Whyalla and EP Heavy Industry Cluster Summary Background

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

To Download the Whyalla Trip Guide

c/- Adelaide University Sport, University of Adelaide, SA 5005 Whyalla Trip Guide General Trip Overview Revision 0 (compiled by David Warren 30/05/2018) Whyalla Trip Guide Rev0 Page 1 Adelaide University Scuba Diving Club Table of contents Table of contents ......................................................................................................................... 2 1 Introduction ......................................................................................................................... 3 2 Location ............................................................................................................................... 4 2.1 Accommodation .................................................................................................................................... 6 3 Finances ............................................................................................................................... 7 4 Diving ................................................................................................................................... 8 4.1 Shore Sites ............................................................................................................................................. 8 4.1.1 Stony Point ............................................................................................................................................................................. 8 4.1.2 Black Point ............................................................................................................................................................................. -

The Underground Economy and Carbon Dioxide (CO2) Emissions in China

sustainability Article The Underground Economy and Carbon Dioxide (CO2) Emissions in China Zhimin Zhou Lingnan (University) College, Sun Yat-Sen University, Guangzhou 510275, China; [email protected]; Tel.: +86-1592-6342-100 Received: 21 April 2019; Accepted: 9 May 2019; Published: 16 May 2019 Abstract: China aims to reduce carbon dioxide (CO2) intensity by 40–45% compared to its level in 2005 by 2020. The underground economy accounts for a significant proportion of China’s economy, but is not included in official statistics. Therefore, the nexus of CO2 and the underground economy in China is worthy of exploration. To this end, this paper identifies the extent to which the underground economy affects CO2 emissions through the panel data of 30 provinces in China from 1998 to 2016. Many studies have focused on the quantification of the relationship between CO2 emissions and economic development. However, the insights provided by those studies have generally ignored the underground economy. With full consideration of the scale of the underground economy, this research concludes that similar to previous studies, the inversely N-shaped environmental Kuznets curve (EKC) still holds for the income-CO2 nexus in China. Furthermore, a threshold regression analysis shows that the structural and technological effects are environment-beneficial and drive the EKC downward by their threshold effects. The empirical techniques in this paper can also be applied for similar research on other emerging economies that are confronted with the difficulties of achieving sustainable development. Keywords: carbon emissions; informal economy; EKC; industry structural effects; technological effects 1. Introduction During the past few decades, climate change has been a challenging problem all over the world [1]. -

Whyalla and Eyre Peninsula

SOUTH AUSTRALIAN CENTRE FOR ECONOMIC STUDIES ADELAIDE & FLINDERS UNIVERSITIES Regional Development Australia Whyalla and Eyre Peninsula Overview Geography RDA Whyalla and Eyre Peninsula covers an area of 170,500 square kilometres or 17.3 per cent of the State’s land mass. Population As at 30th June 2010 the region’s population was 58,700 persons or 3.6 per cent of the State’s population. The Indigenous population was estimated at 2,500 persons or 4.4 per cent of the region’s population. Economy and Labour force The region contributed $2,297 million to the State economy in 2006/07 or 3.4 per cent of gross state product. The four largest employing industries in the Whyalla Eyre Peninsula region were agriculture and fisheries (18.2 per cent), retail trade (14.3 per cent), manufacturing (11.9 per cent) and health and community services (10.9 per cent). Mining was relatively small at 1.4 per cent but is likely to show strong growth in the median term. The labour market is relatively strong with a participation rate above the State average and lower unemployment than the State average. Participation in VET courses is well above that for the State as a whole, while full-time participation in secondary school at age 16 is 71.4 per cent compared to South Australia at 78.4 per cent. NAPLAN reading results at year 3 are 15 percentage points lower than the State average but by year 7 they are 4.5 percentage points below the State average which indicates stronger school attendance over primary years of schooling. -

2021 Sustainability Report 3

1 2021 Sustainability Report 3 Contents CEO statement We acknowledge the Traditional Owners It is with great pleasure that I present the 2021 of the land on which our operations exist 3 CEO statement Santos Sustainability Report, demonstrating how and on which we work. We recognise their the principles of sustainability are critical to 4 About us the way that we operate our business and deliver continuing connection to land, waters on our Transform-Build-Grow strategy. and culture. We pay our respects to their 7 Our approach to sustainability Elders past, present and emerging. As Australia’s biggest domestic gas supplier and a leading 7 Our sustainability pillars Asia-Pacific LNG supplier, Santos has improved the lives of people throughout Australia and Asia for more santos.com/sustainability/ Governance and than 50 years. Our values drive everything we do, as we 9 build a better future for our customers, employees and management approaches the communities in which we operate. With significant expansion in recent years, this responsibility grows even As a major fuels producer for the Asia-Pacific region, 12 Structure of this report greater. Santos assets span across Australia, Papua Santos has an important global role to play in a sustainable New Guinea and Timor-Leste, with our focus continuing world. We are committed to realising a global future where 13 Economic sustainability to be on safely providing cleaner, reliable, low-cost temperature increase is limited to below 2 degrees Celsius, fuel products. while reliable and affordable energy continues to power 17 Health and safety domestic and global markets. -

Olympic Dam Expansion Draft Environmental Impact Statement 2009 Executive Summary

OLYMPIC DAM EXPANSION DRAFT ENVIRONMENTAL IMPACT STATEMENT 2009 EXECUTIVE SUMMARY Olympic Dam Expansion Draft Environmental Impact Statement 2009 Executive Summary 1 DISCLAIMER The Draft Environmental Impact Statement (Draft EIS) has been prepared by Arup Pty Ltd and ENSR Australia Pty Ltd (Arup/ENSR) on behalf of BHP Billiton Olympic Dam Corporation Pty Ltd (BHP Billiton) for submission to the Commonwealth Minister for Environment, Heritage and the Arts under the Environment Protection and Biodiversity Conservation Act 1999 (Commonwealth), the South Australian Minister for Mineral Resources Development under the Development Act 1993 (SA) and the Roxby Downs (Indenture Ratification) Act 1982 (SA) (and the indenture scheduled to that Act) and the Northern Territory Minister for Natural Resources, Environment and Heritage under the Environmental Assessment Act and the Environmental Assessment Administrative Procedures (together, the Ministers). The Draft EIS has been prepared for that purpose only and no one other than the Ministers should rely on the information contained in the Draft EIS to make any decision. In preparing the Draft EIS, Arup/ENSR and BHP Billiton have relied on information provided by specialist consultants, government agencies and other third parties available during preparation. BHP Billiton has not fully verified the accuracy or completeness of that information, except where expressly acknowledged in the Draft EIS. The Draft EIS has been prepared for information purposes only and, to the full extent permitted by law, BHP Billiton, in respect of all persons other than the Ministers, makes no representation and gives no warranty or undertaking, express or implied, in respect of the information contained in the Draft EIS and does not accept responsibility and is not liable for any loss or liability whatsoever arising as a result of any person acting or refraining from acting on any information contained in the Draft EIS. -

Annual Report 2018-2019

THE CORPORATION OF THE CITY OF ANNUAL REPORT 2018/2019 Reconciliation Action Plan Working Group ACKNOWLEDGEMENT OF COUNTRY We acknowledge the lands in our region belonging to the Barngarla people, and acknowledge them as the traditional custodians from the past, for the present and into the future. The Barngarla people are strong, and are continuously connecting to their culture and their country. Whyalla City Council and the Barngala people can work together to build a stronger future. This document fulfils our obligations under the Local Government Act 1999 which stipulates that all councils must produce an Annual report (relating to the immediately preceding financial year) to be prepared and adopted by council on or before 30 November. Information within this report is as prescribed by the legislation and as per the Annual Report Guidelines provided by the Local Government Association of South Australia. DISCLAIMER Every effort has been made to ensure the information contained within this Annual Report is accurate. No responsibility or liability can be accepted for any inaccuracies or omissions. 2018 – 19 ANNUAL REPORT CONTENTS MAYORS MESSAGE 1 OUR PEOPLE 40 CEO’S MESSAGE 2 OPERATIONAL HIGHLIGHTS OUR CITY PROFILE 3 CITY GROWTH 47 STRATEGIC PLAN 2017-2022 4 TOURISM 51 MEASURING OUR PERFORMANCE EVENTS 59 OUR PEOPLE 5 COMMUNITY 60 OUR PLACES 9 ARTS AND CULTURE 63 OUR ECONOMY 13 YOUTH 65 OUR IMAGE 17 CORPORATE 67 STRATEGIC MANAGEMENT PLANS, AIRPORT 69 DOCUMENTS & PROGRAMS 19 WHYALLA JETTY UPDATE 71 2018/2019 ANNUAL BUSINESS PLAN SUMMARY 20 INFRASTRUCTURE 73 ELECTED MEMBERS 23 FINANCIAL STATEMENT 90 GENERAL POLICIES 31 SUBSIDIARY REPORTS 136 CONNECTING WITH OUR COMMUNITY 35 1 CITY OF WHYALLA MAYOR'S MESSAGE I am pleased to present Whyalla City Council’s 2018-19 Annual Report, in my first term as Mayor of the City of Whyalla. -

Santos 2021 Climate Change Report

1 Climate Change Report Santos Climate Change Report 2021 CEO Statement Report highlights Contents 4 About us Industry-leading targets NTO SA S 6 CEO statement + Santos to achieve net-zero emissions by 2040. NET-ZERO 8 Executive summary + 26-30 per cent reduction from 2019-20 EMISSIONS 12 Introduction emissions and emissions intensity by 2030. + Reduce customer emissions by more than 16 Metrics and targets 2 0 4 0 one million tonnes per annum by 2030. Santos’ strategy and 22 climate change 46 Governance and risk Resilience and opportunity Zero-emission Zero-emission technologies: 54 technologies: carbon clean hydrogen in a lower-carbon future capture and storage (CCS) + Pathway to cleaner fuels + Moomba CCS Project ready for enabled by low-cost CCS. We acknowledge the Traditional final investment decision: the + Established new Midstream Owners of the land on which our world’s second largest CCS Infrastructure and Low-carbon project with lowest unit cost at Fuels division. operations exist and on which we less than A$30 per tonne. work. We recognise their continuing + Ability to store 1.7 million connection to land, waters and tonnes of CO2 per annum with culture. We pay our respects to their potential of up to 20 million. Reducing operational Elders past, present and emerging. emissions santos.com/sustainability + Emissions intensity reduced 20 per cent in the past 5 years. Nature-based offsets + Stringent management and Disclaimer: This report contains forward looking statements that are subject + West Arnhem Land Fire to risk factors associated with the oil and gas industry. It is believed that reporting of emissions. -

The Dynamics of Industrial Growth In

The Dynamicsof Industrial Growth in the Old Northwest 1830-70:An InterdisciplinaryApproach Margaret Walsh Department of History, University of Birmingham and University of Illinois, Chicago Circle Historians have customarily talked about the economic devel- opment of the Old Northwest in the middle years of the 19th cen- tury within an agrarianframework. 1 Thoughthe Jeffersonianimage has been modernized and modified by studies of the rapid growth of commercial farming, of the national importance of mineral and for- est resources, and of urban frontiers, little systematic attention has yet been given to the growth of a manufacturing sector. Pre- sumablywestern industrial enterpriseswere either nonexistentor unimportant. A similar conclusion about the insignificance of manufactur- ing in the Old Northwest in the period 1830-70 could be reached from a different approach -- namely an analysis of the process of American industrialization. Throughout both the customary and "new" discussions of the timing, location, and causes of indus- trial growth, attention has been focused on the Northeastern States. Presumably cotton textiles, heavy goods, or the railroad provided the keys to understanding the rise of the factory system somewhere between 1815 and 1850. But neither the West nor the Southwas destined to playa noteworthypart in the modernization of the economy. Given this disinterest in or lack of information on western manufacturing in a period in which the American economy was under- going rapid change, some quantitative evidence must first be pro- duced to show that there was an industrial sector which fulfilled a significant function in both regional and national development. Then it is possible to discuss alternative approaches to analyzing the dynamics of growth before suggesting a new synthesis. -

North East of England

Organisation for Economic Co-operation and Development Directorate for Education Education Management and Infrastructure Division Programme on Institutional Management of Higher Education (IMHE) Supporting the Contribution of Higher Education Institutions to Regional Development Peer Review Report: North East of England Chris Duke, Robert Hassink, James Powell and Jaana Puukka January 2006 The views expressed are those of the authors and not necessarily those of the OECD or its Member Countries. 1 This Peer Review Report is based on the review visit to the North East of England in October 2005, the regional Self-Evaluation Report, and other background material. As a result, the report reflects the situation up to that period. The preparation and completion of this report would not have been possible without the support of very many people and organisations. OECD/IMHE and the Peer Review Team for the North East of England wish to acknowledge the substantial contribution of the region, particularly through its Coordinator, the authors of the Self-Evaluation Report, and its Regional Steering Group. 2 TABLE OF CONTENTS PREFACE...................................................................................................................................... 5 ABBREVIATIONS AND ACRONYMS...................................................................................... 7 1. INTRODUCTION..................................................................................................................... 9 1.1 Evaluation Context and Approach -

MEAT SOURCING Engaging Qsrs on Climate and Water Risks to Protein Supply Chains

GLOBAL INVESTOR ENGAGEMENT ON MEAT SOURCING Engaging QSRs on climate and water risks to protein supply chains PROGRESS BRIEFING • APRIL 2021 1 Executive summary The Global Investor Engagement on Meat However, progress towards mitigating risks related Sourcing, initiated in 2019, consists of dialogues to water scarcity and pollution has been limited. between six of the largest quick-service restaurant In addition, only two of the six companies have (QSR) brands and institutional investors with over disclosed plans to conduct a 2°C scenario analysis, a $11 trillion in combined assets. Investors have urged key recommendation of the Task Force on Climate- the QSRs to analyse and reduce their vulnerability Related Financial Disclosures (TCFD). While the to the impacts of climate change, water scarcity, progress to date is encouraging, there are critical and pervasive threats to water quality driven by elements yet to be addressed around climate and animal protein production. water-related financial risks. Companies have made notable progress in addressing these concerns. All six target companies have now publicly stated they will set or have already set global GHG reduction targets. Five of the six QSRs have now set or committed to setting emissions reduction targets approved by the Science-Based Targets initiative (SBTi) that would align their businesses with the Paris Agreement’s goal to limit global temperature rises to well below 2°C. 2 Contents The case for engagement 4 Trends in company performance 6 Board oversight and ESG risk management -

Engineering / Builders Risk at a Glance

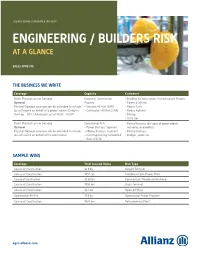

ALLIANZ GLOBAL CORPORATE & SPECIALTY® ENGINEERING / BUILDERS RISK AT A GLANCE SALES APPETITE THE BUSINESS WE WRITE Coverage Capacity Customers Direct Physical Loss or Damage Course of Construction •Building & Construction / Infrastructure Projects Optional Projects •Power & Utilities Physical Damage coverage can be extended to include –Erection All Risk (EAR) • Heavy Civils loss of income on behalf of a project owner (Delay in –Contractors All Risk (CAR) •Heavy Industry Start-up – DSU / Advanced Loss of Profit – ALOP) • Mining •Oil & Gas Direct Physical Loss or Damage Operational Risk • Power Business (all types of power plants, Optional – Power Business Segment including renewables) Physical Damage coverage can be extended to include – Mining Business Segment • Mining Business loss of income on behalf of the plant owner – Civil Engineering Completed • Bridges, roads etc. Risks (CECR) SAMPLE WINS Coverage Total Insured Value Risk Type Course of Construction $1.9 bn Airport Terminal Course of Construction $855 mn Combined Cycle Power Plant Course of Construction $1.65 bn Commercial / Residential Building Course of Construction $930 mn Grain Terminal Course of Construction $2.3 bn Open-pit Mine Operational All Risk $7.5 bn Operational Power Program Course of Construction $876 mn Petrochemical Plant agcs.allianz.com STANDARD & POOR‘S AA A.M. BEST A+ FOR MORE INFORMATION PLEASE CONTACT: TIM COOK Regional Head of Engineering, North America Tel: +1.212.823.8972 [email protected] CONTRACTORS ALL RISK / ERECTION ALL RISK / CIVIL ENGINEERING -

17 May 2012 One Thousand Export Cargoes from Port Bonython Today

Media enquiries Chandran Vigneswaran +61 8 8116 5856 / +61 (0) 467 775 055 [email protected] 17 May 2012 One thousand export cargoes from Port Bonython Today marked the 1,000th export cargo from Santos’ Port Bonython liquids processing plant near Whyalla in South Australia. Santos celebrated the milestone with the presentation of a commemorative plaque to the captain of the Tandara Spirit, currently taking on a cargo of crude oil. Port Bonython – named in honour of Santos’ founding Chairman, John Bonython AO – issued its first shipment in 1983. Since then, more than 40 million tonnes of product including crude oil, LPG and naphtha have been exported from the plant. Cargoes have gone to all Australian domestic refineries, New Zealand, Singapore, Japan, Hawaii, Indonesia, Hong Kong, Japan, India, Taiwan, South Korea and China. Gross revenue generated by Port Bonython totals over $14 billion and total gross wharfage paid to the South Australian Government exceeds $70 million. “We’re very pleased to celebrate this significant milestone,” said Lou Dello, Santos’ General Manager Oil & Offshore Business. “Port Bonython has long been an important part of Santos’ business, processing liquids from the Cooper Basin in South Australia’s remote north and shipping them right across the country and the Asia-Pacific. “It’s a testament to the vision of the company at the time, and the ongoing commitment of our employees, that Port Bonython remains a thriving business today.” Santos is the operator of Port Bonython and a 66.6% shareholder, with partners Delhi holding 20.2% and Origin 13.2%. Ends.