Aboitiz Equity Ventures, Inc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report 2010 Mission

sharpening our focus AnnuAl report 2010 Mission: to create long-term value for all its stakeholders Brand EssEncE: passion for better ways Brand spikEs • Driven • Driven to lead • Driven to excel • Driven to Serve corporatE ValuEs • passion • Innovation • professionalism • Integrity About the cover: Aboitiz equity Ventures, Inc. (AeV) has achieved unprecedented growth through the years, having expanded into power generation and distribution, banking and food. As it advances into another period filled with opportunities and challenges, AeV opts to sharpen its focus on its core strengths and maximize its potentials. TABLE OF CONTENTS 02 Financial Highlights Report to Stockholders 04 From your Chairman and President & CEO Results of Operations 08 Power 14 Financial Services 18 Food 20 Transport 22 From your Chief Financial Officer 25 From your Chief Risk Management Officer 26 Risk Management Report 28 From your Chief Compliance Officer 29 Corporate Governance Report FEATURES 42 CitySavings prepares to take on Luzon 44 Running the good race 46 Sustainability Statement 48 CSR: Helping people help themselves 50 Board of Directors / Board Committees 52 Corporate Officers 54 Operating Unit Heads 55 Management Directory 56 Location of Operations 57 Corporate Structure 58 Audit Committee Report 59 Statement of Management Responsibility 60 Independent Auditors’ Report 62 Consolidated Financial Statement The complete Securities & Exchange Commission Form 20-IS (Information Statement) and Annual Report is inside the CD inserted at the inside back cover -

Communication Management Category 1: Internal Communcation List of Winners Title Company Entrant's Name AGORA 2.0 Aboitiz Equity Ventures, Inc

Division 1: Communication Management Category 1: Internal Communcation List of Winners Title Company Entrant's Name AGORA 2.0 Aboitiz Equity Ventures, Inc. Lorenne Alejandrino-Anacta Keep It Simple, Sun Lifers: Gamifying A Simple Language Sun Life Financial Philippines Campaign Donante Aaron Peji Data Defenders: Data Privacy Lessons Made Fun and Sun Life Financial Philippines Engaging For Sun Life Employees Donante Aaron Peji PLDT Group Data Privacy Office Handle With Care Ramon R. Isberto Campaign PLDT Aboitiz Equity Ventures, Inc. (Pilmico Foods Super Conversations with SMA Corporation) Lorenne Alejandrino-Anacta Inside World: Engaging a new generation of Megaworld employees via a dynamic e-newsletter Megaworld Corporation Harold C. Geronimo Harnessing SYKES' Influence from Within to Inspire Beyond Reach Sykes Asia, Incorporated Miragel Jan Gabor ManilaMed's #FeelBetter Campaign Comm&Sense Inc. Aresti Tanglao Category 2: Employee Engagement Title Company Entrant's Name LOVE Grants Resorts World Manila Archie Nicasio a.Lab Aboitiz Equity Ventures, Inc. Lorenne V. Alejandrino CineNRW Maynilad Water Services, Inc Sherwin DC. Mendoza Central NRW Point System Maynilad Water Services, Inc Sherwin DC. Mendoza Leadership with a Heart Megaworld Foundation Dr. Francisco C. Canuto Dare 2B Fit ALLIANZ PNB LIFE INSURANCE, INC. ROSALYN MARTINEZ Category 3: Human Resources and Benefits Communication Title Company Entrant's Name Recruitment in the Social Media Era Manila Electric Company Gavin D. Barfield Category 5: Safety Communication Title Company Entrant's Name Championing cybersecurity awareness Bank of the Philippine Islands (BPI) Owen L. Cammayo Unang Hakbang Para Sa Kaligtasan: 2018 First Working MERALCO - Organizational Safety and Day Safety Campaign Resiliency Office Antonio Abuel Jr. -

Diversification Strategies of Large Business Groups in the Philippines

Philippine Management Review 2013, Vol. 20, 65‐82. Diversification Strategies of Large Business Groups in the Philippines Ben Paul B. Gutierrez and Rafael A. Rodriguez* University of the Philippines, College of Business Administration, Diliman, Quezon City 1101, Philippines This paper describes the diversification strategies of 11 major Philippine business groups. First, it reviews the benefits and drawbacks of related and unrelated diversification from the literature. Then, it describes the forms of diversification being pursued by some of the large Philippine business groups. The paper ends with possible explanations for the patterns of diversification observed in these Philippine business groups and identifies directions for future research. Keywords: related diversification, unrelated diversification, Philippine business groups 1 Introduction This paper will describe the recent diversification strategies of 11 business groups in the Philippines. There are various definitions of business groups but in this paper, these are clusters of legally distinct firms with a managerial relationship, usually by virtue of common ownership. The focus on business groups rather than on individual firms has to do with the way that business firms in the Philippines are organized and managed. Businesses that are controlled and managed by essentially the same set of principal owners are often organized as separate corporations, not as separate divisions within the same firm, as is often the case in American corporations like General Electric, Procter and Gamble, or General Motors (Echanis, 2009). Moreover, studies on emerging markets have pointed out that business groups often occupy dominant positions in the business landscape in markets like India, Korea, Indonesia, Thailand, and the Philippines (Khanna & Palepu, 1997; Khanna & Yafeh, 2007). -

2015 Issue 2

The Official Publication of the Aboitiz Group • www.aboitiz.com • 2nd Issue 2015 Aboitiz Group achieves Project Forward CSR 2.0: a defining Risk Maturity Level 4 in full force to metric towards inclusive P. 5 achieve 1AP & sustainable growth P. 19 P.43 contents Cover Story Banking CSR 4 The Role of the Corporate Center 30 UnionBank celebrates 33 years of Making Da Diff 43 CSR 2.0: A defining metric towards inclusive & sustainable growth 31 First-ever UnionBank Mr. & Ms. DNA Ambassadors named 44 Education 45 Health & Well-Being Corporate Center 31 UnionBank Internal Audit Division bags top 50 Other News 5 Aboitiz Group achieves Risk Maturity Level 4 certification 32 UnionBank RBC Makati Region holds 51 WeatherPhilippines conducts its first 6 Coaching and Mentoring Course launched Weather 101 training for an LGU in the Aboitiz Group investment briefing 32 CitySavings 2015 Sales Rally 51 Understanding our weather empowers the 7 Aboitiz honors bankers and brokers at Filipino nation annual cocktail parties 33 CitySavings launches new branches in Luzon, 8 Key learnings from the Aboitiz brand Mindanao, and NCR forum 33 Shaping the financial industry with 10 22 Aboitiz Toastmasters inducted in Taguig UnionBank’s UITF RAFI 11 Aboitiz Groupwide Inspired by Passion 34 MAA and AAL: Recognizing CitySavings’ pillars 52 RAFI’s Kool Adventure Camp promotes Disaster Team Awards 2014 Response Principles at RESCYouth 2014 12 EIA Messages 53 Cash aid for Samar families affected by Food Typhoon Ruby 14 Aboitiz kicks off Groupwide Sportsfest 2015 53 Cebu is -

Metro Pacific Investments

07 June 2013 Asia Pacific/Philippines Equity Research Conglomerates Metro Pacific Investments (MPI.PS / MPI PM) Rating OUTPERFORM* Price (06 Jun 13, P) 5.86 INITIATION Target price (P) 7.90¹ Upside/downside (%) 34.8 Mkt cap (P mn) 152,456 (US$ 3,620) Hospitals biz deserves a second look Enterprise value (P mn) 189,919 ■ Initiate with OUTPERFORM. We initiate coverage on Metro Pacific Number of shares (mn) 26,016.46 Investments with an OUTPERFORM rating and a P7.90 target price, Free float (%) 43.9 52-week price range 6.29 - 3.92 implying 35% potential upside. Our target price is SOTP-based and ADTO - 6M (US$ mn) 6.1 translates to an implied 2014E PER of 20.6x and PBR of 2.0x (sector *Stock ratings are relative to the coverage universe in each average of 18.0x and 2.2x, respectively). The company focuses on water, analyst's or each team's respective sector. ¹Target price is for 12 months. power, toll roads, and hospitals. We forecast that hospitals will contribute 11% to 2014E net profit but we estimate that its NAV contribution is more Research Analysts substantial at 20%. Alvin Arogo ■ Multi-year growth potential for hospitals. Metro Pacific manages and 63 2 858 7716 [email protected] operates various privately held hospitals and we forecast its total beds to witness an 18% CAGR to 3,000 by 2015. This would be the main driver for Gab Roque 63 2 858 7756 the 47% CAGR in its net income contribution, in our view. -

In the Philippines, We Have Several Blue Chip Companies That Are Being Traded in the Philippine Stock Market

In the Philippines, we have several blue chip companies that are being traded in the Philippine Stock Market. These blue chip companies were chosen based on GEMSS Growth Profitability Earnings Visibility Management Credibility Superior Products/Services Strong Balance Sheet Thirty blue-chip stocks listed on the Philippine Stock Exchange are included in the 210 most exciting stocks in the Asean Exchange, the newly launched common website of seven bourses in Southeast Asia. These 30 Philippine stocks mostly firms engaged in banking, real estate and utilities are part of the so-called Asean Stars, a selection of the largest and most dynamic Southeast Asian firms that are in the league of world leaders in their respective sectors. Blue Chips Class A Stocks All Stocks Preferred / By Sector Current Price Previous 52-Week High 52-Week Symbol Name PE (%) Close (%) Low AC Ayala Corporation 635 (-0.78%) 640 660 (3.94%) 485 35.568 Aboitiz Equity Ventures, AEV 54.8 (-0.27%) 54.95 61.6 (12.41%) 40 12.656 Inc. AGI Alliance Global Group, Inc. 28.45 (0.00%) 28.45 31.85 (11.95%) 20.25 21.014 ALI Ayala Land, Inc. 30.3 (-3.19%) 31.3 33.3 (9.90%) 23 46.119 AP Aboitiz Power Corporation 36 (-1.10%) 36.4 42.6 (18.33%) 30 10.843 BDO BDO Unibank, Inc. 88.9 (-2.52%) 91.2 93.5 (5.17%) 66.2 22.281 Bloomberry Resorts BLOOM 10.68 (0.00%) 10.68 12.52 (17.23%) 8.28 152.571 Corporation Bank of the Philippine 103.22 BPI 88.25 (-0.40%) 88.6 80.95 19.255 Islands (16.96%) DMC DMCI Holdings, Inc. -

SEC FORM 17-A (ANNUAL REPORT) (B) Has Been Subject to Such Filing Requirements for the Past 90 Days

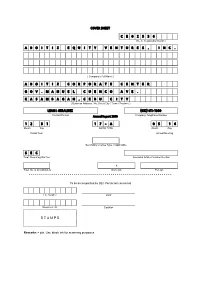

COVER SHEET CE02536 S.E.C. Registration Number ABOI T I Z EQU I TY VENTURES , INC . ( Company's Full Name ) ABOI T I Z CORPORATE CENTER GOV .MANUE L CUENCO AVE . KASAMBAGAN , CEBU C ITY ( Business Address: No. Street City / Town / Province ) LEAH I. GERALDEZ (032) 411-1800 Contact Person Annual Report 2010 Company Telephone Number 12 31 17-A 05 16 Month Day FORM TYPE Month Day Fiscal Year Annual Meeting Secondary License Type, if Applicable SEC Dept. Requiring this Doc Amended Articles Number/Section x Total No. of Stockholders Domestic Foreign - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - To be accomplished by SEC Personnel concerned File Number LCU Document I.D. Cashier S T A M P S Remarks = pls. Use black ink for scanning purposes SEC FORM 20 - IS (INFORMATION STATEMENT) DEFINITION OF TERMS Aboitiz Group ACO and the companies or entities in which AJMAN or AJMSI Aboitiz Jebsen Manpower Solutions, Inc. ACO has a beneficial interest and, directly or indirectly, exercises management control, including, without limitation, Ambuklao-Binga Refers to the 75 MW Ambuklao Aboitiz Equity Ventures, Inc., Aboitiz Power Hydroelectric Hydroelectric Power Plant of SNAP- Corporation, Union Bank of the Philippines Power Complex Benguet located in Bokod, Benguet and the and their respective Subsidiaries and 100 MW Binga Hydroelectric Power Plant of Affiliates SNAP-Benguet located at Itogon, Benguet Aboitiz Jebsen The Company’s joint venture with the AP Group Aboitiz Power Corporation and Group Jebsen Group of Norway and is composed its Subsidiaries of Aboitiz Jebsen Bulk Transport Corporation, Aboitiz Jebsen Manpower Solutions, Inc., Jebsen Maritime, Inc. and APRI AP Renewables, Inc. -

PHILIPPINES Typhoons Mangkhut (Ompong) / Yutu (Rosita) 3W As of 21 January 2019

PHILIPPINES Typhoons Mangkhut (Ompong) / Yutu (Rosita) 3W As of 21 January 2019 Ongoing and planned activities by province and cluster BATANES Province Cluster Ongoing Planned No. of Org. Abra FSAL 1 0 1 2,187 Multi-cluster 0 11 1 Apayao Nutrition 0 2 1 Protection 15 0 1 activities Early Recovery 1 0 1 Education 1 0 1 FSAL 19 1 3 52 organizations Benguet Health 0 5 1 Multi-cluster 2 1 2 Number of activities by status Shelter 6 15 2 ILOCOS (Note: 19 activities have undetermined status) NORTE WASH 18 0 1 APAYAO CAGAYAN 182 Cash 3 25 2 Planned 129 Early Recovery 3 0 1 Mangkhut path Ongoing FSAL 6 39 3 ABRA Health 1 0 2 South KALINGA China Cagayan Multi-cluster 7 16 4 Sea ILOCOS SUR NFI 1 0 1 MT. PROVINCE ISABELA 1,857 Protection 12 29 3 IFUGAO Completed 2 LA UNION Yutu path Shelter 4 9 WASH 13 0 4 BENGUET Ilocos Norte FSAL 1 7 1 NUEVA VIZCAYA QUIRINO Philippines Sea Number of ongoing and planned activities by cluster FSAL 1 0 1 88 Planned Ongoing Ilocos Sur Shelter 6 0 1 AURORA PANGASINAN Cash 4 1 1 NUEVA ECIJA Number of Isabela FSAL 3 2 3 56 activites by TARLAC Multi-cluster 0 5 1 Municipality ZAMBALES 42 41 Education 0 6 1 1 - 10 Kalinga PAMPANGA 33 31 FSAL 1 4 2 11 - 50 BULACAN 51 - 100 Mt. Province FSAL 0 1 1 Pangasinan FSAL 0 2 1 101 - 200 BATAAN RIZAL 7 6 4 MANILA 2 1 Total 129 181 > 200 CAVITE LAGUNA Multi- Early FSAL Protection cluster Shelter Cash WASH Education Health Recovery Nutrition NFI Note: 1 organization with no province location The boundaries, names shown and the designations used on this map do not imply official endorsement or acceptance by the United Nations. -

Corporate Governance Issues in Listed Philippine Companies by Arthur S

Corporate Governance Issues in Listed Philippine Companies By Arthur S. Cayanan Presentation Outline I. Introduction II. Objectives of the Study III. Methodology IV. Findings V. Conclusion What is Corporate Governance Corporate Governance is defined as the system of stewardship and control to guide organizations in fulfilling their long-term economic, moral, legal and social obligations towards their stakeholders.* *From the Code of Corporate Governance for Publicly-Listed Companies. Objectives of the Study 1. To assess some corporate governance practices of the 30 PSEi- indexed stocks, e.g. ownership structure, related party transactions, different individuals holding the positions of the chairman of the BOD and CEO, and tender offers. 2. To raise questions on the effectiveness of the regulatory regime in protecting the interest of the minority stockholders. Methodology 1. Reviewed Code of Corporate Governance for publicly listed companies issued by the Securities and Exchange Commission (SEC) in 2016. 2. Reviewed Corporation Code of the Philippines, especially the provisions of the code which require at least two-third (2/3) votes of the capital stock for a decision to be carried out by a company. 3. Reviewed the 2017 annual reports of the 30 listed Philippine companies which comprise the Philippine stock index (PSEi), with emphasis on their respective members of the board of directors, top stockholders with voting rights, and the process for nominating directors. Company Float as of October 22, 2018 1Ayala Corporation (AC) 43% 2Aboitiz Equity Ventures (AEV) 45% 3Alliance Global, Inc. (AGI) 31% 4Ayala Land Inc. (ALI) 52% 5Aboitiz Power Corporation (AP) 19% 6BDO Unibank, Inc. (BDO) 45% 7Bank of the Philippine Islands (BPI) 48% 8DMCI Holdings, Inc. -

Retire Smart-FFS-2040

Fund Fact Sheet as of January 31, 2019 Retire Smart 2040 Fund INVESTMENT OBJECTIVE To provide long term appreciation of fund assets to support retirement needs of each cohort by adjusting its underlying asset mix over time. The fund provides diversification by gradually reducing risky assets and increasing exposure to safer assets as the target retirement date approaches [2040]. HISTORICAL PERFORMANCE FUND INFORMATION Since inception Inception date 5-June-17 11.0 Fund currency PHP Fund manager AXA Philippines, Metrobank-Trust 10.5 Custodian bank Citibank N.A. Asset management charge 2.25% 10.0 FUND DETAILS 9.5 Net asset value (NAV) 5.7mn NAV per unit (12/28/18) 9.5 9.0 Initial NAV per unit 10.0 Highest NAV per unit 10.6 8.5 Lowest NAV per unit 8.4 8.0 Jun-17 Sep-17 Jan-18 May-18 Sep-18 Jan-19 CUMULATIVE AND ANNUALIZED PERFORMANCE CUMULATIVE ANNUALIZED Total net Year-to-date 5-year Since inception Year-to-date 5-year Since inception return 5.3% N/A -4.8% 5.3% N/A -2.9% Cumulative is the TOTAL earnings performance of the fund in a given number of years. Annualized is the compounded annual growth rate, or the simulated growth rate on a yearly basis if principal plus Interest are re-invested annually. ASSET ALLOCATION TOP 10 EQUITY HOLDINGS 2.0% Fund % 3.8% Cash Corporate FI 1 -SM INVESTMENTS CORP 13.5% 2 -SM PRIME HOLDINGS INC 8.8% 3 -AYALA LAND INC 8.8% 15.6% Government FI 4 -BDO UNIBANK INC 6.9% 5 -AYALA CORPORATION 6.5% 6 -BANK OF PHILIPPINE ISLANDS 5.1% 78.6% 7 -JG SUMMIT HOLDINGS INC 4.9% Equity 8 -METROPOLITAN BANK & TRUST 4.2% 9 -JOLLIBEE FOODS CORPORATION 4.2% 10 -ABOITIZ EQUITY VENTURES INC 3.9% Allocation based on Net Asset Value Report and adjusted for unsettled trade transactions. -

Philequity Corner (June 6, 2011) by Valentino Sy the Big Boys in A

Philequity Corner (June 6, 2011) By Valentino Sy The Big Boys In a previous article (Does Size Matter?, 9 May 2011), we ranked listed companies in the index by various metrics. As expected, we had companies from different sectors filling up the list. For this article though, we will focus on the largest listed conglomerates (the “Big Boys”). Not only are these holding companies a representation of the Philippine economy, they are also the biggest listed companies in the Philippine stock exchange. There are, however, a number of conglomerates as well as subsidiaries of the companies enumerated below that are not listed. Since investors cannot participate in these, we will limit our discussion only to listed companies. Jacks of all Trades A conglomerate is a holding company that owns a significant stake in a number of subsidiaries which conduct business through distinct corporate vehicles. Thus, a conglomerate can have exposure to different sectors without affecting its own operations. For instance, FPH is exposed to both energy and media. While the businesses are generally unrelated, the choice of subsidiaries is usually part of an overall strategy to create synergy and increase efficiency yet still have a singular corporate structure. Owning both a bank and a property company is one example of a symbiotic relationship in a well- managed conglomerate. Ranking the Big Boys Below, we ranked the various conglomerates (the “Big Boys”) by market capitalization as of June 3, 2011, sales and net income (Table 1). In addition, a breakdown of the top 5 holding companies’ listed subsidiaries will be provided (Tables 2-6). -

PSE PDEX EQUITY BONDS CP ETF 1 2GO Group, Inc. √ √ 2 8990 Holdings, Inc. √ √ √ √ 3 a Brown Company, Inc. √ √ 4 A

LISTED INSTRUMENT No. REGISTERED ISSUER OF SECURITIES TO THE PUBLIC PSE PDEX EQUITY BONDS CP ETF 1 2GO Group, Inc. √ √ 2 8990 Holdings, Inc. √ √ √ √ 3 A Brown Company, Inc. √ √ 4 A. Soriano Corporation √ √ 5 AbaCore Capital Holdings, Inc. √ √ 6 Aboitiz Equity Ventures, Inc. √ √ √ √ 7 Aboitiz Power Corporation √ √ √ √ 8 Abra Mining and Industrial Corporation √ √ 9 ABS-CBN Holdings Corporation √ √ √ √ 10 Acesite (Phils.) Hotel Corporation √ √ 11 AG Finance, Incorporated √ √ 12 AgriNurture, Inc. √ √ 13 Alliance Global Group, Inc. √ √ 14 Alliance Select Foods International, Inc. √ √ 15 Alsons Consolidated Resources, Inc. √ √ 16 Anchor Land Holdings, Inc. √ √ 17 Anglo Philippine Holdings Corporation √ √ 18 APC Group, Inc. √ √ 19 Apex Mining Co., Inc. √ √ 20 Araneta Properties, Inc. √ √ 21 Arthaland Corporation √ √ 22 Asia Amalgamated Holdings Corporation √ √ 23 Asia United Bank Corporation √ √ 24 Asiabest Group International Inc. √ √ 25 Asian Terminals, Inc. √ √ 26 Atlas Consolidated Mining and Development Corporation √ √ 27 ATN Holdings, Inc. √ √ 28 Atok-Big Wedge Co., Inc. √ √ 29 Ayala Corporation √ √ √ √ 30 Ayala Land, Inc. √ √ √ √ 31 Bank of the Philippine Islands √ √ 32 Basic Energy Corporation √ √ 33 BDO Leasing and Finance, Inc. √ √ √ 34 BDO Unibank, Inc. √ √ 35 Belle Corporation √ √ 36 Benguet Corporation √ √ 37 Berjaya Philippines Inc. √ √ 38 BHI Holdings, Inc. √ √ 39 Bloomberry Resorts Corporation √ √ 40 Bogo Medellin Milling Company, Inc. √ √ 41 Boulevard Holdings, Inc. √ √ 42 Bright Kindle Resources & Investment, Inc. √ √ 43 Calata Corporation √ √ 44 Cebu Air, Inc. √ √ 45 Cebu Holdings, Incorporated √ √ √ √ 46 Cebu Property Ventures and Development Corporation √ √ 47 Central Azucarera de Tarlac, Inc. √ √ 48 Centro Escolar University √ √ 49 Century Pacific Foods, Inc. √ √ 50 Century Peak Metals Holdings Corporation √ √ 51 Century Properties Group, Inc. √ √ √ 52 Chemical Industries of the Philippines, Inc.