Unconventional Oil and Gas -Current Status and Issues

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Oil Shale and Tar Sands

Fundamentals of Materials for Energy and Environmental Sustainability Editors David S. Ginley and David Cahen Oil shale and tar sands James W. Bunger 11 JWBA, Inc., Energy Technology and Engineering, Salt Lake City, UT, USA 11.1 Focus 11.2 Synopsis Tar sands and oil shale are “uncon- Oil shale and tar sands occur in dozens of countries around the world. With in-place ventional” oil resources. Unconven- resources totaling at least 4 trillion barrels (bbl), they exceed the world's remaining tional oil resources are characterized petroleum reserves, which are probably less than 2 trillion bbl. As petroleum becomes by their solid, or near-solid, state harder to produce, oil shale and tar sands are finding economic and thermodynamic under reservoir conditions, which parity with petroleum. Thermodynamic parity, e.g., similarity in the energy cost requires new, and sometimes of producing energy, is a key indicator of economic competitiveness. unproven, technology for their Oil is being produced on a large commercial scale by Canada from tar sands, recovery. For tar sands the hydrocar- and to a lesser extent by Venezuela. The USA now imports well over 2 million barrels bon is a highly viscous bitumen; for of oil per day from Canada, the majority of which is produced from tar sands. oil shale, it is a solid hydrocarbon Production of oil from oil shale is occurring in Estonia, China, and Brazil albeit on called “kerogen.” Unconventional smaller scales. Importantly, the USA is the largest holder of oil-shale resources. oil resources are found in greater For that reason alone, and because of the growing need for imports in the USA, quantities than conventional petrol- oil shale will receive greater development attention as petroleum supplies dwindle. -

Secure Fuels from Domestic Resources ______Profiles of Companies Engaged in Domestic Oil Shale and Tar Sands Resource and Technology Development

5th Edition Secure Fuels from Domestic Resources ______________________________________________________________________________ Profiles of Companies Engaged in Domestic Oil Shale and Tar Sands Resource and Technology Development Prepared by INTEK, Inc. For the U.S. Department of Energy • Office of Petroleum Reserves Naval Petroleum and Oil Shale Reserves Fifth Edition: September 2011 Note to Readers Regarding the Revised Edition (September 2011) This report was originally prepared for the U.S. Department of Energy in June 2007. The report and its contents have since been revised and updated to reflect changes and progress that have occurred in the domestic oil shale and tar sands industries since the first release and to include profiles of additional companies engaged in oil shale and tar sands resource and technology development. Each of the companies profiled in the original report has been extended the opportunity to update its profile to reflect progress, current activities and future plans. Acknowledgements This report was prepared by INTEK, Inc. for the U.S. Department of Energy, Office of Petroleum Reserves, Naval Petroleum and Oil Shale Reserves (DOE/NPOSR) as a part of the AOC Petroleum Support Services, LLC (AOC- PSS) Contract Number DE-FE0000175 (Task 30). Mr. Khosrow Biglarbigi of INTEK, Inc. served as the Project Manager. AOC-PSS and INTEK, Inc. wish to acknowledge the efforts of representatives of the companies that provided information, drafted revised or reviewed company profiles, or addressed technical issues associated with their companies, technologies, and project efforts. Special recognition is also due to those who directly performed the work on this report. Mr. Peter M. Crawford, Director at INTEK, Inc., served as the principal author of the report. -

OPEC in a Shale Oil World

OPEC in a Shale Oil World Mohamed Ramady • Wael Mahdi OPEC in a Shale Oil World Where to Next? Mohamed Ramady Wael Mahdi Department of Finance and Economics Regus, Building 12, Level 4 Trust Tower Visiting Associate Professor OPEC & Middle East Energy King Fahd University of Petroleum Correspondent Bloomberg News and Minerals Manama , Bahrain Dhahran , Saudi Arabia ISBN 978-3-319-22370-4 ISBN 978-3-319-22371-1 (eBook) DOI 10.1007/978-3-319-22371-1 Library of Congress Control Number: 2015946616 Springer Cham Heidelberg New York Dordrecht London © Springer International Publishing Switzerland 2015 This work is subject to copyright. All rights are reserved by the Publisher, whether the whole or part of the material is concerned, specifi cally the rights of translation, reprinting, reuse of illustrations, recitation, broadcasting, reproduction on microfi lms or in any other physical way, and transmission or information storage and retrieval, electronic adaptation, computer software, or by similar or dissimilar methodology now known or hereafter developed. The use of general descriptive names, registered names, trademarks, service marks, etc. in this publication does not imply, even in the absence of a specifi c statement, that such names are exempt from the relevant protective laws and regulations and therefore free for general use. The publisher, the authors and the editors are safe to assume that the advice and information in this book are believed to be true and accurate at the date of publication. Neither the publisher nor the authors or the editors give a warranty, express or implied, with respect to the material contained herein or for any errors or omissions that may have been made. -

Unconventional Oil Resources Exploitation: a Review

Acta Montanistica Slovaca Volume 21 (2016), number 3, 247-257 Unconventional oil resources exploitation: A review Šárka Vilamová 1, Marian Piecha 2 and Zden ěk Pavelek 3 Unconventional crude oil sources are geographically extensive and include the tar sands of the Province of Alberta in Canada, the heavy oil belt of the Orinoco region of Venezuela and the oil shales of the United States, Brazil, India and Malagasy. High production costs and low oil prices have hitherto inhibited the inclusion of unconventional oil resources in the world oil resource figures. In the last decade, developing production technologies, coupled with the higher market value of oil, convert large quantities of unconventional oil into an effective resource. From the aspect of quantity and technological and economic recoverability are actually the most important tar sands. Tar sands can be recovered via surface mining or in-situ collection techniques. This is an up-stream part of exploitation process. Again, this is more expensive than lifting conventional petroleum, but for example, Canada's Athabasca (Alberta) Tar Sands is one example of unconventional reserve that can be economically recoverable with the largest surface mining machinery on the waste landscape with important local but also global environmental impacts. The similar technology of up-stream process concerns oil shales. The downstream part process of solid unconventional oil is an energetically difficult process of separation and refining with important increasing of additive carbon production and increasing of final product costs. In the region of Central Europe is estimated the mean volume of 168 million barrels of technically recoverable oil and natural gas liquids situated in Ordovician and Silurian age shales in the Polish- Ukrainian Foredeep basin of Poland. -

OPEC Imposes 'Swing Producer' Role Upon U.S. Shale: Evidence And

International Association for Energy Economics | 17 OPEC Imposes ‘Swing Producer’ Role upon U.S. Shale: Evidence and Implications By Jim Krane and Mark Agerton* Introduction When OPEC declared in November that it would not cut production to boost oil prices, shock waves cascaded across the global oil sector. Oil prices had been dropping since June 2014, and OPEC’s an- nouncement propelled prices lower. By December, oil prices were half of what they had been in June. Now, emerging data show that those shock waves also disrupted the booming growth in the U.S. shale oil sector. Starting in January, U.S. shale producers reacted to the new price environment by idling rigs and reducing the number of wells drilled. Those actions, in turn, reduced the amount of new oil brought to market. The cutbacks accelerated through February and March. Taken together, it appears that market signals produced a collective “swing” response from shale producers that is helping to balance global markets, but via a new and untested channel. Since the 1970s, most of the market-reactive cuts in crude oil production have been orchestrated by the OPEC cartel. Shale’s unique characteristics are now allowing it to assume a swing role. These include a cost struc- ture that differs from the front-loaded investment required by conventional oil and gas production. Shale allows short lead times and smaller initial investment, along with lower barriers to entry and exit. Since shale wells are characterized by steep production decline curves, companies invest in real time, drilling and producing when prices warrant. -

Origin and Resources of World Oil Shale Deposits - John R

COAL, OIL SHALE, NATURAL BITUMEN, HEAVY OIL AND PEAT – Vol. II - Origin and Resources of World Oil Shale Deposits - John R. Dyni ORIGIN AND RESOURCES OF WORLD OIL SHALE DEPOSITS John R. Dyni US Geological Survey, Denver, USA Keywords: Algae, Alum Shale, Australia, bacteria, bitumen, bituminite, Botryococcus, Brazil, Canada, cannel coal, China, depositional environments, destructive distillation, Devonian oil shale, Estonia, Fischer assay, Fushun deposit, Green River Formation, hydroretorting, Iratí Formation, Israel, Jordan, kukersite, lamosite, Maoming deposit, marinite, metals, mineralogy, oil shale, origin of oil shale, types of oil shale, organic matter, retort, Russia, solid hydrocarbons, sulfate reduction, Sweden, tasmanite, Tasmanites, thermal maturity, torbanite, uranium, world resources. Contents 1. Introduction 2. Definition of Oil Shale 3. Origin of Organic Matter 4. Oil Shale Types 5. Thermal Maturity 6. Recoverable Resources 7. Determining the Grade of Oil Shale 8. Resource Evaluation 9. Descriptions of Selected Deposits 9.1 Australia 9.2 Brazil 9.2.1 Paraiba Valley 9.2.2 Irati Formation 9.3 Canada 9.4 China 9.4.1 Fushun 9.4.2 Maoming 9.5 Estonia 9.6 Israel 9.7 Jordan 9.8 Russia 9.9 SwedenUNESCO – EOLSS 9.10 United States 9.10.1 Green RiverSAMPLE Formation CHAPTERS 9.10.2 Eastern Devonian Oil Shale 10. World Resources 11. Future of Oil Shale Acknowledgments Glossary Bibliography Biographical Sketch Summary ©Encyclopedia of Life Support Systems (EOLSS) COAL, OIL SHALE, NATURAL BITUMEN, HEAVY OIL AND PEAT – Vol. II - Origin and Resources of World Oil Shale Deposits - John R. Dyni Oil shale is a fine-grained organic-rich sedimentary rock that can produce substantial amounts of oil and combustible gas upon destructive distillation. -

Full Report – BP Statistical Review of World Energy 2019

BP Statistical Review of World Energy 2019 | 68th edition Contents Introduction For 66 years, Natural the BPgas Statistical Review of WorldRenewable energy 1 Group chief executive’s introductionEnergy 3has 0 Reserves provided high-quality objective 5 1 andRenewables consumption 2 2018 at a glance globally 3consistent 2 Production data on world energy 52 markets. Generation by source 3 Group chief economist’s analysisThe review 3 4 Consumption is one of the most widely respected 5 3 Biofuels production and authoritative 3 7 Prices publications in the field of energy 3 8 Trade movements Electricity Primary energy economics, used for reference by the media, 8 Consumption 5 4 Generation 9 Consumption by fuel academia, Coalworld governments and energy 56 Generation by fuel 12 Consumption per capita companies. 4 2 Reserves A new edition is published every June. 44 Production CO2 Carbon Oil 45 Consumption 5 7 Carbon dioxide emissions 1 4 Reserves Discover more 47 onlinePrices and trade movements 1 6 Production All the tables and charts found in the latest printed Key minerals edition are available at bp.com/statisticalreviewNuclear energy 20 Consumption plus a number of extras, including: 5 8 Production • The energy charting tool – view 4 8 Consumption 2 4 Prices predetermined reports or chart specific data 59 Reserves 2 6 Refining according to energy type, region, country 59 Prices and year. Hydroelectricity 2 8 Trade movements • Historical data from 1965 for many sections. • Additional data 4 9for refinedConsumption oil production Appendices demand, natural gas, coal, hydroelectricity, nuclear energy and renewables. 6 0 Approximate conversion factors • PDF versions and PowerPoint slide packs of 6 0 Definitions the charts, maps and graphs, plus an Excel workbook of the data. -

Oil Shale Development in the United States: Prospects and Policy Issues

INFRASTRUCTURE, SAFETY, AND ENVIRONMENT THE ARTS This PDF document was made available from www.rand.org as CHILD POLICY a public service of the RAND Corporation. CIVIL JUSTICE EDUCATION Jump down to document ENERGY AND ENVIRONMENT 6 HEALTH AND HEALTH CARE INTERNATIONAL AFFAIRS The RAND Corporation is a nonprofit research NATIONAL SECURITY organization providing objective analysis and POPULATION AND AGING PUBLIC SAFETY effective solutions that address the challenges facing SCIENCE AND TECHNOLOGY the public and private sectors around the world. SUBSTANCE ABUSE TERRORISM AND HOMELAND SECURITY TRANSPORTATION AND Support RAND INFRASTRUCTURE Purchase this document WORKFORCE AND WORKPLACE Browse Books & Publications Make a charitable contribution For More Information Visit RAND at www.rand.org Explore RAND Infrastructure, Safety, and Environment View document details Limited Electronic Distribution Rights This document and trademark(s) contained herein are protected by law as indicated in a notice appearing later in this work. This electronic representation of RAND intellectual property is provided for non-commercial use only. Permission is required from RAND to reproduce, or reuse in another form, any of our research documents. This product is part of the RAND Corporation monograph series. RAND monographs present major research findings that address the challenges facing the public and private sectors. All RAND monographs undergo rigorous peer review to ensure high standards for research quality and objectivity. Oil Shale Development in the United States Prospects and Policy Issues James T. Bartis, Tom LaTourrette, Lloyd Dixon, D.J. Peterson, Gary Cecchine Prepared for the National Energy Technology Laboratory of the U.S. Department of Energy The research described in this report was conducted within RAND Infrastructure, Safety, and Environment (ISE), a division of the RAND Corporation, for the National Energy Technology Laboratory of the U.S. -

The Exxonmobil-Xto Merger: Impact on U.S

THE EXXONMOBIL-XTO MERGER: IMPACT ON U.S. ENERGY MARKETS HEARING BEFORE THE SUBCOMMITTEE ON ENERGY AND ENVIRONMENT OF THE COMMITTEE ON ENERGY AND COMMERCE HOUSE OF REPRESENTATIVES ONE HUNDRED ELEVENTH CONGRESS SECOND SESSION JANUARY 20, 2010 Serial No. 111–91 ( Printed for the use of the Committee on Energy and Commerce energycommerce.house.gov U.S. GOVERNMENT PRINTING OFFICE 76–003 WASHINGTON : 2012 For sale by the Superintendent of Documents, U.S. Government Printing Office Internet: bookstore.gpo.gov Phone: toll free (866) 512–1800; DC area (202) 512–1800 Fax: (202) 512–2104 Mail: Stop IDCC, Washington, DC 20402–0001 VerDate Mar 15 2010 00:51 Nov 06, 2012 Jkt 076003 PO 00000 Frm 00001 Fmt 5011 Sfmt 5011 E:\HR\OC\A003.XXX A003 pwalker on DSK7TPTVN1PROD with HEARING COMMITTEE ON ENERGY AND COMMERCE HENRY A. WAXMAN, California, Chairman JOHN D. DINGELL, Michigan JOE BARTON, Texas Chairman Emeritus Ranking Member EDWARD J. MARKEY, Massachusetts RALPH M. HALL, Texas RICK BOUCHER, Virginia FRED UPTON, Michigan FRANK PALLONE, JR., New Jersey CLIFF STEARNS, Florida BART GORDON, Tennessee NATHAN DEAL, Georgia BOBBY L. RUSH, Illinois ED WHITFIELD, Kentucky ANNA G. ESHOO, California JOHN SHIMKUS, Illinois BART STUPAK, Michigan JOHN B. SHADEGG, Arizona ELIOT L. ENGEL, New York ROY BLUNT, Missouri GENE GREEN, Texas STEVE BUYER, Indiana DIANA DEGETTE, Colorado GEORGE RADANOVICH, California Vice Chairman JOSEPH R. PITTS, Pennsylvania LOIS CAPPS, California MARY BONO MACK, California MICHAEL F. DOYLE, Pennsylvania GREG WALDEN, Oregon JANE HARMAN, California LEE TERRY, Nebraska TOM ALLEN, Maine MIKE ROGERS, Michigan JANICE D. SCHAKOWSKY, Illinois SUE WILKINS MYRICK, North Carolina CHARLES A. -

Pyrene in Oil Shale Industry Wastes, Some Bodies of Water in the Estonian S.S.R

Environmental Health Perspectives Vol. 30, pp. 211-216, 1979 Levels of Benzo(a)pyrene in Oil Shale Industry Wastes, Some Bodies of Water in the Estonian S.S.R. and in Water Organisms by 1. A. Veldre,* A. R. Itra,*and L. P. Paalme* Data on the content of benzo(a)pyrene (BP) in oil shale industry wastewater, the effectiveness of various effluent treatment processes (evaporation, extraction with butyl acetate, trickling rilters, aeration tanks) in reducing the level of BP in oil shale wastewater, the level of BP in various bodies of water of Estonia, and in fish and other water organisms are reviewed. The quantitative determination of BP in concentrated diethyl ether extracts of water samples was carried out by ultraviolet and spectroluminescence procedures by use of the quasi-linear spectra at -196C in solid paraffins. It has been found that oil shale industry wastewater contains large amounts of BP. The most efficient purification process for removing the BP in oil shale industry phenol water is extraction with butyl acetate. The level of BP in the rivers of the oil shale industry area is comparatively higher than in other bodies of water of the Republic. The concentration of BP in the lakes of the Estonian S.S.R. is on the whole insignificant. Even the maximum concentration found in our lakes is as a rule less than the safety limit for BP in bodies of water (0.005 ,ug/l.). Drinking water is treated at the waterworks. The effectiveness of the water treatment in reducing the level of BP varies from 11 to 88%. -

The Shale Oil Boom: a U.S

The Geopolitics of Energy Project THE SHALE OIL BOOM: A U.S. PHENOMENON LEONARDO MAUGERI June 2013 Discussion Paper #2013-05 Geopolitics of Energy Project Belfer Center for Science and International Affairs Harvard Kennedy School 79 JFK Street Cambridge, MA 02138 Fax: (617) 495-8963 Email: [email protected] Website: http://belfercenter.org Copyright 2013 President and Fellows of Harvard College The author of this report invites use of this information for educational purposes, requiring only that the reproduced material clearly cite the full source: Leonardo Maugeri. “The Shale Oil Boom: A U.S. Phenomenon” Discussion Paper 2013-05, Belfer Center for Science and International Af- fairs, Harvard Kennedy School, June 2013. Statements and views expressed in this discussion paper are solely those of the author and do not imply endorsement by Harvard University, the Harvard Kennedy School, or the Belfer Center for Science and International Affairs. The Geopolitics of Energy Project THE SHALE OIL BOOM: A U.S. PHENOMENON LEONARDO MAUGERI June 2013 iv The Shale Oil Boom: A U.S. Phenomenon ABOUT THE AUTHOR Leonardo Maugeri is the Roy Family Fellow at the Belfer Center for Science and International Affairs, John F. Kennedy School of Government, Harvard University. Leonardo Maugeri has been a top manager of Eni (the sixth largest multinational oil company), where he held the positions of Senior Executive Vice President of Strategy and Development (2000-2010) and Executive Chairman of Polimeri Europa, Eni’s petrochemical branch (2010- 2011). On August 31th, 2011, he left Eni. Maugeri has published four books on energy, among them the The Age of Oil: the Mythology, History, and Future of the World’s Most Controversial Resource (Praeger, 2006), and Beyond the Age of Oil: The Myths and Realities of Fossil Fuels and Their Alternatives (Praeger, 2010). -

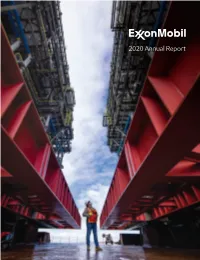

2020 Annual Report

2020 Annual Report CONTENTS II To our shareholders IV Positioning for a lower-carbon energy future VI Energy for a growing population Scalable technology solutions VIII Providing energy and products for modern life IX Progressing advantaged investments X Creating value through our integrated businesses XII Upstream XIV Downstream XV Chemical XVI Board of Directors 1 Form 10-K 124 Stock performance graphs 125 Frequently used terms 126 Footnotes 127 Investor information ABOUT THE COVER Delivery of two modules to the Corpus Christi Chemical Project site in 2020. Each module weighed more than 17 million pounds, reached the height of a 17-story building, and was transported more than 5 miles over land. Cautionary Statement • Statements of future events or conditions in this report are forward-looking statements. Actual future results, including financial and operating performance; demand growth and mix; planned capital and cash operating expense reductions and efficiency improvements, and ability to meet or exceed announced reduction objectives; future reductions in emissions intensity and resulting reductions in absolute emissions; carbon capture results; resource recoveries; production rates; project plans, timing, costs, and capacities; drilling programs and improvements; and product sales and mix differ materially due to a number of factors including global or regional changes in oil, gas, or petrochemicals prices or other market or economic conditions affecting the oil, gas, and petrochemical industries; the severity, length and ultimate