Apple Value Chain Analysis and Market Assessment for Uttarkashi District Uttarakhand

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Sites & Names of Site Incharge for The

LIST OF SITES & NAMES OF SITE INCHARGE FOR THE PLANTATION CAMPAIGN MONITORING SYSTEM Sl No Circle Division Forest Range Name Phone Name of the Sites 1 Mandi Karsog Seri sagar 9560453757 Shamlat Haler Sh. Ranjeet 2 Shimla Theog Balson 8091350003 U-371 Chamble,U-366 Khanar,U-401 Khar,U-370 Kargoli Singh Sh. 3 Shimla Theog Kotkhai Ghanshyam 7018556195 UPF-479 Khola,UPF 456 Badruni Singh 4 Shimla Theog Theog Sh. Hari Saran 9418455366 D-126 Guthan Sh. Narender 5 Shimla Chopal Tharoach Singh, Dy. 8894537991 Birda DPF Ranger Sh. Parma 6 Shimla Chopal Nerwa 9805161004 Obta UPF Nand Sh. Mahender 7 Shimla Chopal Kanda 9816601060 Malnoon DPF Singh Sh. Ashwani 8 Shimla Chopal Bamta 7807503756 Momvi UPF Kumar Miss. Sapna 9 Shimla Chopal Sarain 9805198318 Nora-thalan DPF Verma, Fgd 10 Shimla Rohru Bashla Sh. Sunil Dutt 9418469089 UPF-8 Bashuni Sarswati Sh. Yashwant 11 Shimla Rohru 9816364369 C. No. 14 Chhajpur Nagar Singh C No. 2,C No. 5,C No. 10,C No. 40,C No. 12,C No. 16(b),C No. Urban Chaura Sh. Bahadur 12 Shimla 7018582415 37,C No. 16(c),C No. 36,C No. 19,C No. 34,C No. 21,C No. 31,C Division Maidan Singh No. 24,C No. 30,C No. 25,C No. 26,C No. 29,C No. 28 13 Hamirpur Una Bharwain Piar Singh FR 9418177107 R-II Lohara AC-4 Ashok Kumar 14 Hamirpur Una Amb 9418137656 R-III-Dharuhi-DC-1,Shamlat Haler FR Rajesh Kumar 15 Hamirpur Una Una 9418156944 SL Kotla Kalan,SL Badhera,SL Barnoh FR Ajeet Singh 16 Hamirpur Una Bangana 9816112244 U.P.F. -

Pneumonic Plague, Northern India, 2002

LETTERS compare the results of seroepidemio- Pneumonic Plague, and hemoptysis. A total of 16 cases logic investigations among cats living were reported from 3 hospitals in the in sites contaminated by avian viruses. Northern India, area: a local civil hospital, the state 2002 medical college, and a regional terti- This work was supported by the ary care hospital. Clinical material University of Milan grant F.I.R.S.T. To the Editor: A small outbreak collected from the case-patients and of primary pneumonic plague took their contacts was initially processed Saverio Paltrinieri,* place in the Shimla District of in the laboratories of these hospitals. Valentina Spagnolo,* Himachal Pradesh State in northern Wayson staining provided immediate Alessia Giordano,* India during February 2002. Sixteen presumptive diagnosis, and confirma- Ana Moreno Martin,† cases of plague were reported with a tory tests were performed at NICD. and Andrea Luppi† case-fatality rate of 25% (4/16). The Diagnosis of plague was confirmed infection was confirmed to the molec- *University of Milan, Milan, Italy; and for 10 (63%) of 16 patients (1). †Istituto Zooprofilattico Sperimentale della ular level with PCR and gene NICD conducted the following Lombardia e dell’Emilia, Brescia, Italy sequencing (1). A previous outbreak laboratory tests on 2 suspected culture in this region during 1983 was sug- References isolates, 2 sputum specimens, 1 lung gestive of pneumonic plague (22 autopsy material specimen, and 1 lung 1. Hopp M. Germany: H5N1 in domestic cats. cases, 17 deaths) but was not con- lavage sample (Table): 1) direct fluo- ProMed. 2006 Mar 1. [cited 2006 Mar 1]. -

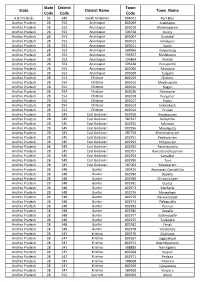

State State Code District Code District Name Town Code Town Name

State District Town State District Name Town Name Code Code Code A & N Islands 35 640 South Andaman 804041 Port Blair Andhra Pradesh 28 553 Anantapur 803009 Anantapur Andhra Pradesh 28 553 Anantapur 803010 Dharmavaram Andhra Pradesh 28 553 Anantapur 594760 Gooty Andhra Pradesh 28 553 Anantapur 803007 Guntakal Andhra Pradesh 28 553 Anantapur 803012 Hindupur Andhra Pradesh 28 553 Anantapur 803011 Kadiri Andhra Pradesh 28 553 Anantapur 594956 Kalyandurg Andhra Pradesh 28 553 Anantapur 595357 Madakasira Andhra Pradesh 28 553 Anantapur 594864 Pamidi Andhra Pradesh 28 553 Anantapur 595448 Puttaparthi Andhra Pradesh 28 553 Anantapur 803006 Rayadurg Andhra Pradesh 28 553 Anantapur 803008 Tadpatri Andhra Pradesh 28 554 Chittoor 803019 Chittoor Andhra Pradesh 28 554 Chittoor 803015 Madanapalle Andhra Pradesh 28 554 Chittoor 803016 Nagari Andhra Pradesh 28 554 Chittoor 803020 Palamaner Andhra Pradesh 28 554 Chittoor 803018 Punganur Andhra Pradesh 28 554 Chittoor 803017 Puttur Andhra Pradesh 28 554 Chittoor 803013 Srikalahasti Andhra Pradesh 28 554 Chittoor 803014 Tirupati Andhra Pradesh 28 545 East Godavari 802958 Amalapuram Andhra Pradesh 28 545 East Godavari 587337 Gollaprolu Andhra Pradesh 28 545 East Godavari 802955 Kakinada Andhra Pradesh 28 545 East Godavari 802956 Mandapeta Andhra Pradesh 28 545 East Godavari 587758 Mummidivaram Andhra Pradesh 28 545 East Godavari 802951 Peddapuram Andhra Pradesh 28 545 East Godavari 802954 Pithapuram Andhra Pradesh 28 545 East Godavari 802952 Rajahmundry Andhra Pradesh 28 545 East Godavari 802957 Ramachandrapuram -

Lok Mitra Kendras (Lmks)

DistrictName BlockName Panchayat Village VLEName LMKAddress ContactNo Name Name Chamba Bharmour BHARMOUR bharmour MADHU BHARMOUR 8894680673 SHARMA Chamba Bharmour CHANHOTA CHANHOTA Rajinder Kumar CHANHOTA 9805445333 Chamba Bharmour GAROLA GAROLA MEENA KUMARI GAROLA 8894523608 Chamba Bharmour GHARED Ghared madan lal Ghared 8894523719 Chamba Bharmour GREEMA FANAR KULDEEP SINGH GREEMA 9816485211 Chamba Bharmour HOLI BANOON PINU RAM BANOON 9816638266 Chamba Bharmour LAMU LAMU ANIL KUMAR LAMU 8894491997 Chamba Bharmour POOLAN SIRDI MED SINGH POOLAN 9816923781 Chamba Bharmour SACHUIN BARI VANDANA SACHUIN 9805235660 Chamba Bhattiyat NULL Chowari SANJAY Chowari 9418019666 KAUSHAL Chamba Bhattiyat NULL DEEPAK RAJ Village Kathlage 9882275806 PO Dalhausie Tehsil Dalhausie Distt Chamba Chamba Bhattiyat AWHAN Hunera Sanjeet Kumar AWHAN 9816779541 Sharma Chamba Bhattiyat BALANA BALANA RAM PRASHAD 9805369340 Chamba Bhattiyat BALERA Kutt Reena BALERA 9318853080 Chamba Bhattiyat BANET gaherna neelam kumari BANET 9459062405 Chamba Bhattiyat BANIKHET BANIKHET NITIN PAL BANIKET 9418085850 Chamba Bhattiyat BATHRI BATHRI Parveen Kumar BATHRI 9418324149 Chamba Bhattiyat BINNA chhardhani jeewan kumar BINNA 9418611493 Chamba Bhattiyat CHUHAN Garh (Bassa) Ravinder Singh CHUHAN 9418411276 Chamba Bhattiyat GAHAR GAHAR SHASHI GAHAR 9816430100 CHAMBIAL Chamba Bhattiyat GHATASANI GHATASANI SHEETAL GHATASANI 9418045327 Chamba Bhattiyat GOLA gola santosh GOLA 9625924200 Chamba Bhattiyat JIYUNTA kunha kewal krishan JIYUNTA 9418309900 Chamba Bhattiyat JOLNA Jolna Meena -

(A) Appellate Authorities

HIMACHAL PRADESH Public Works Department Himachal Pradesh Public Works Deaprtment Notification In supersession of this office Notification No:- PW-ROIA/WS- 534-763, dated 11-10-2005 and this office further order No. PW(B)-RTI Act 2005/WS-8745-8820, dated 07-11-2006. I, The Engineer-in-Chief HP, PWD in exercise of the powers conferred upon me under sub-section (1) and (2) of section-5 of the RTI Act,05 re-designate the following officers of the Himachal Pradesh Public Works Department as appellate Authorities, Public Information Officers and Asstt. Public Information Officers with immediate effect in the public interest, (A) Appellate Authorities Sr. Designation Of Authority States under the Act Telephone No No Office Residence 1. Superintending Engineer For O/O E-in-C, HP, PWD, Shimla-2, 2625821 2626426 (Works) O/OE-in-C, HP, O/O Chief Engineer (South) HP,PWD, PWD, Nigam Vihar, Shimla-2 and for O/O Land Acquisition Shimla- 171 002. Officer, HP, PWD, Winter Field, Shimla-3. 2. Superintending Engineer For O/O E-in-C (Q.C.) Office, HP, 2652438 2622914 (Q.C.&D) O/O E-in-C(Q.C.) PWD,U.S.Club, Shimla-1. Office, HP, PWD,U.S.Club, Shimla-1. 3 Superintending Engineer For O/O Chief Engineer(CZ) HP, PWD, 221621 221154 (Works) O/O Chief Engineer Mandi and for O/O Land Acquisition (CZ) HP, PWD, Mandi. Officer, HP, PWD, Mandi. 4 Superintending Engineer For O/O Chief Engineer (NZ) office 223189 226264 (Works) O/O Chief Engineer HP,PWD, Dharamshala and for O/O (NZ) HP,PWD,Dharamshala. -

Rds ) of Shimla SSA Customer Service Centers (Cscs

Franchisees of Shimla SSA Franchisee Name Complete Address Phone No Fax No Mobile No e-mail id Area being served Sh Dinesh Gupta Gupta Electricals, 38 Middle Bazar Shimla 1772803000 Nil 9418020000 [email protected] Shimla City Sh Dinesh Gupta Gupta Electricals, 38 Middle Bazar Shimla 1772803000 Nil 9418020000 [email protected] Shimla- Rural (SDO-T Area ) Sh Gourav Sood Satyam Enterprises, The Mall Shimla 1783238939 177-2657207 9418034567 [email protected] Theog,kotkhai, Nerwa, Chopal Sh Satish Kumar Babu Ram Satish Kumar, Main Bazar Rohru 1781220080 Nil 8988206600 [email protected] Rohru, Jubbal Sh Sateesh Negi TIC building,Main bajar,Recongpeo,shimla 1786223666 Nil 9418016161 [email protected] Recongpeo, Pooh 01772658055, Sh Adarsh Sood Best Gas Service, 94/1 The Mall Shimla Nil 9418000027 [email protected] Rampur, Nirmand, Anni, Kumarsain 01782234911 Rural Distributors (RDs ) of Shimla SSA RD Name Complete Address Phone No Fax No Mobile No e-mail id Area being served Sh Anil Thakur VPO Poabo, Tehsil Shimla Rural NIL NIL NIL Poabo 9418201782 Sh Chitter Sain C S Communication, VPO Basantpur NIL NIL 9418088715 NIL Basantpur Sh Narvda Sharma N B Communication, Ghanahatti NIL NIL 9418600474 NIL Dhami Sh Jagdish Khachi VPO Dhamandri, Tehsil Theog NIL NIL 9418161533 NIL Chaila Sh Nilesh Kumar Nilesh Communication Theog NIL NIL 9418901122 NIL Matiyana Sh Suresh Kumar Vill Chandni, PO Deha, Tehsil Theog NIL NIL 9459633236 NIL Deha Sh Narender Sharma VPO Bharech, Tehsil Kotkhai NIL NIL 9459178200 NIL Gumma Sh Shaveen Chauhan -

Woodcarvings from Pabbar Valley

Indian Journal of Traditional Knowledge Vol. 4(4), October 2005, pp. 380-385 Woodcarvings from Pabbar Valley Hari Chauhan Himachal State Museum, Shimla 171004, Himachal Pradesh Received 15 October 2004, revised 22 February 2005 Woodcarving was the favoured medium of artistic expression of the Indian subcontinent. Indian houses and temples were profusely adorned with it and are often inseparable from it. Woodcarving, an indigenous tradition craft finds a mention in the ancient texts such as the Rig Veda and Matsya Purana. Woodcarving craft was well developed in many states spe- cially, Himachal Pradesh, Uttar Pradesh, Rajasthan, Gujarat, Kerala, Kashmir and Madhya Pradesh. They differed in terms of the kind of wood and the craft tradition. In the early days of kings and nawabs, woodcarving was essentially seen as an adjunct to architecture. Palaces, havelis and temples were decorated with incredibly carved doors, windows and jalis (lattice work). The present paper describes traditional woodcarving work adoring houses and temples of Pabbar valley of Himachal Pradesh. Keywords: Woodcarving, Traditional Craft, Pabbar Valley, Himachal Pradesh IPC Int. Cl.7: B44C1/22, B44C5/04 The woodcarving, an indigenous craft tradition has worked windows made up of pieces of wood. In Ben- retained its economic and cultural importance for gal, the clay houses have large wooden pillars and hundreds of years. Wood was one of the most impor- beams with intricate carvings. Assam has a rich tradi- tant materials used in arts to express thoughts. Wood tion of wood works. Their places of worship included was used to carve various items for household use as large carvings of mythical figures. -

Success Story

SUCCESS STORY Name of Trainee Beena Father Name Mr. Hari Kumar Village Shoba Tehsil Jubbal District Shimla State Himachal Pradesh Passed Out NSIC-Training Centre, 2015-16 (125 Hours) Family Background Miss Beena was born in Shoba, Jubbal. Her father is working as a farmer. After completing her 8th from Govt School, she joined NSIC Training center and successfully passed the ESDP conducted by MSME course of Fashion Designing. Present Status After receiving her certificate from MSME, she has started work from home and now she is earning approximately 3000 per Month to be financially independent. SUCCESS STORY Name of Trainee Rupa Father Name Mr. Ganesh Bahadur Village Battar Galu Tehsil Jubbal District Shimla State Himachal Pradesh Passed Out NSIC-Training Centre, 2015-16 (125 Hours) Family Background Miss Rupa was born in Battar Galu, Jubbal. Her father is working as a farmer. After completing her 8th from Govt School, she joined NSIC Training center and successfully passed the ESDP conducted by MSME course of Fashion Designing. Present Status After receiving her certificate from MSME, she has started work from home and now she is earning approximately 3000 per Month to be financially independent. SUCCESS STORY Name of Trainee Manju Father Name Mr. Satiman Village Badhal Tehsil Jubbal District Shimla State Himachal Pradesh Passed Out NSIC-Training Centre, 2015-16 (125 Hours) Family Background Miss Manju was born in Badhal, Jubbal. Her father is working as a farmer. After completing her 10th from Govt. School, she joined NSIC Training center and successfully passed the ESDP conducted by MSME course of Fashion Designing. -

43464-023: Himachal Pradesh Clean Energy

Social Monitoring Report Project Number: 43464-023 May 2019 Period: July 2018 – December 2018 IND: Himachal Pradesh Clean Energy Transmission Investment Program - Tranche 1 Submitted by Himachal Pradesh Power Transmission Corporation Limited (HPPTCL) This social monitoring report is a document of the borrower. The views expressed herein do not necessarily represent those of ADB's Board of Directors, Management, or staff, and may be preliminary in nature. In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area. July 2018 to December 2018 Social Monitoring Report HIMACHAL PRADESH POWER TRANSMISSION CORPORATION LTD. (A STATE GOVERNMENT UNDERTAKING) Semi-Annual Social Monitoring Report Loan: 2794-IND May, 2019 IND: Himachal Pradesh Clean Energy Transmission Investment Program (Tranche 1) Reporting Period: July 2018 to December 2018 Prepared by: Himachal Pradesh Power Transmission Corporation Ltd (A State Government Undertaking) for Asian Development Bank. Table of Contents 1. Introduction and Project Description .................................................................................. 1 2. Purpose of the Report ......................................................................................................... 3 3. Social Safeguards Categorization ...................................................................................... -

Shimla DLR.Xlsx

Settlement Patwari Examination-2015 Date 25/11/2015 Time 11:00AM 12:30PM For Shimla division: NOTE: In case of any query please contact Settlement Office Shimla at 0177-2622109/0177-2623995/0177-2624640 Sr. No. Roll No. Name of Candidate Father's Name Permanent/ Correspondence Sub Division Name of Center Address District 1 266314 Surender Jagat Ram V.PO.Sari,Teh-Chopal, Distt. Shimla CHOPAL Shimla DAV Public School Chopal 2 266315 Pawan Kumar Hira Singh V-NarathaDhar, P.O.-Chopal, Teh- CHOPAL Shimla DAV Public School Chopal, Distt. Shimla Chopal 3 266316 Rohit Kumar RoshanLal VPO-Tharoch, Teh-Chopal, Distt. CHOPAL Shimla DAV Public School Shimla Chopal 4 266317 Rohini Hari Singh V.Dak, P.O. Dhar Chandna, Teh-Kupvi, CHOPAL Shimla DAV Public School Distt, Shimla Chopal 5 266318 Lucky Madan Lal V-Fawla, P.O.-Irra, Teh-Chopal, Distt . CHOPAL Shimla DAV Public School Shimla Chopal 6 266319 Sushant Chauhan Deepak Chauhan V-Katach, P.O. Maraog, Teh-Chopal, CHOPAL Shimla DAV Public School Distt. Shimla Chopal 7 266320 Ashish Kumar Rai Singh v-Sarain, P.O. Pouria, Teh-Chopal, CHOPAL Shimla DAV Public School Distt. Shimla Chopal 8 266321 Piyush Kumar Lokender Singh V-Khokha, P.O Ruslah, Teh-Chopal, CHOPAL Shimla DAV Public School Distt. Shimla Chopal 9 266322 Rajesh Kumar Sher Singh V-Sailpab, P.O. Kulag, Teh-Kupvi, Dsitt. CHOPAL Shimla DAV Public School Shimla Chopal 10 266323 Ranbir Singh Laiq Ram V-Shalan, P.O. Nalau, Teh-Chopal, CHOPAL Shimla DAV Public School No Catag Distt. Shimla Chopal 11 266324 Preeti Kumari Devinder Singh V-Sarahan, P.O. -

Department/Public Authority : DC Office, Shimla

HIMACHAL PRADESH DC Office, Shimla Department/Public Authority : D.C. Office, Shimla Sr. Designation Office Address Jurisdiction E-mail Tele/Fax No. No Deputy Commissioner O/O Deputy D.C. Office, 2653535 (Appellant Authority) Commissioner, Shimla Shimla. 2653535(fax) 1. Addl. District O/O Addl. District Shimla District 2657005 Magistrate (L&O), Magistrate (L&O), (PIO) Shimla. D.C Office, Shimla. Sub-Divisional Level 2. Sub-Divisional O/O Sub-Divisional S.D.M’s Office, 2657007 Magistrate, (PIO) Magistrate, Shimla Shimla(U). (Urban) 3. Sub-Divisional O/O Sub-Divisional S.D.M.s Office, 2657009 Magistrate, (PIO) Magistrate, Shimla Shimla (Rural) 4. Sub-Divisional O/O Sub Divisional S.D.Ms Office 951783-238502 Magistrate, (PIO) Magistrate, Theog. Theog. 5. Sub-Divisional O/O Sub Divisional S.D.Ms Office 951782-233002 Magistrate, (PIO) Magistrate, Rampur. Rampur 6. Sub-Divisional O/O Sub Divisional S.D.Ms Office 951781-240009 Magistrate, (PIO) Magistrate, Rohru. Rohru. 7. Sub-Divisional O/O Sub Divisional S.D.Ms Office 951783-260014 Magistrate, (PIO) Magistrate, Chopal. Chopal. 8. Sub-Divisional O/O Sub Divisional S.D.Ms Office 951781-272001 Magistrate, (PIO) Magistrate, Dodra-Kwar. Dodra-Kwar. 9. Supdt. Grade-I (APIO) D.C.Office,Shimla D.C.Office,Shiml 2657005 a. 10. Supdt. Grade-II (APIO) D.C.Office, Shimla Supdt. Revenue. 2657005 D.C.Office, Shimla 11. Supdt. Grade-II (APIO) D.C. Office, Shimla Supdt. 2657003 Development, D.C. Office, Shimla 12. Supdt. Grade-II (APIO) O/O SDM Shimla(Rural) O/O SDM 2657009 Shimla(Rural) 13. Supdt. -

Contact Numbers of Officers of Treasuries

Contact Numbers of Officers of Treasuries, Accounts and Lotteries, Directorate, Block No-23, SDA Complex, Kasumpti, Shimla-171009(H.P.) Name Designation Email Phone Office Phone(Resi) Sh. Amarjeet Singh, I.A.S Spl. Secretary(Fin)- cum- Director, Treasuries, Accounts & dirtre-hp[at]nic[dot]in, 0177-2622132 Lotteries Sh. Deepak Bhardwaj Additional Director addtre-hp[at]nic[dot]in 0177-2621820, 2626444 Sh. Arun Ojha Joint Director jdirtre-hp[at]nic[dot]in 0177-2928642 94184-60120 Sh. P L Sharma Joint Director (NPS) Jd-nps-shi[at]hp[dot]nic[dot]in 0177-2622820 94184-89789 Sh. Hira Mani Verma Additional Director (HPF&AS) [email protected] 0177-2620684 94180-26963 Sh. Yudhvir Singh Thakur Deputy Director (HPPFM-CBP) ddpfm-shi-hp[at]gov[dot]in 0177-2626444 94180-40219 Sh. Rakesh Dharmani Deputy Director(Inspection) ddtre-shi-hp [at]nic[dot]in 0177-2622820 94592-90584 Sh. Rakesh Kumar Deputy Director (Admin) ddhqtre-hp [at]nic[dot]in 0177-2620684 94181-89791 Sh. Inderdeep Sharma District Treasury Officer (HPPFM-CBP) dtopfm-shi-hp[at]gov[dot]in 0177-2626444 98166-03922 Sh. Satish Kumar District Treasury Officer (NPS) dtonps-shi-hp[at] SH. MOHD IRFAN Sub-Treasury Dadahu, Nahan to-smr05-hp [at]nic[dot]in 94180-29440 SH. RANVEER KUMAR Sub-Treasury Sangrah, Nahan to-smr06-hp [at]nic[dot]in 01702-248054 98166-61444 SH. KASHMA DUTT Sub-Treasury Pachhad, Nahan to-smr07-hp [at]nic[dot]in 01799-236060 98573-28822 SH. HARIMAN Sub-Treasury Nohradhar, Nahan to-smr08-hp [at]nic[dot]in 80917-17550 KINNAUR Sh.