Tapping Into Africa's Potential

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Public Notice

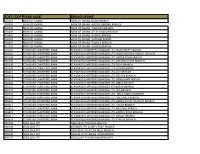

PUBLIC NOTICE PROVISIONAL LIST OF TAXPAYERS EXEMPTED FROM 6% WITHHOLDING TAX FOR JANUARY – JUNE 2016 Section 119 (5) (f) (ii) of the Income Tax Act, Cap. 340 Uganda Revenue Authority hereby notifies the public that the list of taxpayers below, having satisfactorily fulfilled the requirements for this facility; will be exempted from 6% withholding tax for the period 1st January 2016 to 30th June 2016 PROVISIONAL WITHHOLDING TAX LIST FOR THE PERIOD JANUARY - JUNE 2016 SN TIN TAXPAYER NAME 1 1000380928 3R AGRO INDUSTRIES LIMITED 2 1000049868 3-Z FOUNDATION (U) LTD 3 1000024265 ABC CAPITAL BANK LIMITED 4 1000033223 AFRICA POLYSACK INDUSTRIES LIMITED 5 1000482081 AFRICAN FIELD EPIDEMIOLOGY NETWORK LTD 6 1000134272 AFRICAN FINE COFFEES ASSOCIATION 7 1000034607 AFRICAN QUEEN LIMITED 8 1000025846 APPLIANCE WORLD LIMITED 9 1000317043 BALYA STINT HARDWARE LIMITED 10 1000025663 BANK OF AFRICA - UGANDA LTD 11 1000025701 BANK OF BARODA (U) LIMITED 12 1000028435 BANK OF UGANDA 13 1000027755 BARCLAYS BANK (U) LTD. BAYLOR COLLEGE OF MEDICINE CHILDRENS FOUNDATION 14 1000098610 UGANDA 15 1000026105 BIDCO UGANDA LIMITED 16 1000026050 BOLLORE AFRICA LOGISTICS UGANDA LIMITED 17 1000038228 BRITISH AIRWAYS 18 1000124037 BYANSI FISHERIES LTD 19 1000024548 CENTENARY RURAL DEVELOPMENT BANK LIMITED 20 1000024303 CENTURY BOTTLING CO. LTD. 21 1001017514 CHILDREN AT RISK ACTION NETWORK 22 1000691587 CHIMPANZEE SANCTUARY & WILDLIFE 23 1000028566 CITIBANK UGANDA LIMITED 24 1000026312 CITY OIL (U) LIMITED 25 1000024410 CIVICON LIMITED 26 1000023516 CIVIL AVIATION AUTHORITY -

Africa Beyond Covid-19: President George Weah, US Senator Chris

Africa Beyond Covid-19: President George Weah, US Senator Chris Coons, Tony Elumelu and Other Global Leaders at the 2nd UBA Africa Day Conversations Urge Government and Private Sector Collaboration . Demand a new deal in and for Africa . Advocate speedy implementation of AFCFTA . Call for Increased Investment in Digital Connectivity United Bank for Africa (UBA) celebrated Africa Day 2020, by bringing together global leaders at the 2nd UBA Africa Day Conversations, screened live across the continent. UBA helps set the debate around African economic development through its series of “Africa Conversations”. This year, the focus was on the Sustainable Development Goals (SDGs) and the Covid-19 pandemic. Leaders emphasised the need for meaningful collaboration between governments and the private sector, as a requirement for the quick recovery of the economy of the African continent post Covid-19. The panel included the President of Liberia, H.E George Weah; United States Senator Chris Coons; the President & Chairman of the Board of Directors of the African Export–Import Bank (AFREXIMBANK), Professor Benedict Okey Oramah; President, International Committee of the Red Cross (ICRC), Peter Maurer; and was moderated by the Group Chairman, UBA Plc, Tony O. Elumelu. Other leading voices contributing were the Founder, Africa CEO Forum, Amir Ben Yahmed; the Secretary-General of the African Caribbean and Pacific Group of States (ACP), H.E George Chikoti; Administrator, United Nations Development Program (UNDP), Achim Steiner and Donald Kaberuka, the former President of the African Union. Elumelu spoke on the need to mobilise quickly and explained the necessity to identify a more fundamental solution to Africa’s challenges. -

Digital Access: the Future of Financial Inclusion in Africa Acronyms

DIGITAL ACCESS: THE FUTURE OF FINANCIAL INCLUSION IN AFRICA ACRONYMS ADC Alternative Delivery Channel ISO International Organization for Standardization AFSD African Financial Sector Database IT Information Technology ARPU Average Revenue Per User KES Kenyan Shilling API Application Programming Interface KPI Key Performance Indicator ATM Automated Teller Machine KYC Know Your Customer B2P Business to Person LAPO MfB Lift Above Poverty Organization BCEAO Central Bank of West Africa (Banque Centrale Microfinance Bank des Etats de l’Afrique de l’Ouest) M-banking Mobile Banking BOI Banking Operations Intermediary M-wallet Mobile Wallet BVN Bank Verification Number MFI Microfinance Institution CEO Chief Executive Officer MM Mobile Money CBA Commercial Bank of Africa MSME Micro, Small and Medium Enterprise CBN Central Bank of Nigeria MTN Mobile Telephone Network CFA West African Franc, or Central African Franc MNO Mobile Network Operator CGAP Consultative Group to Assist the Poor MVNO Mobile Virtual Network Operator CRM Customer Relationship Management NFC Near Field Communication DFS Digital Financial Services OTC Over the Counter DJ Disc Jockey P2B Person to Business DVD Digital Versatile Disc P2P Person to Person E-banking Electronic Banking PC Personal Computer EFT Electronic Funds Transfer PIN Personal Identification Number EMI e-Money Issuer POS Point of Sale E-money Electronic Money PSP Payment Service Provider E-wallet Electronic Wallet E-warehousing Electronic Warehousing QR Quick Response FCMB First City Monument Bank RCT Randomized -

Societe Generale Ghana 2019 Annual Report

ANNUAL REPORT 2019 2019 ANNUAL REPORT AND FINANCIAL STATEMENTS 2019 Major Events WE INTRODUCED NEW INNOVATIONS Electronic billboard to communicate Our 24/7 drive-in ATM to the public about our product offers at Achimota branch & Our solar project. A cleaner, more effective energy source at our head office WE LAUNCHED NEW SERVICES 2019 Major Events WE LAUNCHED EXCITING COMMERCIAL PROMOTIONS & CAMPAIGNS Loans Promotion Deposit and Win Promotion WE OPENEDM ORE OUTLETS Achimota Branch Osu Branch TABLE OF CONTENTS Overview 02 Notice and agenda for annual general meeting Corporate Governance 03 Corporate information 04 Profile of the board of directors 07 Key management personnel Strategic report 10 Chairman's statement 13 Managing director’s review Financial statements 16 Report of the directors 31 Statement of directors responsibilities 32 Independent report of the auditors 36 Financial highlights 38 Statement of profit or loss and other comprehensive income 39 Statement of financial position 40 Statement of changes in equity 41 Statement of cash flows 42 Notes to financial statement 94 Proxy form 95 Resolutions 97 Branch network 2019 ANNUAL REPORT & FINANCIAL STATEMENTS 1 Notice and Agenda NOTICE AND AGENDA FOR ANNUAL GENERAL MEETING NOTICE IS HEREBY GIVEN THAT the 40th Annual General Meeting of Societe Generale Ghana Limited (the “Company”) will be held on Thursday, 26 March 2020 at 11am at the Alisa Hotel, Ridge Arena, Accra Ghana for the following purpose:- Ordinary Business: Ordinary Resolutions 1. To elect Directors, the following directors appointed 5. To approve Directors’ fees. during the year and retiring in accordance with Section 72(1) of the Company’s Regulations: 6. -

United Bank of Africa Customer Success Story

CUSTOMER SUCCESS STORY United Bank for Africa Invests in Polycom® RealPresence® Platform to Drive Polycom UC Solution Across its Global Network Industry Overview Finance United Bank for Africa (UBA) Group is one of Africa’s leading financial institutions offering banking services to more than seven million customers via Daily use 750 branches in 18 African countries. With further offices in New York, London • Executive briefings and Paris, UBA is connecting people and businesses across the world through retail and corporate banking, innovative cross-border payments, trade finance • Board meetings and investment banking. • Quarterly business reviews • Corporate training Over the past three years, UBA had undergone a period of rapid expansion that had seen affiliate banks in 16 African countries come on board. This expansion Solution has naturally put the group’s communication infrastructure under pressure. A flexible unified communications platform In order for the Group to improve and extend its communication network at the that delivered an integrated telephony same time as alleviating the increasing pressure on travelling executives it sought and video conferencing solution to an integrated communications platform to deliver the flexibility and dynamic accommodate the growing number of resource allocation they needed for unified communications (UC). disparate and geographically-dispersed end-points. The Group stated “We required a platform to deliver an integrated telephony and video conferencing solution with the flexibility to accommodate the growing Results and benefits number of disparate and geographically-dispersed end-points.” • Increased productivity meetings The IT team was asked to lead an investigation on the best solutions • Savings in travel costs available. -

Participant List

Participant List 10/20/2019 8:45:44 AM Category First Name Last Name Position Organization Nationality CSO Jillian Abballe UN Advocacy Officer and Anglican Communion United States Head of Office Ramil Abbasov Chariman of the Managing Spektr Socio-Economic Azerbaijan Board Researches and Development Public Union Babak Abbaszadeh President and Chief Toronto Centre for Global Canada Executive Officer Leadership in Financial Supervision Amr Abdallah Director, Gulf Programs Educaiton for Employment - United States EFE HAGAR ABDELRAHM African affairs & SDGs Unit Maat for Peace, Development Egypt AN Manager and Human Rights Abukar Abdi CEO Juba Foundation Kenya Nabil Abdo MENA Senior Policy Oxfam International Lebanon Advisor Mala Abdulaziz Executive director Swift Relief Foundation Nigeria Maryati Abdullah Director/National Publish What You Pay Indonesia Coordinator Indonesia Yussuf Abdullahi Regional Team Lead Pact Kenya Abdulahi Abdulraheem Executive Director Initiative for Sound Education Nigeria Relationship & Health Muttaqa Abdulra'uf Research Fellow International Trade Union Nigeria Confederation (ITUC) Kehinde Abdulsalam Interfaith Minister Strength in Diversity Nigeria Development Centre, Nigeria Kassim Abdulsalam Zonal Coordinator/Field Strength in Diversity Nigeria Executive Development Centre, Nigeria and Farmers Advocacy and Support Initiative in Nig Shahlo Abdunabizoda Director Jahon Tajikistan Shontaye Abegaz Executive Director International Insitute for Human United States Security Subhashini Abeysinghe Research Director Verite -

Établissements De Crédit Taux De Base Bancaire

BANQUE CENTRALE DES ETATS DE L'AFRIQUE DE L'OUEST (BCEAO) CONDITIONS DEBITRICES APPLIQUEES PAR LES ETABLISSEMENTS DE CREDIT DE L'UMOA AU TITRE DU SECOND SEMESTRE 2019 Date de la dernière Taux de base Taux débiteur Établissements de crédit modification du taux de Bancaire (%) Maximum (%) base bancaire BENIN ORABANK BENIN 9,00 15,00 01/01/19 BANK OF AFRICA - BENIN (BOA - BENIN) 9,00 13,00 01/02/18 ECOBANK - BENIN (ECOBANK) 9,00 15,00 01/01/17 BANQUE INTERNATIONALE DU BENIN (B.I.BE.) 9,00 13,00 01/04/19 UNITED BANK FOR AFRICA BENIN (UBA - BENIN) 9,00 14,00 01/04/11 NSIA BANQUE BENIN 8,00 14,00 17/11/15 SOCIETE GENERALE - BENIN 9,00 13,00 01/10/14 BANQUE SAHELO-SAHARIENNE POUR L'INVESTISSEMENT ET LE COMMERCE BENIN (BSIC- 9,00 13,50 04/01/19 BENIN) BANQUE ATLANTIQUE BENIN (BANQUE ATLANTIQUE) 9,00 14,00 01/08/05 BGFIBANK BENIN 9,80 15,00 01/09/18 CBAO, GROUPE ATTIJARIWAFA BANK, SUCCURSALE DU BENIN 9,00 14,00 01/03/18 BANQUE AFRICAINE POUR L'INDUSTRIE ET LE COMMERCE (BAIC) 9,00 13,00 01/07/19 CCEI BANK BENIN 9,00 13,00 31/12/16 CORIS BANK INTERNATIONAL, SUCCURSALE DU BENIN 8,00 14,00 01/01/19 SONIBANK, SUCCURSALE DU BENIN 9,00 12,50 23/03/18 BURKINA UNITED BANK FOR AFRICA BURKINA (UBA BURKINA) 10,75 15,00 30/06/16 BANQUE INTERNATIONALE POUR LE COMMERCE, 9,75 12,50 01/01/15 L'INDUSTRIE ET L'AGRICULTURE DU BURKINA (BICIA - B) BANQUE COMMERCIALE DU BURKINA (BCB) 10,00 13,50 18/02/12 SOCIETE GENERALE - BURKINA FASO 9,50 14,75 21/11/14 ECOBANK - BURKINA (ECOBANK) 10,00 13,50 01/09/19 BANK OF AFRICA - BURKINA FASO (BOA - BURKINA FASO) 9,50 15,00 15/07/19 -

The Financial Statements of the Company (Together with the Reports of the Directors and the Auditors of the Company) for the Year Ended 31 December 2020

Find out more: VISIT GO ONLINE societegenerale.com.gh 2020 ANNUAL REPORT AND FINANCIAL STATEMENTS 2020 Major Events WE INTRODUCED INNOVATIONS Our all new innovation lab WE LAUNCHED NEW SERVICES Easily pay your customs duty Pay for all government services at any SG Ghana branch and taxes at any SG Ghana branch 2020 Major Events WE LAUNCHED EXCITING COMMERCIAL PROMOTIONS & CAMPAIGNS Loans Promotion Cards Promotion àƺǝǣƬǼƺˡȇƏȇƬǣȇǕȒǔǔƺȸǔȒȸȒɖȸƬɖɀɎȒȅƺȸɀ in collaboration with CFAO Motors WE OPENED MORE OUTLETS Airport City Branch Derby Avenue Branch Lapaz Branch TABLE OF CONTENTS Overview 2 Our purpose and values in the service of our clients 4 Notice and Agenda for Annual General Meeting Corporate Governance 5 Corporate information 6 Profile of the board of directors 9 Key management personnel Strategic Report 12 Board chair’s statement 14 Managing Directors Review Financial Statements 18 Report of the Directors 28 Corporate structure 33 Statement of Directors Responsibilities 34 Independent Report of the Auditors 38 Financial highlights 40 Statement of profit or loss and other comprehensive income 41 Statement of financial position 42 Statement of changes in equity 43 Statement of cash flows 44 Notes to financial statement 99 Proxy Form 100 Resolutions 102 Branch network SOCIETE GENERALE GHANA PLC 1 OUR PURPOSE AND VALUES IN THE SERVICE OF OUR CLIENTS OUR PURPOSE segments by tailoring our support to the issues facing each Building together with our clients, a better and sustainable one of them; future through responsible and innovative financial solutions. y connecting people and businesses: creating a link between those who have projects and those who can help them; OUR MISSION STATEMENT The Bank’s mission is to create the preferred banking institution, y using our resources responsibly: putting our balance sheet which employs team spirit, innovation, responsibility & to work to help those who want to invest; commitment to provide quality products and services that best y evaluating and managing risks: managing risks in a satisfy the needs of our customers. -

Millennium Bim Fined MZN 76 Million by Bank of Mozambique for AML and CTF Violations

ORX News reference: 9134 ORX Standard: Banking Banco Comercial Português MZN 76,000,000.00 | Metical USD 1,203,080.00 | US Dollar EUR 1,085,280.00 | Euro BL0301 - Retail Banking EL0402 - Improper Business or Market Practices MZ - Mozambique Africa Loss Event Published in media 28 October 2019 Millennium Bim fined MZN 76 million by Bank of Mozambique for AML and CTF violations On 28 October 2019, Verdade reported that the Bank of Mozambique had fined Millennium Bim MZN 76 million (USD 1.2 million, EUR 1.1 million) for violating the country’s law on anti-money laundering (AML) and counter-terrorist financing (CTF) between the financial years of 2014 and 2018. According to a statement issued by the Bank of Mozambique, Millenium Bim failed to identify and verify customers, continuously monitor business relationships, maintain documents and immediately report suspicious transactions. The Bank of Mozambique fined Millennium Bim as part of a wider action. In total, the Bank of Mozambique issued 20 fines totalling MZN 172.9 million (approximately USD 2.7 million) to 18 firms. The 19 remaining fines ranged from MZN 100,000 to MZN 28 million (approximately USD 2,000 to USD 443,000). Between the financial years of 2013 and 2019, the 18 firms violated the AML and CTF law and a law on credit institutions and financial entities. The other banks were Standard Bank, Banco Único, Banco Comercial e de Investimentos (BCI), Vodafone M-Pesa, First National Bank (FNB), Barclays Bank, Banco Nacional de Investimentos (BNI), Banco de Investimento Global (BIG), Société Générale, Mybucks Bank, Cooperativa de Poupança e Crédito (CPC), Caixa de Poupança Postal de Moçambique (CPPM), United Bank for Africa (UBA), Banco Letshego, GAPI – Sociedade de Investimento, Yingwe Microbanco, African Banking Corporation (BancABC), First Capital Bank and Banco Moçambicano de Apoio aos Investimentos (MAIS). -

Sort Code Bank Name Branch Name

SORT CODE BANK NAME BRANCH NAME 010101 BANK OF GHANA BANK OF GHANA ACCRA BRANCH 010303 BANK OF GHANA BANK OF GHANA -AGONA SWEDRU BRANCH 010401 BANK OF GHANA BANK OF GHANA -TAKORADI BRANCH 010402 BANK OF GHANA BANK OF GHANA -SEFWI BOAKO BRANCH 010601 BANK OF GHANA BANK OF GHANA -KUMASI BRANCH 010701 BANK OF GHANA BANK OF GHANA -SUNYANI BRANCH 010801 BANK OF GHANA BANK OF GHANA -TAMALE BRANCH 011101 BANK OF GHANA BANK OF GHANA - HOHOE BRANCH 020101 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD-HIGH STREET BRANCH 020102 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD- INDEPENDENCE AVENUE BRANCH 020104 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD-LIBERIA ROAD BRANCH 020105 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD-OPEIBEA HOUSE BRANCH 020106 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD-TEMA BRANCH 020108 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD-LEGON BRANCH 020112 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD-OSU BRANCH 020118 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD-SPINTEX BRANCH 020121 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD-DANSOMAN BRANCH 020126 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD-ABEKA BRANCH 020127 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH)-ACHIMOTA BRANCH 020129 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD- NIA BRANCH 020132 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD- TEMA HABOUR BRANCH 020133 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD- WESTHILLS BRANCH 020436 -

UBA Kenya Quarter 2 Financials

UBA Kenya Bank Limited Head Office Westlands Branch: Apollo Centre, Westlands P.O. Box 3415-00100 Nairobi E-mail: [email protected] Tel +254 20361200-2 Enterprise Branch: Tel:020 3612081 Upper Hill Branch: Tel 020 3612091 UNAUDITED FINANCIAL STATEMENTS AND OTHER DISCLOSURES FOR THE PERIOD ENDED 30th JUNE 2016 United Bank for Africa Plc I STATEMENT OF FINANCIAL POSITION June 2016 March 2016 December 2015 June 2015 (Unaudited) (Unaudited) (Audited) (Unaudited) at a glance Shs '000 Shs '000 Shs '000 Shs '000 A ASSETS 1 Cash ( both Local & Foreign) 43,225 39,821 46,767 42,074 2 Balances due from Central Bank of Kenya 766,415 317,410 196,299 278,833 3 Kenya Government and other securities held for dealing purposes - - - - 4 Financial Assets at fair value through profit and loss - - - - London 5 Investment Securities: a) Held to Maturity: 1,448,236 1,484,683 1,402,444 1,789,123 a. Kenya Government securities 1,448,236 1,484,683 1,402,444 1,789,123 b. Other securities - - - - b) Available for sale: a. Kenya Government securities - - - - b. Other securities - - - - New York 6 Deposits and balances due from local banking institutions 594 101,126 2,084 2,435 7 Deposits and balances due from banking institutions abroad 324,785 1,171,165 2,899,113 2,790,857 8 Tax recoverable 3,898 3,898 3,898 3,898 9 Loans and advances to customers (net) 2,591,236 2,876,324 2,733,280 1,855,687 10 Balances due from banking institutions in the group - - - - 11 Investments in associates - - - - 12 Investments in subsidiary companies - - - - Paris 13 Investments -

The Process of Monetary Decoloniza Tjon in Africa A

The African e-Journals Project has digitized full text of articles of eleven social science and humanities journals. This item is from the digital archive maintained by Michigan State University Library. Find more at: http://digital.lib.msu.edu/projects/africanjournals/ Available through a partnership with Scroll down to read the article. THE PROCESS OF MONETARY DECOLONIZA TJON IN AFRICA A. MENSAH. Africa is split up into many different monetary zones which have been under- going one process of transformation or the other. The main aim of this essay is to trace the process and examine the mechanics of monetary decolonization from the time when many African countries became politicallv independent up to 1977 1. THE EVOLUTION AND CHARACTERISTICS OF THE MONETARY ZONES Before the colonial subjugation of Africa 1 there was, apart from barter, monetary economy in various parts of the continent2. With the physical balkanization3 of Africa during the colonial era the colonial powers found it equally expedient to effect a monetary fragmentation of the continent. Thus they introduced their own currencies or varieties of them into their areas of influence or colonies4, so that during the colonial period the following:major foreign monetary zones emerged on the African continent: the French Franc zone, the Sterling zone, the Escudo zone, the Peseta zone, the Dollar zone, the Lira zone and the Belgian Franc zones The foreign monetary zones in Africa had and still have certain common chara- cteristics. Four such features are6: i. they have a colonial origin, .ii. their ultimate decision making organs are situated outside Africa'.