The Financial Statements of the Company (Together with the Reports of the Directors and the Auditors of the Company) for the Year Ended 31 December 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2016 Ghana Banking Survey How to Win in an Era of Mobile Money

2016 Ghana Banking Survey How to win in an era of mobile money August 2016 www.pwc.com/gh Contents A message from our CSP 2 A message from the Executive Secretary of Ghana Association of Bankers 4 Comments on 2016 Ghana Banking Survey 6 A message from our Tax Leader 8 1 How to win in an era of mobile money 10 2 Overview of the economy 26 3 Overview of the banking industry 32 4 Quartile analysis 36 5 Market share analysis 48 6 Profitability and efficiency 56 7 Return to shareholders 64 8 Liquidity 68 9 Asset quality 74 A List of participants 77 B Glossary of key financial terms, equations and ratios 78 C List of abbreviations 79 D Our profile 80 E Our leadership team 84 PwC 2016 Ghana Banking Survey 1 A message from our CSP for consumer banking. Besides, it offers in designing a practical and forward huge cheap deposits that banks could looking regulation that will streamline use to create money in the economy. It operations in the mobile money market. is against this backdrop that we focused This will require extensive consultation this year’s banking survey on “How to win locally and leveraging the experience of in an era of mobile money”. other countries such as Kenya that are advanced in the delivery of the service. Unlike the 2015 banking survey that sought responses from bank executives In addition to regulations and as well as bank customers, this year’s partnerships, the other critical success survey was based on responses from factors which we discussed with bank bank executives only. -

Public Notice

PUBLIC NOTICE PROVISIONAL LIST OF TAXPAYERS EXEMPTED FROM 6% WITHHOLDING TAX FOR JANUARY – JUNE 2016 Section 119 (5) (f) (ii) of the Income Tax Act, Cap. 340 Uganda Revenue Authority hereby notifies the public that the list of taxpayers below, having satisfactorily fulfilled the requirements for this facility; will be exempted from 6% withholding tax for the period 1st January 2016 to 30th June 2016 PROVISIONAL WITHHOLDING TAX LIST FOR THE PERIOD JANUARY - JUNE 2016 SN TIN TAXPAYER NAME 1 1000380928 3R AGRO INDUSTRIES LIMITED 2 1000049868 3-Z FOUNDATION (U) LTD 3 1000024265 ABC CAPITAL BANK LIMITED 4 1000033223 AFRICA POLYSACK INDUSTRIES LIMITED 5 1000482081 AFRICAN FIELD EPIDEMIOLOGY NETWORK LTD 6 1000134272 AFRICAN FINE COFFEES ASSOCIATION 7 1000034607 AFRICAN QUEEN LIMITED 8 1000025846 APPLIANCE WORLD LIMITED 9 1000317043 BALYA STINT HARDWARE LIMITED 10 1000025663 BANK OF AFRICA - UGANDA LTD 11 1000025701 BANK OF BARODA (U) LIMITED 12 1000028435 BANK OF UGANDA 13 1000027755 BARCLAYS BANK (U) LTD. BAYLOR COLLEGE OF MEDICINE CHILDRENS FOUNDATION 14 1000098610 UGANDA 15 1000026105 BIDCO UGANDA LIMITED 16 1000026050 BOLLORE AFRICA LOGISTICS UGANDA LIMITED 17 1000038228 BRITISH AIRWAYS 18 1000124037 BYANSI FISHERIES LTD 19 1000024548 CENTENARY RURAL DEVELOPMENT BANK LIMITED 20 1000024303 CENTURY BOTTLING CO. LTD. 21 1001017514 CHILDREN AT RISK ACTION NETWORK 22 1000691587 CHIMPANZEE SANCTUARY & WILDLIFE 23 1000028566 CITIBANK UGANDA LIMITED 24 1000026312 CITY OIL (U) LIMITED 25 1000024410 CIVICON LIMITED 26 1000023516 CIVIL AVIATION AUTHORITY -

Africa Beyond Covid-19: President George Weah, US Senator Chris

Africa Beyond Covid-19: President George Weah, US Senator Chris Coons, Tony Elumelu and Other Global Leaders at the 2nd UBA Africa Day Conversations Urge Government and Private Sector Collaboration . Demand a new deal in and for Africa . Advocate speedy implementation of AFCFTA . Call for Increased Investment in Digital Connectivity United Bank for Africa (UBA) celebrated Africa Day 2020, by bringing together global leaders at the 2nd UBA Africa Day Conversations, screened live across the continent. UBA helps set the debate around African economic development through its series of “Africa Conversations”. This year, the focus was on the Sustainable Development Goals (SDGs) and the Covid-19 pandemic. Leaders emphasised the need for meaningful collaboration between governments and the private sector, as a requirement for the quick recovery of the economy of the African continent post Covid-19. The panel included the President of Liberia, H.E George Weah; United States Senator Chris Coons; the President & Chairman of the Board of Directors of the African Export–Import Bank (AFREXIMBANK), Professor Benedict Okey Oramah; President, International Committee of the Red Cross (ICRC), Peter Maurer; and was moderated by the Group Chairman, UBA Plc, Tony O. Elumelu. Other leading voices contributing were the Founder, Africa CEO Forum, Amir Ben Yahmed; the Secretary-General of the African Caribbean and Pacific Group of States (ACP), H.E George Chikoti; Administrator, United Nations Development Program (UNDP), Achim Steiner and Donald Kaberuka, the former President of the African Union. Elumelu spoke on the need to mobilise quickly and explained the necessity to identify a more fundamental solution to Africa’s challenges. -

Digital Access: the Future of Financial Inclusion in Africa Acronyms

DIGITAL ACCESS: THE FUTURE OF FINANCIAL INCLUSION IN AFRICA ACRONYMS ADC Alternative Delivery Channel ISO International Organization for Standardization AFSD African Financial Sector Database IT Information Technology ARPU Average Revenue Per User KES Kenyan Shilling API Application Programming Interface KPI Key Performance Indicator ATM Automated Teller Machine KYC Know Your Customer B2P Business to Person LAPO MfB Lift Above Poverty Organization BCEAO Central Bank of West Africa (Banque Centrale Microfinance Bank des Etats de l’Afrique de l’Ouest) M-banking Mobile Banking BOI Banking Operations Intermediary M-wallet Mobile Wallet BVN Bank Verification Number MFI Microfinance Institution CEO Chief Executive Officer MM Mobile Money CBA Commercial Bank of Africa MSME Micro, Small and Medium Enterprise CBN Central Bank of Nigeria MTN Mobile Telephone Network CFA West African Franc, or Central African Franc MNO Mobile Network Operator CGAP Consultative Group to Assist the Poor MVNO Mobile Virtual Network Operator CRM Customer Relationship Management NFC Near Field Communication DFS Digital Financial Services OTC Over the Counter DJ Disc Jockey P2B Person to Business DVD Digital Versatile Disc P2P Person to Person E-banking Electronic Banking PC Personal Computer EFT Electronic Funds Transfer PIN Personal Identification Number EMI e-Money Issuer POS Point of Sale E-money Electronic Money PSP Payment Service Provider E-wallet Electronic Wallet E-warehousing Electronic Warehousing QR Quick Response FCMB First City Monument Bank RCT Randomized -

Management and Staff of Societe Generale Ghana Support the Ghana Heart Foundaton with Ghs 160,000.00

Accra – Ghana, 20th March, 2019 MANAGEMENT AND STAFF OF SOCIETE GENERALE GHANA SUPPORT THE GHANA HEART FOUNDATON WITH GHS 160,000.00 Fig 1. Management, Staff Representatives of Societe Generale Ghana with Members of the Ghana Heart Foundation Management and Staff of Societe Generale Ghana, TOGETHER made a donation amount of GHS 160,000.00 to the Ghana Heart Foundation to support the Foundation in the area of health care delivery. Receiving Societe Generale Ghana, Prof. Dr. Mark Tettey, Cardiothoracic Surgeon of the National Cardiothoracic Centre at Korle-Bu Teaching Hospital and Representative for the Ghana Heart Foundation at the ceremony expressed their heartfelt gratitude to Management and Staff of the bank for their continued and loyal support to the Foundation over the years to date. Prof. Dr. Tettey stated that the Ghana Heart Foundation (GHF) of the Korle-Bu Teaching Hospital is a charity organization dedicated to saving lives and improving health care by informing the public on heart or cardiovascular related diseases. He said the Foundation also assisted people with cardiovascular disease by providing for cardiovascular research and training for health workers involved in cardiovascular care. 1 Speaking at the event, Mr Hakim Ouzzani; Managing Director of Societe Generale Ghana noted the very successful administration of funds received by GHF to the extent that every Ghanaian patient undergoing heart surgery receives 50% subsidy from the Trust Fund. He mentioned the values of the bank which encompass; Responsibility, Team Spirit, Commitment, Innovation and consequently, the bank’s presence at the centre for the donation which is an expression of Team Spirit aimed at preserving the lives. -

Societe Generale Ghana 2019 Annual Report

ANNUAL REPORT 2019 2019 ANNUAL REPORT AND FINANCIAL STATEMENTS 2019 Major Events WE INTRODUCED NEW INNOVATIONS Electronic billboard to communicate Our 24/7 drive-in ATM to the public about our product offers at Achimota branch & Our solar project. A cleaner, more effective energy source at our head office WE LAUNCHED NEW SERVICES 2019 Major Events WE LAUNCHED EXCITING COMMERCIAL PROMOTIONS & CAMPAIGNS Loans Promotion Deposit and Win Promotion WE OPENEDM ORE OUTLETS Achimota Branch Osu Branch TABLE OF CONTENTS Overview 02 Notice and agenda for annual general meeting Corporate Governance 03 Corporate information 04 Profile of the board of directors 07 Key management personnel Strategic report 10 Chairman's statement 13 Managing director’s review Financial statements 16 Report of the directors 31 Statement of directors responsibilities 32 Independent report of the auditors 36 Financial highlights 38 Statement of profit or loss and other comprehensive income 39 Statement of financial position 40 Statement of changes in equity 41 Statement of cash flows 42 Notes to financial statement 94 Proxy form 95 Resolutions 97 Branch network 2019 ANNUAL REPORT & FINANCIAL STATEMENTS 1 Notice and Agenda NOTICE AND AGENDA FOR ANNUAL GENERAL MEETING NOTICE IS HEREBY GIVEN THAT the 40th Annual General Meeting of Societe Generale Ghana Limited (the “Company”) will be held on Thursday, 26 March 2020 at 11am at the Alisa Hotel, Ridge Arena, Accra Ghana for the following purpose:- Ordinary Business: Ordinary Resolutions 1. To elect Directors, the following directors appointed 5. To approve Directors’ fees. during the year and retiring in accordance with Section 72(1) of the Company’s Regulations: 6. -

PRESS RELEASE PR. No 105/2020 SOCIETE

PRESS RELEASE PR. No 105/2020 SOCIETE GENERALE GHANA LIMITED (SOGEGH) - 2019 ANNUAL REPORT SOGEGH has released its Annual Report for the year ended 31 December, 2019 as per the attached. Issued in Accra, this 18th day of March, 2020. - E N D – att’d. Distribution: 1. All LDMs 2. General Public 3. Company Secretary, SOGEGH 4. NTHC Registrars, (Registrars for SOGEGH shares) 5. GSE Securities Depository 6. Securities & Exchange Commission 7. Custodian 8. GSE Council Members 9. GSE Notice Board For enquiries, contact: Head of Listings, GSE on 0302 669908, 669914, 669935 *GA ANNUAL REPORT 2019 2019 ANNUAL REPORT AND FINANCIAL STATEMENTS 2019 Major Events WE INTRODUCED NEW INNOVATIONS Electronic billboard to communicate Our 24/7 drive-in ATM to the public about our product offers at Achimota branch & Our solar project. A cleaner, more effective energy source at our head office WE LAUNCHED NEW SERVICES 2019 Major Events WE LAUNCHED EXCITING COMMERCIAL PROMOTIONS & CAMPAIGNS Loans Promotion Deposit and Win Promotion WE OPENEDM ORE OUTLETS Achimota Branch Osu Branch TABLE OF CONTENTS Overview 02 Notice and agenda for annual general meeting Corporate Governance 03 Corporate information 04 Profile of the board of directors 07 Key management personnel Strategic report 10 Chairman's statement 13 Managing director’s review Financial statements 16 Report of the directors 31 Statement of directors responsibilities 32 Independent report of the auditors 36 Financial highlights 38 Statement of profit or loss and other comprehensive income 39 Statement of financial position 40 Statement of changes in equity 41 Statement of cash flows 42 Notes to financial statement 94 Proxy form 95 Resolutions 97 Branch network 2019 ANNUAL REPORT & FINANCIAL STATEMENTS 1 Notice and Agenda NOTICE AND AGENDA FOR ANNUAL GENERAL MEETING NOTICE IS HEREBY GIVEN THAT the 40th Annual General Meeting of Societe Generale Ghana Limited (the “Company”) will be held on Thursday, 26 March 2020 at 11am at the Alisa Hotel, Ridge Arena, Accra Ghana for the following purpose:- Ordinary Business: Ordinary Resolutions 1. -

United Bank of Africa Customer Success Story

CUSTOMER SUCCESS STORY United Bank for Africa Invests in Polycom® RealPresence® Platform to Drive Polycom UC Solution Across its Global Network Industry Overview Finance United Bank for Africa (UBA) Group is one of Africa’s leading financial institutions offering banking services to more than seven million customers via Daily use 750 branches in 18 African countries. With further offices in New York, London • Executive briefings and Paris, UBA is connecting people and businesses across the world through retail and corporate banking, innovative cross-border payments, trade finance • Board meetings and investment banking. • Quarterly business reviews • Corporate training Over the past three years, UBA had undergone a period of rapid expansion that had seen affiliate banks in 16 African countries come on board. This expansion Solution has naturally put the group’s communication infrastructure under pressure. A flexible unified communications platform In order for the Group to improve and extend its communication network at the that delivered an integrated telephony same time as alleviating the increasing pressure on travelling executives it sought and video conferencing solution to an integrated communications platform to deliver the flexibility and dynamic accommodate the growing number of resource allocation they needed for unified communications (UC). disparate and geographically-dispersed end-points. The Group stated “We required a platform to deliver an integrated telephony and video conferencing solution with the flexibility to accommodate the growing Results and benefits number of disparate and geographically-dispersed end-points.” • Increased productivity meetings The IT team was asked to lead an investigation on the best solutions • Savings in travel costs available. -

Databank Weekly Market Watch

March 3, 2017 GSE MARKET STATISTICS SUMMARY Weekly Stock Market Review SCB Tops Gainers Chart for 3rd Consecutive Week: The bulls maintained their Current Previous % Change hold on the equities market this week, supported by price gains in 7 counters. Databank Stock Index 24,460.95 24,329.82 0.54 The Ghana Stock Exchange’s Composite Index (GSE-CI) increased by 11.09 points GSE-CI Level 1,868.19 1,857.10 0.60 w/w to ~1,868 points, while the Databank Stock Index advanced by 131.13 points Market Cap (GH¢ m) 49,147.28 52,310.92 -6.05 w/w to ~24,461 points. The year to date returns of the GSE-CI and the Databank YTD Return DSI 9.53% 8.94% Stock Index thus increased to 10.60% and 9.53% respectively. YTD Return GSE-CI 10.60% 9.95% Market activity was vibrant this week. A block trade in Guinness Ghana Weekly Volume Traded (Shares) 3,567,878 921,507 287.18 Breweries pushed up the volume of shares traded by ~% w/w to ~3.57 million Weekly Turnover (GH¢) 4,603,367 4,555,231 1.06 shares, with a value of ~GH¢4.60 million. Out of the 25 counters that traded this Avg. Weekly Volume Traded (Shares) 878,352 861,281 1.98 week, Guinness Ghana Breweries emerged the most active counter, accounting Avg. Weekly Value Traded (GH¢) 1,268,601 1,246,575 1.77 for 56% of aggregate trade volumes. No. of Counters Traded 25 23 The market breath of the Ghana Stock Exchange was positive this week, with 7 No. -

Participant List

Participant List 10/20/2019 8:45:44 AM Category First Name Last Name Position Organization Nationality CSO Jillian Abballe UN Advocacy Officer and Anglican Communion United States Head of Office Ramil Abbasov Chariman of the Managing Spektr Socio-Economic Azerbaijan Board Researches and Development Public Union Babak Abbaszadeh President and Chief Toronto Centre for Global Canada Executive Officer Leadership in Financial Supervision Amr Abdallah Director, Gulf Programs Educaiton for Employment - United States EFE HAGAR ABDELRAHM African affairs & SDGs Unit Maat for Peace, Development Egypt AN Manager and Human Rights Abukar Abdi CEO Juba Foundation Kenya Nabil Abdo MENA Senior Policy Oxfam International Lebanon Advisor Mala Abdulaziz Executive director Swift Relief Foundation Nigeria Maryati Abdullah Director/National Publish What You Pay Indonesia Coordinator Indonesia Yussuf Abdullahi Regional Team Lead Pact Kenya Abdulahi Abdulraheem Executive Director Initiative for Sound Education Nigeria Relationship & Health Muttaqa Abdulra'uf Research Fellow International Trade Union Nigeria Confederation (ITUC) Kehinde Abdulsalam Interfaith Minister Strength in Diversity Nigeria Development Centre, Nigeria Kassim Abdulsalam Zonal Coordinator/Field Strength in Diversity Nigeria Executive Development Centre, Nigeria and Farmers Advocacy and Support Initiative in Nig Shahlo Abdunabizoda Director Jahon Tajikistan Shontaye Abegaz Executive Director International Insitute for Human United States Security Subhashini Abeysinghe Research Director Verite -

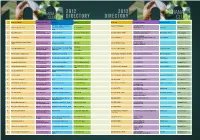

2012-Edition-GC100-Directory.Pdf

2012 2012 DIRECTORY DIRECTORY NAME OF COMPANY BUSINESS CATEGORY LOCATION ADDRESS TELEPHONE FAX/E-MAIL/WEBSITE CONTACT PERSON TITLE 7 Dr. Amilcar Cabral Road, Accra (233-302) 770189/90/91 “(233-302) 770187 1 Abosso GoldFields Limited Mining Institution Airport Residential Area P. O. Box KA 30742 www.goldfields.co.za” Alfred Baku Managing Director Accra Banking Services [email protected] Head, Corporate 2 Acces Bank (Ghana) (Commercial & Merchant) “Starlets ‘91 Road “P. O. Box GP 353 Osu- Accra” (233-302) 684860 / 742699 www.accessbankplc.com/gh Matilda Asante-Aseidu Communications (233-302) 2688960 3 Accra Brewery Manufacturing - Beverages Opp. Ohene Djan Staduim” P. O. Box GP351 (233-302) 688851-6 [email protected] Gregory Metcalf Managing Director www.sabmiller.com (233-302) 685176 4 Activa International Insurance Company Non-Banking-Insurance Graphic Road, Adabraka PMB KA 85 (233-32) 686352 / 672145 [email protected] Limited www.group-activa.com “P. O. Box 35 Banking Service-Rural & 3rd Floor Heritage Tower, 6th Ave. West (233-322) 420926 / 90099 Lucy Opoku-Arthur Ag General Manager 5 Adansi Rural Bank Limited Community Banking Ridge, Accra Fomena-Adansi” Banking Services-Rural & 6 Adonten Community Bank Limited Community Banking Head Office: Fomena - Adansi P.O.Box 140 3420-24109/027-895636/027-7609343 3420-26780 [email protected] Mr.Francis Mensah Senior Manager Banking Services-Rural & 7 Ahantaman Rural Bank Limited Community Banking New Tafo, Akyem, Eastern Region P. O. Box 41, Ahanta (233-312) 23431 / 21016 (233-312)29116 David Bampoe General Manager Banking Services-Rural & 8 Amanano Rural Bank Limited Community Banking Agona Ahanta,Western Region P. -

The Annual Public Debt Report for the 2020 Financial Year

The Annual Public Debt Report for the 2020 Financial Year Submitted to Parliament on Monday, 29th March, 2021 by Osei Kyei-Mensah-Bonsu, MP Minister Responsible for Finance In Fulfilment of the Requirements of Section 72 of the Public Financial Management Act, 2016 (Act 921) Annual Public Debt Report for the 2020 Financial Year The 2020 Annual Public Debt Report The 2020 Annual Public Debt Report is available on the internet at: www.mofep.gov.gh ii The 2020 Annual Public Debt Report Acronyms and Abbreviations ABED - Arab Bank for Economic Development ABN AMRO - ABN Amro Bank N.V. ABG - Access Bank (Ghana) Plc ADF - African Development Fund AfDB - African Development Bank APEX - ARB Apex Bank Limited AMCs - Asset Management Companies AMI - Asset Management Industry ATM - Average Time to Maturity ATR - Average Time to Re-fixing BAAG - Bank Austria AG BADB - Banco do Brasil BANS - Banco Santander BBNV - Belfius Bank NV/SA BBP - Barclays Bank UK Plc BELG - Government of Belgium BHI - Bank Hapoalim BMS - Bond Market Specialists BNDS - Banco Nacionale de Desenvolvimento Economico E Sociale BNP - Banque Nationale de Paris BoG - Bank of Ghana BoP - Balance of Payments BOST - Bulk Oil Storage and Transportation Company Ltd BMH - Mees Pierson NV CALB - CAL Bank Limited CBG - Consolidated Bank Ghana Limited CCAB - Credit Agricole CCRB - Cooeratieve Central Raifffeisen-Bank CDB - China Development Bank Corporation CITI - Citi Group CMBK - Commerzbank COVID-19 - Coronavirus Disease of 2019 CNY - Chinese Yuan CPI - Consumer Price Index CRAs - Credit Risk Assessments CSOB - Ceskoslovenska Obchodni Banka A.S CWE - China International Water & Electric Corporation DBF - Deutsche Bank, Frankfurt DBI - Deutsche Bank, Italy DBL - Deutsche Bank, London DBNY - Deutsche Bank, New York iii The 2020 Annual Public Debt Report DBSA - Deutsche Bank S.A.