Written Evidence Submitted by North Norfolk District Council

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

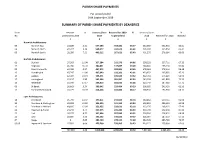

Parish Share Report

PARISH SHARE PAYMENTS For period ended 30th September 2019 SUMMARY OF PARISH SHARE PAYMENTS BY DEANERIES Dean Amount % Deanery Share Received for 2019 % Deanery Share % No Outstanding 2018 2019 to period end 2018 Received for 2018 received £ £ £ £ £ Norwich Archdeaconry 06 Norwich East 23,500 4.41 557,186 354,184 63.57 532,380 322,654 60.61 04 Norwich North 47,317 9.36 508,577 333,671 65.61 505,697 335,854 66.41 05 Norwich South 28,950 7.21 409,212 267,621 65.40 401,270 276,984 69.03 Norfolk Archdeaconry 01 Blofield 37,303 11.04 327,284 212,276 64.86 338,033 227,711 67.36 11 Depwade 46,736 16.20 280,831 137,847 49.09 288,484 155,218 53.80 02 Great Yarmouth 44,786 9.37 467,972 283,804 60.65 478,063 278,114 58.18 13 Humbleyard 47,747 11.00 437,949 192,301 43.91 433,952 205,085 47.26 14 Loddon 62,404 19.34 335,571 165,520 49.32 322,731 174,229 53.99 15 Lothingland 21,237 3.90 562,194 381,997 67.95 545,102 401,890 73.73 16 Redenhall 55,930 17.17 339,813 183,032 53.86 325,740 187,989 57.71 09 St Benet 36,663 9.24 380,642 229,484 60.29 396,955 243,433 61.33 17 Thetford & Rockland 31,271 10.39 314,266 182,806 58.17 300,933 192,966 64.12 Lynn Archdeaconry 18 Breckland 45,799 11.97 397,811 233,505 58.70 382,462 239,714 62.68 20 Burnham & Walsingham 63,028 15.65 396,393 241,163 60.84 402,850 256,123 63.58 12 Dereham in Mitford 43,605 12.03 353,955 223,631 63.18 362,376 208,125 57.43 21 Heacham & Rising 24,243 6.74 377,375 245,242 64.99 359,790 242,156 67.30 22 Holt 28,275 8.55 327,646 207,089 63.21 330,766 214,952 64.99 23 Lynn 10,805 3.30 330,152 196,022 59.37 326,964 187,510 57.35 07 Repps 0 0.00 383,729 278,123 72.48 382,728 285,790 74.67 03 08 Ingworth & Sparham 27,983 6.66 425,260 239,965 56.43 420,215 258,960 61.63 727,583 9.28 7,913,818 4,789,282 60.52 7,837,491 4,895,456 62.46 01/10/2019 NORWICH DIOCESAN BOARD OF FINANCE LTD DEANERY HISTORY REPORT MONTH September YEAR 2019 SUMMARY PARISH 2017 OUTST. -

Sheringham Coast Protection Scheme 2009

Document 7 - Sheringham Coast Protection Scheme The challenge of protecting the coast at Sheringham Facing due north, Sheringham has a well documented history of coming under fierce attack by storm surge seas. Northerly winds blowing across the sea all the way from the North Pole can generate severe storm waves, which must be resisted by the natural and man-made defences of the town. If these defences fail then considerable damage will be sustained. The first line of defence is the natural sand beach and shingle bank to the rear. These are reinforced by the man-made defences comprising groynes, promenades and sea walls, which act as the last line of defence in extreme conditions. In the late 1980’s there was great concern about the integrity of the coastal defences at Sheringham. Waves and tides had gradually removed the once-healthy beach from this exposed stretch of the North Norfolk coast allowing storm waves to attack the man-made defences inflicting considerable damage. The sea walls, groynes and promenades (first built during the last century) have fixed the alignment of the frontage at Sheringham. Consequently, whilst the cliffs to the east and west of Sheringham have continued to erode naturally, the promenades now jut out by up to 70m seaward of the natural coast line. The exposed position of the beaches and defences means they are subject to an ever-increasing wave attack. Research has shown that most beaches in North Norfolk including Sheringham are eroding, getting shorter and steeper allowing deeper water inshore to attack the man made defences. -

A Most Impressive & Beautifully Restored

A MOST IMPRESSIVE & BEAUTIFULLY RESTORED GRADE II LISTED COUNTRY HOUSE WOOD NORTON HALL WOOD NORTON, NORFOLK A MOST IMPRESSIVE AND BEAUTIFULLY RESTORED GRADE II LISTED COUNTRY HOUSE SET IN MANAGEABLE PARKLAND GARDENS WOOD NORTON HALL WOOD NORTON, NORFOLK Fakenham: 6 miles, Holt: 9 miles, Blakeney: 11 miles, Cley-next-the- Sea: 12 miles, Norwich: 20 miles. Ground floor: Reception hall w drawing room w dining room w ballroom/kitchen w playroom w pantry w cloakroom w utility room w cellar First floor: Gallery w master bedroom suite with en-suite bath/ shower room/dressing room w guest bedroom with shower room and cloakroom w further bedroom with adjoining bath/ shower room w office Second floor: Bedroom with en-suite shower room w 5 further bedrooms w bath/shower room Self-contained East Wing Ground floor: Sitting room w dining area w kitchen w WC First floor: 2 bedrooms w bathroom Outside: Mature gardens and grounds w hard tennis court w in all extending to 2.830 acres (est) The Property Wood Norton Hall is a most impressive Grade II listed country house, dating from the 17th century and set in magnificent mature gardens and grounds in a secluded and peaceful position on the edge of this popular and unspoilt North Norfolk village. The house dates from the 17th century and was acquired by the Norris family in 1780 when the house was substantially altered and enlarged. It was further altered and enlarged in the 19th century and was originally the centre of a big estate extending to 1,200 acres, which was eventually broken up in 1928. -

Norfolk Through a Lens

NORFOLK THROUGH A LENS A guide to the Photographic Collections held by Norfolk Library & Information Service 2 NORFOLK THROUGH A LENS A guide to the Photographic Collections held by Norfolk Library & Information Service History and Background The systematic collecting of photographs of Norfolk really began in 1913 when the Norfolk Photographic Survey was formed, although there are many images in the collection which date from shortly after the invention of photography (during the 1840s) and a great deal which are late Victorian. In less than one year over a thousand photographs were deposited in Norwich Library and by the mid- 1990s the collection had expanded to 30,000 prints and a similar number of negatives. The devastating Norwich library fire of 1994 destroyed around 15,000 Norwich prints, some of which were early images. Fortunately, many of the most important images were copied before the fire and those copies have since been purchased and returned to the library holdings. In 1999 a very successful public appeal was launched to replace parts of the lost archive and expand the collection. Today the collection (which was based upon the survey) contains a huge variety of material from amateur and informal work to commercial pictures. This includes newspaper reportage, portraiture, building and landscape surveys, tourism and advertising. There is work by the pioneers of photography in the region; there are collections by talented and dedicated amateurs as well as professional art photographers and early female practitioners such as Olive Edis, Viola Grimes and Edith Flowerdew. More recent images of Norfolk life are now beginning to filter in, such as a village survey of Ashwellthorpe by Richard Tilbrook from 1977, groups of Norwich punks and Norfolk fairs from the 1980s by Paul Harley and re-development images post 1990s. -

Contents of Volume 14 Norwich Marriages 1813-37 (Are Distinguished by Letter Code, Given Below) Those from 1801-13 Have Also Been Transcribed and Have No Code

Norfolk Family History Society Norfolk Marriages 1801-1837 The contents of Volume 14 Norwich Marriages 1813-37 (are distinguished by letter code, given below) those from 1801-13 have also been transcribed and have no code. ASt All Saints Hel St. Helen’s MyM St. Mary in the S&J St. Simon & St. And St. Andrew’s Jam St. James’ Marsh Jude Aug St. Augustine’s Jma St. John McC St. Michael Coslany Ste St. Stephen’s Ben St. Benedict’s Maddermarket McP St. Michael at Plea Swi St. Swithen’s JSe St. John Sepulchre McT St. Michael at Thorn Cle St. Clement’s Erh Earlham St. Mary’s Edm St. Edmund’s JTi St. John Timberhill Pau St. Paul’s Etn Eaton St. Andrew’s Eth St. Etheldreda’s Jul St. Julian’s PHu St. Peter Hungate GCo St. George Colegate Law St. Lawrence’s PMa St. Peter Mancroft Hei Heigham St. GTo St. George Mgt St. Margaret’s PpM St. Peter per Bartholomew Tombland MtO St. Martin at Oak Mountergate Lak Lakenham St. John Gil St. Giles’ MtP St. Martin at Palace PSo St. Peter Southgate the Baptist and All Grg St. Gregory’s MyC St. Mary Coslany Sav St. Saviour’s Saints The 25 Suffolk parishes Ashby Burgh Castle (Nfk 1974) Gisleham Kessingland Mutford Barnby Carlton Colville Gorleston (Nfk 1889) Kirkley Oulton Belton (Nfk 1974) Corton Gunton Knettishall Pakefield Blundeston Cove, North Herringfleet Lound Rushmere Bradwell (Nfk 1974) Fritton (Nfk 1974) Hopton (Nfk 1974) Lowestoft Somerleyton The Norfolk parishes 1 Acle 36 Barton Bendish St Andrew 71 Bodham 106 Burlingham St Edmond 141 Colney 2 Alburgh 37 Barton Bendish St Mary 72 Bodney 107 Burlingham -

NORTH NORFOLK 2 PCN Pharmacy Lead

North Norfolk PCN Please note this list is subject to change and is provided for Pharmacy Contractors in Norfolk/Suffolk to facilitate the process of organising communication and nomination of PCN Leads. The list is not final and should not be circulated for any purpose other than facilitating the organisation of Pharmacy PCNs/Leads. NORTH NORFOLK 1 PCN Pharmacy Lead: Geoff Ray Clinical Director: Email: [email protected] Contact Details: Pharmacy Details: Kelling Pharmacy, FWK09 GP Practices Pharmacies Holt Medical Practice David Jagger Ltd Sheringham Medical Practice Fakenham Pharmacy Wells Health Centre Kelling Pharmacy The Fakenham Medical Practice Lloyds Pharmacy Sheringham Well Fakenham - Holt Road Your Local Boots Pharmacy Sheringham Your Local Boots Pharmacy Fakenham Your Local Boots Pharmacy Holt NORTH NORFOLK 2 PCN Pharmacy Lead: Carrie Catchpole Clinical Director: Email: [email protected] Contact Details: Pharmacy Details: Boots North Walsham, FK436 GP Practices Pharmacies Cromer Group Practice Coastal Pharmacy Mundesley Medical Centre Cromer Pharmacy Birchwood Surgery Lloyds Pharmacy Cromer Paston Surgery North Walsham Pharmacy Aldborough Surgery Well North Walsham - Market Place Bacton Surgery Your Local Boots Pharmacy Cromer Your Local Boots Pharmacy North Walsham North Norfolk PCN Please note this list is subject to change and is provided for Pharmacy Contractors in Norfolk/Suffolk to facilitate the process of organising communication and nomination of PCN Leads. The list -

Norfolk Vanguard Offshore Wind Farm Consultation Report Appendix 20.3 Socc Stakeholder Mailing List

Norfolk Vanguard Offshore Wind Farm Consultation Report Appendix 20.3 SoCC Stakeholder Mailing List Applicant: Norfolk Vanguard Limited Document Reference: 5.1 Pursuant to APFP Regulation: 5(2)(q) Date: June 2018 Revision: Version 1 Author: BECG Photo: Kentish Flats Offshore Wind Farm This page is intentionally blank. Norfolk Vanguard Offshore Wind Farm Appendices Parish Councils Bacton and Edingthorpe Parish Council Witton and Ridlington Parish Council Brandiston Parish Council Guestwick Parish Council Little Witchingham Parish Council Marsham Parish Council Twyford Parish Council Lexham Parish Council Yaxham Parish Council Whinburgh and Westfield Parish Council Holme Hale Parish Council Bintree Parish Council North Tuddenham Parish Council Colkirk Parish Council Sporle with Palgrave Parish Council Shipdham Parish Council Bradenham Parish Council Paston Parish Council Worstead Parish Council Swanton Abbott Parish Council Alby with Thwaite Parish Council Skeyton Parish Council Melton Constable Parish Council Thurning Parish Council Pudding Norton Parish Council East Ruston Parish Council Hanworth Parish Council Briston Parish Council Kempstone Parish Council Brisley Parish Council Ingworth Parish Council Westwick Parish Council Stibbard Parish Council Themelthorpe Parish Council Burgh and Tuttington Parish Council Blickling Parish Council Oulton Parish Council Wood Dalling Parish Council Salle Parish Council Booton Parish Council Great Witchingham Parish Council Aylsham Town Council Heydon Parish Council Foulsham Parish Council Reepham -

The Cromer Moraine

THE CROMER MORAINE - A STUDY OF ITS PROGRESSIVE RECLAMATION ELIZABETH LANGTON ProQuest Number: 10097240 All rights reserved INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted. In the unlikely event that the author did not send a complete manuscript and there are missing pages, these will be noted. Also, if material had to be removed, a note will indicate the deletion. uest. ProQuest 10097240 Published by ProQuest LLC(2016). Copyright of the Dissertation is held by the Author. All rights reserved. This work is protected against unauthorized copying under Title 17, United States Code. Microform Edition © ProQuest LLC. ProQuest LLC 789 East Eisenhower Parkway P.O. Box 1346 Ann Arbor, Ml 48106-1346 ilBSTRAGT The Cromer Moraine forms a distinctive geographical region near the coast of the northern part of the County of Norfolk. A pro nounced characteristic of this region is the vridespread cover of heatb-land, far less extensive than in former times. This heathland appears in its turn to have developed from an original woodland cover which was destroyed by the depredations of man and his domesticated animals . It has been necessary first to delimit the region as accurately as possible and this has been accomplished by means of a detailed study of local topography and of well-sections. The earliest evidence of the location of heathland comes from tlie Domesday Survey and this has been confirmed by references to heathland in various other documents dovm to 1750. By the middle of the eighteenth century the new developments in agriculture^ or ’Norfolk Husbandry’ as it was called, became widely known and practised, resulting in this region in a greatly accelerated reclama tion of heathland; so that by the time of the Tithe Survey (183S-42) less than a hundred years later over 4000 acres of heath had been reclaimed. -

An Erasmian Pilgrimage to Walsingham

Peregrinations: Journal of Medieval Art and Architecture Volume 2 Issue 2 1-16 2007 An Erasmian Pilgrimage to Walsingham Gary Waller State University of New York, Purchase College Follow this and additional works at: https://digital.kenyon.edu/perejournal Part of the Ancient, Medieval, Renaissance and Baroque Art and Architecture Commons Recommended Citation Waller, Gary. "An Erasmian Pilgrimage to Walsingham." Peregrinations: Journal of Medieval Art and Architecture 2, 2 (2007): 1-16. https://digital.kenyon.edu/perejournal/vol2/iss2/4 This Feature Article is brought to you for free and open access by the Art History at Digital Kenyon: Research, Scholarship, and Creative Exchange. It has been accepted for inclusion in Peregrinations: Journal of Medieval Art and Architecture by an authorized editor of Digital Kenyon: Research, Scholarship, and Creative Exchange. For more information, please contact [email protected]. Waller 1 An Erasmian Pilgrimage to Walsingham By Gary Waller Professor of Literature, Cultural Studies and Drama Studies Purchase College, State University of New York In the summer of 2006, I undertook what I will explain was an ‘Erasmian’ pilgrimage to the Shrine of Our Lady of Walsingham, in remote northern Norfolk. I did so partly for scholarly purposes, partly from nostalgia for peregrinations there in student days. What I discovered--as in the case of so many folk who longen “to goon on pilgrimages”--was an unexpected measure of the uncanny and I think that fellow peregrinators, scholars and travelers alike, might be amused by sharing my discoveries. Erasmus, who made pilgrimages to Walsingham in 1512 and 1524, traveling (as I did) from Cambridge, gave a detailed, though fictionalized, description in one of the dialogues of his Colloquies.1 He went to Walsingham when it was England’s most important medieval Marian pilgrimage site, surpassed only by the shrine of St Thomas a Becket in Canterbury as the most popular place of pilgrimage in England,. -

North Norfolk District Council (Alby

DEFINITIVE STATEMENT OF PUBLIC RIGHTS OF WAY NORTH NORFOLK DISTRICT VOLUME I PARISH OF ALBY WITH THWAITE Footpath No. 1 (Middle Hill to Aldborough Mill). Starts from Middle Hill and runs north westwards to Aldborough Hill at parish boundary where it joins Footpath No. 12 of Aldborough. Footpath No. 2 (Alby Hill to All Saints' Church). Starts from Alby Hill and runs southwards to enter road opposite All Saints' Church. Footpath No. 3 (Dovehouse Lane to Footpath 13). Starts from Alby Hill and runs northwards, then turning eastwards, crosses Footpath No. 5 then again northwards, and continuing north-eastwards to field gate. Path continues from field gate in a south- easterly direction crossing the end Footpath No. 4 and U14440 continuing until it meets Footpath No.13 at TG 20567/34065. Footpath No. 4 (Park Farm to Sunday School). Starts from Park Farm and runs south westwards to Footpath No. 3 and U14440. Footpath No. 5 (Pack Lane). Starts from the C288 at TG 20237/33581 going in a northerly direction parallel and to the eastern boundary of the cemetery for a distance of approximately 11 metres to TG 20236/33589. Continuing in a westerly direction following the existing path for approximately 34 metres to TG 20201/33589 at the western boundary of the cemetery. Continuing in a generally northerly direction parallel to the western boundary of the cemetery for approximately 23 metres to the field boundary at TG 20206/33611. Continuing in a westerly direction parallel to and to the northern side of the field boundary for a distance of approximately 153 metres to exit onto the U440 road at TG 20054/33633. -

Norfolk Gardens 2011

Norfolk Gardens 2011 Sponsored by The National Gardens Scheme www.ngs.org.uk NATIONAL GARDENS SCHEME ! BAGTHORPE HALL $ BANK FARM 1 Bagthorpe PE31 6QY. Mr & Mrs D Morton. 3 /2 m N of Fallow Pipe Road, Saddlebow, Kings Lynn PE34 3AS. East Rudham, off A148. At King’s Lynn take A148 to Mr & Mrs Alan Kew. 3m S of Kings Lynn. Turn off Kings Fakenham. At East Rudham (approx 12m) turn L opp The Lynn southern bypass (A47) via slip rd signed St Germans. 1 Crown, 3 /2 m into hamlet of Bagthorpe. Farm buildings on Cross river in Saddlebow village. 1m fork R into Fallow 1 L, wood on R, white gates set back from road, at top of Pipe Rd. Farmhouse /4 m by River Great Ouse. Home- drive. Home-made teas. Adm £3.50, chd free. Sun 20 made teas. Adm £3, chd free. Sun 10 July (11-5). 3 Feb (11-4). /4 -acre windswept garden was created from a field in Snowdrops carpeting woodland walk. 1994. A low maintenance garden of contrasts, filled with f g a b trees, shrubs and newly planted perennials. Many features include large fish pond, small vegetable garden with greenhouse. Splashes of colour from annuals. Walks along the banks of Great Ouse. Dogs on leads. Wood turning demonstration by professional wood turner. Short gravel entrance. Cover garden: Dale Farm, Dereham e f g b Photographer: David M Jones # BANHAMS BARN Browick Road, Wymondham NR18 9RB. Mr C Cooper % 5 BATTERBY GREEN & Mrs J Harden. 1m E of Wymondham. A11 from Hempton, Fakenham NR21 7LY. -

PLACES to STAY Hotels

. PLACES TO STAY We are pleased to provide visitors to the school with a list of local accommodation from bed and breakfasts to self- catering accommodation which you may wish to consider to help you plan your visit. This is not an advertising feature. Preferential rates or offers are available where indicated by an , please advise the hotel/B&B when booking that you are visiting Gresham’s to take advantage of these. Hotels Byford’s Cliftonville Hotel, Cromer A ‘posh B&B’ located in the heart of Holt. Indulge in Edwardian Elegance on the North Norfolk Seafront. From £165 per night, including breakfast From £90 bed and breakfast +44 1263 711400 +44 1263 512543 www.byfords.org.uk www.cliftonvillehotel.co.uk [email protected] [email protected] The Dales Country House Hotel The Blakeney White Horse A peaceful country manor in nearby One of the regions foremost small hotels. Sheringham. From £130 per night From £99 per room +44 1263 824555 +44 1263 740574 www.mackenziehotels.com www.blakeneywhitehorse.co.uk [email protected] [email protected] Felbrigg Lodge The Links Country Park Hotel A quiet boutique hotel. Country Park Hotel and Golf Club. From £179 for 2 people sharing per night From £100 per night +44 1263 666 010 +44 1263 838383 www.felbrigglodge.co.uk www.links-hotel.co.uk [email protected] [email protected] The Sea Marge Hotel The Pheasant Hotel Luxurious family hotel. Located in Kelling, 5 minutes’ drive from Greshams School. From £130 per night From £190 per night (B&B) +44 1263 579579 + 44 1263 588382 www.seamargehotel.co.uk www.pheasanthotelnorfolk.co.uk [email protected] [email protected] The Stiffkey Red Lion The Crown Hotel “An old English inn…with the comfort of a An elegant hotel in nearby Wells-next-the-sea.