Presentation Daimler Truck Strategy Day May 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Vehicle Identification Number (VIN) Coding Summary (Internal Use Only)

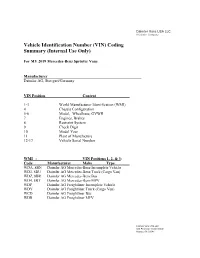

Daimler Vans USA LLC A Daimler Company Vehicle Identification Number (VIN) Coding Summary (Internal Use Only) For MY 2019 Mercedes-Benz Sprinter Vans Manufacturer Daimler AG, Stuttgart/Germany VIN Position Content 1-3 World Manufacturer Identification (WMI) 4 Chassis Configuration 5-6 Model, Wheelbase, GVWR 7 Engines, Brakes 8 Restraint System 9 Check Digit 10 Model Year 11 Plant of Manufacture 12-17 Vehicle Serial Number WMI - VIN Positions 1, 2, & 3: Code Manufacturer Make Type WDA, 8BN Daimler AG Mercedes-Benz Incomplete Vehicle WD3, 8BU Daimler AG Mercedes-Benz Truck (Cargo Van) WDZ, 8BR Daimler AG Mercedes-Benz Bus WD4, 8BT Daimler AG Mercedes-Benz MPV WDP Daimler AG Freightliner Incomplete Vehicle WDY Daimler AG Freightliner Truck (Cargo Van) WCD Daimler AG Freightliner Bus WDR Daimler AG Freightliner MPV Daimler Vans USA LLC 303 Perimeter Center North Atlanta, GA 30346 Daimler Vans USA LLC A Daimler Company Chassis Configuration - VIN Position 4: Code Chassis Configuration / Intended Market P All 4x2 Vehicle Types / U.S. B All 4x2 Vehicle Types / Canada F All 4x4 Vehicle Types / U.S. C All 4x4 Vehicle Types / Canada Model, Wheelbase, GVWR - VIN Positions 5 & 6: Code Model Wheelbase GVWR E7 C1500/C2500/P1500 3665 mm/ 144 in. 8,000 lbs. to 9,000 lbs. Class G E8 C2500/P2500 4325 mm/ 170 in. 8,000 lbs. to 9,000 lbs. Class G F0 C2500/C3500 3665 mm/ 144 in. 9,000 lbs. to 10,000 lbs. Class H F1 C2500/C3500 4325 mm/ 170 in. 9,000 lbs. to 10,000 lbs. Class H F3 C4500/C3500 3665 mm/ 144 in. -

Daimler AG, Formerly Known As

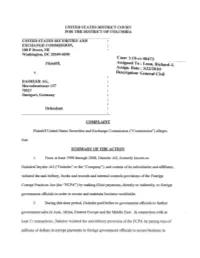

UNITED STATES DISTRICT COURT FOR THE DISTRICT OF COLUMBIA UNITED STATES SECURITIES AND EXCHANGE COMMISSION, 100 F Street,NE Washington, DC 20549-6030 Case: 1:10-cv-00473 Plaintiff, Ass~gned To : Leon, RichardJ-.- ASSIgn. Date: 3/22/2010 v. Description: General Civil DAIMLERAG, .Mercedesstrasse 137 70327 . Stuttgart, Germany Defendant. COMPLAINT PlaintiffUnited States Securities and Exchange Commission ("Commission") alleges that: SUMMARY OF THE ACTION 1. From at least 1998 through 2008, Daimler AG, formerly knoWn as DaimlerChrysler AG ("Daimler" or the "Company"), and certain ofits subsidiaries and affiliates, violated the anti-bribery, books and records and internal controls provisions ofthe Foreign _ Corrupt Practices Act (the "FCPA") by making illicit payments, directly or indirectly, to foreign government officials in order to secure and maintain business worldWide. 2. During this time period, Daimler paid bribes to government officials to further government sales in Asia, Africa, Eastern Europe and the Middle East. In connection With at least 51 transactions, Daimler violated the anti-bribery provision of the FCPA by paying tens of millions of dollars in corrupt payments to foreign government officials to secure business in · Russia,Chilia,Vietnam, Nigeria, Hungary, Latvia, Croatia and Bosnia. These corrupt payments were made through the use ofU.S. mails or the means or instrumentality ofU.S. interstate commerce. 3. Daimler also violated the FCPA's books and records and internal controls provisions in connection with the 51 transactions and at least an additional 154 transactions, in which it made improper payments totaling atleast $56 million to secure business in 22 countries, including, among others, Russia, China, Nigeria, Vietnam, Egypt, Greece, Hungary, North Korea, andIndonesia. -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

United States Court of Appeals for the Federal Circuit

Case: 15-1914 Document: 48 Page: 1 Filed: 12/21/2015 2015-1914, -1919 United States Court of Appeals for the Federal Circuit ALTERA CORPORATION, XILINX, INC., Plaintiffs-Appellants, v. PAPST LICENSING GMBH & CO. KG, Defendant-Appellee. Appeals from the United States District Court for the Northern District of California in Case Nos. 5:14-cv-04794-LHK and 5:14-cv-04963-LHK, Judge Lucy H. Koh BRIEF FOR AMICI CURIAE AO KASPERSKY LAB, LIMELIGHT NETWORKS, INC., QVC, INC., SAS INSTITUTE INC., SYMMETRY LLC, AND VIZIO, INC. IN SUPPORT OF PLAINTIFF-APPELLANT XILINX, INC. STEVEN D. MOORE DARIUS SAMEROTTE KILPATRICK TOWNSEND & STOCKTON LLP Eighth Floor, Two Embarcadero Center San Francisco, CA 94111 Telephone: 415 576 0200 Attorneys for AMICI CURIAE DECEMBER 21, 2015 COUNSEL PRESS, LLC (888) 277-3259 Case: 15-1914 Document: 48 Page: 2 Filed: 12/21/2015 CERTIFICATE OF INTEREST Counsel for amici certifies the following: 1. The full name of every party or amicus represented by me is: AO Kaspersky Lab, Limelight Networks, Inc., QVC, Inc., SAS Institute Inc., Symmetry LLC, and VIZIO, Inc. 2. The name of the real party in interest represented by us is: N/A 3. All parent corporations and any public companies that own 10 percent or more of the stock of the parties represented by me are: AO Kaspersky Lab is a wholly owned subsidiary of Kaspersky Lab Ltd. Investment entities affiliated with Goldman, Sachs & Co. own over 10 percent of Limelight Networks, Inc. QVC is a wholly owned subsidiary of Liberty Interactive Corporation. SAS Institute Inc. and Symmetry LLC have no parent corporations, and there are no public companies that own 10% or more of them. -

The Mercedes-Benz Truck Range

The Mercedes-Benz Truck range The big star in At Mercedes-Benz we are dedicated to providing each and every one of our customers with innovative and comprehensive solutions for total transport efficiency. We call this continued drive RoadEfficiency. So what does RoadEfficiency mean for you and your business? Low total costs Greater safety Maximised use Everything we do aims to deliver low Always ahead of the curve in truck Mercedes-Benz Uptime ensures maximum total costs for our customers, from the innovation, Mercedes-Benz Trucks now availability of your vehicles at all times. outset and throughout a truck’s life. offer the latest in safety systems. It is a ground-breaking service product, › Innovative, market leading fuel-saving › Active Brake Assist 4 with pedestrian based on real-time monitoring of your technology – our 2nd generation safety – this technology is unrivalled vehicles, significantly increasing the engines and powertrain can achieve by any other truck manufacturer. efficiency of your fleet. Uptime builds up to 6% fuel savings. upon the telematics and connectivity- based innovations we’ve been offering › Low repair and maintenance costs with Fleetboard for over 15 years. › Competitive finance options › High residual values Contents Everything we do is driven by our total commitment to deliver RoadEfficiency to each and every one of our customers. Low total costs + greater safety + maximised use For more information on any of our models, to find your nearest Dealer or to download a brochure, please visit: Efficiency is the sum of the details Visit mercedes-benz.com/roadefficiency for more details mbtrucks.co.uk Atego The Atego is a winner on all fronts, offering the attributes to suit your tasks whatever the application. -

2019 RAM 1500 Truck Owner Manual

2019 RAM 1500 2019 RAM 1500 OWNER’S MANUAL 19DS-126-AC ©2018 FCA US LLC. All Rights Reserved. Third Edition Ram is a registered trademark of FCA US LLC. Printed in the U.S.A. VEHICLES SOLD IN CANADA This manual illustrates and describes the operation of With respect to any Vehicles Sold in Canada, the name features and equipment that are either standard or op- FCA US LLC shall be deemed to be deleted and the name tional on this vehicle. This manual may also include a FCA Canada Inc. used in substitution therefore. description of features and equipment that are no longer DRIVING AND ALCOHOL available or were not ordered on this vehicle. Please Drunken driving is one of the most frequent causes of disregard any features and equipment described in this accidents. manual that are not on this vehicle. Your driving ability can be seriously impaired with blood FCA US LLC reserves the right to make changes in design alcohol levels far below the legal minimum. If you are and specifications, and/or make additions to or improve- drinking, don’t drive. Ride with a designated non- ments to its products without imposing any obligation drinking driver, call a cab, a friend, or use public trans- upon itself to install them on products previously manu- portation. factured. WARNING! Driving after drinking can lead to an accident. Your perceptions are less sharp, your reflexes are slower, and your judgment is impaired when you have been drinking. Never drink and then drive. Copyright © 2018 FCA US LLC SECTION TABLE OF CONTENTS PAGE 1 1 INTRODUCTION ...................................................................3 -

Investigation of Class 2B Trucks (Vehicles of 8,500 to 10,000 Lbs GVWR)

ORNL/TM-2002/49 Investigation of Class 2b Trucks (Vehicles of 8,500 to 10,000 lbs GVWR) March 2002 Stacy C. Davis Lorena F. Truett DOCUMENT AVAILABILITY Reports produced after January 1, 1996, are generally available free via the U.S. Department of Energy (DOE) Information Bridge: Web site: http://www.osti.gov/bridge Reports produced before January 1, 1996, may be purchased by members of the public from the following source: National Technical Information Service 5285 Port Royal Road Springfield, VA 22161 Telephone: 703-605-6000 (1-800-553-6847) TDD: 703-487-4639 Fax: 703-605-6900 E-mail: [email protected] Web site: http://www.ntis.gov/support/ordernowabout.htm Reports are available to DOE employees, DOE contractors, Energy Technology Data Exchange (ETDE) representatives, and International Nuclear Information System (INIS) representatives from the following source: Office of Scientific and Technical Information P.O. Box 62 Oak Ridge, TN 37831 Telephone: 865-576-8401 Fax: 865-576-5728 E-mail: [email protected] Web site: http://www.osti.gov/contact.html This report was prepared as an account of work sponsored by an agency of the United States Government. Neither the United States government nor any agency thereof, nor any of their employees, makes any warranty, express or implied, or assumes any legal liability or responsibility for the accuracy, completeness, or usefulness of any information, apparatus, product, or process disclosed, or represents that its use would not infringe privately owned rights. Reference herein to any specific commercial product, process, or service by trade name, trademark, manufacturer, or otherwise, does not necessarily constitute or imply its endorsement, recommendation, or favoring by the United States Government or any agency thereof. -

Conversion of a Gasoline Internal Combustion Engine to a Hydrogen Engine

Paper ID #3541 Conversion of a Gasoline Internal Combustion Engine to a Hydrogen Engine Dr. Govind Puttaiah P.E., West Virginia University Govind Puttaiah is the Chair and a professor in the Mechanical Engineering Department at West Virginia University Institute of Technology. He has been involved in teaching mechanical engineering subjects during the past forty years. His research interests are in industrial hydraulics and alternate fuels. He is an invited member of the West Virginia Hydrogen Working Group, which is tasked to promote hydrogen as an alternate fuel. Timothy A. Drennen Timothy A. Drennen has a B.S. in mechanical engineering from WVU Institute of Technology and started with EI DuPont de Nemours and Co. in 2010. Mr. Samuel C. Brunetti Samuel C. Brunetti has a B.S. in mechanical engineering from WVU Institute of Technology and started with EI DuPont de Nemours and Co. in 2011. Christopher M. Traylor c American Society for Engineering Education, 2012 Conversion of a Gasoline Internal Combustion Engine into a Hydrogen Engine Timothy Drennen*, Samual Brunetti*, Christopher Traylor* and Govind Puttaiah **, West Virginia University Institute of Technology, Montgomery, West Virginia. ABSTRACT An inexpensive hydrogen injection system was designed, constructed and tested in the Mechanical Engineering (ME) laboratory. It was used to supply hydrogen to a gasoline engine to run the engine in varying proportions of hydrogen and gasoline. A factory-built injection and control system, based on the injection technology from the racing industry, was used to inject gaseous hydrogen into a gasoline engine to boost the efficiency and reduce the amount of pollutants in the exhaust. -

2002 Combined Truck Vehicle Base Prices

2002 CHEVROLET PICKUP TRUCKS 2002 CHEVROLET PICKUP TRUCKS AND VANS SAMPLE VIN: 1GCDC14H32F000000 AND VANS (continued) MODEL: C14 BODY TYPE MODEL WEIGHT BASE PRICE BODY TYPE MODEL WEIGHT BASE PRICE CHEVROLET AVALANCHE 1500 1/2 TON CHEVROLET K-2500 SILVERADO PICKUP 3/4 TON − 4 x 4 (cont.) 4 Door Pickup − 4 x 2 C13 5,400 $29,397 Extended Cab − 8’ − Base Model K29 5,824 $28,382 4 Door Pickup − 4 x 4 K13 5,652 32,761 Extended Cab − 8’ − LS K29 5,824 30,184 Extended Cab − 8’ − LT K29 5,824 34,588 CHEVROLET AVALANCHE 2500 3/4 TON Crew Cab − 6 1/2’ K23 5,879 29,725 4 Door Pickup − 4 x 2 C23 5,400 31,150 Crew Cab − 6 1/2’ − LS K23 5,879 31,717 4 Door Pickup − 4 x 4 K23 5,652 34,670 Crew Cab − 6 1/2’ − LT K23 5,879 36,220 CHEVROLET S-10 PICKUP 1/2 TON − 4 x 2 Crew Cab − 8’ K23 6,025 30,025 Fleetside − 6’ Box S14 3,016 13,625 Crew Cab − 8’ − LS K23 6,025 32,017 Fleetside − 6’ Box − LS S14 3,016 14,607 Crew Cab − 8’ − LT K23 6,025 36,520 Fleetside − Extended Cab − 6’ S19 3,198 15,607 CHEVROLET C-3500 SILVERADO PICKUP 1 TON − 4 x 2 Fleetside − Extended Cab − 6’ − LS S19 3,198 16,607 Regular Cab C34 5,674 24,039 Regular Cab − LS C34 5,674 25,521 CHEVROLET S-10 PICKUP 1/2 TON − 4 x 4 Fleetside − Extended Cab − 6’ T19 3,761 19,325 Extended Cab C39 5,935 26,819 Fleetside − Extended Cab − 6’ − LS T19 3,761 20,307 Extended Cab − LS C39 5,935 28,301 Crew Cab T13 4,039 23,999 Extended Cab − LT C39 5,935 32,426 Crew Cab C33 6,103 28,244 CHEVROLET C-1500 SILVERADO PICKUP 1/2 TON − 4 x 2 Crew Cab − LS C33 6,103 29,916 Regular Cab − 6 1/2’ Box − Base Model C14 -

European Commission

C 268/18 EN Offi cial Jour nal of the European Union 14.8.2020 PROCEDURES RELATING TO THE IMPLEMENTATION OF COMPETITION POLICY EUROPEAN COMMISSION Prior notification of a concentration (Case M.9572 – BMW/Daimler/Ford/Porsche/Hyundai/Kia/IONITY) Candidate case for simplified procedure (Text with EEA relevance) (2020/C 268/06) 1. On 7 August 2020, the Commission received notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 (1). This notification concerns the following undertakings: — BMW AG (‘BMW’, Germany), — Daimler AG (‘Daimler’, Germany), — Ford Motor Company (‘Ford’, USA), — Dr Ing. h.c. F. Porsche Aktiengesellschaft (‘Porsche’, Germany). Porsche is part of the Volkswagen Group, — Hyundai Motor Company (‘Hyundai’, South Korea), which indirectly controls Kia Motor Corporation (‘Kia’, South Korea). Hyundai and Kia (together ‘Hyundai’) both belong to the Hyundai Motor Group (South Korea). BMW, Daimler, Ford, Porsche and Hyundai acquire within the meaning of Article 3(1)(b) and Article 3(4) of the Merger Regulation joint control of the whole of IONITY Holding GmbH & Co. KG (‘IONITY’, Germany), a full function joint venture established in 2017 by BMW, Daimler, Ford and Porsche. The concentration is accomplished by way of purchase of shares. 2. The business activities of the undertakings concerned are: — for BMW: is globally active in the development, production and marketing of passenger cars and motorbikes. BMW and its affiliates also provide financial services for private and business customers, -

Daimler Truck North America Launche Reward Program

Daimler Truck North America Launche Reward Program 03 26, 2014 Contact: [email protected] LOUISVILLE, Ky., – (March 26, 2014) – Daimler Trucks North America (DTNA) is pleased to announce the official launch of its new customer rewards program for those who are searching for quality commercial truck and bus parts and services. The Truck Bucks℠ rewards program, rewards customers that shop within the DTNA network of Freightliner, Western Star, Detroit™ and Thomas Built Buses retail locations, while opening up a new channel of communication with its aftermarket customers across all brands. Through the Truck Bucks℠ rewards program, customers who are members of the program receive special incentives throughout the year. Specials include discounts on select parts and services, which are automatically deducted at checkout without the need for coupons or further action by the customer. “Truck Bucks℠ is a great opportunity for us to reward our customers for the parts and services that they purchase every day,” explains Paul Tuomi, director dealer and fleet parts sales, Daimler Trucks North America. “This rewards program will allow us to get closer to our best customers, and help us provide a better aftermarket experience.” With close to 800 retail locations, DTNA is one of the largest retail networks in the industry. DTNA has taken great lengths to improve the customer experience through the integration of new technologies and operational efficiencies at every stage of the customer ownership cycle. “We recognize that today, fleets and owneroperators are very conscious of their total cost of ownership,” added Tuomi. “To us, that means our parts and service operations have to be exceptional and provide value to our customers; this rewards program keeps us focused on that goal.” Customers are able to sign up for Truck Bucks online starting April 1 at www.MyTruckBucks.com or at any Freightliner, Western Star, Detroit™ or Thomas Built Buses retail location across the country. -

01 14 Canada Sales by Model.Qxp

Canada light-vehicle sales by nameplate, January 2014 Vehicles are domestic unless noted. Jan. Jan. Jan. Jan. Jan. Jan. Jan. Jan. 2014 2013 2014 2013 2014 2013 2014 2013 1 series (I) ........................................... 94 42 LaCrosse.............................................. 26 52 Rondo (I) ............................................. 387 216 IS (I)..................................................... 177 52 1 series (I) ........................................... 1 94 Regal.................................................... 43 98 Sedona (I)............................................ 36 78 LFA (I) .................................................. – 1 3 series (I) ........................................... 374 676 Verano.................................................. 222 226 Sorento ................................................ 864 753 LS (I).................................................... 12 11 4 series (I) ........................................... 111 – Total Buick car............................ 291 376 Sportage (I) ......................................... 413 422 Total Lexus car (I) ....................... 392 359 5 series (I) ........................................... 187 191 Enclave................................................. 167 195 Kia truck (D) .............................. 864 753 GX (I) ................................................... 60 26 6 series (I) ........................................... 27 18 Encore (I)............................................. 232 1 Kia truck (I) ..............................