HYOFFWIND – Power to Gas

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Review of Annual Reports 2010 of Euronext Brussels Listed Companies 2 Grant Thornton Corporate Governance Review

Corporate Governance Review Review of Annual Reports 2010 of Euronext Brussels listed companies 2 Grant Thornton Corporate Governance Review Contents Contents 3 Foreword 5 Executive summary 7 PART I - Legally binding provisions 11 1. Corporate Governance Statement 12 2. Remuneration committee 17 3. Remuneration report 19 4. Audit committee – Legal requirements 22 PART II - Results corporate governance code 25 5. Board of directors 26 6. Independence 28 7. Nomination committee 30 8. Audit committee – Code requirements 32 Appendix A - Survey methodology 37 Appendix B - List of companies 39 3 4 Grant Thornton Corporate Governance Review Foreword We are pleased to present the Another key factor in the corporate governance debate is the interest of the European Commission second annual publication in Grant and the impact this will have on corporate governance Thornton’s series of reviews of the legislation. The European Commission released a corporate governance disclosures consultation paper on an EU corporate governance of Belgian companies quoted on framework and is seeking submissions from interested parties. We may, therefore, see a single EU-wide the Euronext stock exchange. The corporate governance framework in the not so distant review examines the extent to which future. companies comply with regulatory Corporate governance is fundamentally about requirements. ensuring that key stakeholders, including the public, can have confidence in how business is conducted and This year’s report arrives at a time of turmoil for results are disclosed by public interest entities such Belgian listed companies. While the Belgian banking as listed companies, financial institutions and public sector was struggling for survival and stock markets sector organisations. -

Elia Group Full Year 2020 Results

Elia Group Full Year 2020 Results Wednesday, 3rd March 2021 Transcript produced by Global Lingo London – 020 7870 7100 www.global-lingo.com Elia Group Full Year 2020 Results Wednesday, 3rd March 2021 Elia Group Full Year 2020 Results Marleen Vanhecke: Good morning, ladies and gentlemen. Thank you for participating in our livestreamed event, which is being broadcast from a corona-proof studio in Brussels. It would have been nicer to meet you in person, of course, but the lockdown measures have forced us to present our full year results in another format. The setup is different, but we will keep you just as informed as we normally would. What hasn't changed are today's speakers. Elia Group is represented by Catherine Vandenborre, CFO, and by Chris Peeters, CEO, both in good health, as you can see. Today's programme is as follows. First, we will give you an overview of the headlines from 2020. We will talk with Chris Peeters about the acceleration of the energy transition and how Elia Group is managing it. Catherine Vandenborre will then present the financial results. And finally, we will present our conclusion and an outlook on the years to come. Before we start, I would like to present a disclaimer for today's presentation as mentioned on the title page. You must read the disclaimer before we can continue. I suppose you have all done it by now. Am I right? So let's immediately go to the first question for Chris. Marleen Vanhecke: Chris, looking back at 2020, it's impossible to avoid the corona crisis, of course. -

Colruyt Group Increases Stake in Holding That Includes Fashion Retailer ZEB

PRESS RELEASE - Halle (Belgium) – 3 September 2020 (17h45 CET) Colruyt Group increases stake in holding that includes fashion retailer ZEB On 3 September 2020 Colruyt Group increased its stake in Fraluc Group from 68% to over 96%. Fraluc is the holding that includes the fashion retail chains ZEB, PointCarré, The Fashion Store and ZEB For Stars. The management teams of the respective companies remain unchanged. On 21 June 2014 Colruyt Group acquired a 50% stake in the Belgian fashion retailer ZEB through the company Fraluc NV. As part of the agreement, the management agreed to grant put and call options, enabling Colruyt Group to gain control over ZEB via Fraluc NV. In the meantime, ZEB has continued to develop within the Fraluc Group, which also comprises PointCarré, The Fashion Store and ZEB For Stars. At the end of the financial year 2019/20, Colruyt Group held 68% of the Fraluc Group shares. On 3 September 2020, Colruyt Group and Fraluc Group's management entered into an agreement to increase Colruyt Group's stake in Fraluc Group to over 96%. The management remains on board in its current composition. The parties agreed not to disclose any details on the terms of the transaction. The transaction is subject to approval by the Belgian Competition Authority (BCA), which is expected to be obtained in the coming weeks. Following approval by the BCA, the stake held in Fraluc Group will be fully consolidated as a subsidiary of Colruyt Group and no longer be accounted for as a joint venture using the equity method. Contacts For questions on this press release or for further information, please contact us as follows: Journalists: Silja Decock (Press Officer) Tel. -

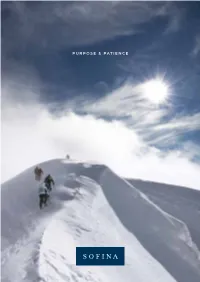

Purpose & Patience

PURPOSE & PATIENCE We aspire to be the preferred partner of entrepreneurs and families who lead growing companies by backing them with patient capital and supportive advice — Q1 2020 Edition — OUR MISSION Our goal at Sofina is to create economic value with a human approach We believe that the entrepreneurial spirit that characterises many family businesses and growth companies is a source of progress. By supporting these entrepreneurs and innovators, we intend to contribute to global growth, development and innovation. We believe entrepreneurs become successful by being competitive in a globalised market Our mission is to provide patient capital, expertise and advice to growing companies led by entrepreneurs and families. We aspire to be their preferred partner, and have a long-term horizon that few other investors can match. Our heritage and culture are what make us unique We put human relationships at the heart of what we do. All our investments are stories of shared values, friendships and ambitious projects with talented entrepreneurs and their management teams. By continuously working in this way, we aspire to become the preferred investment partner of those sharing our beliefs and vision. 2 SOFINA - PURPOSE & PATIENCE OUR MISSION 3 KEY FIGURES Highlights EUR 7.63 BN GLOBAL SHAREHOLDERS’ EQUITY REACH A FAMILY RUN 3 US EUROPE ASIA AND CONTROLLED COMPLEMENTARY Change over the last 20 INVESTMENT COMPANY INVESTMENT years (2) STYLES 8.00 7.00 6.00 5.00 FOUR FOCUS 4.00 SECTORS Long-term minority 3.00 investments 2.00 1.00 43% OF SHAREHOLDERS’ EQUITY (1) Offices in Brussels, 0 Luxembourg and Singapore Consumer and Retail 1999 2019 Sofina Private Funds – Investments in venture and growth capital funds Digital Transformation 31% OF SHAREHOLDERS’ EQUITY (1) Roots going back 26 Sofina Growth – Investments in Education investment fast-growing businesses professionals 120+ YEARS across our 20% OF SHAREHOLDERS’ EQUITY (1) 3 offices Healthcare (1) Considering the portfolio in transparency. -

Ets Fr. COLRUYT SA Limited Liability Company Edingensesteenweg 196 – 1500 Halle Company Number: 0400.378.485

PRESS RELEASE - Halle (Belgium), 18/12/2015 - Regulated information – Declaration of transparency Ets Fr. COLRUYT SA Limited Liability Company Edingensesteenweg 196 – 1500 Halle Company number: 0400.378.485 Structure of the shareholdership of the Ets Fr. Colruyt S.A. according to the latest transparency notifications of 17/12/2015 In the framework of the law of 2 May 2007 and the Royal decree of 14 February 2008 (publication of the important participations in the companies listed on the stock exchange) we received an updated notification of the participation of the Colruyt family, Sofina Group and Colruyt Group on 17/12/2015. On 13 July 2015 D.I.M. NV, H.I.M. NV, H.I.M. Drie NV, D.H.A.M. NV and KORYS NV were merged. As a result, all Colruyt shares held by these companies are now owned by KORYS NV and KORYS NV has crossed the 45% threshold . 7.500.000 treasury shares were cancelled on 17/12/2015. Hence, the 'Colruyt treasury shares purchased' rate was updated and the number of treasury shares purchased by Colruyt Group has dropped below the 5% threshold. The new denominator of 149.609.386 shares takes into account the cancellation of 7.500.000 treasury shares and the capital increase reserved for employees, for which 472.883 new shares were issued on 17/12/2015. The company has no knowledge of other agreements between shareholders. The legal thresholds per 5% portion apply.. I. Colruyt family and relatives Number % 1. Stichting Administratiekantoor Cozin 0 0,00 2. Colruyt family 9.127.879 6,10 3. -

Etn. Fr. COLRUYT NV Publication of a Transparency

PRESS RELEASE – Halle (Belgium), 18/02/2019, 17h45 CET – Regulated information - Transparency notification Etn. Fr. COLRUYT NV Limited liability company Edingensesteenweg 196 – 1500 Halle Enterprise number: 0400.378.485 Publication of a transparency notification (Article 14, first paragraph, of the Law of 2 May 2007 on disclosure of major holdings) Summary of the notification Pursuant to article 14 of the Law of 2 May 2007 on disclosure of major holdings, the Colruyt family and relatives, Colruyt Group and Sofina Group have submitted a notification to the FSMA. This transparency notification dated 15 February 2019 reports the completion of a sale of shares between reference shareholders acting in concert. By virtue of this sale of shares Sofina NV has crossed the threshold of 5% downwards. The shareholders acting in concert Colruyt family and relatives, Colruyt Group and Sofina Group hold a total of 90.955.630 Colruyt shares as per 15 February 2019 and thus jointly represent 63,36% of the total number of shares issued by the company (143.552.090). The company has no knowledge of other agreements between shareholders. The statutory thresholds per bracket of 5% apply. Content of the notification The notification dated 15/02/2019 contains the following information: Reason for the notification: downward crossing of the threshold by persons of the shareholders acting in concert Colruyt family and relatives, Colruyt Group and Sofina Group Notification by: persons acting in concert Person(s) subject to the notification requirement: Stichting Administratiekantoor Cozin, Claude Debussylaan 24, 1085 MD Amsterdam Korys NV, Villalaan 96 – 1500 Halle Korys Business Services I NV, Villalaan 96 – 1500 Halle Korys Business Services II NV, Villalaan 96 – 1500 Halle Korys Business Services III NV, Villalaan 96 – 1500 Halle Korys Investments NV, Villalaan 96 – 1500 Halle Impact Capital NV, Gemeentehuisstraat 6, 3078 Everberg Stiftung Pro Creatura, Oberer Flooz 2579, CH 9620 Lichtensteig Etn. -

85 % Des Entreprises Du Bel20 Vont Verser Des Dividendes

85 % DES ENTREPRISES DU BEL20 VONT VERSER DES DIVIDENDES « LES MARGES SONT LÀ POUR AUGMENTER LES SALAIRES » L’écrasante majorité des entreprises du Bel20 s’apprête à distribuer de juteux dividendes à leurs actionnaires en 2021. Au total, il s’agit d’un montant d’un peu plus de 5 milliards d’euros, selon les chiffres communiqués par les entreprises elles- mêmes. Le service d’étude du PTB a calculé qu’une augmentation salariale de 5 % dans ces entreprises coûterait 1,2 milliard d’euros (voir tableau 1). Soit seulement 25 % des dividendes annoncés. « Cela confirme que dans toute une série de grandes entreprises, il y a de la marge pour augmenter davantage les salaires, constate Raoul Hedebouw, porte-parole du PTB. C’est pourquoi nous exigeons que la loi de 1996 soit modifiée que la norme salariale soit rendue indicative, afin que les travailleurs aient la liberté de négocier de vraies augmentations. » 17 ENTREPRISES DU BEL20 DISTRIBUENT DE GÉNÉREUX DIVIDENDES Selon leurs propres rapports et annonces, la grande majorité des entreprises du Bel20 réalisera des bénéfices et distribuera des dividendes encore cette année. Sur les 19 entreprises qui ont déjà communiqué à ce sujet, 17 annoncent qu’elles verseront des dividendes allant de 34 millions à 1 milliard d’euros. En d’autres mots, au moins 85 % des entreprises du Bel20 verseront des dividendes. Dividende (par Dividende action) proposé (montant total) Nombre d'actions Société du Bel 20 sur base du proposé sur base bénéfice 2020 du bénéfice 2020 AB InBev 0,50 € 1.998.000.000 999.000.000 € Ackermans & van Haaren 2,53 € 33.500.000 84.755.000 € Ageas 2,65 € 198.370.000 525.680.500 € Aperam 1,75 € 83.700.000 146.475.000 € Argen-X 0,00 € 42.760.000 0 € Barco 0,378 € 88.270.000 33.366.060 € Cofinimmo 6,00 € 25.850.000 155.100.000 € Colruyt Group 1,35 € 138.430.000 186.880.500 € Galapagos 0,00 € 64.670.000 0 € GBL 3,03 € 161.360.000 488.920.800 € ING 0,12 € 3.896.730.000 467.607.600 € KBC 0,44 € 416.390.000 183.211.600 € Ontex n.d. -

Rapport Annuel • 2011-2012 • Colruyt Group

Rapport annuel • 2011-2012 • Colruyt Group Créer ensemble une valeur ajoutée durable fondée sur nos valeurs et notre savoir-faire dans la distribution WorldReginfo - 62bc7365-1652-46ba-a580-a3ed55c9c1b3 Risques inhérents aux prévisions Les déclarations formulées par Colruyt Group dans le présent communiqué de presse, de même que les références à ce communiqué dans toutes les autres déclara- tions écrites ou orales du groupe, portant sur les perspectives d’avenir en matière d’activités, sur les événements et les développements stratégiques de Colruyt Group, sont des prévisions et comportent à ce titre des risques et des incertitudes. Les informations communiquées reposent sur les données disponibles à ce moment ; ces informations sont susceptibles de différer du résultat final. Les facteurs pouvant induire une distorsion entre les prévisions et la réalité sont les suivants : changement de contexte microéconomique ou macroéconomique, circonstances de marché variables, climat concurrentiel changeant, décisions défavorables concernant la con- struction et/ou l’agrandissement de nouveaux magasins ou de magasins existants, problèmes d’approvisionnement avec les fournisseurs, sans oublier tous les autres facteurs pouvant avoir un impact sur le résultat du groupe. Colruyt Group se décharge de toute obligation quant aux communications futures susceptibles d’avoir des répercussions sur le résultat du groupe ou d’entraîner un écart par rapport aux prévisions fournies dans le présent communiqué de presse ou dans toute autre com- munication du groupe, qu’elle soit orale ou écrite. WorldReginfo - 62bc7365-1652-46ba-a580-a3ed55c9c1b3 Hal, 22 juin 2012 Société anonyme Ets. Fr. Colruyt Siège social : Wilgenveld Edingensesteenweg 196 B-1500 HAL RPM Bruxelles TVA : BE 400.378.485 Numéro d’entreprise : 0400.378.485 Tél. -

Latest Evolutions in the Field of Psychosocial Well-Being

Latest evolutions in the field of psychosocial well-being: practical cases of Ab Inbev, Colruyt, Moderator, Delhaize, Eurocontrol, Johnson & Johnson, NS-HSK, Port of Antwerp and Proximus Item Type Book Keywords Pulso Europe; Well-being--Psychological aspects; Well-being-- Social aspects; Employee assistance programs; Case studies; Work environment Publisher Pulso Download date 05/10/2021 17:20:12 Link to Item http://hdl.handle.net/10713/11206 Latest evolutions in the field of psychosocial well-being Practical cases of Ab Inbev, Colruyt, Moderator, Delhaize, Eurocontrol, Johnson & Johnson, NS-HSK, Port of Antwerp and Proximus Latest evolutions in the field of psychosocial well-being Practical cases of Ab Inbev, Colruyt, Moderator, Delhaize, Eurocontrol, Johnson & Johnson, NS-HSK, Port of Antwerp and Proximus Pulso Europe: 20 years of experience Reflecting on the history of Pulso Europe means more than just looking back on this last year since this organisation was founded. It is also a celebration of the more than twenty years that have led to the success of Pulso Europe today. This journey has started in the ‘90s with three separate Leuven-based companies: • ISW, spin-off of the Leuven University and pioneer in science-based prevention, assessment and treat- ment of stress complaints; • Limits, expert in moral and sexual harassment in the workplace; • Eupora, expert in co-creating Employee Assistance Programmes in close collaboration with their cus- tomer organisations. Two mergers onwards (first ISW and Limits, then ISW Limits and Eupora) we have taken our journey to an even higher level. We move forward together, and the new name ‘Pulso Europe’ already hints one of the di- rections. -

The Annual Report on the Most Valuable Belgian Brands July 2018 Foreword

Belgium 10 2018 The annual report on the most valuable Belgian brands July 2018 Foreword. What is the purpose of a strong brand: to attract customers, to build loyalty, to motivate staff? All true, but for a commercial brand at least, the first answer must always be ‘to make money’. Huge investments are made in the design, launch, and ongoing promotion of brands. Given their potential financial value, this makes sense. Unfortunately, most organisations fail to go beyond that, missing huge opportunities to effectively make use of what are often their most important assets. Monitoring of brand performance should be the next step, but is often sporadic. Where it does take place, it frequently lacks financial rigour and is heavily reliant on qualitative measures, poorly understood by non-marketers. David Haigh As a result, marketing teams struggle to communicate the value of their work and CEO, Brand Finance boards then underestimate the significance of their brands to the business. Sceptical finance teams, unconvinced by what they perceive as marketing mumbo jumbo, may fail to agree necessary investments. What marketing spend there is, can end up poorly directed as marketers are left to operate with insufficient financial guidance or accountability. The end result can be a slow but steady downward spiral of poor communication, wasted resources, and a negative impact on the bottom line. Brand Finance bridges the gap between marketing and finance. Our teams have experience across a wide range of disciplines from market research and visual identity to tax and accounting. We understand the importance of design, advertising, and marketing, but we also believe that the ultimate and overriding purpose of brands is to make money. -

Career Report Master in Innovation & Entrepreneurship

Career report Master in Innovation & Entrepreneurship About this career report You can find AMS alumni worldwide! In this report, you’ll see a list of the full-time master’s alumni of the Innovation & Entrepreneurship program from the past six years. Due to GDPR compliance, names cannot be mentioned, but we can share their year of graduation, their first employer and job title, and the country where they initially started to work. Please keep in mind this also means the professional information of these alumni refers to their first job, not necessarily to their current professional activity. Full-Time Master’s Alumni Antwerp Management School 2 Academic Function Company Country year 2014-2015 Finance and Administration manager JV NPD & EMP & EWWCE Rwanda 2014-2015 Research Consultant InSites Consulting Belgium 2014-2015 Business Consultant Atos Consulting Belgium 2014-2015 Unix - Linux - Storage - Backup - Middleware Specialist TEKsystems Belgium 2014-2015 UMC manager candidate program UNIQLO Belgium 2014-2015 Innovation Consultant/ Business Designer Board of Innovation Belgium 2014-2015 Clinical Trial Pharmacist and quality system coordinator SGS Belgium 2014-2015 Marketing and Customer Service Officer ORAC nv Belgium 2014-2015 Export Customer Service MSC Mediterranean Shipping Company 2014-2015 Co-founder RBLS Belgium 2014-2015 Business Transformational Intern Sutherland Global Services USA 2014-2015 Innovation Consultant Deloitte Digital Belgium 2014-2015 Digital Transformation Consultant / Head of Operations Sense Consulting / Kliker.co -

BEYOND CHOCOLATE Annual Report 2019 CONTENTS

BEYOND CHOCOLATE Annual Report 2019 CONTENTS Foreword by Beyond Chocolate Steering Committee chairmen Patrick Hautphenne (2018-2019) and Philippe de Selliers (2020) 4 Beyond Chocolate 2019 internal events and meetings 6 BEYOND CHOCOLATE Partnership for a more sustainable Belgian chocolate sector 8 1. Scope 9 1.1 Which chocolate is the partnership targeting? 9 1.2 Which farmers is the partnership targeting? 12 2. Goals and Commitments 13 2.1 What is sustainability? 13 2.2 What are the current issues? 14 2.3 What are the Beyond Chocolate commitments? 14 2.3.1 Certification and sustainability schemes 14 2.3.2 Towards a living income for farmers 15 2.3.3 Deforestation 17 2.4 How will activities be implemented? 19 2.5 Signatories 19 The Beyond Chocolate Governance Structure 20 1. IDH, The Sustainable Trade Initiative 22 2. The Belgian Directorate-general Development Cooperation and Humanitarian Aid 22 3. The Beyond Chocolate Steering Committee 23 3.1 Composition of the Steering Committee 23 3.1.1 The Chairman 23 3.1.2 The Secretary 24 3.1.3 Members 24 3.2 Decision making process and Transparency 24 3.3 Objectives achieved in 2019 25 4. The Beyond Chocolate Working Groups 25 4.1 Composition of the working groups 25 4.2 Objectives achieved in 2019 27 5. The development of the Beyond Chocolate AME Working group 28 5.1 The composition of the AME Working group 28 5.2 Objectives of the AME Working group 29 6. The Beyond Chocolate Advisory Groups 29 The Accountability, Monitoring and Evaluation (AME) Framework 30 1.