Uganda Clays Ltd FY2015 Published Accounts Snapshot

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Unbs Upgrades Fuel Calibration Rig

UNBS UPGRADES FUEL CALIBRATION RIG PLUS: • UNBS wins Best Web Interface Award • UNBS’ New State of the Art Lab • Full List of UNBS Certified Products UNBS - Standards House Bweyogerere Industrial Park, Plot 2 - 12, Kyaliwajala road, P.O Box 6329 Kampala, Uganda Tel: +256 417 333 250 +256 312 262 688/9 Fax: +256 414 286 123 Website: www.unbs.go.ug Emial: [email protected] Toll Free Hotline: 0800133133 PUBLISHER The Quality Chronicles is a Quarterly publication produced for the Uganda National Bureau of Standards by: EAST AFRICAN MEDIA CONSULT Serena Hotel International Conference Centre Suite 152, P.O.Box 71919, Kampala Telephone: 256-41-4341725/6 Facsimile:256-41-4341726 Mob: 0772 593939 E-mail: [email protected] Editorial www.eastafricanmediaconsult.co.ug Uganda National Bureau of Standards MANAGING EDITOR continues to register success as one of the Julius Edwin Mirembe 0772 593939 leading government agencies both in service Contents delivery and non-tax revenue collection. In its EDITOR annual year performance report for 2018/2019, Jovia Kaganda • EXECUTIVE DIRECTOR’S PREFACE 041-4341725/6 the Bureau undertook Product Certification and UNBS Registers Exponential Growth in SME Registration 4 Management Systems Certification to improve STAFF WRITERS the quality of locally manufactured products so Julius Edwin Mirembe • FEATURE: Timothy Kyamulesire that more Ugandan goods are able to access Ssemutooke Joseph UNBS Set To Open Ultra Modern regional and international markets. This has Akena Joel Food Safety Laboratories 8 translated in increased growth. East African Media Consult • LEAD STORY Exports to the East African region grew by DESIGN AND LAYOUT Unbs Upgrades Calibration Rig To 51.8 percent from US$ 89.40 million in May Allan Brian Mukwana State Of The Art 12 East African Media Consult 2016 to US$ 135.74 million in May 2017. -

Annual Report | Uganda Development Bank Ltd

2019 ANNUAL REPORT | UGANDA DEVELOPMENT BANK LTD 2019 Annual Report Improving livelihoods of Ugandans i www.udbl.co.ug 2019 ANNUAL REPORT | UGANDA DEVELOPMENT BANK LTD Our Mandate “To operate as Uganda’s Development Finance Institution, particularly through interventions in priority sectors and in line with the Government of Uganda’s development priorities” Purpose Statement “To improve the Quality of Life of Ugandans” High Impact Goals Reduce Poverty Build a Industrialize in Uganda – Sustainable Food Uganda – Create Uplift 500,000 System in Uganda Ushs 4 trillion in people out of – Relieve 1,000,000 industrial output poverty by 2024. people out of by 2024. hunger by 2024. ii 2019 ANNUAL REPORT | UGANDA DEVELOPMENT BANK LTD Table of Contents Minister’s Company Governance Foreword Overview Pg30 Pg03 Pg09 Operating Sustainability Financial Environment Report Sustainability Pg59 Pg64 Pg107 Human Financial Capital Statements Pg113 Pg117 iii 2019 ANNUAL REPORT | UGANDA DEVELOPMENT BANK LTD Definitions Value of Output: This is the measure of total economic activity in the production of new goods and services in an accounting period for the UDB funded projects. It is a much broader measure of the economy than the gross domestic product (GDP), which is limited mainly to final output (finished goods and services). Tax contribution: Refers to the annual direct or indirect taxes paid by funded projects. These include corporation tax, PAYE, VAT (18%), customs taxes, etc. Foreign exchange earnings: Refers to the foreign currency generated by funded projects expressed in Uganda Shillings equivalent. The foreign currency generated includes earnings arising from the export of goods and services Jobs created and maintained: Refers to the total number of permanent and temporary workers employed by funded projects and are paid a wage or income. -

The Promotional Activities and Consumer Behavior in Uganda Clays Limited at Kajjansi Entebbe Road

THE PROMOTIONAL ACTIVITIES AND CONSUMER BEHAVIOR IN UGANDA CLAYS LIMITED AT KAJJANSI ENTEBBE ROAD BEKUNDA HADSON MWINE BMM/11329/61/DU ARESEARCH PROJECT SUBMITED IN PARTIAL FULFILMENT FOR THE AWARD OF ADEGREE IN MARKETING AND MANAGEMENT OF KAMPALA INTERNATIAL UNIVERSITY (KIU) MAY2009 DECLARATION I Bekunda Hadson Mwine, a student of Kampala International University in the school of business and management, declare that this research project is original and has not been submitted in any institution for the award of a diploma or degree. ~~•t+ · - Signed: ........................................... ( .................................... BEKUNDA HADSON MWINE BMM/11329/61/DU (CANDIDATE) Date: ................... 0. \lb~.I?:~ ............................... APPROVAL This research project by Bekunda Hadson Mwine which was carried out under the title: PROMOTIONAL ACTIVITIES AND CONSUMER BEHAVIOR IN UGANDA CLAYS LIMITED AT KAJJANSI ENTEBBE ROAD' has been under my supervision and is now ready for submission to Kampala International University with my approval. MR. SSENDAGIRE HASSAN WASSWA (SUPERVISOR). Date ................ ~\\~ \~'t ................................. .. ...................... 11 DEDICATION I dedicate this research to my loving daddy Mr. Jackson Torogo and my dearest late Mummy Mrs. Niwamanya Winnie who labored tirelessly to provide me with descent education though their moral and financial support and has also instilled in me the nobility of honesty and fairness. These virtues will always remain my source of inspiration. May Almighty God bless them abundantly so that daddy may live to see the fruits of his blood. Ill ACKNOWLEDGEMENT The completion of my studies at Kampala International University could not have been possible without the support of some individuals: in a special way, I would like to express my gratitude to my daddy Mr. -

Uganda Clays Limited Annual Report 2019 .Pdf

BUILDING ON TOMORROW CONTENTS INTRODUCTION FINANCIAL STATEMENTS Notice Of Meeting ........................................................6 Directors Report ...........................................................58 Uganda Clays at a glance ........................................9 Statement of Directors Responsibility.............. 61 Corporate Information .............................................. 12 Report of the Independent Auditors..................62 About Us ............................................................................ 15 Our Products ................................................................... 16 Statement Of Profit Or Loss ....................................65 Statement Of Financial Position ..........................66 Chairman’s Statement ..............................................24 Statement Of Changes In Equity ..........................67 Managing Director’s Statement ............................28 Statement Of Cash Flows .........................................68 Notes To The Financial Statements ....................69 Our Year in Pictures ....................................................32 Sustainability Reporting ..........................................36 Notes ..................................................................................94 Corporate Governance ...............................................48 Board Of Directors ......................................................48 Management Team......................................................52 Managing Risk ...............................................................54 -

The “Uganda Gazettepublished

The ns tm biic or vgam» \ Published by “Uganda Gazette Authority Vol. XCIII No. 17 10th March, 2000 Price: Shs. 700 CONTENTS 11. CWH Importer Unknown/Capt 2 Dozs Men’s Shirts (New) 19 Dozs Boy’s Trousers The Customs Management Act— Notice................ 87-88 (New) 3 Pcs Gambling The Companies Act—Notice...................................... 88 Machines Display Screens 7 Dozs + 11 Pcs Perfumes The Advocates Act—Notices.............. 88 12. CWH Importer Unknown/Capt 1 Pkg Cloth, Toys, The Privatisation Unit—Notice.................................. 89 Windsrecn-Protectors Pottie Paraa Lodges Limited—Notice .......................... 89 13. CWH Assorted Importers (Capt) 8 Pkgs Assorted The Money Lenders Act—Notice .......................... 89 Personal Effects 14 CWH C. Drezen (Copt) 1 Pkg Assorted Spares The Trade Marks Act—Registration of applications 90-92 (Air Toulouse) and 20 Tins Turbo Oil Advertisements ................................................ 92-94 2350 940 ML 15. CWH Assorted Importers (Capt) 11 Pkgs Assorted Personal Effects 17 Pcs Toner Cartridges General Notice No. 95 of 2000. 1 Pc Used TV 1 Pkg Shower Fittings THE CUSTOMS MANAGEMENT ACT. 16. CWH Mukasa (EN) 1 Pc Fridge (Cap. 27). 1 Pc Washing Machine NOTICE OF SALE BY PUBLIC AUCTION. 2 Pcs Cleaner and Walker 1 Pc Fan Notice is hereby given for general information that 17. CWH Importer Unknown (EN) 47 Ctns Tassenburg Wine Uganda Revenue Authority will conduct a sale by public 18. CWH Nakascro Blood 2 Pkgs Tube Sealer auction for goods whose particulars appear in the Schedule Bank (EN) MDL ACS-152 hereto at lhe Customs Warehouse. 19. CWH Importer Unknown (EN) 4 Pkgs Assorted Garments 37 Rolls Textile Material Time: After one calendar month. -

Market Update 13Th July 2017

Market Update th 13 July 2017 USE ALSI Close: 1,653.29 Previous: 1,653.99 (UP:8.19%YTD) - USD/UGX: 3,597.71 Previous: 3,597.46 (UP: 0.17%YTD) USE ALSI* Key Statistics: Market Synopsis: Turnover dropped to Ugx10.78Mn ($2,997) from Ugx346.64Mn ($96,357) Close 1,653.29 1D* % Change (0.04) yesterday. Stanbic Bank Uganda (USE:SBU) traded the highest number of MTD* % Change (1.63) shares with 107,779 shares moved to realise a turnover of Ugx2.94Mn. Its share YTD* % Change 8.19 price appreciated by 0.93 to close at Ugx27.25. dfcu (USE:DFCU) and New Vision Printing and Publishing Company Limited (USE:NVL) realised 52 Week Range 1,330.82 – 1,701.46 Volume 119,679 turnovers of Ugx4.93Mn and Ugx2.91Mn from 6,500 shares and 5,400 shares Turnover (ugx) 10.78Mn ($2,997) traded at Ugx759 and Ugx539 each respectively. The USE All Share Index PE 9.25 depreciated by 0.04 percent to close at 1,653.29 whereas the C8 increased by EPS 35.33 0.299 percent closing today’s trading session at 117.06. Dividend Yield 1.0% Headlines: Market Cap (ugx) 22,598.48Bn ($6,281.35Mn) Uganda clays set for bumper UNRA settlement: Uganda Clays Limited (UCL) is set to receive Sh4.5b for land that was compulsorily acquired by the USE ALSI*- USE All Share Index, 1D*- One Day, MTD*- Month to Date, YTD*- Year to Date Uganda National Roads Authority (UNRA) for the construction of the Entebbe- Source: Uganda Securities Exchange, Bloomberg Kampala Expressway. -

Roskilde University

Roskilde University Assessing privatization in Uganda Kibikyo, David Lameck Publication date: 2009 Document Version Publisher's PDF, also known as Version of record Citation for published version (APA): Kibikyo, D. L. (2009). Assessing privatization in Uganda. Roskilde Universitet. General rights Copyright and moral rights for the publications made accessible in the public portal are retained by the authors and/or other copyright owners and it is a condition of accessing publications that users recognise and abide by the legal requirements associated with these rights. • Users may download and print one copy of any publication from the public portal for the purpose of private study or research. • You may not further distribute the material or use it for any profit-making activity or commercial gain. • You may freely distribute the URL identifying the publication in the public portal. Take down policy If you believe that this document breaches copyright please contact [email protected] providing details, and we will remove access to the work immediately and investigate your claim. Download date: 04. Oct. 2021 Assessing Privatization in Uganda David Lameck KIBIKY0 [email protected] Supervisor: Associate Professor Thorkil Gustav Casse, PhD IDS, Roskilde University, Denmark [email protected] A Thesis submitted to the Department of International Development Studies (IDS) for the Award of a Degree of Doctor of Philosophy (PhD) of Roskilde University Centre (RUC), Denmark 30 August 2008 Table of Contents Table of Contents ......................................................................................................... -

Kampala City Roads Rehabilitation Project Country: Uganda

Language: English Original: English PROJECT: KAMPALA CITY ROADS REHABILITATION PROJECT COUNTRY: UGANDA ESIA SUMMARY FOR THE PROPOSED SELECTED ROAD LINKS AND JUNCTIONS/INTERSECTIONS TO IMPROVE MOBILITY IN KAMPALA CITY Date: May 2019 Team Leader: G. MAKAJUMA, Transport Engineer, RDGE.3 Preparation Team E&S Team Member: E.B. KAHUBIRE, Social Development Officer, RDGE4 /SNSC 1 1. INTRODUCTION 1.1. Traffic congestion in Kampala city is fast growing due to a combination of poor roads network, uncontrolled junctions, and insufficient roads capacity which is out of phase with the increasing traffic (vehicular and pedestrian) on Kampala roads. This congestion results into higher vehicle operating costs, long travel times and poor transport services. The overall city aesthetics and quality of life is highly compromised by the dilapidated paved roads and sidewalks, unpaved shoulders and unpaved roads which are sources of mud and dust that hovers over large sections of the City. 1.2. The Government of Uganda through Kampala Capital City Authority (KCCA) with support from the African Development Bank intends to improve mobility in Kampala City through improvement of selected road links and Junctions/intersections. The selected junctions/intersections are to be signalized while the selected roads are to be dualled or reconstructed or upgraded to paved standard. 1.3. The National Environmental Act, CAP 153 requires that an Environmental Impact Assessment (EIA) is undertaken for all projects that are listed under the third schedule of the Act with a view of sustainable development. The proposed project is one of the projects listed under Section 3 (Transportation) of the Schedule. Therefore, to fulfill legal requirements an EIA has been conducted for the proposed project as part of the consultancy services for the preliminary and detailed engineering design of selected road links and junctions/intersections to improve mobility in Kampala City under the Second Kampala Institutional and Infrastructure Development Project. -

Journal of Agriculture and Crops Agro-Related Policy Awareness

Journal of Agriculture and Crops ISSN(e): 2412-6381, ISSN(p): 2413-886X Vol. 5, Issue. 5, pp: 57-64, 2019 Academic Research Publishing URL: https://arpgweb.com/journal/journal/14 Group DOI: https://doi.org/10.32861/jac.55.57.64 Original Research Open Access Agro-Related Policy Awareness and Their Influence in Adoption of New Agricultural Technologies; A Case of Tissue Culture Banana in Uganda Wanyana Barbra* Faculty of Agriculture, Uganda Martyrs` University Nkozi, P.O Box 5498, Kampala, Uganda Murongo Marius Flarian Faculty of Agriculture, Uganda Martyrs` University Nkozi, P.O Box 5498, Kampala, Uganda African Centre of Excellence in Agroecology and Livelihood Systems, Faculty of Agriculture, Uganda Martyrs University, Nkozi. P.O Box 5498, Kampala, Uganda Mwine Julius African Centre of Excellence in Agroecology and Livelihood Systems, Faculty of Agriculture, Uganda Martyrs University, Nkozi. P.O Box 5498, Kampala, Uganda Wamani Sam National Crops Resources Research Institute, P.O Box 7084, Kampala, Uganda Faculty of Agriculture, Uganda Martyrs` University Nkozi, P.O Box 5498, Kampala, Uganda Abstract Adoption of banana tissue culture in Uganda still remains low despite the availability of policies geared to enhancing agriculture. A survey was carried out on 115 smallholder farmers in Central Uganda to establish the influence of agro-related policies in tissue culture banana adoption between January and July 2018. Results from the study indicated that 83.8% of the respondents were aware about the Plan for Modernization of Agriculture policy as compared to National Agricultural Policy (5.5%), National Development Plan (13.12%) and Agricultural Sector Development Strategy and Investment Plan (3.3%). -

Nkumba Business Journal

Nkumba Business Journal Volume 17, 2018 NKUMBA UNIVERSITY 2018 1 Editor Professor Wilson Muyinda Mande 27 Entebbe Highway Nkumba University P. O. Box 237 Entebbe, Uganda E-mail: [email protected] [email protected] ISSN 1564-068X Published by Nkumba University © 2018 Nkumba University. All rights reserved. No article in this issue may be reprinted, in whole or in part, without written permission from the publisher. Editorial / Advisory Committee Prof. Wilson M. Mande, Nkumba University Assoc. Prof. Michael Mawa, Uganda Martyrs University Dr. Robyn Spencer, Leman College, New York University Prof. E. Vogel, University of Delaware, USA Prof. Nakanyike Musisi, University of Toronto, Canada Dr Jamil Serwanga, Islamic University in Uganda Dr Fred Luzze, Uganda-Case Western Research Collaboration Dr Solomon Assimwe, Nkumba University Dr John Paul Kasujja, Nkumba University Prof. Faustino Orach-Meza, Nkumba University Peer Review Statement All the manuscripts published in Nkumba Business Journal have been subjected to careful screening by the Editor, subjected to blind review and revised before acceptance. Disclaimer Nkumba University and the editorial committee of Nkumba Business Journal make every effort to ensure the accuracy of the information contained in the Journal. However, the University makes no representations or warranties whatsoever as to the suitability for any purpose of the content and disclaim all such representations and warranties whether express or implied to the maximum extent permitted by law. The views expressed in this publication are the views of the authors and are not necessarily the views of the Editor, Nkumba University or their partners. Correspondence Subscriptions, orders, change of address and other matters should be sent to the editor at the above address. -

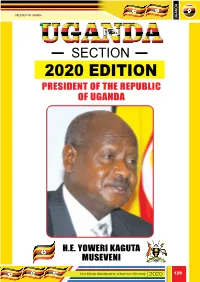

Uganda Section 2020

PRESIDENT OF UGANDA UGANDA UGANDA SECTION 2020 EDITION PRESIDENT OF THE REPUBLIC OF UGANDA H.E. YOWERI KAGUTA MUSEVENI East African Manufacturers & Investors Directory East African Manufacturers & Investors Directory 129 UGANDA PROFILE UGANDA UGANDA Uganda Profile ganda officially the Republic of Uganda, is a landlocked country in East Africa. Uganda is bordered to the east by Kenya, to the north by South Sudan, to the west by the Democratic Republic of the Congo, to the southwest Uby Rwanda, and to the south by Tanzania. Uganda is the world’s second most populous landlocked country after Ethiopia. The southern part of the country includes a substantial portion of Lake Victoria, shared with Kenya and Tanzania. Uganda is in the African Great Lakes region. Uganda also lies within the Nile basin, and has a varied but generally a modified equatorial type of climate. Uganda takes its name from the Buganda kingdom, which encompasses a large portion of the south of the country, including the capital Kampala. The people of Uganda were hunter-gatherers until 1,700 to 2,300 years ago, when Bantu- speaking populations migrated to the southern parts of the country. Environment and conservation The Crested crane is the national bird. Conservation in Uganda Uganda has 60 protected areas, including ten national parks: Bwindi Impenetrable National Park and Rwenzori Mountains National Park (both UNESCO World Heritage Sites[43]), Kibale National Park, Kidepo Valley National Park, Lake Mburo National Park, Mgahinga Gorilla National Park, Mount Elgon National Park, Murchison Falls National Park, Queen Elizabeth National Park, and Semuliki National Park. Economy and infrastructure The Bank of Uganda is the central bank of Uganda and handles monetary policy along with the printing of the Ugandan shilling. -

Annual Report Table of Contents I List of Acronyms Iv Company Information 01 02 03 02 About the Fund 12 Our Business 46 Financial Review

Annual Report Table Of Contents i List Of Acronyms iv Company Information 01 02 03 02 About The Fund 12 Our Business 46 Financial Review 02 30 Years of NSSF 13 Financial and Operational 48 Financial Performance Highlights 04 Our Locations 51 Business Review 19 Board Of Directors 05 Mission, Vision, Values 21 Senior Management Team 09 Why Save with NSSF 26 Chairman’s Statement 32 Managing Director’s Statement 37 Business Strategy 04 05 06 74 Corporate Governance and 102 Directors’ Report and Risk Management Financial Statements 170 Sustainability Report 75 Risk Management and Control 103 Statement of Directors’ 173 Responsible Business 85 Corporate Governance and Responsibility 185 Contributing to Sustainable Remuneration Report 104 Report of Auditor General on Economic Growth Financial Statements 189 Environmental Management 106 Financial Statements 193 Corporate Social Responsibility 110 Notes to the Financial Statements i ii List Of Acronyms ACCA Association of Chartered Certified Accountants NOTU National Organisation of Trade Unions AMM Annual Members’ Meeting NSE Nairobi Stock Exchange BA. Bachelor of Arts NSSF National Social Security Fund Bn. Billion PDL Premier Developments Limited BSc. Bachelor of Sciences Rd. Road CCW Customer Connect Week RSE Rwanda Stock Exchange COFTU Central Organisation Of Free Trade Unions SAA Strategic Asset Allocation CSR Corporate Social Responsibility SACA Staff Administration and Corporate Affairs Committee DSE Dar-Es-Salam Stock Exchange VPDL Victoria Properties Development Limited EIA Environmental Impact Assessment WHT Witholding Tax ExCo Executive Committee FCCA Fellow of the Chartered Certified Accountants IAS International Accounting Standards IASB International Accounting Standards Board ICPAU Institute of Certified Public Accountants of Uganda IFRS International Financial Reporting Standards K Thousand KCCA Kampala City Council Authority KPI Key Performance Indicator Kshs.