Impact Evaluation Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

9M 2019 Results Briefing Reports

Q1 Q2 Q3 (Amounts in Mln PhP, Except Sales Volume) Q1 2019 Q2 2019 Q3 2019 Q1 2018 Q2 2018 Q3 2018 % Inc (Dec) % Inc (Dec) % Inc (Dec) Sales Volume (GWh) 10,381 12,442 12,182 10,145 11,520 11,256 2% 8% 8% Revenues 75,378 89,575 76,173 70,807 79,737 76,867 6% 12% -1% Electric 73,632 87,635 74,109 69,009 77,894 74,363 7% 13% 0% Distribution 14,273 18,182 16,769 14,081 16,582 15,546 1% 10% 8% Generation and other pass-through 59,359 69,453 57,340 54,928 61,312 58,817 8% 13% -3% Non-electricity 1,746 1,940 2,064 1,798 1,843 2,504 -3% 5% -18% Core Income 5,598 6,719 6,136 4,917 5,934 5,835 14% 13% 5% Reported Income 5,671 6,336 6,314 5,312 6,661 6,239 7% -5% 1% Core EBITDA 8,828 11,051 9,883 8,688 8,897 8,979 2% 24% 10% Reported EBITDA 8,828 11,051 9,883 8,688 8,897 8,979 2% 24% 10% 241,126 241,126 227,411 227,411 Distribution revenues 49,224 46,209 Q3 76,173 76,867 Q2 89,575 79,737 Generation & other pass- 186,152 through charges 175,057 Electricity Revenues = 235,376 = Revenues Electricity Electricity Revenues = 221.266 = Revenues Electricity Q1 75,378 70,807 Non-electricity revenues 5,750 6,145 9M 2019 9M 2018 9M 2019 9M 2018 6,400 9,092 19,346 3% 4% 9% Costs Costs and Expenses 183,355 84% Purchased Power Operating Expenses Depreciation & Amortization Other Expenses 15,701 Others 10,048 Subtransmission & 23% Distribution Facilities 77% Capital Capital Expenditures 9M 2019 9M 2018 12.3% 11.7% 12.3% 11.7% Margins 7.7% 7.3% 7.6% 8.0% 29,762 29,762 26,564 26,564 Q3 9,883 9,883 8,979 8,979 18,453 18,321 18,212 16,686 6,136 6,314 Q2 11,051 -

ADDITIONAL REVENUE STREAMS for SERVICE PROVIDERS USING GPON Fttx SOLUTIONS

Addition Revenue Streams for Service Providers Using GPON Solutions Reggie A. Posadas BSEE MSIEM MSECE Philippine Country Manager YFC-BONEAGLE International Inc., ADDITIONAL REVENUE STREAMS FOR SERVICE PROVIDERS USING GPON FTTx SOLUTIONS Reggie A. Posadas BSEE MS IEM MS ECE Country Manager, Philippines YFC-BONEAGLE INTERNATIONAL, INC. ADDITIONAL REVENUE STREAMS FOR SERVICE PROVIDERS USING GPON FTTx SOLUTIONS Lecture Outline : 1. Introduction to GPON FTTx Cabling 2. GPON FTTx Cabling Architecture 3. GPON Business Models 4. Sample Additional Revenue Streams Thru GPON FTTx 5. Sample Project/s ADDITIONAL REVENUE STREAMS FOR SERVICE PROVIDERS USING GPON FTTx SOLUTIONS Introduction to GPON FTTx Cabling GPON OVERVIEW PON/GPON grew from a requirement for more bandwidth in the Service Provider Market. (Higher access speeds than DSL could deliver) More Bandwidth (2.5G Downstream and 1.2G Upstream) – Higher Subscriber density – Best replacement for aging copper / coax infrastructure – Environmentally friendly - green – Reduce power and TCO (Total Cost of Ownership) • Long term life expectancy of the fiber infrastructure • Lower capital expenditures, since AN eqpt. and components are considerably reduced and/or completely excluded in the FTTx network • Lower operating costs through reduction of active components, support for greater distances between equipment nodes • Reduced re-occurring operating and maintenance costs ADDITIONAL REVENUE STREAMS FOR SERVICE PROVIDERS USING GPON FTTx SOLUTIONS Introduction to GPON FTTx Cabling GPON OVERVIEW • The -

Club Intramuros Golf Course

ClubClub IntramurosIntramuros GolfGolf CourseCourse BonifacioBonifacio Drive,Drive, Intramuros,Intramuros, ManilaManila The golf course is stretched on a prime parcel of land bounded on the West by Roxas Blvd., from Del Pan Bridge to Manila Hotel; on the East by P. Burgos, from the Manila City Hall to Roxas Boulevard; and on the North to Northwest by the walls of Intramuros, from Del Pan Bridge to the Manila Bulletin Building. It is adjacent to the historic Fort Santiago, Letran College and the Port Area. Competitive Advantages: v Unique - This is the only day & night golf course; it can host weddings, parties and seminars. v Historical - It is set amidst the old Spanish walled city of Intramuros, with the San Agustin Church and Manila Cathedral providing a scenic backdrop. v Accessibility – It is located right in the heart of the City of Manila. v Environmentally friendly – the planning and development of the golf course improved the scenery due to the additional trees planted within and outside the property and fresh water from the lagoon is used to irrigate the golf course. Mode of Privatization: Lease/Management Contract Total Land Area: 233,600 sqm Status: Operational Legal Bases: PD 1763 TIEZA Business Development Department Tourism Infrastructure & Enterprise Zone Authority 142 Amorsolo St. Legaspi Village Makati Contact no. 831-0811 Facilities: Par 66, 18-hole Day & Night Golf Course Driving Range Practice Green Main Club Verandah Restaurant Main Dining Room (A/C – 70 pax) Function Room (A,B & C - 150 pax) Executive Lounge VIP Room Locker Room (male & female) Roof Deck (Open Air, (300 – 400 pax) Male / Female Comfort Room Administration Offices 19th Hole Bar & Restaurant Utilities: A. -

Celebrating a Future of Possibilities 2 MERALCO POWERCLUB MERALCO POWERCLUB 3 AUGUST 2017 AUGUST 2017 Inside MESSAGES a MERALCO PUBLICATION

MERALCO POWERCLUB 1 AUGUST 2017 A MERALCO PUBLICATION | SPECIAL LUMINARIES EDITION | AUGUST 2017 CELEBRATING A FUTURE OF POSSIBILITIES 2 MERALCO POWERCLUB MERALCO POWERCLUB 3 AUGUST 2017 AUGUST 2017 INSIDE MESSAGES A MERALCO PUBLICATION MERALCO POWER CLUB MAGAZINE VOLUME 7 ISSUE 3 eralco launched its Luminaries and open access to keep them PUBLISHER: SUMMIT MEDIA LOOK BACK, program six years ago, when competitive. We enable their pursuit of Analysis A joint project with Meralco’s Mthe Philippine economy was green initiatives with renewable energy 4 CAN WE AFFORD TO SAVE Corporate Business Group, Marketing, MOVE beginning to take off. Inspired by Meralco sources or electric-vehicle and charging THE CLIMATE? Customer Solutions and Product Chairman Manuel V. Pangilinan, our systems. And to serve them and their The Paris Agreement compels even V20 members to tap renewable energy Development. Published four times a FORWARD vision for the Luminaries is to showcase local communities, we build large-scale year for key officers of Meralco businesses that make a difference in the electric infrastructure for their real-estate Electric Capital Projects corporate accounts. lives of Filipinos across the country. projects. 7 ENERGIZING THE ASEAN AT 50 Our pioneering Luminaries As the economy continues to Meralco makes sure the Philippines’s hosting of the Asean Summit goes at full power EDITORIAL TEAM were already household names in the soar, we anticipate more positive EDNA T. BELLEZA Publisher electronics, food manufacturing, and real- changes. Small businesses become large Industry Trends estate sectors; companies like Samsung enterprises. Established businesses 8 COLD COMFORTS Estrellita Faustino Editor-in-Chief Companies in the air conditioning business look Electro Mechanics Philippines, Universal diversify into non-core activities such Creative Director/ forward to a promising business climate DONDI LIMGenco Robina Corp., and Ayala Land Inc. -

DECARBONIZING MERALCO the Imperatives to Prioritize Pro-People, Pro-Climate Models in the Power Business

DECARBONIZING MERALCO The imperatives to prioritize pro-people, pro-climate models in the power business To be part of the solution to the climate crisis, power companies must urgently shift to renewable energy. This study shows how the Philippines’ biggest distribution utility Meralco, together with its power generation subsidiary MGen, can refocus its business and source all of its new energy contracts from renewable energy while ensuring a reliable, affordable, and secure supply of clean electricity. DECARBONIZING MERALCO The imperative to prioritize pro-people, pro-climate models in the power business © Greenpeace Southeast Asia - Philippines, April 2021 Greenpeace is a global, independent campaigning organization that uses peaceful protest and creative communication to expose global environmental problems and promote solutions that are essential to a green and peaceful future. Greenpeace has been present in the Philippines since 2000, working to safeguard the constitutional rights of Filipinos to a balanced and healthful ecology. Greenpeace Southeast Asia - Philippines 30 Scout Tuason Street Room 201 JGS Building, Quezon City, 1103 Metro Manila, Philippines www.greenpeace.org.ph The Center for Renewable Energy and Sustainable Technology (CREST) is the lead author of this report. CREST is a non-government organization that promotes the use of renewable energy systems and climate technologies by providing technical support and capacity-building to cities and communities. Decarbonizing Meralco is dedicated to the memory of the late Roberto S. Verzola, who was the lead researcher for this project. DECARBONIZING MERALCO The imperatives to prioritize pro-people, pro-climate models in the power business Table of Contents PART 1: Meralco, the Company PART 3: Generation Cost A. -

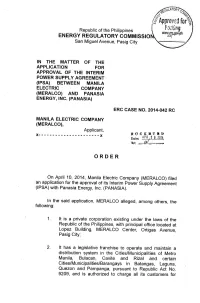

X------X Date: .~~!3,F.?~.~.,.~Rm

Republic of the Philippines ENERGY REGULATORY COMMISSIO San Miguel Avenue, Pasig City IN THE MATTER OF THE APPLICATION FOR APPROVAL OF THE INTERIM POWER SUPPLY AGREEMENT (IPSA) BETWEEN MANILA ELECTRIC COMPANY (MERALCO) AND PANASIA ENERGY, INC. (PANASIA) ERC CASE NO~ 2014-042 RC MANILA ELECTRIC COMPANY (MERALCO), Applicant. DOCKliTliD x----------------------x Date: .~~!3,f.?~.~.,.~rm. -my: _ ••.ttY.:&llU"-__ ORDER On April 10, 2014, Manila Electric Company (MERALCO) filed an application for the approval of its Interim Power Supply Agreement (IPSA) with Panasia Energy, Inc. (PANASIA). In the said application, MERALCO alleged, among others, the following: 1. It is a private corporation existing under the laws of the Republic of the Philippines, with principal office located at Lopez Building, MERALCO Center, Ortigas Avenue, Pasig City; 2. It has a legislative franchise to operate and maintain a distribution system in the Cities/Municipalities of Metro Manila, Bulacan, Cavite and Rizal and certain Cities/Municipalities/Barangays in 8atangas, Laguna, Quezon and Pampanga, pursuant to Republic Act No. 9209, and is authorized to charge all its customers for ERC CASE NO. 2014-042 RC ORDER/April 21, 2014 Page 2 of 19 their electric consumption at the rates approved by the Commission; 3. PANASIA is a corporation duly organized and existing under the laws of the Republic of the Philippines, with office address at E-3204-B Philippine Stock Exchange Centre, Exchange Road, Ortigas Center, Pasig City. It operates and manages the energy output of the 540 MW diesel-fired combined cycle power plant in Limay, Bataan (Limay Plant); 4. Based on the power supply forecast of the System Operator, National Grid Corporation of the Philippines (NGCP), for the supply period April to June 2014, the reserve capacity will be below the required Contingency Reserves due to scheduled maintenance shutdowns and forced outages of major baseload coal- and gas-fired power plants in Luzon; 5. -

Sustaining Energy 2019 Meralco Annual Report

Sustaining Energy 2019 Meralco Annual Report 2019 Reports Meralco Annual Report Meralco Sustainability Report One Meralco Foundation Annual Report Our Cover With the backdrop of a sky at dusk, mother and child admire the view of tree-lined residential houses Meralco is the largest private sector electric distribution utility in the set against a cityscape. Amid this urban growth, Meralco in 2019 embeds sustainability in its business Philippines. It covers 36 cities and 75 municipalities, with a franchise area strategy – with a promise of prosperity and of a planet worth admiring for generations to come. of 9,685 square kilometers. This coverage is just 3% of the land area of the Philippines, but accounts for 55% of the country’s electricity output. Celebrating 117 years of service in 2020, the Company is committed to its record of providing reliable and affordable energy. Our Reports Beginning 2019, Manila Electric Company (Meralco) is providing three annual reports: the first covers the distribution utility and its subsidiaries; the second is its sustainability report; and the third is that of its social development arm, One Meralco Foundation. Sustaining Energy 2019 Meralco Annual Report Sustaining Energy: Sustaining Energy shows Meralco’s transition to renewable energy to better support future generations, and executes a digital transformation to upgrade its systems and operations for greater efficiency and a better customer experience. Sustaining the Future 2019 Meralco Sustainability Report Sustaining the Future: Sustaining the Future maps out Meralco’s sustainability agenda, in the context of the United Nations Sustainable Development Goals. It details the focus on Power, Planet, People, and Prosperity in alignment with Meralco’s business strategy. -

A Financial and Operational Analysis of Meralco

Presented at the DLSU Research Congress 2015 De La Salle University, Manila, Philippines March 2-4, 2015 A Financial and Operational Analysis of Meralco Cheska Kamille Soriano, Christian Johanne Co, Catherine Lei Chua, Riane Charlene Ng, Ferdinand Licup, Cindee Yu De La Salle University Taft Ave., Malate, Manila Abstract: Meralco, being the largest utility distribution company in the Philippines for 111 years, providing power to 5, 189, 247 customers, has indeed, been serving a large portion of the country’s population. The Meralco Group Structure is in charge of a number of corporations such as the Clark Electric Distribution Corporation (CEDC), Meralco Powergen Corporation (MPC), Lighthouse Overseas Insurance Limited (LOIL) and Corporation Information Solutions, Inc. (CIS). This is a paper that summarizes the analysis on the current financial and operational aspects of Meralco. Being the country’s service power of choice, it holds opportunities for franchise expansion and innovative solutions, catering to a wide range of market, however, uncontrollable number of power pilferers and the increasing number of solar panel users pose a threat to the success of this firm. A weakness is the incorrect and unwanted charging of electricity to several consumers. The objective of this paper is to analyze Meralco Group’s current financial situation through sales, operational and financial performance, analyze its developments over the years and suggest appropriate strategies for improvement or recommendations. In the report, the highlights of the quarter, balance sheets, statement of income and statement of retained earnings are shown. With the determination to serve in a constant and relentless manner, Meralco has reached a core net income of 12.07 billion pesos and a total revenue of 298.6 billion pesos. -

Meralco Powers up a New Model for Customer Service Excellence

VMWARE CASE STUDY Meralco Powers Up a New Model for Customer Service Excellence INDUSTRY The Philippine electricity distributor needed to transform Utilities its IT function from a cost center to a driver of innovation, operational excellence and cost-effectiveness. Virtualizing its LOCATION datacenters has enabled Meralco to cut the time needed to The Philippines deliver applications such as a new pre-paid retail electricity system, automate key infrastructure processes, and ensure KEY CHALLENGES • Boost the effectiveness of IT business continuity in the event of a major datacenter outage. service delivery • Achieve greater flexibility to support business growth • Streamline disaster recovery processes Meralco is the largest electricity distributor in the Philippines with a franchise area of 9,337 square kilometers, covering 25 percent of the country’s total population. SOLUTION Implement VMware The company provides power to about “As in most organizations, the IT virtualization as the foundation 5.4 million residential, commercial and function was generally viewed as a cost of a more effective IT delivery industrial customers in 34 cities and 77 center within Meralco,” said Marthyn model with automated disaster municipalities, including Metro Manila, the Cuan, Meralco Vice President and Chief recovery, infrastructure provinces of Rizal, Cavite and Bulacan, Information Officer. “We wanted to management and efficient and parts of the provinces of Pampanga, change this perception by transforming operations Batangas, Laguna and Quezon. our IT to drive innovation, operational excellence and cost-efficiency.” Even after operating for more than BUSINESS BENEFITS 100 years, Meralco continues to pursue “However, our traditional approach domestic and international growth was to run at least one server for every • Reduced IT implementation through investments and joint ventures. -

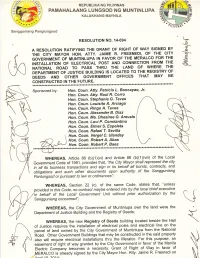

No.-14-094-Right-Of-Way-Meralco-For

REPUBLIKA NG PILIPINAS PAMAHALAANG LUNGSOD NG MUNTINLUPA KALAKHANG MAYNILA Sangguniang Panglungsod L: RESOLUTION NO. 14-094 -L A RESOLUTION RATIFYING THE GRANT OF RIGHT OF WAY SIGNED BY THE CITY MAYOR HON. ATTY. JAIME R. FRESNEDI, OF THE CITY -il GOVERNMENT OF MUNTINLUPA IN FAVOR OF THE MERALCO FOR THE s INSTALLATION OF ELECTRICAL POST AND CONNECTION FROM THE S- NATIONAL ROAD TO PASS THRU THE LAND OF WHERE THE (h DEPARTMENT OF JUSTICE BUILDING IS LOCATED TO THE REGISTRY OF DEEDS AND OTHER GOVERNMENT OFFICES THAT MAY BE CONSTRUCTED IN THE FUTURE. ***r(**r.*r,*************r,*******r,***rr****rr**r,********r,****r.***r,***r,**,.***,.****J'*************** Sponsored by: Hon. Coun. Atty. Patricio L. Boncayao, Jr. Hon. Coun. AttY. Raul R. Corro Hon. Coun. StePhanie G.IeYes Hon. Coun. Louisito A. Arciaga Hon. Coun. Ringo A. Teves Hon. Coun. Alexander B. Diaz Hon. Coun. Ma. Dhesiree G. Arevalo Hon. Coun. Luvi P. Constantino Hon. Coun. Elmer S. EsPelefa Hon. Coun. RafaelT. Sevilla Hon. Coun. Vergel C. UlandaY Hon. Coun. Robert A. Abas Hon. Coun. Robert P. Baes **r.*****rr******r(*****r(*************rr***r.************r.****,(***,.*****,'******** WHEREAS, Article 86 (b)(1)(vi) and Article 86 (b)(1)(viii) of the Local Government Code of 199'1, provides that, "the City Mayor shall represent the city in att its business fransactions and sign in its behalf all bonds, contracts, and obligations and such other documents upon authority of the Sangguniang Panlungsod or pursuant to law or ordinances"; WHEREAS, Section 22 (c), of the same Code, states that, -

Springer Geography

Springer Geography More information about this series at http://www.springer.com/series/10180 Yves Boquet The Philippine Archipelago Yves Boquet Département de Géographie Université de Bourgogne Dijon, France ISSN 2194-315X ISSN 2194-3168 (electronic) Springer Geography ISBN 978-3-319-51925-8 ISBN 978-3-319-51926-5 (eBook) DOI 10.1007/978-3-319-51926-5 Library of Congress Control Number: 2017930197 © Springer International Publishing AG 2017 This work is subject to copyright. All rights are reserved by the Publisher, whether the whole or part of the material is concerned, specifically the rights of translation, reprinting, reuse of illustrations, recitation, broadcasting, reproduction on microfilms or in any other physical way, and transmission or information storage and retrieval, electronic adaptation, computer software, or by similar or dissimilar methodology now known or hereafter developed. The use of general descriptive names, registered names, trademarks, service marks, etc. in this publication does not imply, even in the absence of a specific statement, that such names are exempt from the relevant protective laws and regulations and therefore free for general use. The publisher, the authors and the editors are safe to assume that the advice and information in this book are believed to be true and accurate at the date of publication. Neither the publisher nor the authors or the editors give a warranty, express or implied, with respect to the material contained herein or for any errors or omissions that may have been made. The publisher remains neutral with regard to jurisdictional claims in published maps and institutional affiliations. Printed on acid-free paper This Springer imprint is published by Springer Nature The registered company is Springer International Publishing AG The registered company address is: Gewerbestrasse 11, 6330 Cham, Switzerland Acknowledgements In loving memory of Mrs Josefina Labrador (1939-1977) This book would not exist without the warm welcome of my Filipino friends and colleagues. -

Meralco Sustainability Report 2019 Contents

Meralco Sustainability Report 2019 Contents About the Report 4 Message from the Chairman and President & CEO 5 One Meralco and Sustainability 10 Understanding What Matters 15 Engaging Stakeholders 17 One Meralco’s Contribution to the UN Sustainable Development Goals 20 One Meralco Sustainability Agenda 23 Power 24 Planet 39 People 56 Prosperity 65 Corporate Governance 76 Moving Forward 79 1 List of Abbreviations ADMS Advanced Distribution Management System AMI Advanced Metering Infrastructure BCDA Bases Conversion and Development Authority BCM Business Continuity Management Program BESS Battery Energy Storage System BFP Bureau of Fire Protection CAIDI Customer Average Interruption Duration Index CDC Clark Development Corporation CEDC Clark Electric Distribution Corporation CEO Chief Executive Officer CFZ Clark Freeport Zone CSEZ Clark Special Economic Zone CSO Chief Sustainability Officer CSP Competitive Selection Process CSR Corporate Social Responsibility CxTP Customer Experience Transformation Program DENR Department of Environment and Natural Resources DER Distributed Energy Resources DOE Department of Energy DOTr Department of Transportation DLSAU De La Salle Araneta University DU Distribution Utility EE Energy Efficiency Services EIA Environmental Impact Assessments EPC Engineering, Procurement and Construction Services ERC Energy Regulatory Commission ESH Environment, Safety and Health EV Electric Vehicle FLISR Fault Location, Isolation and Service Restoration GHG Greenhouse Gases GRI Global Reporting Initiative HELE High Efficiency, Low Emission HEP Household Electrification Program HFP High Fire Point HVAC Heating, Ventilation, and Air-Conditioning ICT Information and Communication Technology IVVO Integrated Volt-VAR Optimization LPIP Lightning Protection Improvement Program LGU Local Government Unit MEP Meralco Electrification Program MERALCO Manila Electric Company MGen Meralco Powergen Corporation MGREEN MGen Renewable Energy, Inc.