Retail Industry Audit Technique Guide

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Age of Exploration

ABSS8_ch05.qxd 2/9/07 10:54 AM Page 104 The Age of 5 Exploration FIGURE 5-1 1 This painting of Christopher Columbus arriving in the Americas was done by Louis Prang and Company in 1893. What do you think Columbus might be doing in this painting? 104 Unit 1 Renaissance Europe ABSS8_ch05.qxd 2/9/07 10:54 AM Page 105 WORLDVIEW INQUIRY Geography What factors might motivate a society to venture into unknown regions Knowledge Time beyond its borders? Worldview Economy Beliefs 1492. On a beach on an island in the Caribbean Sea, two Values Society Taino girls were walking in the cool shade of the palm trees eating roasted sweet potatoes. uddenly one of the girls pointed out toward the In This Chapter ocean. The girls could hardly believe their eyes. S Imagine setting out across an Three large strange boats with huge sails were ocean that may or may not con- headed toward the shore. They could hear the tain sea monsters without a map shouts of the people on the boats in the distance. to guide you. Imagine sailing on The girls ran back toward their village to tell the ocean for 96 days with no everyone what they had seen. By the time they idea when you might see land returned to the beach with a crowd of curious again. Imagine being in charge of villagers, the people from the boats had already a group of people who you know landed. They had white skin, furry faces, and were are planning to murder you. -

Merchants and the Origins of Capitalism

Merchants and the Origins of Capitalism Sophus A. Reinert Robert Fredona Working Paper 18-021 Merchants and the Origins of Capitalism Sophus A. Reinert Harvard Business School Robert Fredona Harvard Business School Working Paper 18-021 Copyright © 2017 by Sophus A. Reinert and Robert Fredona Working papers are in draft form. This working paper is distributed for purposes of comment and discussion only. It may not be reproduced without permission of the copyright holder. Copies of working papers are available from the author. Merchants and the Origins of Capitalism Sophus A. Reinert and Robert Fredona ABSTRACT: N.S.B. Gras, the father of Business History in the United States, argued that the era of mercantile capitalism was defined by the figure of the “sedentary merchant,” who managed his business from home, using correspondence and intermediaries, in contrast to the earlier “traveling merchant,” who accompanied his own goods to trade fairs. Taking this concept as its point of departure, this essay focuses on the predominantly Italian merchants who controlled the long‐distance East‐West trade of the Mediterranean during the Middle Ages and Renaissance. Until the opening of the Atlantic trade, the Mediterranean was Europe’s most important commercial zone and its trade enriched European civilization and its merchants developed the most important premodern mercantile innovations, from maritime insurance contracts and partnership agreements to the bill of exchange and double‐entry bookkeeping. Emerging from literate and numerate cultures, these merchants left behind an abundance of records that allows us to understand how their companies, especially the largest of them, were organized and managed. -

Transforming Food, Drug, and Mass Merchant Retail with AI Table of 04 Executive Summary Contents 06 Why Are We Focused on AI/ML in Retail?

Transforming food, drug, and mass merchant retail with AI Table of 04 Executive summary contents 06 Why are we focused on AI/ML in retail? 07 Chapter 1: the state of retail Waves of change in retail Shifting behaviors and impact on retail Digital transformation and the power of AI/ML 15 Chapter 2: the value of AI/ML Overview of value chain and use cases High-value use cases Value at stake Implementation across retailers, today and in the future High-value use cases for Food, Drug, Mass merchant retailers Personalized promotions (redeemed online) Personalized promotions (redeemed offline/in-store) Loyalty program management Auto-populated and personalized online cart Customer care chatbots Personalized product recommendations Frictionless checkout Shelf-checking Automated task dispatch and in-store execution Picker routing 2 Table of Design to value Assortment optimization contents Pricing optimization Demand Planning Inventory optimization Omni-channel fulfillment optimization Warehousing operations optimization AI-enabled last mile 47 Chapter 3: accelerating delivery of AI/ML Achieved impact Enablers of value Barriers to value Barriers in the future 53 Chapter 4: AI/ML myths and how Google Cloud can help AI/ML myths debunked How Google Cloud can help 3 Executive summary The $15T global retail industry has been rocked with significant waves over the past decade, but the most recent disruption and global health crisis, COVID-19, has caused the biggest shock of all. Within several months, the global pandemic not only amplified differences between retail leaders and laggards, but seriously condensed the timeline available to play ‘catch up’ in digital transformation and e-commerce. -

Trade in the Ancient World

Trade in the Ancient World The seaborne con�merce of Rome was unsurpassed until relatively recent times. Evidence for this marine traffic comes from many sources, including the newly stimulated underwater archaeology by Lionel Casson built five ships, loaded them with wide arc. The arteries were the shipping have of ancient vessels come from the wine-worth its weight in gold at the lanes, the largest leading from points on graves of merchants who had a sketch I time-and sent them to Rome.. the perimeter to the huge capital at of the craft to which they owed their Every one of my ships went down .... Rome, and later at Constantinople. Over fortunes inscribed on their tombs. Find Neptune swallowed up 30 million ses them passed the great ships, leaving on ings of Egyptian pottery in Crete, of terces in one day... I built others, big regular schedules to carry the thousands Syrian glass in Italy, of Italian dishes in ger, better and luckiel·, loaded them with of bushels of wheat, the jars of oil and southern France and so on enable us to wine again, plus bacon, beans, perfume, wine and salt fish. Both large and small trace many lines of commerce. We can .slaves ....When the gods are behind vessels transported luxury goods ranging reconstruct the wine and oil trade from something it happens qUickly: I netted from Chinese silks to Athenian statuary. clay shipping jars, stamped with the 10 million sesterces on that one voyage. To piece together the details of this place of origin, whicq excavators have The time is the first century and the ancient commerce the investigator must unearthed at dozens of sites. -

The Legal Responsibilities of the Person Preparing Tax Returns and Furnishing Tax Advice and Reliance Upon Advice of Counsel Louis L

Marquette Law Review Volume 46 Article 3 Issue 3 Winter 1962-1963 The Legal Responsibilities of the Person Preparing Tax Returns and Furnishing Tax Advice and Reliance Upon Advice of Counsel Louis L. Meldman Follow this and additional works at: http://scholarship.law.marquette.edu/mulr Part of the Law Commons Repository Citation Louis L. Meldman, The Legal Responsibilities of the Person Preparing Tax Returns and Furnishing Tax Advice and Reliance Upon Advice of Counsel, 46 Marq. L. Rev. 313 (1963). Available at: http://scholarship.law.marquette.edu/mulr/vol46/iss3/3 This Article is brought to you for free and open access by the Journals at Marquette Law Scholarly Commons. It has been accepted for inclusion in Marquette Law Review by an authorized administrator of Marquette Law Scholarly Commons. For more information, please contact [email protected]. THE LEGAL RESPONSIBILITIES OF THE PERSON PREPARING THE TAX RETURNS AND FURNISHING TAX ADVICE AND RELIANCE UPON ADVICE OF COUNSEL Louis L. MELDMAN** The preparation of income tax returns and the furnishing of tax ad- vice and assistance by the tax practitioner results in many responsibili- ties. The practitioner has a duty first, to his client, the taxpayer. Sec- ondly, he has a duty to the government, the treasury department. And, finally, he has a duty to society to aid in the administration of justice. All of his actions must, in the last analysis, be guided by his own con- science.' RESPONSIBILITY TO THE CLIENT, THE TAXPAYER The attorney, C.P.A., or the accountant has a responsibility to his client. -

CAREER PATH Client Service Skills, Duties and Requirements

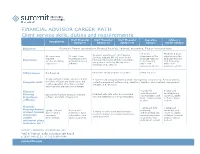

FINANCIAL ADVISOR CAREER PATH Client service skills, duties and requirements Staff Financial Staff Financial Staff Financial Associate Advisor / Paraplanner Advisor I Advisor II Advisor III Advisor Senior Advisor Education Bachelor’s Degree (preferably in Financial Planning, Business, Accounting, Finance or related field) 4+ years’ Minimum 5 years’ 3+ years’ experience in the Financial No experience At least 1 year experience in the experience in the Services industry OR 1–2 years in the required experience in the Financial Planning Financial Planning Experience Financial Planning field delivering advice (prefer internship Financial Services field delivering field delivering and services to clients OR any of the experience) industry advice and advice and following: CFA, CPA, JD services to clients services to clients Not Required Enrolled in CFP® program or licensee CFP® required CFP® License Strong computer skills, experienced and + experienced and proficient in portfolio management software (e.g. Portfolio Center), Computer skills proficient in Excel and Word, basic and contact management software (e.g. Salesforce, Junxure), and document management routine operation of portfolio, contact, software (e.g. Worldox) and document management software Financial + proficient + advanced describing client knowledge and Planning Basic understanding Financial Planning Proficient with data entry and reviewing report package and expertise, ability software and data entry process and understanding client report package Projections Monte Carlo analysis -

The Decline in Tax Adviser Professionalism in American Society

Fordham Law Review Volume 84 Issue 6 Article 14 2016 The Decline in Tax Adviser Professionalism in American Society John S. Dzienkowski University of Texas School of Law Robert J. Peroni University of Texas School of Law Follow this and additional works at: https://ir.lawnet.fordham.edu/flr Part of the Tax Law Commons Recommended Citation John S. Dzienkowski and Robert J. Peroni, The Decline in Tax Adviser Professionalism in American Society, 84 Fordham L. Rev. 2721 (2016). Available at: https://ir.lawnet.fordham.edu/flr/vol84/iss6/14 This Symposium is brought to you for free and open access by FLASH: The Fordham Law Archive of Scholarship and History. It has been accepted for inclusion in Fordham Law Review by an authorized editor of FLASH: The Fordham Law Archive of Scholarship and History. For more information, please contact [email protected]. THE DECLINE IN TAX ADVISER PROFESSIONALISM IN AMERICAN SOCIETY John S. Dzienkowski* & Robert J. Peroni** INTRODUCTION The United States faces a tax-avoidance crisis that seriously undermines the integrity and effectiveness of the federal income tax system1 and creates a significant tax revenue gap.2 Some tax practitioners and some prominent law and accounting firms have participated in creating and intensifying this crisis.3 Yet, more than a century after the enactment of the modern federal income tax statute, academics, tax lawyers, and accountants continue to debate the appropriate role of the tax practitioner in the tax system. This vigorous discussion has involved many of the leading tax advisers and academic commentators of their time.4 Many of these advisers and * Dean John F. -

MERCHANTS and TRADERS a Supply and Demand Game

W 411 MERCHANTS AND TRADERS A Supply and Demand Game Danielle Pleasant, 4-H Extension Agent, Johnson County MANAGEMENT OF APHIDS AND BYD IN TENNESSEE WHEAT 1 Tennessee 4-H Youth Development Merchants and Traders A Supply and Demand Game Skill Level Intermediate Introduction to Content Learner Outcomes This lesson introduces the concepts of The learner will be able to: supply and demand as well as uses key • Model a supply and demand relationship. terms from sixth-grade social studies. The • Model a bartering economic system. barter trading system and scenarios • Build Communication skills. reinforce the importance of commodities and currency used in ancient world Educational Standard(s) Supported history. This lesson explores bartering Social Studies 6.07, 6.18, 6.25, 6.38 from several different periods including Success Indicator Mesopotamian, Greek and Roman times. Learners will be successful if they: Understand a basic supply and demand relationship. Introduction to Methodology Time Needed “Merchants and Traders” is a simulation 45 minutes to 1 hour designed to teach the concepts of a barter trading system as well as supply and Materials List demand. The simulation is set from the Silk, gems, cotton balls, salt, tea bags, time period of approximately 4,000 BC Popsicle sticks, sheep pictures, coins. to 44 BC, which correlates to the ancient Enough for 10 “currency” (gems or coins) for world history curriculum covered under half of group and 10 “commodities” for half the current education standards. of group Author Pleasant, Danielle. 4-H Youth Development Agent, Johnson County. 3 Terms and Concepts Introduction Tips for Engagement Defined in supplemental information • Explain that students can trade as many items as they want at one time but can only trade once per round, just as they can Setting the Stage and Opening Questions buy a cart full of groceries but they will only go through the Begin by asking: checkout once. -

Tax Audits in Germany: a Primer and a Plan

Tax Audits in Germany: a Primer and a Plan ROSEMARIE A. RHINES, SCOTT M. BENNETT, AND SILKE BACHT* I. Introduction In Germany, as in most other countries, taxpayers become anxious the moment the rev- enue authority starts an audit. Regardless of whether the taxpayer is German or foreign, neither one looks forward to an audit. Foreign corporations face a bigger challenge, how- ever, because taxes, particularly international taxes, generally are managed by the parent company's tax department, very often with little involvement by the tax advisors of the various subsidiary companies other than the preparation of year-end financial statements and in dealings with the local tax authorities. Herein lies the dilemma: the tax department of the parent company must be "in charge," but it may not know or have experience with the foreign tax laws and regulations affecting the various subsidiaries, familiarity with foreign languages and mentalities, and all the other aspects that can be described as "insight" or "insider knowledge." This dilemma is worsened by tight budgets, shortages of qualified support staff, and the frictions that often arise between tax advisors and business people, who often see the work of the "tax guys" as interfering with their creativity and freedom. Establishing and balancing the roles of the local and non-local tax departments is the major challenge when it comes to dealing professionally with a foreign tax audit. Generally speaking, the in-house tax department can only lose. Even if a favorable tax settlement is reached, local management often feels inconvenienced by the presence of the parent com- pany's advisors and is only relieved when the audit is over because it means that the "tax guys" will finally go away and let the local company get back to business. -

Tax Advisors and Conflicted Citizens

Georgetown University Law Center Scholarship @ GEORGETOWN LAW 2014 Tax Advisors and Conflicted Citizens Milton C. Regan Georgetown University Law Center, [email protected] This paper can be downloaded free of charge from: https://scholarship.law.georgetown.edu/facpub/1335 http://ssrn.com/abstract=2436605 16 Legal Ethics 322-349 (2014) This open-access article is brought to you by the Georgetown Law Library. Posted with permission of the author. Follow this and additional works at: https://scholarship.law.georgetown.edu/facpub Part of the Law and Society Commons, Legal Ethics and Professional Responsibility Commons, Legal Profession Commons, and the Tax Law Commons DOI: http://dx.doi.org/10.5235/1460728X.16.2.322 Legal Ethics, Volume 16, Part 2 Tax Advisors and Conflicted Citizens Milton C Regan, Jr* IntrODuctIOn How should we think about the obligations of a lawyer who counsels and provides legal advice outside of litigation? thousands of lawyers are involved every day in advising clients in this setting. these lawyers counsel companies or individuals on how they can benefit from or avoid violating statutes, regulations, and other sources of law. Legal counsellors do their job behind closed doors. they engage in conversations that are usually protected from disclosure. they move in the shadows, and their influence can be hard to trace. that influence can be profound, however. It can determine who is exposed to what chemicals, who keeps and who loses their jobs, who will be able to count on retire- ment savings and who won’t. rules of professional responsibility devote remarkably little sustained attention to the role of the advisor. -

Auditor Tax Advisory Services and Clients' Tax Avoidance

Auditor Tax Advisory Services and Clients’ Tax Avoidance: Do Auditors Draw a Line in the Sand for Tax Advisory Services? Wayne L. Nesbitt Broad College of Business Michigan State University [email protected] Anh Persson Broad College of Business Michigan State University [email protected] Joanna Shaw Broad College of Business Michigan State University [email protected] October 2018 Acknowledgments: We are thankful for the support and guidance of Edmund Outslay and helpful comments from James Anderson, Michelle Nessa, Preetika Joshi (discussant), Sarah Stuber, Dan Wangerin and workshop participants at Michigan State University, the 8th EIASM Conference on Current Research in Taxation, and the 2018 AAA Midwest Region Meeting. We gratefully acknowledge financial support from the Eli Broad College of Business at Michigan State University. Joanna Shaw also acknowledges the generous support from the Grant Thornton Doctoral Fellowship. All errors are our own. Auditor Tax Advisory Services and Clients’ Tax Avoidance: Do Auditors Draw a Line in the Sand for Tax Advisory Services? Abstract We investigate whether current PCAOB regulations on the prohibition of the provision of aggressive tax strategies to publicly-listed clients, limits the association between auditor- provided tax services (APTS) and clients’ level of tax avoidance. A resurgence of consultancy services as well as incidents of audit firms’ involvement in clients’ tax aggressive activities have reignited concerns about the provision of non-audit services. Using non-linear and quartile regressions, we document a negative but declining association between tax fees paid and clients’ effective tax rates (ETR). Further, we find evidence that the association becomes positive for the most tax aggressive clients. -

The Traders in Rome's Eastern Commerce

THE TRADERS IN ROME‟S EASTERN COMMERCE THE TRADERS IN ROME‟S EASTERN COMMERCE By KYLE MCLEISTER, B.A. A Thesis Submitted to the School of Graduate Studies in Partial Fulfilment of the Requirements for the Degree Master of Arts McMaster University © Copyright by Kyle McLeister, September 2011 MASTER OF ARTS (2011) McMaster University (Classics) Hamilton, Ontario TITLE: The Traders in Rome‟s Eastern Commerce AUTHOR: Kyle McLeister, B.A. (Honours, University of Toronto) SUPERVISOR: Professor E.W. Haley NUMBER OF PAGES: v, 111 ii Abstract Rome‟s Eastern trade flourished for over two centuries, from reign of Augustus to that of Caracalla, bringing highly valuable goods from India and East Africa to consumers in Rome, and this thesis examines the traders who operated in Egypt and transported goods between the Red Sea and the Mediterranean. Chapter 1 examines the identities of the traders, in terms of ethnicity, wealth, and social standing, and also examines the evidence for the involvement of the imperial family in the Eastern trade, while Chapter 2 analyzes the many different customs dues, transit tolls, and other taxes imposed upon Eastern traders operating in Egypt. Chapter 3 presents an analysis of customs abuses, including the forms of abuses which occurred, legislative attempts to curb abuses, and the frequency of abuses. Chapter 4 investigates the potential for profits in the Eastern trade, taking into consideration the various expenses, such as transport fees and customs dues, incurred in the course of transporting the goods across Egypt, as well as the evidence for the value of Eastern goods at Rome.