The Challenge of Providing Sufficient Grid Capacity for Electrification to Be a Key Factor in Achieving Climate Neutrality Until

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Download Full Text (Pdf)

http://www.diva-portal.org This is the published version of a chapter published in Approaches and methods in architectural research: Proceeding Series 2021-1. Citation for the original published chapter: Legeby, A. (2021) Developing station communities: Alternative approaches and perspectives on access In: M. Andersson, M. Rönn and A. E. Toft (ed.), Approaches and methods in architectural research: Proceeding Series 2021-1 (pp. 107-134). Göteborg: Nordic Academic Press of Architecture Research Proceeding Series 2021-1 N.B. When citing this work, cite the original published chapter. Permanent link to this version: http://urn.kb.se/resolve?urn=urn:nbn:se:kth:diva-300430 Nordisk Arkitekturforskning The Nordic Association of Architectural Research Proceedings Series 2021-1 APPROACHES AND METHODS IN ARCHITECTURAL RESEARCH Editors: Anne Elisabeth Toft, Magnus Rönn and Morgan Andersson Nordisk Arkitekturforskning The Nordic Association of Architectural Research Proceedings Series 2021-1 APPROACHES AND METHODS IN ARCHITECTURAL RESEARCH APPROACHES AND METHODS IN ARCHITECTURAL RESEARCH Proceeding Series 2021-1 PUBLISHER Nordic Academic Press of Architecture Research http://arkitekturforskning.net/na/issue/publishing EDITORS Anne Elisabeth Toft, Magnus Rönn and Morgan Andersson GRAPHIC DESIGN Jonas Vetlesen COPY-EDITING Dawn Michelle d'Atri, Rabea Berghäuser and Amy Springer PRINTING 07 Media © 2021 NAAR and authors All rights reserved The authors are responsible for copyrights for photographs, illustrations and images in their chapter. ISBN 978-91-983797-5-4 -

Elections Act the Elections Act (1997:157) (1997:157) 2 the Elections Act Chapter 1

The Elections Act the elections act (1997:157) (1997:157) 2 the elections act Chapter 1. General Provisions Section 1 This Act applies to elections to the Riksdag, to elections to county council and municipal assemblies and also to elections to the European Parliament. In connection with such elections the voters vote for a party with an option for the voter to express a preference for a particular candidate. Who is entitled to vote? Section 2 A Swedish citizen who attains the age of 18 years no later than on the election day and who is resident in Sweden or has once been registered as resident in Sweden is entitled to vote in elections to the Riksdag. These provisions are contained in Chapter 3, Section 2 of the Instrument of Government. Section 3 A person who attains the age of 18 years no later than on the election day and who is registered as resident within the county council is entitled to vote for the county council assembly. A person who attains the age of 18 years no later than on the election day and who is registered as resident within the municipality is entitled to vote for the municipal assembly. Citizens of one of the Member States of the European Union (Union citizens) together with citizens of Iceland or Norway who attain the age of 18 years no later than on the election day and who are registered as resident in Sweden are entitled to vote in elections for the county council and municipal assembly. 3 the elections act Other aliens who attain the age of 18 years no later than on the election day are entitled to vote in elections to the county council and municipal assembly if they have been registered as resident in Sweden for three consecutive years prior to the election day. -

Connecting Øresund Kattegat Skagerrak Cooperation Projects in Interreg IV A

ConneCting Øresund Kattegat SkagerraK Cooperation projeCts in interreg iV a 1 CONTeNT INTRODUCTION 3 PROgRamme aRea 4 PROgRamme PRIORITIes 5 NUmbeR Of PROjeCTs aPPROveD 6 PROjeCT aReas 6 fINaNCIal OveRvIew 7 maRITIme IssUes 8 HealTH CaRe IssUes 10 INfRasTRUCTURe, TRaNsPORT aND PlaNNINg 12 bUsINess DevelOPmeNT aND eNTRePReNeURsHIP 14 TOURIsm aND bRaNDINg 16 safeTy IssUes 18 skIlls aND labOUR maRkeT 20 PROjeCT lIsT 22 CONTaCT INfORmaTION 34 2 INTRODUCTION a short story about the programme With this brochure we want to give you some highlights We have furthermore gathered a list of all our 59 approved from the Interreg IV A Oresund–Kattegat–Skagerrak pro- full-scale projects to date. From this list you can see that gramme, a programme involving Sweden, Denmark and the projects cover a variety of topics, involve many actors Norway. The aim with this programme is to encourage and and plan to develop a range of solutions and models to ben- support cross-border co-operation in the southwestern efit the Oresund–Kattegat–Skagerrak area. part of Scandinavia. The programme area shares many of The brochure is developed by the joint technical secre- the same problems and challenges. By working together tariat. The brochure covers a period from March 2008 to and exchanging knowledge and experiences a sustainable June 2010. and balanced future will be secured for the whole region. It is our hope that the brochure shows the diversity in Funding from the European Regional Development Fund the project portfolio as well as the possibilities of cross- is one of the important means to enhance this development border cooperation within the framework of an EU-pro- and to encourage partners to work across the border. -

Företagarfakta Ystads Kommun

Företagarfakta Ystads kommun Februari 2020 2 Visste du att det finns 6 073 jobb i de små företagen i Ystads kommun? Och visste du att företagarna tillsammans med alla anställda i dessa företag bidrar med 391 miljoner kronor till kommunens skatteintäkter? Vi har sammanställt den här rapporten för att visa hur det lokala näringslivet ser ut och för att synliggöra småföretagens betydelse för din kommun. En stor majoritet av faktan kommer från Statistiska centralbyrån (SCB), men vi har också använt statistik från Arbetsförmedlingen, Skatteverket, Bolagsverket och Företagarnas egna undersökningar. Nästan alla företag vill växa och många vill anställa fler personer. Jobben som skapas i de privata företagen genererar inte bara inkomster till de anställda utan också till allmänheten. Vår förhoppning är att den här rapporten leder till en öppen dialog om det lokala näringslivsklimatet och hur villkoren för företagare i kommunen kan förbättras. Mår de mindre företagen bra mår hela Ystads kommun bra. Magnus Engelbäck, regionchef Företagarna Syd René Bongard, statistiker, Företagarna Företagarna företräder över 60 000 företagare och samhällsbärare och har ca 2 000 förtroendevalda. Vi erbjuder nätverk, kunskap och praktisk hjälp samt driver utvecklingen för ett bättre företagsklimat, så att företagare får rätt förutsättningar för att kunna utveckla sin verksamhet och nå sina mål. foretagarna.se | [email protected] | 08 – 406 17 00 3 Nästan alla företag är småföretag I Ystads kommun finns 3 096 arbetställen* som tillhör privata företag. Nio av tio är så kallade mikroföretag och har färre än tio anställda, och nästan alla har färre än 50 anställda. Under 2018 startades 66 750 nya företag i Sverige, varav 199 i Ystad (källa: Tillväxtanalys). -

Collaboration on Sustainable Urban Development in Mistra Urban Futures

Collaboration on sustainable urban development in Mistra Urban Futures 1 Contents The Gothenburg Region wants to contribute where research and practice meet .... 3 Highlights from the Gothenburg Region’s Mistra Urban Futures Network 2018....... 4 Urban Station Communities ............................................................................................ 6 Thematic Networks within Mistra Urban Futures ......................................................... 8 Ongoing Projects ............................................................................................................ 10 Mistra Urban Futures events during 2018 .................................................................. 12 Agenda 2030 .................................................................................................................. 14 WHAT IS MISTRA URBAN FUTURES? Mistra Urban Futures is an international research and knowledge centre for sustainable urban development. We develop and apply knowledge to promote accessible, green and fair cities. Co-production – jointly defining, developing and applying knowledge across different disciplines and subject areas from both research and practice – is our way of working. The centre was founded in and is managed from Gothenburg, but also has platforms in Skåne (southern Sweden), Stockholm, Sheffield-Manchester (United Kingdom), Kisumu (Kenya), and Cape Town (South Africa). www.mistraurbanfutures.org The Gothenburg Region (GR) consists of 13 municipalities The Gothenburg Region 2019. who have chosen -

Public Authorities' Use of Exhibition

Master Thesis in Science Communication Petter Börjesson Supervisor: Lars Broman Local supervisor: Elisabet Eronn Public Authorities' Use of Exhibition HDa-SC-06 2 3 Contents 1 Introduction 5 1.1 Public authorities 6 1.2 Learning theory 7 1.3 Informal learning in science centre 9 1.4 Exhibitions 14 1.5 Summarise of introduction 19 1.6 Acknowledgments 19 2 Methods 20 2.1 Public authorities 20 2.1.1 Interviews 20 2.1.2 Internet 21 2.1.3 Survey 22 2.2 Exhibition and exhibit 22 3 Observations 23 3.1 Public authorities 23 3.1.1 Summary of interviews 23 3.1.2 Internet search 25 3.1.3 Survey 26 3.2 Exhibition and exhibit 31 3.2.1 Exhibition 31 3.2.2 Exhibits from interviews 35 4 Results 40 4.1 Public authorities 40 4.2 Exhibitions 43 5 Discussion 46 5.1 Public authorities 47 5.2 Informal learning and exhibits 49 5.3 The use of experience 50 5.3.1 Moving exhibits to the visitors 50 5.4 Conclusions 52 6 References 53 Appendices 55 Appendix 1 55 A.1.1 Information and questions at interviews 55 Appendix 2 56 A.2.1 Address to museum and science centres in survey 56 Appendix 3 57 A.3.1 The survey 57 A.3.1 Complementary question 59 Appendix 4 60 A.4.1 Notes taken during interviews with public authorities. 60 Appendix 5 65 A.5.1 Answers to survey 65 Appendix 6 71 A.6.1 Background material for exhibition 71 4 Abstract This thesis studies the use of exhibitions by public authorities and the possibilities of making exhibits out of authority topics. -

Material Flow Analysis of Aggregates Case Studies of Two Municipalities in the Göteborg Region

Material Flow Analysis of Aggregates Case Studies of Two Municipalities in the Göteborg Region Master of Science Thesis EVA JOHANSSON Department of Energy and Environment Division of Environmental Systems Analysis CHALMERS UNIVERSITY OF TECHNOLOGY Göteborg, Sweden 2006 Report: 2006:5 MASTER OF SCIENCE THESIS Material Flow Analysis of Aggregates Case Studies of Two Municipalities in the Göteborg Region EVA JOHANSSON Environmental Systems Analysis Department of Energy and Environment CHALMERS UNIVERSITY OF TECHNOLOGY Göteborg, Sweden 2006 Material Flow Analysis of Aggregates Case Studies of Two Municipalities in the Göteborg Region © EVA JOHANSSON, 2006 Report 2006:5 ISSN 1404-8167 Environmental System Analysis Department of Energy and Environment Chalmers University of Technology SE-412 96 Göteborg, Sweden http://www.esa.chalmers.se Telephone + 46 (0)31 772 1000 http://www.chalmers.se Chalmers Reproservice Göteborg, Sweden 2006 Abstract The construction industry is a sector where resource demand is large. Some of the required resources are renewable and some are not. One resource which is without a doubt necessary in the construction industry is aggregates. Aggregates is a common name for sand, gravel, crushed rock and other bulk materials used by the construction industry. Out of the above mentioned materials sand and gravel are very limited and crushed bedrock is more abundant. Therefore it is better, from a resource point of view, to use crushed bedrock instead of sand and gravel for construction. Although, this substitution is complicated in some usage areas because of the better technical properties of sand and gravel. Sweden has an environmental quality objective limiting the extraction of gravel. -

Marine Spatial Planning from a Municipal Perspective

Marine Spatial Planning From a municipal perspective Authors Roger Johansson Frida Ramberg Supervisors Marie Stenseke Andreas Skriver Hansen Master’s thesis in Geography with major in human geography Spring semester 2018 Department of Economy and Society Unit for Human Geography School of Business, Economics and Law at University of Gothenburg Student essay: 45 hec Course: GEO245 Level: Master Semester/Year: Spring 2018 Supervisor: Marie Stenseke, Andreas Skriver Hansen Examinator: Mattias Sandberg Key words: Marine Spatial Planning, municipalities, knowledge, sustainable development Abstract Marine Spatial Planning (MSP) aims to, through physical planning of the marine areas, contribute to a sustainable development where various interests can get along. This master thesis concerns Marine Spatial Planning from a municipal perspective in Sweden. The aim of the thesis is to investigate how MSP is performed on a municipal level. In order to investigate this the thesis has been structured into three themes; The work with marine spatial planning, Marine spatial planning and synergies between marine and terrestrial areas and lastly, Environment and growth in marine spatial planning. It is important to remember that the core theme throughout the thesis; The work with marine spatial planning is interlinked with the other themes and that all of them permeate each other in the municipalities work with MSP. The mixed methods applied to answer the aim in the thesis are semi-structured informant interviews with planners and project leaders of a selection of municipalities and a survey sent to all Swedish coastal municipalities. The results show that cooperation and collaborations are an important part in the work with MSP for several municipalities. -

A Health Promoting Leisure Time for Young Teenage Girls

A health promoting leisure time for young teenage girls Results from a focusgroup study in Sweden Åsa Bringsén Phd, lecturer in Public Health Petra Andersson Frida Arthursson Kjell Lina Ejlertsson Young teenage girls and health Public Health Institute (2009) Young teenage girls and QoL Sweden Sport Confederation (2004) Popular leisure activities among children and adolescents 1 2 3 Sweden Sport Confederation (2004) Teenage girls and organized sports Sweden Sport Confederation (2004) Location and collaboration • Reference group – Scania Sports Federation – Municipalities and schools in Scania northeast • Höör • Kristianstad • Hörby • Perstorp • Östra Göinge • Hässleholm • Osby • Bromölla – Kristianstad University – Region Skåne Project • Action research aiming at increased opportunities for health promoting leisure time among young teenage girls in Scania northeast Research and development process Höör (15200) Kristianstad (79000) Hörby (14800) Perstorp (7000) Planning, anchoring and networking activities Focus group study Planning, anchoring and Planning, anchoring and 7 interviews with 38 networking activities networking activities girls from 2 schools Feedback and reflection in Focus group study Focus group study local reference group 7 interviews with 56 4 interviews with 24 girls from 3 schools girls from 2 schools Planning, anchoring and Implementation networking activities Feedback and reflection in Feedback and reflection in local reference group local reference group Focus group study 3 interviews with 18 Implementatio Implementatio -

Bitillsynmän I Skåne 2020

Bitillsynare i Skåne 2021 dnr: 605-1861-2021 Kommun Bitillsynsman Adress Ort Telefon E-mail Båstad Björn Berndtsson Fornåkersväg 14 269 73 Förslöv 070-344 33 47 [email protected] Båstad Jonas Berndtsson Kroken 205 269 73 Förslöv 070-656 76 38 [email protected] Ängelholm Christel Gustavsson Farhultsvägen 205 263 95 Farhult 070-592 76 38 [email protected] Ängelholm Fahrudin Cehajic Odalgatan 1 262 53 Ängelholm 070-496 31 62 [email protected] Åstorp Lars Åke Eriksson Ö.Fjärestadsväg 180 253 42 Vållåkra 070-433 35 82 [email protected] Klippan Kent Tofft Rögnaröd 4628 264 54 Ljungbyhed 070-813 00 26 [email protected] Klippan Karl-Henrik Jansson Bladgatan 14C 264 36 Klippan 072-734 87 32 [email protected] Perstorp Kent Tofft Rögnaröd 4628 264 54 Ljungbyhed 070-813 00 26 [email protected] Perstorp Karl-Henrik Jansson Bladgatan 14C 264 36 Klippan 072-734 87 32 [email protected] Örkelljunga Fahrudin Cehajic Odalgatan 1 262 53 Ängelholm 070-496 31 62 [email protected] Hässleholm Erling Andersson M P Nilssons väg 4 281 97 Ballingslöv 0451-313 86; 070-631 38 66 [email protected] Hässleholm Stig Hansson Snorresväg 8 281 43 Hässleholm 070-960 91 23 [email protected] Osby Tolfte Carlsson Smedjegatan 6 287 72 Traryd 070-244 05 95 Osby Roy Quarton Tosthult 1195 280 70 Lönsboda 076-039 00 71 [email protected] Östra Göinge Göran Håkansson Högsma 1039 289 72 Sibbhult 070-575 32 62 [email protected] Bromölla Anders Jansson Bygdegårdsvägen 27 297 72 Everöd 076-139 06 24 [email protected] Kristianstad -

Perstorp Chemicals

ANNUAL REPORT 19 9 7/ 98 PERSTORP’S DIVISIONS DIVISIONS STRENGTHS OPERATIONS 1997/98 OBJECTIVES Perstorp Chemicals is a leading global producer of • Leading market positions in important areas • Continued favorable earnings • Strengthen globalization efforts and position as a PERSTORP CHEMICALS specialized chemical products for industrial customers. • Efficient and modern process technology • Capacity expansion in all areas global leader The division includes the operations of the Specialty • Global production and sales • Joint venture concerning special chemicals in • Increase rate of growth Chemicals, Chemitec and Construction Chemicals • Close cooperation with key customers India • Strengthen focus on special chemical products business units. • Production start for Boltorn™ dendritic polymers with high customer value by increasing innova- For many years, the division has had the highest level • Structural transaction in phenolic resins and tion of profitability within the Group and maintained divestments within Chemitec • Increase efficiency and productivity strong positions in the global market. The development • Major agreement with DuPont regarding formalin • Play an active role in the structural transformation of new products and geographic expansion are of the chemicals industry by acquiring, or cooper- important components in the ating with, companies based on similar technolo- strategy established for polyols, formalin technology, gies or that focus on the same type of customers thermosets, resins, composites and construction chemicals. Perstorp Flooring is a world-leading producer of lami- • Pergo® – the laminate flooring market’s strongest • Earnings reduced by lower growth rate, combined • Global leadership for laminate flooring PERSTORP FLOORING nate flooring for residences and institutional environ- brand with higher costs • Extend the product range by strengthening Pergo® ments. -

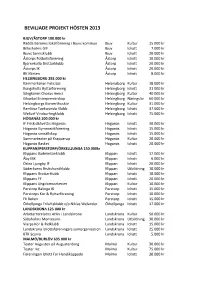

Beviljade Projekt Hösten 2013

BEVILJADE PROJEKT HÖSTEN 2013 BJUV/ÅSTORP 100.000 kr Rädda Barnens lokalförening i Bjuvs kommun Bjuv Kultur 15.000 kr Billesholms GIF Bjuv Idrott 7.000 kr Bjuvs tennisklubb Bjuv Idrott 20.000 kr Åstorps Fotbollsförening Åstorp Idrott 10.000 kr Björnekulla Brottarklubb Åstorp Idrott 20.000 kr Åstorps IK Åstorp Idrott 20.000 kr BK Klinten Åstorp Idrott 8.000 kr HELSINGBORG 292.000 kr Kammarkören Felicitas Helsingborg Kultur 18.000 kr Kungshults Ryttarförening Helsingborg Idrott 31 000 kr Sångkören Chorus Amici Helsingborg Kultur 40 000 kr Glowbal Entreprenörskap Helsingborg Näringsliv 60 000 kr Helsingborgs Konserthuskör Helsingborg Kultur 31.000 kr Ramlösa Taekwondo Klubb Helsingborg Idrott 37.000 kr WeSurf Vindsurfingklubb Helsingborg Idrott 75.000 kr HÖGANÄS 100.000 kr IF Friskis&Svettis Höganäs Höganäs Idrott 30.000 kr Höganäs Gymnastikförening Höganäs Idrott 15.000 kr Höganäs simsällskap Höganäs Idrott 15.000 kr Sommarteater på Krapperup Höganäs Kultur 20.000 kr Höganäs Basket Höganäs Idrott 20.000 kr KLIPPAN/PERSTORP/ÖRKELLJUNGA 150.000kr Klippans Badmintonklubb Klippan Idrott 17.000 kr Åby IBK Klippan Idrott 6.000 kr Östra Ljungby IF Klippan Idrott 20.000 kr Söderåsens Brukshundklubb Klippan Utbildning 10.000 kr Klippans Brottarklubb Klippan Idrott 10.000 kr Klippans FF Klippan Idrott 20.000 kr Klippans Ungdomsorkester Klippan Kultur 10.000 kr Perstorp Bälinge IK Perstorp Idrott 15.000 kr Perstorps Kör & Ryttarförening Perstorp Idrott 10.000 kr Fk Boken Perstorp Idrott 15.000 kr Örkelljunga Friluftsklubb c/o Niklas Welander Örkelljunga