Transit Systems Overview

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Station Area Plan

Brooklyn Park Station Area Plan Brooklyn Park, Minnesota | July 2016 ELECTED OFFICIALS HENNEPIN COUNTY, DEPT OF COMMU- COMMUNITY WORKING GROUP Jennifer Schultz Brooklyn Park Station NITY WORKS AND DEPT OF PLANNING Commissioner Mike Opat Sherry Anderson Albert Smith Darlene Walser Hennepin County, District 1 Cherno Bah Area Plan Bottineau Community Works Ben Stein Mayor Jeffrey Lunde Program Manager Susan Blood * Robert Timperley City of Brooklyn Park Denise Butler * Robin Turner Andrew Gillett Kimberly Carpenter Tonja West-Hafner Peter Crema Principal Planning Analyst Reva Chamblis Council Member, City of Brooklyn Jim White PREPARED FOR Denise Engen Park, East District Daniel Couture Jane Wilson City of Brooklyn Park Principal Planning Analyst Rebecca Dougherty Carol Woehrer Hennepin County Rich Gates Council Member, City of Brooklyn Brent Rusco Janet Durbin Yaomee Xiong * Park, Central District Administrative Engineer Michael Fowler FUNDED BY Kathy Fraser HEALTH EQUITY & ENGAGEMENT Hennepin County John Jordan Karen Nikolai COHORT Teferi Fufa Council Member, City of Brooklyn Administrative Manager African American Leadership Park, West District Jeffrey Gagnon Forum (AALF) CONSULTANT TEAM Joseph Gladke Larry Glover African Career & Education Urban Design Associates Terry Parks Assistant Department Director Resources (ACER) Nelson\Nygaard Consulting Associates Council Member, City of Brooklyn Edmond Gray SB Friedman Development Advisors Park, East District Dan Hall Alliance for Metropolitan Stability CITY OF BROOKLYN PARK (AMS) ZAN Associates Heidi Heinzel Mike Trepanier Kim Berggren Asamblea de Derechos Civiles Westly Henrickson Council Member, City of Brooklyn Director of Community CAPI USA Park, Central District Development Shaquonica Johnson LAO Assistance Center of Michael Kisch Bob Mata Cindy Sherman Minnesota (LAC) Council Member, City of Brooklyn Planning Director Tim Korby Minnesota African Women’s Park, West District Chris Kurle Association (MAWA) Todd A. -

Bass Lake Road Station Area Plan

Bass Lake Road Station Area Plan Crystal, Minnesota | July 2016 ELECTED OFFICIALS Brent Rusco African Career & Education Jason Zimmerman Michael Mechtenberg Bass Lake Road Station Commissioner Mike Opat Administrative Engineer Resources (ACER) City of Golden Valley Metro Transit Hennepin County, District 1 Karen Nikolai Alliance for Metropolitan Stability Rebecca Farrar Shelley Miller Area Plan (AMS) Mayor Jim Adams Administrative Manager City of Minneapolis Metro Transit City of Crystal Joseph Gladke La Asamblea de Derechos Civiles Beth Grosen Alicia Vap Laura Libby Assistant Department Director CAPI USA City of Minneapolis Metro Transit Council Member, City of Crystal, PREPARED FOR LAO Assistance Center of Ward 1 and 2 Don Pflaum Mike Larson City of Crystal CITY OF CRYSTAL Minnesota (LAC) City of Minneapolis Metropolitan Council Hennepin County Elizabeth Dahl John Sutter Minnesota African Women’s Council Member, City of Crystal, Community Development Director Association (MAWA) Jim Voll Eric Wojchik Ward 1 City of Minneapolis Metropolitan Council FUNDED BY Minnesota Center for Neighborhood Dan Olson Organization (MCNO) Hennepin County Jeff Kolb Rick Pearson Jan Youngquist City Planner Nexus Community Partners Council Member, City of Crystal, City of Robbinsdale Metropolitan Council Northwest Human Services Council CONSULTANT TEAM Ward 2 COMMUNITY WORKING GROUP (NHHSC) Chad Ellos Adam Arvidson Urban Design Associates Olga Parsons Gene Bakke Hennepin County Minneapolis Park and Recreation Nelson\Nygaard Consulting Associates Council Member, -

Community Open House METRO Blue Line Extension (Bottineau LRT) Phase 1: Station Area Planning Welcome! November 12Th, 2014 5:30-8:00 P.M

COMMUNITY OPEN HOUSE METRO Blue Line extension (Bottineau LRT) Phase 1: Station Area Planning Welcome! November 12th, 2014 5:30-8:00 p.m. Agenda: 5:30 - Refreshments and Visit » Information Displays » Penn Avenue Community Works Open House Map: » METRO Blue Line Extension GOLDEN VAN WHITE VALLEY BLVD. » C-Line Arterial Bus Rapid Transit ROAD STATION DISCUSSION STATION TABLES 6:00 - Welcome FOOD STATION FOOD STATION 6:10 - Open House Introduction PLYMOUTH PENN AVE. AVE. STATION STATION 6:20 - Station Area Exercises PENN AVE. COMMUNITY WORKS 8:00 - Meeting Closes WHAT IS STATION AREA PLANNING? METRO BLUE LINE C-LINE ARTERIAL Rest Rooms BUS RAPID TRANSIT WELCOME EXTENSION Enter Front Here Door Reception Desk Station Area Planning What is a station area plan? » Plan for the area that surrounds a proposed transit station Proposed » ½ mile radius and/or 10 min. walk Station » Community-based » Focus is on maintaining great neighborhoods and high quality transit-oriented development. » Creates a plan that supports Light Rail Transit by looking at: » Land uses and types/character of buildings » Access/circulation (bike, walk, car, bus) » Improvements to public spaces, including streets/trails Plans will make recommendations on: » Future land use alternatives » Housing (preservation and new) » Potential markets for new development » Circulation and access improvements » Strategies for health equity » Implementation measures such as zoning changes, comprehensive plan amendments and other ordinances or policies Implemented by the cities, county and -

Minneapolis Transportation Action Plan (Engagement Phase 3)

Minneapolis Transportation Action Plan (Engagement Phase 3) Email Comment Topic Comment # The recommendations in this submission expand on this principle and support the overall Transportation Action Plan goals of designing transportation to achieve the aims of Minneapolis 2040, address climate change, reduce traffic fatalities and injuries, and improve racial and economic equity. In line with these goals, our most significant recommendations for the Prospect Park area are to • Invest in the protected bike network: extending the Greenway over the River, and building the Prospect Park Trail along railroad right-of- way • Transform University Avenue and Washington Avenues • Complete the Grand Rounds and use the Granary corridor to redirect truck traffic Priorities for transportation improvements in Prospect Park 1. Improve pedestrian infrastructure throughout the community including safe crossings of University Avenue SE (Bedford, Malcolm, 29th and 27th), Franklin Avenue SE (Bedford, Seymour) and 27th Avenue SE (Essex, Luxton Park to Huron pedestrian overpass). We encourage the city to narrow residential intersections, particularly in Bicycling, the Tower Hill sub-neighborhood where streets do not meet at right Walking, 1 angles, and crossing distances are significantly longer than needed. Additional Planters and plastic delineators could be used to achieve this ahead of Comments reconstruction. Maintenance and improvements should focus on public safety, adequate lighting and landscape upkeep. Throughout the neighborhood residents have cited safety (particularly at night), sidewalk disrepair, narrowness, snow and ice issues, and have expressed support for full ADA compliance. 2. Complete the Minneapolis Grand Rounds and the Granary Corridor (see Map 2) to enhance community access to city and regional parks and trails as well as to adjoining neighborhoods. -

Equity Commitments Matrix Transit Improvements Issue Specific Commitment Requests Responsible Entity City of Minneapolis Connect Penn Ave

Equity Commitments Matrix Transit Improvements Issue Specific Commitment Requests Responsible Entity City of Minneapolis Connect Penn Ave. N. BRT line to the SW Penn Ave. Station stop . “commits to engage in discussions that enhance multi-jurisdictional and private resources that will expedite development along transitways and provide economic opportunity for low-income communities and communities Maximize access and connectivity of SWLRT of color” (pg. 2) Plan and develop multi-modal transit commit to a transit service plan that will analyze the existing bus Hennepin County connections to the Penn Ave N. and Van systems and reconfigure to support the transit rider needs . established the Penn Av. Community Works project in 2012 to conduct a White Southwest Light Rail stations. comprehensive planning and design study, with a goal to “stimulate economic development, enhance mobility and create jobs in North Mpls.” (pg. 1) Coordinate future transit and land-use Coordinated transit service planning; coordinated land use planning . A core feature of this effort is the “Conditions for Success” community planning. the city, county and Met Council commit to an inclusive public designed framework for engagement. Provided funding for W. Broadway Av. planning process for SWLRT, Penn Avenue BRT, Bottineau LRT, Study to evaluate connections to BRT & LRT & mkt. potential for TOD. Partner & contract with community groups Emerson/Fremont Avenue BRT and West Broadway Avenue corridors . Throughout the corridor planning and development process, commits “to to ensure strong public engagement that reaching out to local community groups and neighborhood leaders to have 1 leads to equitable outcomes and Partnership: partner with local, on-the-ground community-based authentic engagement that supports locally-based organizations and ensures community benefits. -

Robbinsdale 2040

Figure 1: Ballfield at Lee Park Robbinsdale, Minnesota Robbinsdale 2040 Comprehensive Plan Robbinsdale 2040 Table of Contents Introduction 2 Land Use 3 Housing 25 Transportation 44 Economic Competitiveness 73 Resilience 82 Parks and Trails 89 Public Facilities – Water, Sewer and Solid Waste 94 Implementation 106 Appendix A: Water Supply Plan Appendix B: Bicycle Pedestrian Plan Appendix C: Light Rail Station Area Report Appendix D: 2020-2029 Capital Improvement Plan Appendix E: Local Surface Water Management Plan Figure 2: Victory Memorial Flagpole 1 Robbinsdale 2040 Introduction Historical Overview Robbinsdale is located immediately north and west of Minneapolis, about 15 minutes from downtown Minneapolis. To the east, Robbinsdale borders North Minneapolis, to the northeast the City of Brooklyn Center, and to the west and southwest the cities of Crystal and Golden Valley. Robbinsdale officially came into existence in 1893 when dissatisfaction among local residents led to the secession of a portion of then Crystal Village to create the Village of Robbinsdale. Robbinsdale remained more rural than urban through the end of the nineteenth century. A small, active commercial nucleus, surrounded by residential areas, developed in the area located along West Broadway in the vicinity of 42nd Avenue. Although large areas of the community had been platted prior to the turn of the century, major growth did not occur until after World War I, when the first significant suburban migration began. This period of growth resulted in the development of large portions of the community situated west and south of County Road 81. A second period of community growth occurred as a result of the suburban boom following World War II. -

November 15, 2017 the Honorable Paul

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp November 15, 2017 The Honorable Paul Torkelson, Chair The Honorable Scott Newman, Chair House Transportation Finance Committee Senate Transportation Finance & Policy Committee 381 State Office Building 3105 Minnesota Senate Building Saint Paul, MN 55155 Saint Paul, MN 55155 The Honorable Linda Runbeck, Chair The Honorable Scott Dibble House Transportation & Regional Governance Policy Ranking Minority Member Committee Senate Transportation Finance & Policy Committee 417 State Office Building 2213 Minnesota Senate Building Saint Paul, MN 55155 Saint Paul, MN 55155 The Honorable Frank Hornstein, DFL Lead The Honorable Connie Bernardy, DFL Lead House Transportation Policy & Finance Committee House Transportation & Regional Governance Policy 243 State Office Building Committee Saint Paul, MN 55155 253 State Office Building Saint Paul, MN 55155 RE: 2017 Guideway Status report Dear Legislators: The Minnesota Department of Transportation, in collaboration with the Metropolitan Council, is pleased to provide the 2017 Guideway Status report as required under 2016 Minnesota Statutes 174.93, subdivision 2. This report updates information for eight guideway corridors currently in operation, construction or design, and thirteen more that are in planning or analysis phase, or that were at the time of the last report in 2015. The capacity analysis looks at regional guideway funding needs and resources related to capital, operations and capital maintenance for the next ten years. If you have specific questions about this report or want additional information, please contact MnDOT’s Brian Isaacson at [email protected] or at 651 234-7783; or, you can contact Met Council’s Cole Hiniker at [email protected] or at 651 602-1748. -

Transit-Study-Final-Report FINAL-1-1.Pdf

Citizens League Report Getting From Here to There: Funding Transit in the Region Prepared by Citizens League Transit Study Committee, 2016-2017 Approved by Citizens League Board of Directors February 2, 2017 Citizens League 400 N Robert Street #1820 St. Paul, MN 55101 1 The Citizens League dedicates this report to the memory of Verne C. Johnson Executive Director of the Citizens League from 1958-1967. This report was made possible by the generous support from the Verne C. Johnson Family Foundation All Transit Study Committee members contributed to the report, but the Citizens League would like to extend a special thank you to the following members for their additional contributions to this report: Peter Bell James Erkel Peter McLaughlin William Schreiber Patty Thorsen Nancy Tyra-Lukens 2 TABLE OF CONTENTS INTRODUCTION ....................................................................................................................................... 4 EXECUTIVE SUMMARY ........................................................................................................................ 5 WORK OF THE CITIZENS LEAGUE TRANSIT STUDY COMMITTEE ........................................ 9 TRANSIT STUDY COMMITTEE AND PROCEDURES ...................................................................................... 9 MEMBERSHIP OF THE TRANSIT STUDY COMMITTEE .............................................................................. 10 BACKGROUND AND CONTEXT: TRANSIT IN TRANSITION IN MINNESOTA ...................... 11 SIGNIFICANT TRANSIT -

Development Guidelines August 2018

Robbinsdale LRT Station CDI Development Guidelines August 2018 Overview The City of Robbinsdale may have the coolest opportunity site along the 13 mile stretch of the Bottineau LRT corridor / Blue Line extension. Located a block from the main street of Robbinsdale’s downtown (West Broadway), the Robbinsdale LRT Station will serve as a central gateway to welcome people to the city. Even though the station will accommodate 440 parking spaces for transit users, it also offers the potential for a unique public space and adjacent uses that provide a fresh version of suburban multi-modal transit hub. Robbinsdale cherishes its small town community feel. While at the same time, is curious about contemporary uses informed by a shared economy. At its core, the Robbinsdale LRT station area has the potential to honor the city’s past, while leaping into the 21st century. The community is actively engaged in imagining its future. Which makes this transit and investment opportunity all the more exciting. Robbinsdale is a great community for people at every life stage. It’s a wonderful place for neighborhood scale businesses to locate. Parks and trails connect with natural amenities, and the North Memorial Health (a major employer) is close by. The vast majority (93%) of the housing stock is currently affordable for a family of four earning $71,900 or less, and is not income restricted through public resources. Considerable planning has already occurred for the Bottineau LRT corridor, including: Robbinsdale Station Area Planning (Oct 2015) Robbinsdale -

Guideway Status November 2013

2013 Legislative Report Guideway Status November 2013 Prepared by The Minnesota Department of Transportation 395 John Ireland Boulevard Saint Paul, Minnesota 55155-1899 Phone: 651-366-3000 Toll-Free: 1-800-657-3774 TTY, Voice or ASCII: 1-800-627-3529 In collaboration with the Metropolitan Council 390 Robert St. North St. Paul, MN 55101-1805 Phone: 651-602-1000 To request this document in an alternative format Please call 651-366-4718 or 1-800-657-3774 (Greater Minnesota). You may also send an email to [email protected]. Cover Photos: Northstar commuter rail train Red Line (Cedar BRT) vehicle on at Target Field opening day Source: Metro Council Source: Metro Council Green Line (Central Corridor LRT) Blue Line (Hiawatha LRT) in vehicle on tracks for testing operation Source: Streets MN Source: Metro Council 2 Guideway Status Report November 2013 Contents Contents .............................................................................................................................................................. 3 Legislative Request............................................................................................................................................. 5 Statutory Requirement ......................................................................................................................... 5 Cost of Report ...................................................................................................................................... 6 Introduction ....................................................................................................................................................... -

Light Rail Update

Big Lake Elk River Ramsey Anoka Coon Rapids Oak Grove Parkway OSSEO METRO Blue Line (LRT): Open 93rd Ave M ISSI METRO Red Line (BRT): Open SS BROOKLYN IPPI METRO Green Line (LRT): Open PARK RI (BRT): Est. 2019 V METRO Orange Line E 85th Ave R METRO Green Line extension (LRT): 2018 METRO Blue Line extension (LRT): TBD METRO Red Line extension (BRT): TBD Brooklyn Blvd Station under consideration Station Fridley BROOKLYN Metro Transit Northstar Line (commuter rail) CENTER updated 11/11/14 63rd Ave CRYSTAL Bass Lake Rd ROBBINSDALE Robbinsdale e v in A p e nn Golden e H Valley Rd t/ e e c a v it i z GOLDEN h tr la st e s a g n A d ll t P a k VALLEY n n Wlv a ill r e a e Di n E k k a P V s w n n Plymouth Ave u t M men o a a m V t P B o le n t u c h l r t B t B i re o e wn s s pe a ic v o e a tad s o E S ro te W N G D W P a e g v Target Field st e d A y t W w mon e e e k e e S Royalston y v v v t v ic - a n P R t r R e A o n A / MINNEAPOLIS a w A g A n t ia S t r l t S Van White d ie in li g r e to r e e v ll in o t i e d r m x t e S s p b C i ai ne a e ic al e a o rs F S H L V D W C R Penn e v n Ri li k t n e 21st St ra v h S Lake St F A t 10 l a t/ tr n e S en West Lake k w C Union Depot a to L id t M Beltline th S 8 3 t ST. -

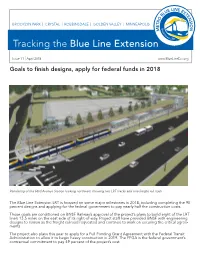

Tracking the Blue Line Extension Issue 11

BROOKLYN PARK | CRYSTAL | ROBBINSDALE | GOLDEN VALLEY | MINNEAPOLIS Tracking the Blue Line Extension Issue 11 | April 2018 www.BlueLineExt.org Goals to finish designs, apply for federal funds in 2018 Rendering of the 63rd Avenue Station looking northwest showing two LRT tracks and one freight rail track The Blue Line Extension LRT is focused on some major milestones in 2018, including completing the 90 percent designs and applying for the federal government to pay nearly half the construction costs. Those goals are conditioned on BNSF Railway’s approval of the project’s plans to build eight of the LRT line’s 13.5 miles on the east side of its right-of-way. Project staff have provided BNSF with engineering designs to review as the freight railroad requested and continue to work on securing the critical agree- ments. The project also plans this year to apply for a Full Funding Grant Agreement with the Federal Transit Administration to allow it to begin heavy construction in 2019. The FFGA is the federal government’s contractual commitment to pay 49 percent of the project’s cost. for news updates, project Visit us online at 2 www.BlueLineExt.org information and events Design for Hwy. 55 aims to slow traffic, improve safety Rendering of the view looking southeast from Van White Boulevard Station in Minneapolis Lowering the speed limit and adding curves, an additional signalized intersection and three mid-block crosswalks are planned for Highway 55 in Minneapolis to slow cars and trucks when light rail tracks are built in the median. Comments from residents of the Harrison, Heritage Park, Near North, Sumner-Glenwood and Willard Hay neighborhoods led to these design changes for improving safety.