August 8, 2000

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Eulogio Rodriguez Jr. Ave, Pasig, 1604 Metro

The World's Property Search Starts Here C O N D O F O R R E N T Eulogio Rodriguez Jr. Ave, Bedrooms 1 Year Built 2017 Pasig, 1604 Metro Manila Bathrooms 1 Date Listed 11/28/2017 Pasig, Metro Manila Size 46 Sq Ft Listing ID GL-1511853657 Philippines Listed by: Property Owner Monthly Rent $700 For more information, visit: https://www.globallistings.com/3222181 Overview The Grove by Rockwell is a prestigious residential district in the center of the city. It continues to grow alongside Rockwell to provide residents a well-balanced lifestyle. Looking for a place to eat? The Retail Row offers great dining experience for your family, friends and neighbors, it features a wide variety of cafes and restaurants right before the entrance, including a convenience store, bank, and a grocery store to satisfy your needs. Looking for a place to exercise? We have a fully equipped gym and if you need guidance, our fitness instructors will assist you according to your workout to put you in peak condition. Some facilities available for an array of choices to enjoy your healthy routine such as our jogging paths, basketball courts, tennis courts and swimming pools. Rockwell is located at the center of Metro Manila, cities such as Mandaluyong, Makati and Ortigas are ease of convenience, especially going to shopping malls like Robinsons Galleria, SM Megamall, Tiendesitas, and Shangri-La and business and social districts like Eastwood City, Ortigas Center, Buendia and so on. for directions, the easiest path going to The Grove is to take the road in C5, if you're coming from the airport terminal, simply take a taxi (preferably Uber) and tell your driver to take the path all the way through at C5 until you get to The Grove. -

Origins There Is Not Enough Evidence to Assert What Conditions Gave Rise to the First Cities

City A city is a relatively large and permanent human settlement.[1][2] Although there is no agreement on how a city is distinguished from a town within general English language meanings, many cities have a particular administrative, legal, or historical status based on local law. Cities generally have complex systems for sanitation, utilities, land usage, housing, and transportation. The concentration of development greatly facilitates interaction between people and businesses, benefiting both parties in the process, but it also presents challenges to managing urban growth.[3] A big city or metropolis usually has associated suburbs and exurbs. Such cities are usually associated with metropolitan areas and urban areas, creating numerous business commuters traveling to urban centers for employment. Once a city expands far enough to reach another city, this region can be deemed aconurbation or megalopolis. Origins There is not enough evidence to assert what conditions gave rise to the first cities. However, some theorists have speculated on what they consider suitable pre- conditions, and basic mechanisms that might have been important driving forces. The conventional view holds that cities first formed after the Neolithic revolution. The Neolithic revolution brought agriculture, which made denser human populations possible, thereby supporting city development.[4] The advent of farming encouraged hunter-gatherers to abandon nomadic lifestyles and to settle near others who lived by agricultural production. The increased population-density encouraged by farming and the increased output of food per unit of land created conditions that seem more suitable for city-like activities. In his book, Cities and Economic Development, Paul Bairoch takes up this position in his argument that agricultural activity appears necessary before true cities can form. -

Starbucks at the Grove Robinsons Galleria Ortigas Ave MRT Station

Robinsons Galleria The Medical City Ortigas Ave MRT Station Starbucks at The Grove Tiendesitas SM Megamall SM Center Pasig Trusted by over 1 million members Try Scribd FREE for 30 days to access over 125 million titles without ads or interruptions! Start Free Trial Cancel Anytime. Trusted by over 1 million members Try Scribd FREE for 30 days to access over 125 million titles without ads or interruptions! Start Free Trial Cancel Anytime. Trusted by over 1 million members Try Scribd FREE for 30 days to access over 125 million titles without ads or interruptions! Start Free Trial Cancel Anytime. *Get to Robinsons Galleria -- MRTT: Get down at Ortigas AAve, then walk towards Rob Galleria (5-10 min walk) -- Bus: Ride the bus marked “Ortigas ILALIM”, ask the conductor to bring you down near Rob Galleria (5 min walk) Mini-Stop Robinsons Galleria Trusted by over 1 million members Try Scribd FREE for 30 days to access over 125 million titles without ads or interruptions! Start Free Trial Cancel Anytime. Trusted by over 1 million members Try Scribd FREE for 30 days to access over 125 million titles without ads or interruptions! Start Free Trial Cancel Anytime. *Transport from Robinsons Galleria -- TTaxi: Ride a taxi cab from taxi terminal in front of Mini-Stop -- Jeep: Walk towards Ortigas AAve, ride a jeep (ROSARIO) from jeep terminal underer the overpass (for lack of better words), tell the driver “IPI lang po” (P8) -- Bus: Walk towards Ortigas AAve, ride a bus (TAAYTAAY/ROSARIO/CAINTA) that will pass by Ortigas Ave, tell the driver “IPI lang po” (P8) Jeep terminal under the overpass Buses tend to stop in this spot Taxi terminal in front of Mini-Stop Trusted by over 1 million members Try Scribd FREE for 30 days to access over 125 million titles without ads or interruptions! Start Free Trial Cancel Anytime. -

The Case of the Pasig City Bus Service

Assessing the Implementation Arrangements for a City Bus Transport System through a Hybrid PPP Model: The Case of the Pasig City Bus Service Annelie LONTOCa, German AVENGOZAb, Nelson DOROYc, Giel Sabrine CRUZd, Alpher DE VERAe , Paolo MANUELf , Candice RAMOS g, ClairedeLune VILLANUEVA h a,b,c,d,e,f,g,h School of Urban and Regional Planning, University of the Philippines a E-mail: [email protected] b E-mail: [email protected] c E-mail: [email protected] d E-mail: [email protected] e E-mail: [email protected] f E-mail: [email protected] g E-mail: [email protected] h E-mail: [email protected] Abstract: The Ortigas Center is an important urban center in Metro Manila where its roads are often congested. Pasig City implemented a free bus service within Ortigas to address the need for public transportation. This Study assessed the implementation arrangements for a free bus service in Ortigas. The Study finds that there is a valid demand for the bus service as Ortigas is a key trip generator. However, the present free bus service is not financially viable. The Study shows that a fleet size fitted for demand will be more efficient than the current service. The Study finds that a Hybrid PPP Model for the bus service is more viable than a Pure PPP Model and the current arrangements. Both PPP Models will require the same institutional requirements such as a PPP Ordinance, the setting-up of a PPP Committee, and processes consistent with the awarding of local government contracts. Keywords: Local Public Transport Route Planning, Viability Assessment, PPP Bus Service 1. -

REGISTERED PET SHOPS (As of JANUARY 31, 2021) NO

BUREAU OF ANIMAL INDUSTRY - REGISTERED PET SHOPS (As of JANUARY 31, 2021) NO. REG NO. TRADE NAME BUSINESS ADDRESS NEW/ REGISTRATION VALIDITY REGION RENEWAL DATE 1 PTS - 0061 168 PET SHOP Gov. Alvarez Extension, Tetuan, Renewal 18-Jun-19 18-Jun-23 REGION IX Zamboanga City 2 PTS - 0135 3 BARKEETEERS PETSHOP Stall #4 Pet Village, Tiendesitas, Ugong, New 17-Dec-20 16-Dec-21 NCR Pasig City 3 PTS - 0100 ARJI’S PETSHOP 350 GSIS Street, Gitnang Bayan I, San Renewal 09-Jul-19 09-Jul-22 REGION IVA Mateo, Rizal 4 PTS – 0146 BARK ANG HUG PET SHOP Tiendesitas En Frontera Verde, Ugong, New 17-Dec-20 16-Dec-21 NCR Pasig City 5 PTS – 0147 BIG PAWS PET SHOP Tiendesitas En Frontera Verde, Ugong, New 17-Dec-20 16-Dec-21 NCR Pasig City 6 PTS - 0108 BIO RESEARCH, INC. CCB 43-B SM City North EDSA, Renewal 20-Jun-18 20-Jun-21 NCR North Avenue, Quezon City 7 PTS - 0118 BIO RESEARCH, INC. (SM #040-041A SM Megamall, Dona Vargas Renewal 12-Nov-18 12-Nov-21 NCR MEGAMALL) cor., EDSA, Mandaluyong City 8 PTS - 0126 BLESSETWIN PET SHOP GUITNANGBAYA, San Mateo , Rizal Renewal 03-Aug-20 03-Aug-23 REGION IVA 9 PTS – 0141 CANINE CREW Tiendesitas En Frontera Verde, Ugong, New 17-Dec-20 16-Dec-21 NCR PET SHOP Pasig City 10 PTS – 0142 CHATEAU PET SHOP Tiendesitas En Frontera Verde, Ugong, New 17-Dec-20 16-Dec-21 NCR Pasig City 11 PTS - 0060 CORNERSTONE ANIMAL HOSPITAL Jalandoni St., Jaro, Iloilo City Renewal 17-Oct-18 17-Oct-21 REGION VI AND VETERINARY SUPPLY 12 PTS - 0114 DAVAO PETCO CORPORATION SM Davao Ground Floor, Quimpo Renewal 26-Nov-19 25-Nov-22 REGION XI Boulevard, Ecoland, Davao City, Davao del Sur 13 PTS - 0124 DAVAO PETCO CORPORATION 2/F Abreeza Mall, JP Laurel Avenue, New 26-Nov-19 25-Nov-22 REGION XI (ABREEZA MALL) Bajada, Davao City 14 PTS - 0123 DAVAO PETCO CORPORATION SM Lanang Premier, Brgy. -

Domestic Branch Directory BANKING SCHEDULE

Domestic Branch Directory BANKING SCHEDULE Branch Name Present Address Contact Numbers Monday - Friday Saturday Sunday Holidays cor Gen. Araneta St. and Aurora Blvd., Cubao, Quezon 1 Q.C.-Cubao Main 911-2916 / 912-1938 9:00 AM – 4:00 PM City 912-3070 / 912-2577 / SRMC Bldg., 901 Aurora Blvd. cor Harvard & Stanford 2 Q.C.-Cubao-Harvard 913-1068 / 912-2571 / 9:00 AM – 4:00 PM Sts., Cubao, Quezon City 913-4503 (fax) 332-3014 / 332-3067 / 3 Q.C.-EDSA Roosevelt 1024 Global Trade Center Bldg., EDSA, Quezon City 9:00 AM – 4:00 PM 332-4446 G/F, One Cyberpod Centris, EDSA Eton Centris, cor. 332-5368 / 332-6258 / 4 Q.C.-EDSA-Eton Centris 9:00 AM – 4:00 PM 9:00 AM – 4:00 PM 9:00 AM – 4:00 PM EDSA & Quezon Ave., Quezon City 332-6665 Elliptical Road cor. Kalayaan Avenue, Diliman, Quezon 920-3353 / 924-2660 / 5 Q.C.-Elliptical Road 9:00 AM – 4:00 PM City 924-2663 Aurora Blvd., near PSBA, Brgy. Loyola Heights, 421-2331 / 421-2330 / 6 Q.C.-Katipunan-Aurora Blvd. 9:00 AM – 4:00 PM Quezon City 421-2329 (fax) 335 Agcor Bldg., Katipunan Ave., Loyola Heights, 929-8814 / 433-2021 / 7 Q.C.-Katipunan-Loyola Heights 9:00 AM – 4:00 PM Quezon City 433-2022 February 07, 2014 : G/F, Linear Building, 142 8 Q.C.-Katipunan-St. Ignatius 912-8077 / 912-8078 9:00 AM – 4:00 PM Katipunan Road, Quezon City 920-7158 / 920-7165 / 9 Q.C.-Matalino 21 Tempus Bldg., Matalino St., Diliman, Quezon City 9:00 AM – 4:00 PM 924-8919 (fax) MWSS Compound, Katipunan Road, Balara, Quezon 927-5443 / 922-3765 / 10 Q.C.-MWSS 9:00 AM – 4:00 PM City 922-3764 SRA Building, Brgy. -

List of Ecpay Cash-In Or Loading Outlets and Branches

LIST OF ECPAY CASH-IN OR LOADING OUTLETS AND BRANCHES # Account Name Branch Name Branch Address 1 ECPAY-IBM PLAZA ECPAY- IBM PLAZA 11TH FLOOR IBM PLAZA EASTWOOD QC 2 TRAVELTIME TRAVEL & TOURS TRAVELTIME #812 EMERALD TOWER JP RIZAL COR. P.TUAZON PROJECT 4 QC 3 ABONIFACIO BUSINESS CENTER A Bonifacio Stopover LOT 1-BLK 61 A. BONIFACIO AVENUE AFP OFFICERS VILLAGE PHASE4, FORT BONIFACIO TAGUIG 4 TIWALA SA PADALA TSP_HEAD OFFICE 170 SALCEDO ST. LEGASPI VILLAGE MAKATI 5 TIWALA SA PADALA TSP_BF HOMES 43 PRESIDENTS AVE. BF HOMES, PARANAQUE CITY 6 TIWALA SA PADALA TSP_BETTER LIVING 82 BETTERLIVING SUBD.PARANAQUE CITY 7 TIWALA SA PADALA TSP_COUNTRYSIDE 19 COUNTRYSIDE AVE., STA. LUCIA PASIG CITY 8 TIWALA SA PADALA TSP_GUADALUPE NUEVO TANHOCK BUILDING COR. EDSA GUADALUPE MAKATI CITY 9 TIWALA SA PADALA TSP_HERRAN 111 P. GIL STREET, PACO MANILA 10 TIWALA SA PADALA TSP_JUNCTION STAR VALLEY PLAZA MALL JUNCTION, CAINTA RIZAL 11 TIWALA SA PADALA TSP_RETIRO 27 N.S. AMORANTO ST. RETIRO QUEZON CITY 12 TIWALA SA PADALA TSP_SUMULONG 24 SUMULONG HI-WAY, STO. NINO MARIKINA CITY 13 TIWALA SA PADALA TSP 10TH 245- B 1TH AVE. BRGY.6 ZONE 6, CALOOCAN CITY 14 TIWALA SA PADALA TSP B. BARRIO 35 MALOLOS AVE, B. BARRIO CALOOCAN CITY 15 TIWALA SA PADALA TSP BUSTILLOS TIWALA SA PADALA L2522- 28 ROAD 216, EARNSHAW BUSTILLOS MANILA 16 TIWALA SA PADALA TSP CALOOCAN 43 A. MABINI ST. CALOOCAN CITY 17 TIWALA SA PADALA TSP CONCEPCION 19 BAYAN-BAYANAN AVE. CONCEPCION, MARIKINA CITY 18 TIWALA SA PADALA TSP JP RIZAL 529 OLYMPIA ST. JP RIZAL QUEZON CITY 19 TIWALA SA PADALA TSP LALOMA 67 CALAVITE ST. -

Mainstreaming Climate Risk Management and Planning for Resilience in the ENR Sector

Sendai + SDG – Covid 19 = Resilience Planning for Sustainable and Inclusive Growth By Elmer Mercado, EnP, fpiep 07 November 2020, 29th PIEP National Convention 5 Current and Future Global Urban Challenges (UN Habitat, 2009) Economic challenges ▪ impacts of global recession; unemployment/underemployment; ▪ increased in-migration to urban centers, increased poverty; ▪ increased pressure for social/economic/infrastructure services --- 2050 – global food crisis due to massive losses/conversion of arable lands into settlements or other uses (Int’l Institute of Population) and WATER --- loss of arable and open lands; rate of conversion of agricultural land in developing countries =5-7% (depending on aggregate increase in farmlands , i.e. conversion of forestlands to agriculture); Global ave = 2%; --rate of deforestation in the Philippines 100,000 hectares/yr. to give way to agricultural lands 5 Code Municipality Land Cover 2002 2012 Difference % 1 Arable land, crops mainly cereals and sugar 3,551.90 284.72 (3,267.18 Deforestation-92 1 Built-up areas 1,193.21 6,999.27 5,806.06) 487 1 Antipolo City Coconut plantations 505.75 367.25 (138.50) -27 Land 1 Cultivated area mixed with brushland/grassland Land 24,518.39 21,893.92 (2,624.47) -11 conversion Settlement1 Grassland, grass covering >70 percent conversion 2,972.47 4,977.45 2,004.98 67 Expansion1 Open canopy, mature trees covering < 50 percent 2,527.22 746.32 (1,780.9)1 -70Massive 2 Arable land, crops mainly cereals and sugar 2,151.11 257.35 (1,893.7)6 Deforestation-88 2 Baras Built-up areas -

Merchant Branch List

Merchant Branch List Anson’s at Landmark SM North Edsa Ayala Fairview Terraces Sta. Lucia East Grand Mall Makati SM Pasig Bonifacio High Street Sta. Lucia East Grand Mall - 2/F Trinoma SM Southmall Centrio Mall Tarlac SM Sucat Eastwood City Walk 1 Waltermart - Pampanga Sta. Lucia East Grand Mall Evia Applebee’s The 30th Mall Fairview Terraces Bonifacio Global City The District Imus Glorietta 3 Bizu Patisserie and Bistro Eastwood City Waltermart Greenbelt 3 Alabang Town Center Harbor Point Eastwood Mall Las Piñas Greenbelt 2 Arena The Bistro Group Marquee Mall Greenhills Promenade Alabang Town Center Baker and Cook Mckinley Hill Robinsons Magnolia SM City North EDSA Conrad Hotel Manila Robinsons Galleria St. Luke’s Global City UP Town Center Robinsons Place Manila Buffalo Wild Wings San Fernando Conrad SM Mall of Asia Black Canyon Coffee The Athlete’s Foot Estancia Mall Solenad Circuit Mall Abreeza Mall, Davao City Glorietta 2 Tomas Morato McKinley Hill Alabang Town Center Uptown Mall Trinoma Ayala Center Cebu Vista Mall Robinsons Place Manila Ayala Two Parkade, BGC Bruno’s Barbers Glorietta 2 Bulgogi Brothers Texas Roadhouse 30th Mall Glorietta 3 Alabang Town Center Uptown Mall Alabang Town Center Limketkai Mall, CDO Greenbelt 5 Conrad Ayala Center Cebu Marquee Mall, Angeles City Newport Mall Ayala Fairview Terraces Robinsons Bacolod SM Lanang Premier Tonkatsu by Terazawa Banawe Robinsons Dumaguete SM Mall of Asia Ayala Center Cebu Centrio Mall Robinsons Ermita Commonwealth Robinsons Galleria Denny’s Village Tavern Eastwood Robinsons Magnolia Trinoma Bonifacio High Street Central Festival Mall Robinsons Palawan Uptown Parade Fort Bonifacio Robinsons Pangasinan Vista Mall Watami Gateway Mall Robinsons Tacloban Greenbelt 2 Glorietta 3 Sta. -

Terms and Conditions

Terms and Conditions 1. The Promo (“Promo”) will run from August 24 to October 31, 2020 (“Promo Period”): Registration Period: August 24 to October 30, 2020 Spend Period: August 25 to October 31, 2020 Redemption Period: September 9, 2020 to December 31, 2020 2. The Promo is open to Principal cardholders of Citi Credit Cards (“Card”) that have been locally issued by Citibank, N.A. Philippine Branch (“Citi”), which are active and in good credit standing, have available credit limit; who have registered valid and updated mobile number and email address with Citibank; who received an SMS and/or email from Citibank regarding the particular promo requirement; and who are not prohibited under applicable Gifts, Anti-Bribery and Corruption laws, regulations, and policies from participating in and/or qualifying for this Promo (“Cardholder”). Incumbent government officials or employees, whether elected or appointed, corporate account and US persons (i.e., a citizen or lawful resident, green card holder of the United States of America) are not eligible to participate in this Promo. 3. It is the responsibility of the Cardholder to update his/her contact information with Citibank by calling CitiPhone at (02) 8995-9999. Cardholders whose contact information in Citibank’s records are not updated, who have the same mobile/phone number or email address as another cardholder in Citi records, who have multiple customer numbers, or who have opted out of receiving marketing communications from Citi based on Citi system records, and new Cardholders (whose credit card account was opened and activated from August 1, 2020 onwards) will not receive the communication about the promotion. -

REGISTERED PET SHOPS (As of DECEMBER 31, 2020) NO

BUREAU OF ANIMAL INDUSTRY - REGISTERED PET SHOPS (As of DECEMBER 31, 2020) NO. REG NO. TRADE NAME BUSINESS ADDRESS NEW/ REGISTRATION VALIDITY REGION RENEWAL DATE 1 PTS - 0061 168 PET SHOP Gov. Alvarez Extension, Tetuan, Renewal 18-Jun-19 18-Jun-23 REGION IX Zamboanga City 2 PTS - 0135 3 BARKEETEERS PETSHOP Stall #4 Pet Village, Tiendesitas, Ugong, 17-Dec-20 16-Dec-21 NCR Pasig City 3 PTS - 0100 ARJI’S PETSHOP 350 GSIS Street, Gitnang Bayan I, San Renewal 09-Jul-19 09-Jul-22 REGION IVA Mateo, Rizal 4 PTS – 0146 BARK ANG HUG PET SHOP Tiendesitas En Frontera Verde, Ugong, New 17-Dec-20 16-Dec-21 NCR Pasig City 5 PTS – 0147 BIG PAWS PET SHOP Tiendesitas En Frontera Verde, Ugong, New 17-Dec-20 16-Dec-21 NCR Pasig City 6 PTS - 0108 BIO RESEARCH, INC. CCB 43-B SM City North EDSA, Renewal 20-Jun-18 20-Jun-21 NCR North Avenue, Quezon City 7 PTS - 0118 BIO RESEARCH, INC. (SM #040-041A SM Megamall, Dona Vargas Renewal 12-Nov-18 12-Nov-21 NCR MEGAMALL) cor., EDSA, Mandaluyong City 8 PTS - 0126 BLESSETWIN PET SHOP GUITNANGBAYA, San Mateo , Rizal Renewal 03-Aug-20 03-Aug-23 REGION IVA 9 PTS – 0141 CANINE CREW Tiendesitas En Frontera Verde, Ugong, New 17-Dec-20 16-Dec-21 NCR PET SHOP Pasig City 10 PTS – 0142 CHATEAU PET SHOP Tiendesitas En Frontera Verde, Ugong, New 17-Dec-20 16-Dec-21 NCR Pasig City 11 PTS - 0060 CORNERSTONE ANIMAL HOSPITAL Jalandoni St., Jaro, Iloilo City Renewal 17-Oct-18 17-Oct-21 REGION VI AND VETERINARY SUPPLY 13 PTS - 0114 DAVAO PETCO CORPORATION SM Davao Ground Floor, Quimpo Renewal 26-Nov-19 25-Nov-22 REGION XI Boulevard, Ecoland, Davao City, Davao del Sur 14 PTS - 0124 DAVAO PETCO CORPORATION 2/F Abreeza Mall, JP Laurel Avenue, New 26-Nov-19 25-Nov-22 REGION XI (ABREEZA MALL) Bajada, Davao City 15 PTS - 0123 DAVAO PETCO CORPORATION SM Lanang Premier, Brgy. -

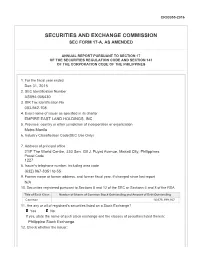

Securities and Exchange Commission Sec Form 17-A, As Amended

CR03055-2016 SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A, AS AMENDED ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF THE CORPORATION CODE OF THE PHILIPPINES 1. For the fiscal year ended Dec 31, 2015 2. SEC Identification Number AS094-006430 3. BIR Tax Identification No. 003-942-108 4. Exact name of issuer as specified in its charter EMPIRE EAST LAND HOLDINGS, INC. 5. Province, country or other jurisdiction of incorporation or organization Metro Manila 6. Industry Classification Code(SEC Use Only) 7. Address of principal office 21/F The World Centre, 330 Sen. Gil J. Puyat Avenue, Makati City, Philippines Postal Code 1227 8. Issuer's telephone number, including area code (632) 867-8351 to 55 9. Former name or former address, and former fiscal year, if changed since last report N/A 10. Securities registered pursuant to Sections 8 and 12 of the SRC or Sections 4 and 8 of the RSA Title of Each Class Number of Shares of Common Stock Outstanding and Amount of Debt Outstanding Common 14,676,199,167 11. Are any or all of registrant's securities listed on a Stock Exchange? Yes No If yes, state the name of such stock exchange and the classes of securities listed therein: Philippine Stock Exchange 12. Check whether the issuer: (a) has filed all reports required to be filed by Section 17 of the SRC and SRC Rule 17.1 thereunder or Section 11 of the RSA and RSA Rule 11(a)-1 thereunder, and Sections 26 and 141 of The Corporation Code of the Philippines during the preceding twelve (12) months (or for such shorter period that the registrant was required to file such reports) Yes No (b) has been subject to such filing requirements for the past ninety (90) days Yes No 13.