirm that the Swiss cantons are committed to competitive taxation. This will be welcomed by companies as they seek stability amid the turbulence of global protectionist trends, like tariffs, Brexit and digital service tax. It’s not just in Switzerland that tax laws are being revised. The national reforms of recent years are part of a global shift towards international harmonization but also increased legislation. For tax departments, these regulatory developments mean increased pressure. Their challenge is to safeguard compliance, while also managing the risk of double or over-taxation. In our fast-paced world, data-driven technology and digital enablers will play an increasingly important role in achieving these aims. Peter Uebelhart Head of Tax & Legal, KPMG Switzerland Going forward, it’s important that Switzerland continues to play to its natural strengths to remain an attractive business location and global trading partner. That means creating certainty by finalizing the corporate tax reform, building further on its network of FTAs, delivering its “open for business” message and pressing ahead with the Digital Switzerland strategy. -

Green Bond Fact Sheet

Green Bond Fact Sheet Canton of Basel Stadt Date: 01-Oct-2018 Issue date: 24-Sept-2018 Maturity date: 24-Sept-2025 Tenor: 7 Issuer Name Canton of Basel Stadt Amount Issued CHF0.23m (USD0.24m) Country of risk Switzerland CBI Database Included Issuer Type1 Local Government Bond Type Senior unsecured Green Bond Framework Link to Framework Second party opinion ISS-Oekom Certification Standard Not certified Assurance report N/A Certification Verifier N/A Green bond rating N/A Use of Proceeds ☐ Energy ☐ Solar ☐ Tidal ☐ Energy storage ☐ Onshore wind ☐ Biofuels ☐ Energy performance ☐ Offshore wind ☐ Bioenergy ☐ Infrastructure ☐ Geothermal ☐ District heating ☐ Industry: components ☐ Hydro ☐ Electricity grid ☐ Adaptation & resilience ☒ Buildings ☐ Certified Buildings ☐ Water performance ☐ Industry: components ☐ HVAC systems ☐ Energy storage/meters ☐ Adaptation & resilience ☒ Energy ☒ Other energy related performance ☐ Transport ☐ Electric vehicles ☐ Freight rolling stock ☐ Transport logistics ☐ Low emission ☐ Coach / public bus ☐ Infrastructure vehicles ☐ Bicycle infrastructure ☐ Industry: components ☐ Bus rapid transit ☐ Energy performance ☐ Adaptation & resilience ☐ Passenger trains ☐ Urban rail ☐ Water & wastewater ☐ Water distribution ☐ Storm water mgmt ☐ Infrastructure ☐ Water treatment ☐ Desalinisation plants ☐ Industry: components ☐ Wastewater ☐ Erosion control ☐ Adaptation & resilience treatment ☐ Energy performance ☐ Water storage ☐ Waste management ☐ Recycling ☐ Landfill, energy capture ☐ Waste to energy ☐ Waste prevention ☐ Energy performance -

Swiss Single Market Law and Its Enforcement

Swiss Single Market Law and its Enforcement PRESENTATION @ EU DELEGATION FOR SWITZERLAND NICOLAS DIEBOLD PROFESSOR OF ECONOMIC LAW 28 FEBRUARY 2017 overview 4 enforcement by ComCo 3 single market act . administrative federalism . principle of origin . monopolies 2 swiss federalism 1 historical background 28 February 2017 Swiss Single Market Law and its Enforcement Prof. Nicolas Diebold 2 historical background EEA «No» in December 1992 strengthening the securing market competitiveness of access the swiss economy 28 February 2017 Swiss Single Market Law and its Enforcement Prof. Nicolas Diebold 3 historical background market access competitiveness «renewal of swiss market economy» § Bilateral Agreements I+II § Act on Cartels § Autonomous Adaptation § Swiss Single Market Act § Act on TBT § Public Procurement Acts 28 February 2017 Swiss Single Market Law and its Enforcement Prof. Nicolas Diebold 4 swiss federalism 26 cantons 2’294 communities By Tschubby - Own work, CC BY-SA 3.0, https://commons.wikimedia.org/w/index.php?curid=12421401 https://upload.wikimedia.org/wikipedia/commons/3/3e/Schweizer_Gemeinden.gif 28 February 2017 Swiss Single Market Law and its Enforcement Prof. Nicolas Diebold 5 swiss federalism – regulatory levels products insurance banking medical services energy mountaineering legal services https://pixabay.com/de/schweiz-alpen-karte-flagge-kontur-1500642/ chimney sweeping nursing notary construction security childcare funeral gastronomy handcraft taxi sanitation 28 February 2017 Swiss Single Market Law and its Enforcement Prof. Nicolas Diebold 6 swiss federalism – trade obstacles cantonal monopolies cantonal regulations procedures & fees economic use of public domain «administrative federalism» public public services procurement subsidies 28 February 2017 Swiss Single Market Law and its Enforcement Prof. -

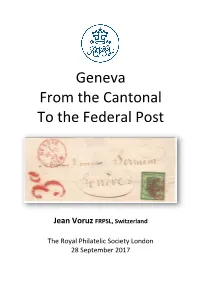

Geneva from the Cantonal to the Federal Post

Geneva From the Cantonal To the Federal Post Jean Voruz FRPSL, Switzerland The Royal Philatelic Society London 28 September 2017 Front cover illustration On 1 st October 1849, the cantonal posts are reorganized and the federal post is created. The Geneva cantonal stamps are still valid, but the rate for local letters is increased from 5 to 7 cents. As the "Large Eagle" with a face value of 5c is sold at the promotional price of 4c, additional 3c is required, materialized here by the old newspapers stamp. One of the two covers being known dated on the First Day of the establishment of the Federal Service. 2 Contents Frames 1 - 2 Cantonal Post Local Mail Frame 2 Cantonal Post Distant Mail Frame 3 Cantonal Post Sardinian & French Mail Frame 4 Transition Period Nearest Cent Frames 4 - 6 Transition Period Other Phases Frame 7 Federal Post Local Mail Frame 8 Federal Post Distant Mail Frames 9 - 10 Federal Post Sardinian & French Mail Background Although I started collecting stamps in 1967 like most of my classmates, I really entered the structured philately in 2005. That year I decided to display a few sheets of Genevan covers at the local philatelic society I joined one year before. Supported by my new friends - especially Henri Grand FRPSL who was one of the very best specialists of Geneva - I went further and got my first FIP Large Gold medal at London 2010 for the postal history collection "Geneva Postal Services". Since then the collection received the FIP Grand Prix International at Philakorea 2014 and the FEPA Grand Prix Finlandia 2017. -

631.230.1 Interkantonale Vereinbarung Über Die Hochschule Für Heilpädagogik Zürich 1

631.230.1 Interkantonale Vereinbarung über die Hochschule für Heilpädagogik Zürich 1 (Vom 21. September 1999) Die Kantone Zürich, Schwyz, Obwalden, Glarus, Zug, Solothurn, Schaffhausen, Appenzell Ausserrhoden, Appenzell Innerrhoden, St. Gallen, Graubünden, Aar- gau und Thurgau vereinbaren: I. Allgemeine Bestimmungen § 1 Träger 1 Die Kantone Zürich, Schwyz, Obwalden, Glarus, Zug, Solothurn, Schaffhausen, Appenzell Ausserrhoden, Appenzell Innerrhoden, St. Gallen, Graubünden, Aar- gau und Thurgau errichten und führen gemeinsam eine Hochschule für Heilpä- dagogik (Heilpädagogische Hochschule HfH, nachfolgend Hochschule). 2 Das Fürstentum Liechtenstein kann der Vereinbarung mit den gleichen Rech- ten und Pflichten wie die eines Trägerkantons beitreten. § 2 Rechtsnatur und Sitz 1 Die Hochschule ist eine öffentlich-rechtliche Anstalt mit eigener Rechtsper- sönlichkeit und mit dem Recht auf Selbstverwaltung. 2 Sitz der Hochschule ist Zürich. § 3 Aufgabe der Hochschule 1 Die Hochschule dient der Aus- und Weiterbildung von heilpädagogischen Lehr- kräften und von pädagogisch-therapeutischem Fachpersonal. 2 Die Hochschule betreibt in ihrem Tätigkeitsgebiet anwendungorientierte For- schungs- und Entwicklungsarbeit und erbringt für Dritte Dienstleistungen. 3 Die Tätigkeit der Hochschule richtet sich, soweit erforderlich, nach den Vor- schriften des Bundes, interkantonaler Vereinbarungen und gegebenenfalls der Trägerkantone über die Anerkennung der von der Hochschule erteilten Ausweise und Diplome. 4 Die Hochschule nimmt auf die Bedürfnisse behinderter Studierender Rück- sicht. § 4 Freiheit von Lehre und Forschung Die Freiheit von Lehre und Forschung ist im Rahmen der Ausbildungsziele der Hochschule gewährleistet. SRSZ 1.1.2015 1 631.230.1 § 5 Studienrichtungen 1. Ausbildungsstufe und –bereiche 1 Die Hochschule bildet im Rahmen von Aus- und Weiterbildung und unter Berücksichtigung der berufs-, fach- und funktionsspezifischen Bedürfnisse in folgenden Bereichen aus: 1.