Chapter V – Compliance Audit Paragraphs

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

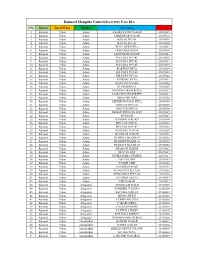

Kurnool Mosquito Control Secretary User Id's

Kurnool Mosquito Control Secretary User Id's S.No District Rural/Urban Mandal Secretariat Username 1 Kurnool Urban Adoni AMARAVATHI NAGAR 21015035 2 Kurnool Urban Adoni AMBEDKAR NAGAR 21015016 3 Kurnool Urban Adoni BAVAJI PET-01 21015002 4 Kurnool Urban Adoni BAVAJI PET-02 21015004 5 Kurnool Urban Adoni BOYA GERI PETA 21015032 6 Kurnool Urban Adoni GOKHARJHANDA 21015003 7 Kurnool Urban Adoni HANUMAN NAGAR 21015041 8 Kurnool Urban Adoni HAVANA PET-01 21015010 9 Kurnool Urban Adoni HAVANA PET-02 21015013 10 Kurnool Urban Adoni HAVANA PET-03 21015015 11 Kurnool Urban Adoni KARWAN PETA 21015014 12 Kurnool Urban Adoni KILICHIN PET-01 21015038 13 Kurnool Urban Adoni KILICHIN PET-02 21015040 14 Kurnool Urban Adoni KOWDAL PETA 21015011 15 Kurnool Urban Adoni KRANTHI NAGAR 21015024 16 Kurnool Urban Adoni KUNIMOHALA 21015007 17 Kurnool Urban Adoni MADHAVARAM ROAD 21015037 18 Kurnool Urban Adoni MARATHVADI STREET 21015031 19 Kurnool Urban Adoni MEDHARI GIRI 21015036 20 Kurnool Urban Adoni METHR MOSQUE PETA 21015009 21 Kurnool Urban Adoni NGO COLONY-01 21015005 22 Kurnool Urban Adoni NGO COLONY-02 21015008 23 Kurnool Urban Adoni NIZAMUDDIN COLONY 21015039 24 Kurnool Urban Adoni PN ROAD 21015027 25 Kurnool Urban Adoni RAMJEELA ROAD 21015006 26 Kurnool Urban Adoni RTC COLONY-01 21015018 27 Kurnool Urban Adoni RTC COLONY-02 21015019 28 Kurnool Urban Adoni SAI BABA NAGAR 21015020 29 Kurnool Urban Adoni SHANKAR NAGAR 21015023 30 Kurnool Urban Adoni SHAROFF BAZAR-01 21015028 31 Kurnool Urban Adoni SHAROFF BAZAR-02 21015029 32 Kurnool Urban Adoni SHAROFF -

PROFILE of ANANTAPUR DISTRICT the Effective Functioning of Any Institution Largely Depends on The

PROFILE OF ANANTAPUR DISTRICT The effective functioning of any institution largely depends on the socio-economic environment in which it is functioning. It is especially true in case of institutions which are functioning for the development of rural areas. Hence, an attempt is made here to present a socio economic profile of Anantapur district, which happens to be one of the areas of operation of DRDA under study. Profile of Anantapur District Anantapur offers some vivid glimpses of the pre-historic past. It is generally held that the place got its name from 'Anantasagaram', a big tank, which means ‘Endless Ocean’. The villages of Anantasagaram and Bukkarayasamudram were constructed by Chilkkavodeya, the Minister of Bukka-I, a Vijayanagar ruler. Some authorities assert that Anantasagaram was named after Bukka's queen, while some contend that it must have been known after Anantarasa Chikkavodeya himself, as Bukka had no queen by that name. Anantapur is familiarly known as ‘Hande Anantapuram’. 'Hande' means chief of the Vijayanagar period. Anantapur and a few other places were gifted by the Vijayanagar rulers to Hanumappa Naidu of the Hande family. The place subsequently came under the Qutub Shahis, Mughals, and the Nawabs of Kadapa, although the Hande chiefs continued to rule as their subordinates. It was occupied by the Palegar of Bellary during the time of Ramappa but was eventually won back by 136 his son, Siddappa. Morari Rao Ghorpade attacked Anantapur in 1757. Though the army resisted for some time, Siddappa ultimately bought off the enemy for Rs.50, 000. Anantapur then came into the possession of Hyder Ali and Tipu Sultan. -

Reg. No Name in Full Residential Address Gender Contact No. Email Id Remarks 9421864344 022 25401313 / 9869262391 Bhaveshwarikar

Reg. No Name in Full Residential Address Gender Contact No. Email id Remarks 10001 SALPHALE VITTHAL AT POST UMARI (MOTHI) TAL.DIST- Male DEFAULTER SHANKARRAO AKOLA NAME REMOVED 444302 AKOLA MAHARASHTRA 10002 JAGGI RAMANJIT KAUR J.S.JAGGI, GOVIND NAGAR, Male DEFAULTER JASWANT SINGH RAJAPETH, NAME REMOVED AMRAVATI MAHARASHTRA 10003 BAVISKAR DILIP VITHALRAO PLOT NO.2-B, SHIVNAGAR, Male DEFAULTER NR.SHARDA CHOWK, BVS STOP, NAME REMOVED SANGAM TALKIES, NAGPUR MAHARASHTRA 10004 SOMANI VINODKUMAR MAIN ROAD, MANWATH Male 9421864344 RENEWAL UP TO 2018 GOPIKISHAN 431505 PARBHANI Maharashtra 10005 KARMALKAR BHAVESHVARI 11, BHARAT SADAN, 2 ND FLOOR, Female 022 25401313 / bhaveshwarikarmalka@gma NOT RENEW RAVINDRA S.V.ROAD, NAUPADA, THANE 9869262391 il.com (WEST) 400602 THANE Maharashtra 10006 NIRMALKAR DEVENDRA AT- MAREGAON, PO / TA- Male 9423652964 RENEWAL UP TO 2018 VIRUPAKSH MAREGAON, 445303 YAVATMAL Maharashtra 10007 PATIL PREMCHANDRA PATIPURA, WARD NO.18, Male DEFAULTER BHALCHANDRA NAME REMOVED 445001 YAVATMAL MAHARASHTRA 10008 KHAN ALIMKHAN SUJATKHAN AT-PO- LADKHED TA- DARWHA Male 9763175228 NOT RENEW 445208 YAVATMAL Maharashtra 10009 DHANGAWHAL PLINTH HOUSE, 4/A, DHARTI Male 9422288171 RENEWAL UP TO 05/06/2018 SUBHASHKUMAR KHANDU COLONY, NR.G.T.P.STOP, DEOPUR AGRA RD. 424005 DHULE Maharashtra 10010 PATIL SURENDRANATH A/P - PALE KHO. TAL - KALWAN Male 02592 248013 / NOT RENEW DHARMARAJ 9423481207 NASIK Maharashtra 10011 DHANGE PARVEZ ABBAS GREEN ACE RESIDENCY, FLT NO Male 9890207717 RENEWAL UP TO 05/06/2018 402, PLOT NO 73/3, 74/3 SEC- 27, SEAWOODS, -

Unauthorised Layout Details

REGIONAL DEPUTY DIRECTOR OF TOWN AND COUNTRAY PLANNING, VISAKHAPATNAM DETAILS OF UNAUTHORIZED LAYOUTS IN URBAN LOCAL BODIES Details of unauthorised Layouts Name of Approx. Year Status of Layout development of Road subdivision Water Sl. No. Name of of ULB Sy.No. & formation Drains Electricity Width of % of Open space if Extent in Ac. Developer Owner of Supply No. of Plots Remakrs Village Gravel/W.B. (Y/N) (Y/N) Roads available land/unautho (Y/N) M/BT/ CC rised layout) 1 Srikakulam 2 Amadalavalasa Plot stones 104&105 1 5.00 S.Tagore - 7 Gravel No No No 168 30`0" - removed by Chintada Department 66&67 T.Bangaru 2 0.45 - 6 - NoNoNo 20 - - Do Akkivalasa Raju 158,159,171&1 3 72 2.50 - - 7 - NoNo No 90 - - Do Akkivalasa 67&68 K.Uma 4 0.50 maheswara - 7 - NoNoNo 14 - - Do Amadalavalas Rao a 2,4,26,27&31 5 1.00 B.Ramana - 6 - No No No 25 - - Do Amadalavalas a 11,12,13,16,21,2 2& 24, S.Seetaram & 6 1.30 - 8 - NoNoNo 30 - - Do Amadalavalas others a 3 Palasa-Kasibugga Bammidi Removal of 211 of 1 1.00 - Simhachalam & 2015 Gravel N N N - - - boundary stones Narsipuram Other and distrub road Removal of 149 of Sanapala 2 0.80 - 2014 Gravel N N N - - - boundary stones Chinabadam Padmalochalna and distrub road Removal of 158 of K Sankara Rao & 3 0.85 - 2014 Gravel N N N - - - boundary stones Chinabadam Others and distrub road Removal of 158 of 4 1.00 - Unknown Perosons 2012 Gravel N N N - - - boundary stones Chinabadam and distrub road Removal of 160 of B Nagaraju & 5 0.70 - 2013 Gravel N N N - - - boundary stones Chinabadam Others and distrub road Removal -

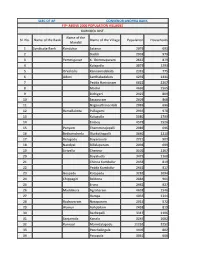

SI. No. Name of the Bank Name of the Mandal Name of the Village

SLBC OF AP CONVENOR:ANDHRA BANK FIP- ABOVE 2000 POPULATION VILLAGES KURNOOL DIST. Name of the SI. No. Name of the Bank Name of the Village Population Households Mandal 1 Syndicate Bank Kandukur Satanur 2079 693 2 Duddi 2938 979 3 Yemmiganur K. Thimmapuram 2637 879 4 Kolagatla 3879 1293 5 Orvakallu Kannamadakala 2326 775 6 Adoni Santhakadaluru 4292 1431 7 Pedda Harivanam 6622 2207 8 Madivi 4696 1565 9 Bichigeri 2427 809 10 Sasapuram 2603 868 11 Naganathana Halli 2089 696 12 Ramallakota Pullagami 2935 978 13 Kulugutla 5380 1793 14 Emboy 4578 1526 15 Panyam Thammarajupalli 2089 696 16 Bethamcherla Illurkothapalli 3640 1213 17 Velugodu Boyarevula 2721 907 18 Nandyal Billalapuram 2098 699 19 Sirivella Chennur 3502 1167 20 Boyakutla 3479 1160 21 Chinna Kumbulur 2458 819 22 Pedda Kumbulur 2452 817 23 Gospadu Kotapadu 3282 1094 24 Chippagiri Beldona 2884 961 25 Eruru 2482 827 26 Maddikera Agraharam 4638 1546 27 Hampa 4033 1344 28 Rudravaram Nasapuram 2915 972 29 Alamur Aahobilam 2458 819 30 Bachepalli 3317 1106 31 Sanjamala Kanala 3247 1082 32 Kurnool Mamidalapadu 11262 2252 33 Panchalingala 4409 882 34 Pasupula 3031 606 35 State Bank of India Kosigi Vandagallu 2219 350 36 Pedda Kadabur Basaladoddi 2213 393 37 Chinna Thumbalam 5148 907 38 Kambaladinne 3268 550 39 Jalvadi 2877 482 40 Kambadahal 2478 469 41 Yemmiganur Enigabala 2474 431 42 Gudikal 10213 1592 43 Banavasi 4377 662 44 Kandanathi 6468 1062 45 Kadivella 4950 782 46 Kotekal 5808 961 47 Kadimetla 7108 1215 48 Nandavaram Halaharvi 6391 1158 49 Mugathi 5044 933 50 Nagaladinne 5170 964 51 C. -

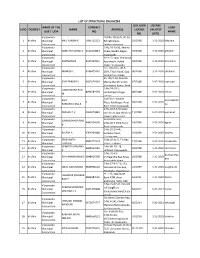

Structural Engineers List

LIST OF STRUCTURAL ENGINEERS ULB /UDA LICENSE NAME OF THE CONTACT USER S.NO DISTRICT NAME ADDRESS LICENSE VALIDITY ULB / UDA NO NAME NO. UPTO Vijayawada Flat No.105 (GF), Sri Sai 1 Krishna Municipal ANIL KUMAR K 7095712323 RatnaEnclave, 01/2008 3-31-2020 kakumar Corporation Seetharampuram Vijayawada D.No.26-20-30, Swamy 2 Krishna Municipal RAMESH KUMAR G 9440140843 Street,Gandhi Nagar. 03/2008 3-31-2020 grkumar Corporation Vijayawada Vijayawada 60-3-17, Opp: Chaitanya 3 Krishna Municipal RAVINDRA N 9440709915 Apartment, Ashok 04/2008 3-31-2020 nravindra Corporation Nagar, Vijayawada Vijayawada C/o. Desicons, 40-5- 4 Krishna Municipal MAHESH C 9246475767 19/9, Tikkle Road, Opp 06/2008 3-31-2020 cmahesh Corporation Siddhartha college, Vijayawada 43-106/1-58, Bharath 5 Krishna Municipal SIVA PRASAD S 9951074339 Matha Mandir Street, 07/2008 3-31-2020 ssprasad Corporation Nandamuri Nagar, Ajith Vijayawada D.No.74-10-1, LINGESWARA RAO 6 Krishna Municipal 8096281594 LakshmipathiNagar 08/2008 3-31-2020 mlrao M Corporation Colony, Vijayawada 2nd Floor, Kakarla SIVA asramakrish 7 Krishna Municipal 0 Plaza, KalaNagar, Near 09/2008 3-31-2020 RAMAKRISHNA A na Corporation Benz Circle,Vijayawada Vijayawada D.No.28-5-1/3,kuppa 8 Krishna Municipal PRASAD P.V 9966573883 vari street,opp.Hotel raj 11/2008 3-31-2020 pvprasad Corporation towers ,eluru road Vijayawada Sri Sai Planners, GANGADHARA RAO 9 Krishna Municipal 9440109695 D.No.40-5-19/4,Tickle 14/2008 3-31-2020 bgrao B Corporation Road, Vijayawada Vijayawada D.No.29-19-44, 10 Krishna Municipal RAJESH A 9703369888 Dornakal Road, 16/2008 3-31-2020 arajesh Corporation Suryaraopet, Vijayawada SREEKANTH D.No.39-11-5, T.K.Rao 11 Krishna 9885721574 17/2008 3-31-2020 lsreekanth Municipal LINGALA Street,Labbipet, Vijayawada VENKATA RAMANA D.No.40-1/1-18, 12 Krishna 9848111681 18/2008 3-31-2020 svramana Municipal S. -

Final EIA and EMP Report Yemmiganur 051020

Environmental Impact Consultancy Services for A.P. Urban Water Supply & Assessment& Environmental Yemmiganur Septage Management Improvement Project (APUWS& Management Plan Municipality SMIP) TABLE OF CONTENT CHAPTER S. NO. PARTICULAR PAGE NO LIST OF TABLES 3 LIST OF FIGURES 4 LIST OF ANNEXURES 5 ACRONYMS 6 EXECUTIVE SUMMARY 9 CHAPTERS 1 1.0 Introduction 12 1.1 Introduction to the overall state-wide project 12 1.2 Sub-project justification 13 1.3 Requirement for an Environmental Impact Assessment 13 1.4 Objectives of the Project’s Environmental and Social 15 Management Planning Framework (ESMPF) 1.5 Scope of Work for this report 15 1.6 Other Legislative and Regulatory Considerations 18 2 PROJECT LOCATION AND BASELINE DATA 2.0 Project Location 25 2.1 Baseline Data 25 2.1.1 Geographical & Demographic characteristics 26 2.1.2 Meteorology of Yemmiganur 28 2.1.3 Air Quality 30 2.1.4 Noise Pollution 33 2.1.5 Water Quality 35 2.1.6 Source Sustainability 35 2.1.7 Surface Water Quality 36 2.1.8 Ground Water Quality 43 2.2 Soils 49 2.3 Flora & Fauna 51 2.3.1 Flora 51 2.3.2 Fauna 56 3 PROJECT DESCRIPTION AND ANALYSIS OF ALTERNATIVES 3.1 Existing and Proposed Water Supply System in Project 61 Area 3.2 Potential Impacts and Risks form the Proposed Water 62 Supply Components 3.3 Proposed Water Supply System in project area 65 3.4 Analysis of Alternatives 73 4 KEY ENVIRONMENTAL IMPACTS 4.1 Identification of Impacts 76 4.2 Potential Environmental Impacts Rise during Construction 77 Phase and Operational Phase 4.3 Impacts During Construction And Operation Stages 85 2 of 131 Environmental Impact Consultancy Services for A.P. -

Quarantine Centre - Andhra Pradesh

QUARANTINE CENTRE - ANDHRA PRADESH Room rate(includi Contact Name of Number of ng meals Person(government Contact District: Type: Hotel/Quarantine Center: Rooms and taxes): Contact Number: offcial in-charge) Number: Remarks: VISAKHAPATNAM On Gratis Vikas Junior College Category Category 1:0 9052782060 Dr. Padma Priya 9052782060 1:74 VISAKHAPATNAM On Gratis Viajaya Residency Category Category 1:0 6300538289 Dr.Satyanarayana 6300538289 1:38 VISAKHAPATNAM On Payment The Park Hotel Category Category 9849121197 Anitha 9000782783 Single Occupancy for 14 1:20 1:35000 days VISAKHAPATNAM On Payment TAJ GATEWAY Category Category 7892142134 Anitha 9000782783 Single Occupancy for 14 1:40 1:35000 days VISAKHAPATNAM On Gratis Srikanth Lodge Category Category 1:0 9100064946 B.Ravikumar 9100064946 1:20 VISAKHAPATNAM On Gratis Sri Sai Brundavan grand Category Category 1:0 6300538289 Dr.Satyanarayana 6300538289 inn 1:28 VISAKHAPATNAM On Gratis SRI PALIMAR Category Category 1:0 9441207504 Dr.SUJATHA 9441207504 1:24 VISAKHAPATNAM On Gratis Post Metric Hostel G) Category 1:8 Category 1:0 9676376031 SDr.S.Vinnila 9676376031 VISAKHAPATNAM On Gratis NARAYANA IIT GIRLS Category Category 1:0 8985356024 Dr.Rajesh Naidu 8985356024 CAMPUS BLOCK 1) 1:140 VISAKHAPATNAM On Gratis Narayana IIT Category Category 1:0 8332954588 Dr.Amaleswari 8332954588 1:92 VISAKHAPATNAM On Gratis NARAYANA CAMPUS Category Category 1:0 9966994015 Dr.Dhanalakshmi 9966994015 1:93 VISAKHAPATNAM On Payment MEGHALAYA Category Category 8008200120 Anitha 9000782783 Single Occupancy for 14 1:45 -

District Census Handbook, Kurnool, Part XIII a & B, Series-2

CENSUS OF INDIA 1981 SERIES 2 ANDHRA PRADESH DI$TRiCT CENSUS HANDBOOK KURNOOL PARTS XIII-A & B VILLAGE 8: TOWN DIRECTORY VILLAGE & TOWNWISE PRIMARY CENSUS ABSTRACT .' S. S. JAVA RAO OF Tt\E '''DIAN ADMINiSTRATIVE S£RVlCE DIRECTOR OF CE"SU~ .OPERATIONS ANDHRA PRAD£SH PUBLISHED BY THE GOVERNMENT OF ANDHRA PRADESH 19" SRI RAGHAVENDRASWAMY SRI NDAVANAM AT MANTRALAYAM The motif presented on the cover page represents 'Sri R8ghavendraswamy Brindavanam' at Mantral, ya,,7 village in Yemmiganur taluk of K'Jrnool district. At Mafitra Ifl yam, ever/ yt:ar in the month of Sravana tAugust) on th~ secon I day of th~ dark fortnigf-it (Bahula Dwitiya) the 'ARADHANA' of Sri Raghavendraswamy (the day on which the saht bJdily entered th1 B rindavan3m) is celebrated with great fervour. Lakhs of people throng Mantra/ayam on this day for the ineffalJ/e ex perience of the just b~lfll therl1. Sri R ghavr::ndraswamy is one of the famous Peetadh'pithis (Pontiffs):md 17th in the line of succes sion from Sri Madhwacharya, the original founder of 'Dwaitha Philos3phy'. Th9 Swa 71iji took over the charge at the PEETHA in the year 1624 4. D. and made extensive tours all over the country and almost ruled the Vedantha Kingdom for 47 years. The Swamiji entered the B'fnddvanam at Mantra/ayam alive in the month of August, 1671. Th:! Briodavanam in which lies the astral body cf the Saint Raghavendraswamy in TAPAS (medJtation, is a rectanfJular black granite stone resting on KURMA (tof!oisf;) carved tn stone. It faces the id']( of S" Hanuman installed by the Saint himself. -

Predominant Weed Species of Kharif Groundnut in Rayalaseema Region of Andhra Pradesh

25th Asian-Pacific Weed Science Society Conference on “Weed Science for Sustainable Agriculture, Environment and Biodiversity”, Hyderabad, India during 13-16 October, 2015 Predominant weed species of Kharif groundnut in Rayalaseema region of Andhra Pradesh T. Prathima, D. Subramanyam and P. Shobha Rani Regional Agricultural Research Station, Tirupati , Andhra Pradesh 517 502, India In Andhra Pardesh, it is cultivated in an area of around Name of the RD RF RDO IVI 13.4 lakh hectares with a production of about 11.1 lakh tones weed and district and a productivity of 0.829 t/ha (2012-13) ( ZREAC, 2014). In Chloris barbata Rayalaseema region of Andhra Pardesh, groundnut is mainly Kurnool 5.80 5.59 1.75 13.14 cultivated during Kharif under rainfed conditions. The weed Anantapur 4.76 4.80 1.16 10.72 flora associated with groundnut is influenced by soil type, Kadapa 12.45 12.39 7.10 31.94 moisture availability and management of groundnut. Apart Chittoor 4.08 4.33 2.99 11.40 Cynodon dactylon from uncertain rainfall during Kharif, weeds significantly Kurnool 14.41 16.08 7.78 38.27 reduce the yield due to increased competition for soil moisture Anantapur 10.27 9.95 4.46 24.67 between crop and weeds including increased diseases as the Kadapa - - - - weeds of groundnut act as alternate hosts. Chittoor 19.24 14.64 11.14 45.03 METHODOLOGY Dactyloctenium aegyptium Kurnool 5.29 5.64 10.47 21.39 As a part of “National Invasive Weed Surveillance Anantapur 2.89 3.40 4.60 10.88 Programme”, weed survey was carried out for three years Kadapa 1.73 1.99 4.40 8.16 during 2008-09 to 2010-11 during both Kharif and Rabi Chittoor 9.27 9.45 7.28 26.00 seasons in different crops of Rayalaseema districts, A.P., in Celosia argentia which the predominant crop grown during Kharif is Kurnool 4.18 4.97 6.77 15.92 Anantapur 8.40 9.14 10.94 28.48 groundnut. -

Ground Water Brochure Anantapur District, Andhra Pradesh

For Official Use Only CENTRAL GROUND WATER BOARD MINISTRY OF WATER RESOURCES GOVERNMENT OF INDIA GROUND WATER BROCHURE ANANTAPUR DISTRICT, ANDHRA PRADESH SOUTHERN REGION HYDERABAD September 2013 CENTRAL GROUND WATER BOARD MINISTRY OF WATER RESOURCES GOVERNMENT OF INDIA GROUND WATER BROCHURE ANANTAPUR DISTRICT, ANDHRA PRADESH (AAP- 2012-13) By V.VINAY VIDYADHAR, ASSISTANT HYDROGEOLOGIST SOUTHERN REGION BHUJAL BHAWAN, GSI Post, Bandlaguda NH.IV, FARIDABAD -121001 Hyderabad-500068 HARYANA, INDIA Andhra Pradesh Tel: 0129-2418518 Tel: 040-24225201 Gram: Bhumijal Gram: Antarjal GROUND WATER BROCHURE ANANTAPUR DISTRICT, ANDHRA PRADESH CONTENTS S.No CHAPTER District at a Glance 1 Introduction 2 Rainfall & Climate 3 Geomorphology & Soil Types 4 Geology 5 Hydrogeology & Ground Water Scenario 6 Ground Water Resources 7 Ground Water Quality 8 Ground Water Development 9 Ground Water Related Issues and Problems 10 Conclusions DISTRICT AT A GLANCE 1. GENERAL North Latitude: 13° 40’ 16°15’ Location East Longitude 70° 50’ 78°38’ Geographical area (sq.km) 19,197 Headquarters Anantapur No. of revenue mandals 65 No. of revenue villages 964 Population (2011) Total 4083315 Population density (persons/sq.km) 213 Work force Cultivators 4,85,056 Agricultural labour 4,62,292 Major rivers Pennar, Papagni Maddileru, Tadikaluru Naravanka Soils Red sandy soil, Mixed red and black soil Agroclimatic zone Scarce Rainfall zone and 2. RAINFALL Normal annual rainfall Total 535 mm Southwest monsoon 316 mm Northeast monsoon 146 mm Summer 72 mm Cumulative departure from - 31% 3. LAND USE (2012) (Area in ha) Forest 196978 Barren and uncultivated 167469 Cultivable waste 48856 Current fallows 85754 Net area sown 1049255 4. -

Yemmiganur Assembly Andhra Pradesh Factbook

Editor & Director Dr. R.K. Thukral Research Editor Dr. Shafeeq Rahman Compiled, Researched and Published by Datanet India Pvt. Ltd. D-100, 1st Floor, Okhla Industrial Area, Phase-I, New Delhi- 110020. Ph.: 91-11- 43580781, 26810964-65-66 Email : [email protected] Website : www.electionsinindia.com Online Book Store : www.datanetindia-ebooks.com Report No. : AFB/AP-144-0118 ISBN : 978-93-5293-042-5 First Edition : January, 2018 Third Updated Edition : June, 2019 Price : Rs. 11500/- US$ 310 © Datanet India Pvt. Ltd. All rights reserved. No part of this book may be reproduced, stored in a retrieval system or transmitted in any form or by any means, mechanical photocopying, photographing, scanning, recording or otherwise without the prior written permission of the publisher. Please refer to Disclaimer at page no. 130 for the use of this publication. Printed in India No. Particulars Page No. Introduction 1 Assembly Constituency at a Glance | Features of Assembly as per 1-2 Delimitation Commission of India (2008) Location and Political Maps 2 Location Map | Boundaries of Assembly Constituency in District | Boundaries 3-8 of Assembly Constituency under Parliamentary Constituency | Town & Village-wise Winner Parties- 2014-PE, 2014-AE and 2009-PE Administrative Setup 3 District | Sub-district | Towns | Villages | Inhabited Villages | Uninhabited 9-12 Villages | Village Panchayat | Intermediate Panchayat Demographics 4 Population | Households | Rural/Urban Population | Towns and Villages by 13-14 Population Size | Sex Ratio (Total