1 in the High Court of Karnataka at Bangalore

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

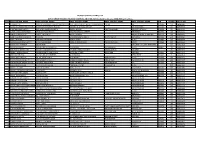

Slno First Holder Name

MURUDESHWAR CERAMICS LTD LIST OF SHARE HOLDERS HOLIDNG SHARES AS ON 07.08.2020 Dividend for the year 2008-2009 with address SLNO FIRST_HOLDER_NAME FIRST_HOLDER_ADDR1 FIRST_HOLDER_ADDR2 FIRST_HOLDER_ADDR3 FIRST_HOLDER_ADDR4 PIN SHARES FOLIO NO 1 A RAMADEVI C/O A V SUBBARAO DEPUTY DIRECTOR OF INDDIST. INDU.CENTRE WEST GODAVARI DIST ELURU A P 534006 150 AE00322 2 ASWATHA NARAYANA RAO N S ASWATHA NARAYANA RAO N S ADVOCATE II CROSS JCR EXT CHITRADURGA 577501 20 AM00008 3 A AJITHKUMAR SHETTY S/O LATE K RAJEEVA SHETTY ASODU HOUSE POST SAWWADY KUNDAPUR TALUK 576222 50 AM00026 4 ALTAF A KHAN M PATHAN NEAR KCC BANK ROAD SHALIBANMAKAN STREET DHARWAD 580001 100 AM00030 5 AMINUDDIN GOUDA GOUSE MOHALLA MURDESHWAR MURDESHWAR TQBHATKAL 581350 100 AM00032 6 ABID HUSAIN M JAMADAR IV CROSS SAVANM NAWAB PLOTS NARAYANPUR DHARWAD 580006 650 AM00042 7 ABDUL H KHAN 145 RENUKA NAGAR GOKUL ROAD HUBLI 580030 150 AM00057 8 ARUN NARASIMHA SHETTY KONKI BADAMANE NADA GUDDEANGADI TQ KUNDAPURA UDUPI 576262 500 AM00081 9 ARVINDRAO BHIKKOJI MISHRIKOTI KALGHATGI TQ DIST DHARWAR 100 AM00103 10 ASHOK V MAHALE ARADHANA APARTMENTS BLOCK NO 3 VIDYANAGAR HUBLI 580021 18 AM00110 11 ANURADHA BHARATAN NO.20 A ASHWINI FLATS II FLOOR ZAKRIA COLONY CHOOLAIMEDU CHENNAI 25 AM00116 12 ABIDA Y AGBOATWALA MADNI MANOR 2ND FLOOR MOTLIBAI STREET AGRIPADA MUMBAI 400011 100 AM00117 13 ABHINAV KHOSLA 200 NILGIRI APPRTMENTS ALAKNANDA NEW DELHI 110019 2 AM00151 14 ANANTRAJ LENGADE METAL MERCHANTS M G MARKET DURGAD BAIL HUBLI 580020 100 AM00172 15 A S NARASIMHA SHETTY S/O MANJAYYA SHETTY SHRIDEVI -

Pricelist As on For

KSBCL - PRICE LIST Disclaimer: Prices are liable to change without Notice. TO SELECT AN ITEM For se arch (i) Press Ctrl+F (ii) Type item name or item code (iii) Press enter Then view the selected item KARNATAKA STATE BEVERAGES CORPORATION LIMITED SUPPLIER-WISE AND ITEM-WISE PRICE LIST AS OF 1ST NOVEMBER-2012 KSBCL MRP Item Names Item Code Wef Landed Selling Per Btl. Cost Price A.J Distilleries D.K (0064) A J Dry Gin 180 Ml (0064) 00640400104 16/04/2009 1334.88 YET TO PRICE A J Dry Gin 375 Ml (0064) 00640400102 16/04/2009 1377.00 YET TO PRICE A J Dry Gin 750 Ml (0064) 00640400101 16/04/2009 1377.00 YET TO PRICE Aj Xxx Rum 180 Ml (0064) 00640300104 16/04/2009 1334.88 YET TO PRICE Aj Xxx Rum 375 Ml (0064) 00640300102 16/04/2009 1377.00 YET TO PRICE Aj Xxx Rum 750 Ml (0064) 00640300101 16/04/2009 1377.00 YET TO PRICE S.K.Deluxe Whisky-N 180 Ml (0064) 00640100804 16/04/2009 1334.88 YET TO PRICE S.K.Deluxe Whisky-N 375 Ml (0064) 00640100802 16/04/2009 1377.00 YET TO PRICE S.K.Deluxe Whisky-N 750 Ml (0064) 00640100801 16/04/2009 1377.00 YET TO PRICE ABInBev India Pvt Ltd (0461) Hoegaarden Beer 330ML(0461) 04610900311 25/10/2012 4016.30 4036.40 185.00 Leffe Beer 330ML(0461) 04610900211 25/10/2012 4016.30 4036.40 185.00 Stella Artois Premium Lager Beer 330ML(0461) 04610900111 25/10/2012 3198.50 3214.50 147.33 Ace Beveragez Pvt Ltd (0388) Alamos Chardonnay 750ML(0388) 03880700301 31/03/2009 12701.76 YET TO PRICE Alamos Chardonnay-DF 750ML(0388) 03880750301 31/03/2009 8434.08 YET TO PRICE Alamos Malbec 750ML(0388) 03880700401 31/03/2009 12701.76 -

Draft Due Diligence Cum Resettlement Plan

Draft Due Diligence cum Resettlement Plan Project Number: 53326-001 September 2020 India: Bengaluru Metro Rail Project Phase 2A Outer Ring Road Silk Board to K.R. Puram Prepared by the Bangalore Metro Rail Corporation Limited for the Asian Development Bank. CURRENCY EQUIVALENTS (as of 8 Septemer 2020) Currency Unit – Indian Rupee (INR) USD1.00 = INR 73.4270 ABBREVIATIONS ADB Asian Development Bank BDA Bengaluru Development Authority BBMP Bruhat Bengaluru Mahanagara Palike BMTC Bangalore Metropolitan Transport Corporation BMRCL Bangalore Metro Rail Corporation Limited BPL Below Poverty Line CRP Compensation and Resettlement Package GoK Government of Karnataka KIADA Karnataka Industrial Areas Development Act KIADB Karnataka Industrial Areas Development Board ORR Outer Ring Road RMV Recommended Market Value NOTE (i) The fiscal year (FY) of the Government of India ends on 31 March. FY before a calendar year denotes the year in which the fiscal year ends, e.g., FY2020 ends on 31 March 2020. (ii) In this report, "$" refers to US dollars This Draft Due Diligence cum Resettlement Plan is a document of the borrower. The views expressed herein do not necessarily represent those of ADB's Board of Directors, Management, or staff, and may be preliminary in nature. Your attention is directed to the “terms of use” section on ADB’s website. In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area. -

Gurdaspur Punjab Kings Whisky 180 35 2 Ab Grains Spirits Pvt

Sr. No. WHOLESALE_VEND_NAME BRAND_NAME SIZE_CODE MRP 1 AB GRAINS SPIRITS PVT. LTD. - GURDASPUR PUNJAB KINGS WHISKY 180 35 2 AB GRAINS SPIRITS PVT. LTD. - GURDASPUR PUNJAB KINGS WHISKY 375 65 3 AB GRAINS SPIRITS PVT. LTD. - GURDASPUR PUNJAB KINGS WHISKY 750 130 4 ALCOBREW DIST (I) PVT LTD. - DERABASSI AUBERGE PREMIUM VODKA GR APPLE 180 100 5 ALCOBREW DIST (I) PVT LTD. - DERABASSI AUBERGE PREMIUM VODKA GR APPLE 375 200 6 ALCOBREW DIST (I) PVT LTD. - DERABASSI AUBERGE PREMIUM VODKA GR APPLE 750 400 7 ALCOBREW DIST (I) PVT LTD. - DERABASSI OLD SMUGGLER BL SCOTCH WHISKY 750 1050 8 ALCOBREW DIST (I) PVT LTD. - DERABASSI OLD SMUGL. XXX MATURED RUM 180 60 9 ALCOBREW DIST (I) PVT LTD. - DERABASSI OLD SMUGL. XXX MATURED RUM 375 120 10 ALCOBREW DIST (I) PVT LTD. - DERABASSI OLD SMUGL. XXX MATURED RUM 750 240 11 ALCOBREW DIST (I) PVT LTD. - DERABASSI WHITE & BLUE PREMIUM WHISKY 180 100 12 ALCOBREW DIST (I) PVT LTD. - DERABASSI WHITE & BLUE PREMIUM WHISKY 375 205 13 ALCOBREW DIST (I) PVT LTD. - DERABASSI WHITE & BLUE PREMIUM WHISKY 750 410 14 ALLIED BLEND&DIST P LTD - AURANGABAD WODKA GORB. VODKA GREEN APPLE 180 145 15 ALLIED BLEND&DIST P LTD - AURANGABAD WODKA GORB. VODKA GREEN APPLE 750 580 16 ALLIED BLEND&DIST P LTD - AURANGABAD WODKA GORB. VODKA ORANGE 180 145 17 ALLIED BLEND&DIST P LTD - AURANGABAD WODKA GORB. VODKA ORANGE 750 580 18 ALLIED BLEND&DIST P LTD - AURANGABAD WODKA GORBATSCHOW VODKA 60 45 19 ALLIED BLEND&DIST P LTD - AURANGABAD WODKA GORBATSCHOW VODKA 90 70 20 ALLIED BLEND&DIST P LTD - AURANGABAD WODKA GORBATSCHOW VODKA 180 135 21 ALLIED BLEND&DIST P LTD - AURANGABAD WODKA GORBATSCHOW VODKA 375 275 22 ALLIED BLEND&DIST P LTD - AURANGABAD WODKA GORBATSCHOW VODKA 750 550 23 A-ONE WINERIES - SANGRUR ORIGINAL CH RARE DEL WHISKY 180 50 24 A-ONE WINERIES - SANGRUR ORIGINAL CH RARE DEL WHISKY 375 100 25 A-ONE WINERIES - SANGRUR ORIGINAL CH RARE DEL WHISKY 750 200 26 BACARDI INDIA PRIVATE LTD. -

C M R INSTITUTE of TECHNOLOGY #132, AECS Layout, ITPL Main Road, Kundalahalli, BENGALURU-560037 JULY - 2020

A PROJECT REPORT (18MBAPR407) on the Topic A Study on Impact of Consumer Perception towards Online Shopping in Flipkart By Mr. Nithin Kumar C USN: 1CR18MBA31 MBA 4th Semester Submitted to VISVESVARAYA TECHNOLOGICAL UNIVERSITY, BELAGAVI in partial fulfillment of the requirements for the award of the degree of MASTER OF BUSINESS ADMINISTRATION Under the Guidance of INTERNAL GUIDE EXTERNAL GUIDE Mr. Kathari Santosh Mr. Arnav Ghosh Asst Professor, Dept of MBA Sr. Manager Flipkart Internet Pvt Ltd CMRIT Bangalore Bangalore DEPARTMENT OF MASTER OF BUSINESS ADMINISTRATION C M R INSTITUTE OF TECHNOLOGY #132, AECS Layout, ITPL Main Road, Kundalahalli, BENGALURU-560037 JULY - 2020 A PROJECT REPORT (18MBAPR407) on the Topic A Study on Impact of Consumer Perception towards Online Shopping in Flipkart By Mr. Nithin Kumar C USN: 1CR18MBA31 MBA 4th Semester Submitted to VISVESVARAYA TECHNOLOGICAL UNIVERSITY, BELAGAVI in partial fulfillment of the requirements for the award of the degree of MASTER OF BUSINESS ADMINISTRATION Under the Guidance of INTERNAL GUIDE EXTERNAL GUIDE Mr. Kathari Santosh Mr. Arnav Ghosh Asst Professor, Dept of MBA Sr. Manager Flipkart Internet Pvt Ltd CMRIT Bangalore Bangalore DEPARTMENT OF MASTER OF BUSINESS ADMINISTRATION C M R INSTITUTE OF TECHNOLOGY #132, AECS Layout, ITPL Main Road, Kundalahalli, BENGALURU-560037 JULY - 2020 ACKNOWLEDGEMENT I have been fortunate enough to get good timely advice and support from a host of people to whom I shall remain grateful. I take this opportunity to express my heartfelt thanks to Dr. Sanjay Jain, Principal, CMR Institute of Technology, Bangalore, for his support and cooperation to undertake and complete the project work. -

Annual Report 2018 2DIAGEO ANNUAL REPORTDIAGEO 2018 ANNUAL REPORT 2018

Annual Report 2018 2DIAGEO ANNUAL REPORTDIAGEO 2018 ANNUAL REPORT 2018 Our performance 2018 Financial Non-financial Volume (equivalent units EU) Net sales(i) Alcohol in society 2018 EU240.4m 2018 £12,163m 2018 225 2017 EU242.2m 2017 £12,050m 2017 264 Reported movement 0.7% Reported movement 0.9% Number of responsible drinking programmes Organic movement 2.5% Organic movement 5.0% Operating profit Net cash from operating activities Health and safety 2018 £3,691m 2018 £3,084m 2018 1.00Δ 2017 £3,559m 2017 £3,132m 2017 1.14 Reported movement 3.7% 2018 decrease of £48m Lost time accident frequency(iv) Organic movement 7.6% 2018 free cash flow(ii) £2,523m £140m Earnings per share (eps) Total recommended dividend per share(iii) Water efficiency(v) 2018 121.7p 2018 65.3p 2018 4.94I/IΔ 2017 106.0p 2017 62.2p 2017 4.98I/I Reported movement 14.8% 5% Eps before exceptional items movement (ii) 9.3% (i) Net sales are sales less excise duties. (ii) See definitions and reconciliations on pages 56-61. (iii) Includes recommended final dividend of 40.4p. (iv) Per 1,000 full-time employees. (v) Data for the year ended 30 June 2017 has been restated in accordance with Diageo’s environmental reporting methodologies. Δ Within PwC’s independent limited assurance scope. For further detail and the reporting methodologies, see our Sustainability & Responsibility Performance Addendum 2018. Performance by region 2018 North America Europe Africa Latin America Asia Pacific and Turkey and Caribbean Volume (equivalent units) EU48.2m EU46.3m EU33.2m EU22.2m EU90.5m Reported -

Download Download

International Journal of Advanced Science and Technology Vol. 29, No. 4s, (2020), pp. 3205-3220 ` Consumer Preferences for Domestic Wines in Delhi-N.C.R. Region 1MohitMalik, 2Dr. Apeksha Bhatnagar, 3Dr. JaswinderKumar 1Research Scholar, Amity University Jaipur Rajasthan. 2Asistant Prof, Amity University Jaipur Rajasthan. 3Asistant Prof. Panjab University Chandigarh Abstract In India the wine market is in a formative process. Wine is considered a refined beverage and in reality considered safer than other alcoholic beverages like Whiskey, Vodka, and Rum etc. Even among women and the young starters this element has made it famous. Drinking wine is a growing trend in India. Drinking wine is no longer viewed as a bad topic by customers. This research aims to establish a deeper picture of the consumer preferences in Delhi for domestic wine. The research was conducted through a method of questionnaire surveys in NCR's Delhi and tri-city areas. Online survey approaches gather quantitative data consisting of standardized questions that are only aimed at Delhi-NCR wine customers and evaluated using SPSS 16.A total of 149 customers were surveyed about their preferences of domestic wine and purchasing behaviour. This paper finds out that India's wine industry is largely informal and at a nascent stage of production. Wine producers can enhance their efforts in wine-making by understanding emerging technologies and market demands. Strategies for regional business growth will help encourage domestic wine and often concentrate on the application of -

Confluence of Faith Begins with Shahi Snan

Follow us on: facebook.com/dailypioneer RNI No.2016/1957, REGD NO. SSP/LW/NP-34/2019-21 @TheDailyPioneer instagram.com/dailypioneer/ Established 1864 OPINION 8 Published From AVENUES 10 WORLD 13 DELHI LUCKNOW BHOPAL A FRACTURED PURSUE BLOGGING AS A TERRORISTS ATTACK BHUBANESWAR RANCHI RAIPUR NEGOTIATION MAINSTREAM CAREER NAIROBI HOTEL CHANDIGARH DEHRADUN Late City Vol. 155 Issue 15 LUCKNOW, WEDNESDAY JANUARY 16, 2019; PAGES 16 `3 *Air Surcharge Extra if Applicable INDIA BEAT AUSTRALIA BY SIX} WICKETS } 15 SPORT www.dailypioneer.com Confluence of faith begins with Shahi Snan PNS n ALLAHABAD congregation in the world, were move about naked with ash the first to take the holy bath smeared on their whole body. umbh, the mega spiritual known as ‘Shahi Snan’. They “It is surreal. I had always Kevent, kicked off to a splen- marched majestically, dancing heard about them. In fact, one of did start as auspicious Makar and humming devotional songs, the reasons we wanted to come Sankranti dawned upon the all the way to the confluence. to the Kumbh was to see them sangam, the confluence of holy “Me and my family came around in real as we are told that this is Ganga, Yamuna and mytholog- 4:30 am thinking that it will be the only festival in which they ical Saraswati. Amid chants of too crowded later. arrive in numbers,” said Manuel ‘Har Har Gange’, thousands of “Not that it is any less crowd- Matthaus, who had come from seers, lakhs of devotees took a ed now. Also, we didn’t want to Germany. -

Four Seasons Wines Ltd. Four Seasons CLASSICS Cabernet Sauvignon Red 1.97 1740.52 883.51 Wine(750) Four Seasons Wines Ltd

EXCISE DUTY ON WINE (2019-2020) Supplier Name Label Name Per Case Per LPL Quantity Excise Duty Excise Duty in LPL (Specific (Specific Component Component + Ad + Ad Valorem) Valorem) Four Seasons Wines Ltd. Four Seasons CLASSICS Cabernet Sauvignon Red 1.97 1740.52 883.51 Wine(750) Four Seasons Wines Ltd. Four Seasons CLASSICS Sauvignon Blanc White 1.97 1622.44 823.57 Wine(750) Four Seasons Wines Ltd. John Exshaw Premium Sweet Red Wine(750) 2.21 1081.19 489.23 Fratelli Wines Pvt. Ltd. Fratelli Cabernet Franc Shiraz(375) 1.97 2435.03 1236.06 Fratelli Wines Pvt. Ltd. Fratelli Cabernet Franc Shiraz(750) 1.97 2206.23 1119.91 Fratelli Wines Pvt. Ltd. Fratelli Cabernet Franc Shiraz(750)-(DEF) 1.97 1544.36 783.94 Fratelli Wines Pvt. Ltd. Fratelli Chardonnay(750) 1.97 2643.83 1342.05 Fratelli Wines Pvt. Ltd. Fratelli Classic Chenin(375) 1.89 1920.76 1016.28 Fratelli Wines Pvt. Ltd. Fratelli Classic Chenin(750) 1.89 1795.96 950.24 Fratelli Wines Pvt. Ltd. Fratelli Classic Merlot(375) 1.89 2066.36 1093.31 Fratelli Wines Pvt. Ltd. Fratelli Classic Merlot(750) 1.89 2003.96 1060.3 Fratelli Wines Pvt. Ltd. Fratelli Classic Merlot(750)-(DEF) 1.89 1402.77 742.21 Fratelli Wines Pvt. Ltd. Fratelli Classic Shiraz(375) 1.89 1920.76 1016.28 Fratelli Wines Pvt. Ltd. Fratelli Classic Shiraz(750) 1.89 1795.96 950.24 Fratelli Wines Pvt. Ltd. Fratelli Gran Cuvee Brut(750) 1.89 3461.16 1831.3 Fratelli Wines Pvt. Ltd. Fratelli Merlot(750) 1.97 2955.43 1500.22 Fratelli Wines Pvt. -

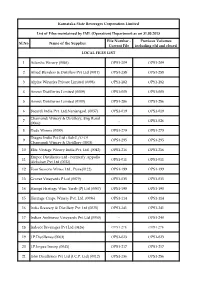

Sl.No Name of the Supplier File Number

Karnataka State Beverages Corporation Limited List of Files maintained by IML (Operation) Department as on 31.03.2013 File Number - Previous Volumes Sl.No Name of the Supplier Current File including old and closed LOCAL FILES LIST 1 Adarsha Winery (0046) OPS1-209 OPS1-209 2 Allied Blenders & Distillers Pvt Ltd (0011) OPS1-258 OPS1-258 3 Alpine Wineries Private Limited (0098) OPS1-282 OPS1-282 4 Amrut Distilleries Limited (0009) OPS1-005 OPS1-005 5 Amrut Distilleries Limited (0100) OPS1-286 OPS1-286 6 Bacardi India Pvt. Ltd,Nanjangud. (0057) OPS1-019 OPS1-019 Chamundi Winery & Distillery, Bng Rural 7 - OPS1-026 (0066) 8 Dada Winers (0099) OPS1-279 OPS1-279 Diageo India Pvt Ltd - Sub L/O Of 9 OPS1-295 OPS1-295 Chamundi Winery & Distillery (0503) 10 Elite Vintage Winery India Pvt. Ltd. (0042) OPS1-216 OPS1-216 Empee Distilleries Ltd - Formerly Appollo 11 OPS1-011 OPS1-011 Alchobev Pvt Ltd (0022) 12 Four Seasons Wines Ltd., Pune(0122) OPS1-199 OPS1-199 13 Grover Vineyards P Ltd (0079) OPS1-035 OPS1-035 14 Hampi Heritage Wine Yards (P) Ltd (0047) OPS1-198 OPS1-198 15 Heritage Grape Winery Pvt. Ltd. (0096) OPS1-114 OPS1-114 16 India Brewery & Distillery Pvt Ltd (0025) OPS1-241 OPS1-241 17 Indian Ambience Vineyards Pvt Ltd (0030) - OPS1-240 18 Indscot Beverages Pvt Ltd (0416) OPS1-278 OPS1-278 19 J.P.Distilleries (0063) OPS1-023 OPS1-023 20 J.P.Impex Incorp (0043) OPS1-217 OPS1-217 21 John Distilleries Pvt Ltd (I.C.P. Ltd) (0012) OPS1-256 OPS1-256 22 John Distillery Pvt Ltd (0067) OPS1-027 OPS1-027 Kalpatharu Breweries & Distilleries Pvt Ltd 23 OPS1-244 OPS1-244 (0024) 24 Khoday Breweries Ltd (Dist. -

United Spirits Limited Registered Office : ‘UB Tower’, #24, Vittal Mallya Road, Bangalore - 560 001

United Spirits Limited Registered Office : ‘UB Tower’, #24, Vittal Mallya Road, Bangalore - 560 001 NOTICE IS HEREBY GIVEN OF THE ELEVENTH ANNUAL GENERAL MEETING of the Company to be held at Good Shepherd Auditorium, Opposite St. Joseph’s Pre-University College, Residency Road, Bangalore – 560 025 on Wednesday, September 29, 2010 at 11.00 a.m. for the following purposes: 1. To receive and consider the accounts for the year ended March 31, 2010 and the reports of the Auditors and Directors thereon; 2. To declare dividend on Equity Shares; 3. To elect a Director in the place of Mr. Subhash Raghunath Gupte, who retires by rotation and being eligible, offers himself for re-appointment; 4. To elect a Director in the place of Mr. Sudhindar Krishan Khanna, who retires by rotation and being eligible, offers himself for re-appointment; 5. To appoint Auditors and fix their remuneration; 6. Commission to Directors To consider and if thought fit, to pass with or without modification, the following Resolution as a Special Resolution: RESOLVED that the Company’s Directors other than a Managing Director or Director(s) in the wholetime employment of the Company, be paid every year a remuneration not exceeding one percent of the net profits of the Company, which amount they may apportion among themselves in any manner they deem fit, in addition to sitting fees, if any payable to each Director for every Meeting of the Board or Committee thereof attended by him/her, and that this Resolution remain in force for a period of five years from April 1, 2011. -

Part a Industry Profile

Part A Industry profile Company profile Mission and Quality statement Mission Statement We constitute a large, global group based in India. We associate with world leaders in order to adopt technologies and processes that will enable a leadership position in a large spectrum of activities. We are focused on assuming leadership in all our target markets. We seek to be the most preferred employer wherever we operate. We recognize that our organization is built around people who are our most valuable asset. We will always be the partner of choice for customers, suppliers and other creators of innovative concepts. We will continually increase the long-term value of our Group for the benefit of our shareholders. We will operate as a decentralized organization and allow each business to develop within our stated values. We will be a major contributor to our National Economy and take full advantage of our strong resource base. We commit ourselves to the ongoing mission of achieving Scientific Excellence. Quality leadership is vital to the long-term success of the UB Group in an increasingly competitive marketplace. Building quality into our workplace, products and service is essential to a successful future for our customers, employees, supplier¶s communities and shareholders. The UB Group will work to provide products and services that always meet or exceed expectations Management will commit resources and create an environment in which each employee can contribute skills, talents and ideas to a never-ending process of improvement and innovation in all aspects of our business. Quality statement Quality leadership is vital to the long-term success of the UB Group in an increasingly competitive marketplace.