The GVH Cleared Concentrations Relating to Magyar RTL Televízió Zrt

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Reuters Institute Digital News Report 2020

Reuters Institute Digital News Report 2020 Reuters Institute Digital News Report 2020 Nic Newman with Richard Fletcher, Anne Schulz, Simge Andı, and Rasmus Kleis Nielsen Supported by Surveyed by © Reuters Institute for the Study of Journalism Reuters Institute for the Study of Journalism / Digital News Report 2020 4 Contents Foreword by Rasmus Kleis Nielsen 5 3.15 Netherlands 76 Methodology 6 3.16 Norway 77 Authorship and Research Acknowledgements 7 3.17 Poland 78 3.18 Portugal 79 SECTION 1 3.19 Romania 80 Executive Summary and Key Findings by Nic Newman 9 3.20 Slovakia 81 3.21 Spain 82 SECTION 2 3.22 Sweden 83 Further Analysis and International Comparison 33 3.23 Switzerland 84 2.1 How and Why People are Paying for Online News 34 3.24 Turkey 85 2.2 The Resurgence and Importance of Email Newsletters 38 AMERICAS 2.3 How Do People Want the Media to Cover Politics? 42 3.25 United States 88 2.4 Global Turmoil in the Neighbourhood: 3.26 Argentina 89 Problems Mount for Regional and Local News 47 3.27 Brazil 90 2.5 How People Access News about Climate Change 52 3.28 Canada 91 3.29 Chile 92 SECTION 3 3.30 Mexico 93 Country and Market Data 59 ASIA PACIFIC EUROPE 3.31 Australia 96 3.01 United Kingdom 62 3.32 Hong Kong 97 3.02 Austria 63 3.33 Japan 98 3.03 Belgium 64 3.34 Malaysia 99 3.04 Bulgaria 65 3.35 Philippines 100 3.05 Croatia 66 3.36 Singapore 101 3.06 Czech Republic 67 3.37 South Korea 102 3.07 Denmark 68 3.38 Taiwan 103 3.08 Finland 69 AFRICA 3.09 France 70 3.39 Kenya 106 3.10 Germany 71 3.40 South Africa 107 3.11 Greece 72 3.12 Hungary 73 SECTION 4 3.13 Ireland 74 References and Selected Publications 109 3.14 Italy 75 4 / 5 Foreword Professor Rasmus Kleis Nielsen Director, Reuters Institute for the Study of Journalism (RISJ) The coronavirus crisis is having a profound impact not just on Our main survey this year covered respondents in 40 markets, our health and our communities, but also on the news media. -

Press Release

PRESS RELEASE Collaboration between AGF and YouTube provides new evidence of the relevance of video in the German media landscape Frankfurt/Hamburg, Mar. 6th, 2019 — For the first time, the AGF Videoforschung (AGF) and YouTube published the results of their cooperation. Their collaboration started more than three years ago. The aim of this cooperation is to map the additional use of video through other platforms within the framework of the AGF convergence standard. The results for the observation period show that — with an average daily viewing time of 267 minutes for persons 18 years and older — the relevance of video in Germany is unbroken! During the study period, traditional linear TV usage averaged 232 minutes per day. Plus 35 minutes of streaming usage, mostly through mobile devices (60%). "It is a remarkable milestone for AGF's video research to have reached the current level together with YouTube. Everyone involved knows that we need to work continuously on this internationally unique project to best reflect the differentiated use of the platform in this dynamically changing technological environment. AGF's goal is to identify YouTube as a reliable, transparent partner in the AGF system, in line with the common market standard", said AGF Managing Director Kerstin Niederauer-Kopf. Dirk Bruns, Head of Video Sales, Google Germany: "We are very proud to be able to present the first results together with AGF Videoforschung and hope that industry representatives from other countries will follow the example of AGF. Google has long been committed to transparent measurement. And the presented data highlights the relevance of the YouTube platform for users, the advertising industry, and our content partners." 1 YouTube as platform in the AGF system Since April 2015, AGF and YouTube have collaborated intensively with the common goal of integrating the YouTube platform into the AGF system. -

Television Advertising Insights

Lockdown Highlight Tous en cuisine, M6 (France) Foreword We are delighted to present you this 27th edition of trends and to the forecasts for the years to come. TV Key Facts. All this information and more can be found on our This edition collates insights and statistics from dedi cated TV Key Facts platform www.tvkeyfacts.com. experts throughout the global Total Video industry. Use the link below to start your journey into the In this unprecedented year, we have experienced media advertising landscape. more than ever how creative, unitive, and resilient Enjoy! / TV can be. We are particularly thankful to all participants and major industry players who agreed to share their vision of media and advertising’s future especially Editors-in-chief & Communications. during these chaotic times. Carine Jean-Jean Alongside this magazine, you get exclusive access to Coraline Sainte-Beuve our database that covers 26 countries worldwide. This country-by-country analysis comprises insights for both television and digital, which details both domestic and international channels on numerous platforms. Over the course of the magazine, we hope to inform you about the pandemic’s impact on the market, where the market is heading, media’s social and environmental responsibility and all the latest innovations. Allow us to be your guide to this year’s ACCESS OUR EXCLUSIVE DATABASE ON WWW.TVKEYFACTS.COM WITH YOUR PERSONAL ACTIVATION CODE 26 countries covered. Television & Digital insights: consumption, content, adspend. Australia, Austria, Belgium, Brazil, Canada, China, Croatia, Denmark, France, Finland, Germany, Hungary, India, Italy, Ireland, Japan, Luxembourg, The Netherlands, Norway, Poland, Russia, Spain, Sweden, Switzerland, UK and the US. -

New Brochure & Film Newbrochure &Film

week 7 / 13 February 2014 PIONEERING SPIRIT How RTL Group made entertainment history PIONEERING SPIRIT How RTL Group bmaderochu entertainmentre & history New film week 7 / 13 February 2014 PIONEERING SPIRIT How RTL Group made entertainment history PIONEERING SPIRIT How RTL Group bmaderochu entertainmentre & history New film Cover Montage with covers of the Always Close To The Audience’s brochure and DVD Publisher RTL Group 45, Bd Pierre Frieden L-1543 Luxembourg Editor, Design, Production RTL Group Corporate Communications & Marketing k before y hin ou T p r in t backstage.rtlgroup.com backstage.rtlgroup.fr backstage.rtlgroup.de QUICK VIEW Happy anniversary, Plug RTL! Plug RTL p. 8–9 90 years of entertainment – captured, documented and celebrated Simon Cowell RTL Group plans return to p.4–7 The X Factor UK FremantleMedia p. 10 Mega marketing campaign for Big Picture Game Of Thrones p.12 RTL II p. 11 PEOPLE p. 13–15 In February 1924 Radio Luxembourg took to the airwaves. 90 years later, RTL Group is marking – and celebrating – the anniversary with a new brochure and film. Titled Always Close 90 YEARS To The Audience, both productions recount the vivid and rich events that OF ENTERTAINMENT – turned a modest radio station based in tiny CAPTURED, Luxembourg into the leading European DOCUMENTED AND entertainment network. CELEBRATED Luxembourg – 13 February 2014 RTL Group Collage from the Always Close To The Audience brochure: Autographe cards & advertisements for various activities 4 Hauled up in their attic in 1924, experimenting with a single radio transmitter, the Anen brothers couldn’t have begun to imagine that their modest Radio Luxembourg would not only become one of the most-listened-to and admired radio stations of their generation but would go on to develop into Europe’s largest commercial free-to-air broadcaster. -

Edition 2016 Entertain. Inform. Engage

EDITION 2016 FULL YEAR RESULTS ENTERTAIN. INFORM. ENGAGE. KEY FIGURES SHARE PRICE PERFORMANCE 01/01/2016 – 31/12/2016 + 6.8 % MDAX INDEX = 100 – 7.6 % EURO STOXX 600 MEDIA – 9.5 % RTL GROUP – 21.7 % PROSIEBENSAT1 RTL Group share price development for January to December 2016 based on the Frankfurt Stock Exchange (Xetra) against MDAX, Euro Stoxx 600 Media and ProSiebenSat1 11.5 % OTHER 10.7 % DIGITAL 48.0 % 21.2 % TV ADVERTISING CONTENT 4.5 % PLATFORM REVENUE 4.1 % RADIO ADVERTISING RTL Group Revenue Split In 2016, TV advertising accounted for 48.0 per cent of RTL Group’s total revenue, making the Group one of the most diversified groups when it comes to revenue. Content represented 21.2 per cent of the total, while greater exposure to fast-growing digital revenue streams and higher margin platform revenue will further improve the mix. 2 RTL Group Full-year results 2016 Key figures REVENUE 2012 – 2016 (€ million) EBITA 2012 – 2016 (€ million) 16 6,237 16 1,205 15 6,029 15 1,167 14 5,808 14 1,144* 13 5,824* 13 1,148** 12 5,998 12 1,078 * Restated for IFRS 11 * Restated for changes in purchase price allocation ** Restated for IFRS 11 NET PROFIT ATTRIBUTABLE TO RTL GROUP SHAREHOLDERS 2012 – 2016 (€ million) EQUITY 2012 – 2016 (€ million) 16 720 16 3,552 15 789 15 3,409 14 652* 14 3,275* 13 870 13 3,593 12 597 12 4,858 * Restated for changes in purchase price allocation * Restated for changes in purchase price allocation TOTAL DIVIDEND/ MARKET CAPITALISATION* 2012 – 2016 (€ billion) DIVIDEND YIELD PER SHARE 2012 – 2016 (€ ) (%) 16 10.7 16 -

No. Channel Logo Features Comeback HD App TV

Features No. Channel Logo TV start TV comfort ComeBack HD App 1 SRF 1 HD 2 SRF zwei HD 3 Das Erste HD 4 ZDF HD 5 SAT.1 HD 6 ProSieben HD 7 RTL HD 8 3+ HD 9 4+ HD 10 RTL II HD 11 VOX HD 12 5+ HD 13 kabel eins HD 14 sixx HD 15 TV24 HD 16 S1 HD 17 ORF 1 HD 18 ORF 2 HD 19 ARTE HD 20 SRF info HD 21 TeleZüri 22 Nickelodeon CH HD 23 SUPER RTL HD 24 ServusTV HD 25 MTV CH HD 26 VIVA CH HD 27 RTL NITRO HD 28 Puls 8 HD 29 TV25 HD 30 ntv CH HD 31 Eurosport HD 33 Discovery Channel HD 34 Animal Planet HD 35 HISTORY HD 36 TNT Serie HD 37 TNT Film HD 38 AXN HD 39 MTV LIVE HD 40 FashionTV HD ftv 41 CHTV HD 42 3sat HD 43 KiKA HD 44 NDR HD 45 WDR Fernsehen HD 46 SWR HD 47 BR HD 48 ZDF Neo HD 49 ZDFinfo HD 50 PHOENIX HD 51 ANIXE HD 52 DMAX 53 TLC 54 ProSieben MAXX CH 55 SAT.1 Gold 56 TELE 5 57 gotv 58 DELUXE MUSIC 59 Schweiz 5 60 STAR TV HD 61 wetter.tv 62 Eurosport 63 SPORT1 64 Disney Channel 65 NATIONAL GEOGRAPHIC CHANNEL 66 TNT Serie 67 TNT Film 68 hr-fernsehen 69 MDR FERNSEHEN 70 rbb Fernsehen 71 ARD-alpha 72 tagesschau24 73 Einsfestival 74 N24 75 euronews 76 Deutsche Welle 77 Bloomberg TV 78 Bibel TV 79 HSE24 80 Teleclub Zoom 81 RTS Deux HD Features No. -

Roadshow Presentation Brussels 21 June

RTL GROUP PRESENTATION Brussels, 21 June 2013 The leading European entertainment network Agenda ● Q1 HIGHLIGHTS o Business Review o Strategy Review 2 Quarter 1 highlights 2013 REVENUE €1.3 billion REPORTED EBITA continuing operations €207 million EBITA MARGIN CASH CONVERSION NET DEBT POSITION NET RESULT 15.6% 164% €278 million €133 million QUARTER 1 BUSINESSES STRATEGY STRONG OPERATIONAL RESULTS AND EXCEPTIONAL CASH GENERATION 3 Agenda o Q1 highlights ● BUSINESS REVIEW o Strategy Review 4 Leading integrated pan-European entertainment network with a truly global presence BROADCAST + CONTENT + DIGITAL P #1 in Europe P #1 global TV P Follow viewers entertainment across all platforms P #1 in Germany producer P Online network of P #1 in Benelux P Productions in 62 200+ websites countries >6.9bn video views #2 in France P P P Distribution into 150+ markets RTL Group 2012 QUARTER 1 Revenue EBITA BUSINESSES €6.0bn €1.1bn STRATEGY 5 RTL Group: at the heart of the European media ecosystem LARGEST EUROPEAN FTA BROADCASTER LARGEST EUROPEAN CONTENT PRODUCER / DISTR. 2012 CONSOLIDATED REVENUES (€BN) 2012 REVENUES (€MN) €6.0bn 1,711 €3.7bn 2x €2.7bn (a) 870 €2.6bn 12x 138 €2.4bn QUARTER 1 BUSINESSES Scale matters: first choice partner for advertisers, content creators and rights owners STRATEGY (a) Converted from £712 at Global Insight 2012 rate of 0.819 £/€ 6 Source: Screen Digest, company filings Leading positions in key European markets GERMANY FRANCE #1 #2 6 FTA channels 3 FTA channels 3 Pay channels 8 Pay channels #1 Audience/ad shr. #2 Audience/ad shr. 54% Group EBITA 21% Group EBITA NETHERLANDS BELGIUM #1 #1 4 FTA channels 3 Pay channels 3 FTA channels #1 Audience/ ad shr. -

Annual Report 2008 Annual Report the Leadingeuropeanentertainment Network

THE LEADING EUROPEAN ENTERTAINMENT NETWORK FIVE-YEAR SUMMARY 2008 2007 2006 2005 2004 €m €m €m €m €m Revenue 5,774 5,707 5,640 5,115 4,878 RTL Group – of which net advertising sales 3,656 3,615 3,418 3,149 3,016 Corporate Communications Other operating income 37 71 86 103 118 45, boulevard Pierre Frieden Consumption of current programme rights (2,053) (2,048) (1,968) (1,788) (1,607) L-1543 Luxembourg Depreciation, amortisation and impairment (203) (213) (217) (219) (233) T: +352 2486 5201 F: +352 2486 5139 Other operating expense (2,685) (2,689) (2,764) (2,518) (2,495) www.RTLGroup.com Amortisation and impairment of goodwill ANNUAL REPORT and fair value adjustments on acquisitions of subsidiaries and joint ventures (395) (142) (14) (16) (13) Gain/(Loss) from sale of subsidiaries, joint ventures and other investments (9) 76 207 1 (18) Profit from operating activities 466 762 970 678 630 Share of results of associates 34 60 72 63 42 Earnings before interest and taxes (“EBIT”) 500 822 1,042 741 672 Net interest income/(expense) 21 (4) 2 (11) (25) Financial results other than interest 7 26 33 2 (19) Profit before taxes 528 844 1,077 732 628 Income tax income/(expense) (232) (170) 34 (116) (196) Profit for the year 296 674 1,111 616 432 Attributable to: RTL Group shareholders 194 563 890 537 366 Minority interest 102 111 221 79 66 Profit for the year 296 674 1,111 616 432 EBITA 916 898 851 758 709 Amortisation and impairment of goodwill (including disposal group) and fair value adjustments on acquisitions of subsidiaries and joint ventures -

Appendix to the Responses of the Government of Hungary to the List Of

Appendix to the Responses of the Government of Hungary to the list of issues and questions with regard to the consideration of the combined seventh and eighth periodic report (CEDAW/C/HUN/7-8) Annex no. 1 Important cases of legal violations established by the Media Council 2008 RTL Klub – Fábry Show In decision no.583/2008. (III. 26.) the ORTT (National Committee for Radio and Television) found that the RTL Klub programme titled "Fábry Show" had committed a legal violation when the presenter, while discussing domestic political issues, made strong, vulgar comments of a sexual nature about the leader of the Hungarian Socialist Party faction, the largest governing party in parliament. Although the presenter apologised to the faction leader, he later countered his statement, noting that the government could also apologise for what they had done, in the light of which the earlier image is not an exaggeration. In the view of the Committee, what was said in that part of the programme put the socialist politician in an undignified and vulnerable position, and hurt her human dignity by making jokes which reduced her to a sexual object. The ORTT (the legal predecessor, until 2010, to the present media authority) found that the broadcasting company Magyar RTL Televízió Zrt. was in breach of Act I of 1996 on radio and television broadcasting (hereafter: Radio and TV Act),1 paragraph 3 (2) (protection of the right to human dignity in the media). In view of the breach, the Committee called upon the programme broadcaster to discontinue its unlawful conduct. 2009 TV2 - Mokka ("Mocha") In decision no. -

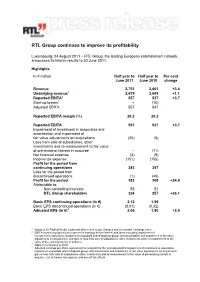

RTL Group Continues to Improve Its Profitability

RTL Group continues to improve its profitability Luxembourg, 24 August 2011 − RTL Group, the leading European entertainment network, announces its interim results to 30 June 2011. Highlights In € million Half year to Half year to Per cent June 2011 June 2010 change Revenue 2,751 2,661 +3.4 Underlying revenue1 2,679 2,649 +1.1 Reported EBITA2 557 537 +3.7 Start-up losses3 − (10) Adjusted EBITA 557 547 Reported EBITA margin (%) 20.2 20.2 Reported EBITA 557 537 +3.7 Impairment of investment in associates and amortisation and impairment of fair value adjustments on acquisitions (20) (5) Loss from sale of subsidiaries, other investments and re-measurement to fair value of pre-existing interest in acquiree − (11) Net financial expense (3) (9) Income tax expense (151) (155) Profit for the period from continuing operations 383 357 Loss for the period from discontinued operations (1) (49) Profit for the period 382 308 +24.0 Attributable to: Non-controlling interests 58 51 RTL Group shareholders 324 257 +26.1 Basic EPS continuing operations (in €) 2.12 1.99 Basic EPS discontinued operations (in €) (0.01) (0.32) Adjusted EPS (in €)4 2.06 1.90 +8.4 1 Adjusted for Radical Media, Ludia and other minor scope changes and at constant exchange rates 2 EBITA (continuing operations) represents earnings before interest and taxes excluding impairment of investment in associates, impairment of goodwill and of disposal group, and amortisation and impairment of fair value adjustments on acquisitions, and gain or loss from sale of subsidiaries, other investments -

Multi-Platform Programming for Digital TV

Multi-Platform Programming for Digital TV German-Japanese Symposium 2007 Session 7: New convergence based applications Berlin, April 20, 2007 Thomas Schultheis, Managing Director, SevenSenses GmbH Agenda German TV market overview Company and business overview Diversification - PayTV - Video on Demand - Mobile 2 Market overview German TV market: On average 54 TV stations per household Private FTA Private FTA Private FTA Public Stations Special Interest Pay TV 38.5%* 18.5%* 26.8%* 13.8%* 2.4%* (1st tier channels) (2nd tier channels) (3rd tier channels) ARD Sat.1 kabel eins ZDF ProSieben RTL II Arte 3Sat RTL VOX ARD Dritte (7 regional channels) Kinderkanal Phoenix et al. et al. Total TV households: 35 million Cable: ~20 million (54%), satellite: ~16.4 million (42%), terrestrial: ~2.1 million (5%) Conclusion: The German TV market, with an average of 54 TV stations per household**, is already fragmented * Audience market share Mon.-Sun., 03:00-03:00 h, viewers 14-49, average 2006; Private FTA Special Interest is the difference to the total of 100 ** Free-to-air and Pay TV channels; as at January 1, 2007 3 Basis: All TV households (Germany + EU), Source: AGF/GfK-Fernsehforschung, pc#tv aktuell, SevenOne Media Marketing & Research Agenda German TV market overview Company and business overview Diversification - PayTV - Video on Demand - Mobile 4 Company overview The ProSiebenSat.1 Media AG is the leading electronic media group in Germany. We provide people with first -class entertainment and comprehensive information – whenever they need it, wherever they are. Company overview ProSiebenSat.1Media AG – Company Trailer 6 Company overview The ProSiebenSat.1 Group ProSiebenSat.1 is the only Group that operates four wholly owned advertising financed TV stations in Germany and their related ancillary and diversification activities. -

C72f99e6-0E06-4C50-A755-473Aab0b2680 Worldreginfo - C72f99e6-0E06-4C50-A755-473Aab0b2680 Key Figures 2008 – 2012

WorldReginfo - c72f99e6-0e06-4c50-a755-473aab0b2680 WorldReginfo - c72f99e6-0e06-4c50-a755-473aab0b2680 Key Figures 2008 – 2012 shAre PriCe PerFormanCe 2008 – 2012 – 6.5 % (2012: – 1.9 %) INDEX = 100 rTl group dJ sToXX – 16.1 % (2012: + 17.5 %) r evenue (€ million) e quiTy (€ million) 12 5,998 12 4,858 11 5,765 11 5,093 10 5,532 10 5,597 09 5,156 09 5,530 08 5,774 08 5,871 e BiTA (€ million) M ArKeT Capitalisation (€ billion)* 12 1,078 12 11.7 11 1,134 11 11.9 10 1,132 10 11.9 09 796 09 7.3 08 916 08 6.6 *Asof31December n eT ProFiT AttriButaBle To rTl grouP shAreholders (€ million) To tal dividend Per shAre (€ ) 12 597 12 10.50 11 696 11 5.10 10 611 10 5.00 09 205 09 3.50 08 194 08 3.50 Dividend payout 2008− 2012: € 4.2 billion WorldReginfo - c72f99e6-0e06-4c50-a755-473aab0b2680 2012 A nnuAl rePorT T he leAding euro PeAn en TerTAinMenT n eTworK WorldReginfo - c72f99e6-0e06-4c50-a755-473aab0b2680 RTL Television’s AlarmfürCobra11, Germany’s most popular action series, has become a hit format in some 140 countries around the globe. Since 2012, it has been one of the signature series of the newly launched action channel, Big RTL Thrill, in India WorldReginfo - c72f99e6-0e06-4c50-a755-473aab0b2680 ConTenTs Corporate information 6 Chairman’s statement 8 Chief executives’ report 14 Profit centres at a glance 16 The year in review 16 Broadcast 34 Content 60 Digital 72 Red Carpet 76 Corporate responsibility 92 Operations 94 How we work 96 The Board / executive Committee Financial information 104 directors’ report 110 Mediengruppe RTL Deutschland 114 Groupe M6 117 FremantleMedia 120 RTL Nederland 123 RTL Belgium 126 RTL Radio (France) 128 Other segments 143 Management responsibility statement 144 Consolidated financial statements 149 Notes 210 Auditors’ report 212 RTl group overview 214 Credits 215 Fully consolidated profit centres at a glance 217 Five-year summary WorldReginfo - c72f99e6-0e06-4c50-a755-473aab0b2680 irman’s ChA enT stateM Thomas rabe ChairmaN of The board of DiRectors In 2012, RTL Group delivered solid financial results.