Suncor Energy – Annual Report 2006

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Exhibits and Financial Statement Schedules 149

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K [ X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2011 OR [ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission File Number 1-16417 NUSTAR ENERGY L.P. (Exact name of registrant as specified in its charter) Delaware 74-2956831 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) 2330 North Loop 1604 West 78248 San Antonio, Texas (Zip Code) (Address of principal executive offices) Registrant’s telephone number, including area code (210) 918-2000 Securities registered pursuant to Section 12(b) of the Act: Common units representing partnership interests listed on the New York Stock Exchange. Securities registered pursuant to 12(g) of the Act: None. Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [X] No [ ] Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X] Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Initial Project Description Summary

SUNCOR ENERGY INC. Base Mine Extension INITIAL PROJECT DESCRIPTION SUMMARY February 2020 SUNCOR ENERGY INC. Base Mine Extension - Initial Project Description Summary February 2020 This Page Intentionally Left Blank SUNCOR ENERGY INC. Base Mine Extension - Initial Project Description Summary February 2020 EXECUTIVE SUMMARY Suncor Energy Inc. (Suncor) is submitting a proposal to develop the Base Mine Extension Project (the Project). All plausible pathways to address global emissions need energy from fossil fuels and Suncor views Canada’s world class, strategic oil sands resource as a key part of the energy future for decades to come. Commensurate with Canada’s ambitions, Suncor is committed to a long-term strategy of reducing absolute emissions. With the innovation we are known for, Suncor can provide the world with trusted low carbon energy. Suncor has invested billions of dollars in infrastructure that produces value added products to meet the energy needs of Albertans and Canadians. This Project is necessary to continue to add value with this infrastructure. The bitumen from this project will be used to supply the existing upgraders at Suncor’s Oil Sands Base Plant operations (Base Plant), when the existing mines are depleted. The Project is adjacent to Base Plant and includes an open pit mining operation and extraction facilities. Production is expected to be nominally 225 thousand barrels per day of replacement bitumen during its estimated 25-year operational life. The Project application will be based on best-available technology. In parallel, Suncor is developing new technologies, such as non-aqueous extraction. These new technologies have the potential to significantly reduce the overall footprint, reclamation timeline, and GHG emissions of mining and will be incorporated as appropriate. -

Suncor Q3 2020 Investor Relations Supplemental Information Package

SUNCOR ENERGY Investor Information SUPPLEMENTAL Published October 28, 2020 SUNCOR ENERGY Table of Contents 1. Energy Sources 2. Processing, Infrastructure & Logistics 3. Consumer Channels 4. Sustainability 5. Technology Development 6. Integrated Model Calculation 7. Glossary SUNCOR ENERGY 2 SUNCOR ENERGY EnergyAppendix Sources 3 202003- 038 Oil Sands Energy Sources *All values net to Suncor In Situ Mining Firebag Base Plant 215,000 bpd capacity 350,000 bpd capacity Suncor WI 100% Suncor WI 100% 2,603 mmbbls 2P reserves1 1,350 mmbbls 2P reserves1 Note: Millennium and North Steepank Mines do not supply full 350,000 bpd of capacity as significant in-situ volumes are sent through Base Plant MacKay River Syncrude 38,000 bpd capacity Syncrude operated Suncor WI 100% 205,600 bpd net coking capacity 501 mmbbls 2P reserves1 Suncor WI 58.74% 1,217 mmbbls 2P reserves1 Future opportunities Fort Hills ES-SAGD Firebag Expansion Suncor operated Lewis (SU WI 100%) 105,000 bpd net capacity Meadow Creek (SU WI 75%) Suncor WI 54.11% 1,365 mmbbls 2P reserves1 First oil achieved in January 2018 SUNCOR ENERGY 1 See Slide Notes and Advisories. 4 1 Regional synergy opportunities for existing assets Crude logistics Upgrader feedstock optionality from multiple oil sands assets Crude feedstock optionality for Edmonton refinery Supply chain Sparing, warehousing & supply chain management Consolidation of regional contracts (lodging, busing, flights, etc.) Operational optimizations Unplanned outage impact mitigations In Situ Turnaround planning optimization Process -

Valero Port Arthur Refinery Presents $750000 to Local Children's Charities

FOR IMMEDIATE RELEASE: VALERO PORT ARTHUR REFINERY PRESENTS $750,000 TO LOCAL CHILDREN’S CHARITIES Despite tournament’s cancellation, community support endures PORT ARTHUR, Texas, October 9, 2020 — The COVID-19 pandemic canceled the Valero Texas Open, like it did so many prominent events across the country, but it didn’t stop the tournament’s legacy of giving back. Business partners, sponsors and individual donors of the tournament and related events including the Valero Benefit for Children still contributed more than $14 million in net proceeds for charitable organizations across the United States, including those in the Port Arthur area. The Valero Port Arthur Refinery will distribute $750,000 to local charities with funds raised through the Valero Energy Foundation and the 2020 Valero Texas Open and Benefit for Children. “This is really positive news for our local nonprofit organizations, many of whom are facing challenges as a result of the pandemic,” said Mark Skobel, Vice President and General Manager of the Valero Port Arthur Refinery. “We know how important it is to continue supporting these agencies and the work they do for the children in our community.” The 2020 Valero Benefit for Children local recipients are: • Port Arthur Independent School District • Gulf Coast Health Center • YMCA of Southeast Texas • Communities in Schools of Southeast Texas • CASA of Southeast Texas • Southeast Texas Food Bank • Garth House, Mickey Mehaffy Children’s Advocacy Program • Richard Shorkey Education and Rehabilitation Center “We are blessed by our long-standing relationships with our tournament and Benefit for Children top sponsors,” said Joe Gorder, Valero Chairman and Chief Executive Officer. -

Suncor Energy – Investor Presentation 2019 Q1

INVESTOR INFORMATION Q1 2019 Published May 1, 2019 2 Canada’s leading integrated energy company $85B ~940 mbpd ~600 mbpd 28+ years ~460 mbpd ~1750 1 Oil production Heavy upgrading 2P Reserve life Refining nameplate Enterprise value Retail sites4 As at March 31, 2019 nameplate capacity2 nameplate capacity2 index3 capacity2 1, 2, 3, 4 See Slide Notes and Advisories 3 Suncor – A resilient business focused on shareholder returns Cash flow growth Cash generation Strong potential FFO1 increase largely independent of market conditions Significant upside FFO1 sensitivity to WTI, based on TTM5 actuals US$62.80 WTI, 0.76 C$/US$, US$18.00 NYH 3-2-1 crack spread 2 (C$ billion) ~5% CAGR (Based on 2019 price guidance) $16 $14 TTM average production 750 mbbls/d $12 Debottlenecks, $10 cost reductions $8 Fort Hills, and margin Syncrude, improvements $6 and Hebron $4 $5.5B Sustaining capital6 + dividend $2 $2.8B Sustaining capital6 $0 2018 FFO1 Production Free funds flow 2023E FFO1 $60 $63 $70 $75 $80 growth 3 growth4 TTM WTI ($USD) Shareholder returns Resilience Commitment to reliable returns through the commodity cycles Managing the balance sheet as a strategic asset Dividend per share7 Liquidity Buyback per share7,8,9 Anticipated buyback per share7,9 7% $5.3B $1.9B cash and $3.4B in available lines of credit Dividend + buyback yield As at March 31, 2019 — 5% 5% A low Credit rating 1.88 Investment grade 0.85 DBRS (A Low) Stable, S&P(A-) stable, Moody’s (Baa1) Stable 1.14 3% 3% Baa1 WTI FFO Break-Even10 (USD) 1.02 1.14 1.16 1.28 1.44 1.68 ~$45 Sustaining capital6 + dividend 2014 2015 2016 2017 2018 2019E 2019 1, 2, 3, 4, 5, 6, 7, 8, 9, 10 See Slide Notes and Advisories. -

Suncor Energy Announces Successful Acquisition of 72.9% of Canadian Oil Sands Shares

News Release FOR IMMEDIATE RELEASE Suncor Energy announces successful acquisition of 72.9% of Canadian Oil Sands shares (All dollar amounts referenced are in Canadian dollars) Calgary, Alberta (Feb. 5, 2016) – Suncor announced today that approximately 72.9 per cent of Canadian Oil Sands shares (“COS”) equating to 353,307,264 common shares and accompanying rights have been tendered to Suncor's Offer. Suncor will take up all tendered shares and those shares will be paid for in accordance with the terms of the Offer, initially made October 5, 2015 and most recently amended January 22, 2016. All shares tendered were held by "Independent Shareholders" as such term is defined by the COS shareholder rights plan dated December 31, 2010 as amended April 30, 2013 (the “COS Rights Plan”). “We’re pleased with the strong level of support from COS shareholders,” said Steve Williams, president and chief executive officer. “From the outset, we’ve spoken about the excellent value this offer creates for both COS and Suncor shareholders and I’m looking forward to delivering on that commitment.” In accordance with the "Permitted Bid" requirements of the COS Rights Plan and the terms of the Offer, Suncor has extended its Offer to Monday, February 22, 2016 at 5:00 p.m. MT (7:00 p.m. ET) so that COS shareholders who have not yet tendered their shares can do so. Further extensions beyond February 22, 2016 are not anticipated. COS shareholders who tendered to the Offer will receive 0.28 of a common share of Suncor for each share, which will be paid in accordance with the terms of the Offer. -

Facts About Alberta's Oil Sands and Its Industry

Facts about Alberta’s oil sands and its industry CONTENTS Oil Sands Discovery Centre Facts 1 Oil Sands Overview 3 Alberta’s Vast Resource The biggest known oil reserve in the world! 5 Geology Why does Alberta have oil sands? 7 Oil Sands 8 The Basics of Bitumen 10 Oil Sands Pioneers 12 Mighty Mining Machines 15 Cyrus the Bucketwheel Excavator 1303 20 Surface Mining Extraction 22 Upgrading 25 Pipelines 29 Environmental Protection 32 In situ Technology 36 Glossary 40 Oil Sands Projects in the Athabasca Oil Sands 44 Oil Sands Resources 48 OIL SANDS DISCOVERY CENTRE www.oilsandsdiscovery.com OIL SANDS DISCOVERY CENTRE FACTS Official Name Oil Sands Discovery Centre Vision Sharing the Oil Sands Experience Architects Wayne H. Wright Architects Ltd. Owner Government of Alberta Minister The Honourable Lindsay Blackett Minister of Culture and Community Spirit Location 7 hectares, at the corner of MacKenzie Boulevard and Highway 63 in Fort McMurray, Alberta Building Size Approximately 27,000 square feet, or 2,300 square metres Estimated Cost 9 million dollars Construction December 1983 – December 1984 Opening Date September 6, 1985 Updated Exhibit Gallery opened in September 2002 Facilities Dr. Karl A. Clark Exhibit Hall, administrative area, children’s activity/education centre, Robert Fitzsimmons Theatre, mini theatre, gift shop, meeting rooms, reference room, public washrooms, outdoor J. Howard Pew Industrial Equipment Garden, and Cyrus Bucketwheel Exhibit. Staffing Supervisor, Head of Marketing and Programs, Senior Interpreter, two full-time Interpreters, administrative support, receptionists/ cashiers, seasonal interpreters, and volunteers. Associated Projects Bitumount Historic Site Programs Oil Extraction demonstrations, Quest for Energy movie, Paydirt film, Historic Abasand Walking Tour (summer), special events, self-guided tours of the Exhibit Hall. -

Suncor Energy – Annual Report 2005

Suncor05ARcvr 3/8/06 1:33 PM Page 1 SUNCOR ENERGY INC. 2005 ANNUAL REPORT > growing strategically Suncor’s large resource base, growing production capacity and access to the North American energy market are the foundation of an integrated strategy aimed at driving profitable growth, a solid return on capital investment and strong returns for our shareholders. A staged approach to increasing our crude oil production capacity allows Suncor to better manage capital costs and incorporate new ideas and new technologies into our facilities. production 50,000 bpd 110,000 bpd (capacity) resources Third party bitumen 225,000 bpd Mining 260,000 bpd 350,000 bpd 500,000 bpd In-situ 500,000 – 550,000 bpd OUR PLANS TO GROW TO HALF A MILLION BARRELS PER DAY IN 2010 TO 2012* x Tower Natural gas Vacuum 1967 – Upgrader 1 1998 – Expand Upgrader 1, Vacuum Tower Future downstream integrat 2001 – Upgrader 2 Other customers 2005 – Expand Upgrader 2, 2008 – Further Expansion of Upgrader 2 2010-2012 – Upgrader 3 Denver refinery ion Sarnia refinery markets To provide greater North American markets reliability and flexibility to our feedstock supplies, we produce bitumen through our own mining and in-situ recovery technologies, and supplement that supply through innovative third-party agreements. Suncor takes an active role in connecting supply to consumer demand with a diverse portfolio of products, downstream assets and markets. Box 38, 112 – 4th Avenue S.W., Calgary, Alberta, Canada T2P 2V5 We produce conventional natural Our investments in renewable wind tel: (403) 269-8100 fax: (403) 269-6217 [email protected] www.suncor.com gas as a price hedge against the energy are a key part of Suncor’s cost of energy consumption. -

Foreign Investment in the Oil Sands and British Columbia Shale Gas

Canadian Energy Research Institute Foreign Investment in the Oil Sands and British Columbia Shale Gas Jon Rozhon March 2012 Relevant • Independent • Objective Foreign Investment in the Oil Sands and British Columbia Shale Gas 1 Foreign Investment in the Oil Sands There has been a steady flow of foreign investment into the oil sands industry over the past decade in terms of merger and acquisition (M&A) activity. Out of a total CDN$61.5 billion in M&A’s, approximately half – or CDN$30.3 billion – involved foreign companies taking an ownership stake. These funds were invested in in situ projects, integrated projects, and land leases. As indicated in Figure 1, US and Chinese companies made the most concerted efforts to increase their profile in the oil sands, investing 2/3 of all foreign capital. The US and China both invested in a total of seven different projects. The French company, Total SA, has also spread its capital around several projects (four in total) while Royal Dutch Shell (UK), Statoil (Norway), and PTT (Thailand) each opted to take large positions in one project each. Table 1 provides a list of all foreign investments in the oil sands since 2004. Figure 1: Total Oil Sands Foreign Investment since 2003, Country of Origin Korea 1% Thailand Norway 6% UK 7% 2% US France 33% 18% China 33% Source: Canoils. Foreign Investment in the Oil Sands and British Columbia Shale Gas 2 Table 1: Oil Sands Foreign Investment Deals Year Country Acquirer Brief Description Total Acquisition Cost (000) 2012 China PetroChina 40% interest in MacKay River 680,000 project from AOSC 2011 China China National Offshore Acquisition of OPTI Canada 1,906,461 Oil Corporation 2010 France Total SA Alliance with Suncor. -

Chevron Unocal Analysis

ANALYSIS OF PROPOSED CONSENT ORDER TO AID PUBLIC COMMENT IN THE MATTER OF CHEVRON CORPORATION AND UNOCAL CORPORATION, FILE NO. 051-0125 I. Introduction The Federal Trade Commission (“Commission” or “FTC”) has issued a complaint (“Complaint”) alleging that the proposed merger of Chevron Corporation (“Chevron,” formerly ChevronTexaco Corporation) and Unocal Corporation (“Unocal”) (collectively “Respondents”) would violate Section 7 of the Clayton Act, as amended, 15 U.S.C. § 18, and Section 5 of the Federal Trade Commission Act, as amended, 15 U.S.C. § 45, and has entered into an agreement containing consent order (“Agreement Containing Consent Order”) pursuant to which Respondents agree to be bound by a proposed consent order (“Proposed Consent Order”). The Proposed Consent Order remedies the likely anticompetitive effects arising from Respondents’ proposed merger, as alleged in the Complaint. II. Description of the Parties and the Transaction A. Chevron Chevron is a major international energy firm with operations in North America and about 180 foreign countries in Europe, Africa, South America, Central America, Indonesia, and the Asia-Pacific region. Its petroleum operations consist of exploring for, developing and producing crude oil and natural gas; refining crude oil into finished petroleum products; marketing crude oil, natural gas, and various finished products derived from petroleum; and transporting crude oil, natural gas, and finished petroleum products by pipeline, marine vessels, and other means. The company operates light petroleum refineries for products such as gasoline, jet fuel, kerosene and fuel oil at Pascagoula, Mississippi; El Segundo, California; Richmond, California; Salt Lake City, Utah; and Kapolei, Hawaii. Chevron is a major refiner and marketer of gasoline that meets the requirements of the California Air Resources Board (“CARB”). -

News Release – the New Suncor Energy

News Release FOR IMMEDIATE RELEASE Suncor Energy reports second quarter 2021 results Unless otherwise noted, all financial figures are unaudited, presented in Canadian dollars (Cdn$), and have been prepared in accordance with International Financial Reporting Standards (IFRS), specifically International Accounting Standard (IAS) 34 Interim Financial Reporting as issued by the International Accounting Standards Board. Production volumes are presented on a working-interest basis, before royalties, except for production values from the company's Libya operations, which are presented on an economic basis. Certain financial measures referred to in this news release (funds from operations, operating earnings (loss) and free funds flow) are not prescribed by Canadian generally accepted accounting principles (GAAP). See the Non-GAAP Financial Measures section of this news release. References to Oil Sands operations exclude Suncor Energy Inc.’s interest in Fort Hills and Syncrude. Calgary, Alberta (July 28, 2021) – “Suncor generated $2.4 billion in funds from operations in the quarter while also completing significant turnaround activities in the upstream and downstream businesses,” said Mark Little, president and chief executive officer. “The improved cash generation enabled us to increase shareholder returns to approximately $1.0 billion, representing approximately 40% of our funds from operations and we’re targeting further debt reduction in the latter half of the year in line with our previously announced capital allocation strategy.” • Funds from operations increased to $2.362 billion ($1.57 per common share) in the second quarter of 2021, compared to $488 million ($0.32 per common share) in the prior year quarter. Cash flow provided by operating activities, which includes changes in non-cash working capital, was $2.086 billion ($1.39 per common share) in the second quarter of 2021, compared to cash flow used in operating activities of $768 million ($0.50 per common share) in the prior year quarter. -

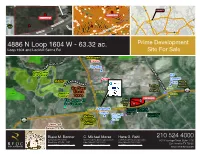

10 4886 N Loop 1604 W

1 02 2 4 9 1 2 0 26 8 10 0 24 4 1 1 0 024 22 1 1024 9 8 6 Hope Center Church 1 9 022 8 1 8 1 0 L 0 2 1 2 L Budget Blinds, Lush Rooftop, Amore Cafe, 1 0 0 L 0 E 8 L Rodrigo Pinheiro BJJ, Pure Fun, Picks Bar, E M 1 M 1022 0 U 0 The Brazilian Capoeira Academy: San Antonio 4 2 9 9 U 4 9 O 2 10 9 2 O L 4 1 L 0 2 10 1 0 00 1 1 2 0 0 4 1 Æþ281 10 022 1 10 00 10 2 06 1020 1 1 8 0 1 06 0 0 0 0 1 1 0 1100 4 !$" 2 # 16 SUBJECT 10 1014 BBQ 2 012 00 1 1 1 0 0 08 Outfitters 4 10 B 2 9 9 2 1000 Not100 Available B Ridge Shopping 99 8 990 Center 996 9 994 9 Not Available 2 9 1604 86 UV 9 1 8 1 4 0 1 0 3355 4 0 !$" 2 # 2 1 4 3 4 0 1 4 0 6 4 0 3 1 0 2 D 8 9 8 1604 R 4 82 9 S 3 UV S 0 E 1 CC UV53 0 A 3 1 0 0 W 1 0 90 4 2 98 9 2 6 0 98 0 8 2 992 Teralta 6 2 10 281 1 0 994 Æþ P V 1 6 218 O 84 8 UV 9 16 O I 80 9 UV L A 9 88 4 Corporate N 9 82 4 9 96 98 1100 98 00 9 #$!" S 10 98 A 32 A D 9 H 10 R Park A S S 02 V CE 10 1604 AC 04 AN 10 UV O W 1008 6 v 4 0 60 10 978 537 1 1 1 UV 0 0 0 OP 10 8 0 O 0 6 6 L 2 1 9 97 W 10 N 01 7 4 10 1 8 1604 60 1 1 0 UV W 6 OP 3 04 98 441100 LO 6 P 16 #$!" N LOO 6 L 4 12 101 N 9 97 L 10 O 76 014 O 1 1 C 0 345 C 3 K UV 8 1604 980 K UV H 0 v 102 1018 H H.E.B Federal IL 9 8 2 8 I 102 2 L 2 441100 02 7 L 1 - 9 #$!" 368 1020 S 9 UV L 8 Credit Union E 0 - 4 S 4 102 L 4 3355 University Oaks 102 26 8 9 $!" 10 30 # E 10 6 M 4 8 L 2 A 9 9 10 0 8 M 32 1 6 Camp Bullis Church of Christ R 9 A 1034 D 9 8 8 8 R 8 Subject D 103 K 421 1 8 1036 A UV 04 K 0 8 O A 2 Y 2 Ft Elevation Lines 4 0 O T 9 7 1 I 7 9 Y 1 BACON RD S 8 0 BACON RD T 4 R 100 Year FEMA Floodplain I 2 E S 1 1 Prime Development V 0 I R 0 1604 4 N 6 1100 E 2 97 151 " 4 UV #$! 6 U 9 UV 8 [email protected] PPIVG Paints 990 0 N Apria CBD 4886 N LoopU 1604 W - 63.32 ac.