ANNUAL REPORT Annual Report for the Financial Year Ended 31 December 2014

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Iproperty Group Limited ABN 99 126 188 538 Appendix 4E Preliminary Financial Report

iProperty Group Limited ABN 99 126 188 538 Appendix 4E Preliminary Financial Report “Results for announcement to the Market.” Information for the year ended 31 December 2014 given to ASX under listing rule 4.3A Key iProperty Group information 2014 2013 Year ended 31 December $000 $000 Change Revenues from ordinary operations 21,836 19,046 15% Profit/(Loss) from ordinary activities after tax attributable to members (10,731) 1,706 (729%) Profit/(Loss) after tax attributable to members (10,731) 1,706 (729%) Cents Cents Profit/(Loss) per Share (basic) (5.91) 0.94 (729%) Profit/(Loss) per Share (diluted) (5.90) 0.94 (728%) NTA per Share 4.58 5.52 (19%) Dividends iProperty Group Limited does not propose to pay a dividend for this reporting period (2013: nil). Basis of this report This report includes the attached audited financial statements of iProperty Group Limited and controlled entities (iProperty) for the year ended 31 December 2014. Together these documents contain all information required by Appendix 4E of the Australian Securities Exchange Listing Rules. It should be read in conjunction with iProperty’s Annual Report when released, and is lodged with the Australian Securities Exchange under listing rule 4.3A. For and on behalf of the Board Patrick Grove Chairman 19 February 2015 iProperty Group Limited And Controlled Entities iProperty Group Limited ABN 99 126 188 538 Audited Financial Statements for the financial year ended 31 December 2014 iProperty Group Limited And Controlled Entities Index Contents Page Directors’ Report 2 Auditor’s -

Icar Asia Limited and Controlled Entities ACN 157 710 846

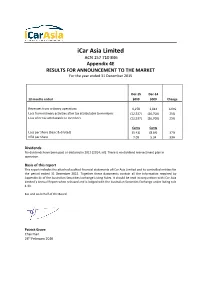

iCarAsiaLimited ACN157710846 Appendix4E RESULTSFORANNOUNCEMENTTOTHEMARKET Fortheyearended31December2014 Dec14 Dec13 12monthsended $000 $000 Change Revenuesfromordinaryoperations 2,814 1,446 95% Lossfromordinaryactivitiesaftertaxattributabletomembers (16,700) (6,902) (142%) Lossaftertaxattributabletomembers (16,700) (6,902) (142%) Cents Cents LossperShare(basic&diluted) (8.64) (4.10) (111%) NTAperShare 5.34 5.94 (10%) Dividends Nodividendshavebeenpaidordeclaredin2014(2013:nil).Thereisnodividendreinvestmentplanin operation. Basisofthisreport ThisreportincludestheattachedauditedfinancialstatementsofiCarAsiaLimitedanditscontrolledentities fortheperiodended31December2014.Togetherthesedocumentscontainalltheinformationrequiredby Appendix4EoftheAustralianSecuritiesExchangeListingRules.ItshouldbereadinconjunctionwithiCarAsia Limited’sAnnualReportwhenreleasedandislodgedwiththeAustralianSecuritiesExchangeunderlistingrule 4.3A. ForandonbehalfoftheBoard For personal use only PatrickGrove Chairman 25thFebruary2015 iiCar Asia Limited and Controlled Entities ACN 157 710 846 Annual Report for the financial year ending 31 December 2014 For personal use only Annual Report Year Ending 31 December 2014 ICAR ASIA LIMITED (ICQ) / ACN 157 710 846 Directors’ Report 1 Auditor’s Independence Declaration 19 Statement of Comprehensive Income 20 Statement of Financial Position 21 Statement of Changes in Equity 22 Statement of Cash Flows 23 Notes to Financial Statements 24 Directors’ Declaration 60 InDependent AuDit Report 61 Corporate Governance 63 -

Northern New South Wales Gas Company to List On

ACN 165 522 887 ASX CODE: IBY ASX ANNOUNCEMENT 13 August 2014 IBUY GROUP COO, KRIS MARSZALEK PROMOTED TO CEO August 13, 2014 – Leading Asian e-Commerce company, iBuy Group Ltd (ASX: IBY), today announced that Krzysztof Marszalek (“Kris”), has been promoted from the Company’s Chief Operating Officer to Chief Executive Officer. Kris will replace outgoing CEO, Patrick Linden, who will leave the company to pursue new opportunities. “As the business expands in complexity and enters a new phase of growth, Kris’s tremendous experience, entrepreneurial energy, passion and drive, make him the perfect candidate to lead iBuy through a period of transformation and consolidation. His contribution whilst COO of the Company made it abundantly clear to the Board that he is the best person to head up the business. We thank Patrick Linden for his excellent service and work in bringing the companies together. We look forward to the next phase of the business under Kris’s guidance and are excited he has chosen to take leadership of the company as it moves to the next level,” said Patrick Grove, Chairman of iBuy Group. Kris said, “The iBuy businesses have extraordinary potential and I am more than excited to be charged with driving the business now and in the future. Our markets offer a once in a lifetime possibility to create an incredible e-Commerce business and I am ready to lead this team to execute on all the opportunities ahead of us. " Prior to co-founding iBuy Group in 2013, Kris has had an outstanding record of achievement as an entrepreneur. -

Programs for Event "2020 WD SEA Highlights" Main Stage Venue

Programs for Event "2020 WD SEA Highlights" Main Stage Venue: Online Tuesday, 3rd November 2020 09:15 - 09:55 10 YEARS LATER: SERIAL FOUNDER VS SERIAL INVESTOR Patrick Grove Co-Founder & Group CEO, Catcha Group Khailee Ng Managing Partner, 500 Startups 09:55 - 10:10 THE NEXT SUPER APP IN SOUTHEAST ASIA Karen Chan CEO, airasia.com 10:10 - 10:35 WOMEN LEADING CHANGE: IMPACT & EMPOWERMENT Beverly Chen Marketing Director, APAC, AppsFlyer Karen Chan CEO, airasia.com Surina Shukri CEO, MDEC Ee Ling Lim (Moderator) Head of Innovation & Partnerships, SEA, 500 Startups 10:40 - 10:55 FOUNDER'S PLAYGROUND: AI, A VOICE BEYOND MACHINES Vu Van Founder & CEO, ELSA 10:55 - 11:10 AUTOMATION, AI BEYOND HUMAN SCALE Main Stage Venue: Online Tuesday, 3rd November 2020 Malina Platon Managing Director, Strategic Accounts, APAC, UiPath FROM THE PHILIPPINES TO THE WORLD: STARTUPS & INVESTORS' GROWTH 11:10 - 11:30 PERSPECTIVES Minette B. Navarrete Co-Founder & President, Kickstart Ventures J.P. Ellis Co-Founder & Chief Executive, C88 Financial Technologies Rexy Dorado (Moderator) Co-Founder & President, Kumu TOP FUNDRAISING TECHNIQUES - HOW TO WIN THE HEARTS & MINDS OF 11:30 - 11:45 INVESTORS Bill Reichert Partner, Pegasus Tech Ventures 11:45 - 12:00 SOUTHEAST ASIA – WHAT IS BEYOND 2020? Dave Ng General Partner, Altara Ventures 12:05 - 12:30 ECOMMERCE IN SEA RIDES HIGH ON PANDEMIC BOOM Giulio Xiloyannis Chief Commercial Officer, ZALORA Casey Liang Co-Founder, Pomelo Fashion Main Stage Venue: Online Tuesday, 3rd November 2020 Joel Leong Co-Founder, ShopBack Ganesh -

Press Release

PRESS RELEASE 18/03/2013 Opt Inc Catcha Digital Asia PTE Opt acquires Catcha Digital Asia Former Apple APAC Head of Online Marketing, Mitsuru Kikunaga to take on CEO role Opt Inc. (“Opt”), Japan’s leading e-marketing company and one of the largest in Asia, today announced that it has acquired Catcha Digital Asia Pte Ltd (CDA), one of Southeast Asia’s leading digital media networks, from Catcha Group Pte Ltd (“Catcha Group”). Former Apple Asia-Pacific Head of Online Marketing, Mitsuru Kikunaga, currently Opt’s Asia-Pacific Business General Manager, will step into the role of CDA CEO. Opt, which has operations in Japan, Korea and China and a head count of 1261 employees, is listed on the Japan Securities Exchange (JASDAQ) and generates revenue of ¥78.9 billion (US$825 million) annually. Its decision to acquire 90 percent of CDA is designed to strengthen its position across Asia and enable CDA to become the one-stop digital solution to meet the requirements of its clients in the ASEAN region, including those of Japanese companies that want to advance into ASEAN’s rapid growth markets. Appointed as CDA’s incoming CEO, Mitsuru Kikunaga, has extensive business experience in the APAC region and is well placed to take advantage of the business opportunities available in this emerging market. Commenting on the move, Kikunaga said, “Opt has determined ASEAN as an important market for Opt’s overseas expansion and will aggressively invest the resources of the company in the region. We are targeting to generate ¥10 billion (US$105 million) in revenue through our overseas businesses by 2020.” As part of this strategy, Opt will be dispatching specialists in performance-based advertising such as Search Engine Marketing (“SEM”) and Display Advertising to South-East Asia; both are fields in which Opt is a Japan market-leader. -

Annual Report & Appendix 4E

iCar Asia Limited ACN 157 710 846 Appendix 4E RESULTS FOR ANNOUNCEMENT TO THE MARKET For the year ended 31 December 2015 Dec-15 Dec-14 12 months ended $000 $000 Change Revenues from ordinary operations 6,278 2,814 123% Loss from ordinary activities after tax attributable to members (12,537) (16,700) 25% Loss after tax attributable to members (12,537) (16,700) 25% Cents Cents Loss per Share (basic & diluted) (5.43) (8.64) 37% NTA per Share 7.09 5.34 33% Dividends No dividends have been paid or declared in 2015 (2014: nil). There is no dividend reinvestment plan in operation. Basis of this report This report includes the attached audited financial statements of iCar Asia Limited and its controlled entities for the period ended 31 December 2015. Together these documents contain all the information required by Appendix 4E of the Australian Securities Exchange Listing Rules. It should be read in conjunction with iCar Asia Limited’s Annual Report when released and is lodged with the Australian Securities Exchange under listing rule 4.3A. For and on behalf of the Board Patrick Grove Chairman 24th February 2016 iiCar Asia Limited and Controlled Entities ACN 157 710 846 Annual Report for the financial year ended 31 December 2015 Annual Report Year Ended 31 December 2015 ICAR ASIA LIMITED (ICQ) / ACN 157 710 846 Directors’ Report 1 Auditor’s Independence Declaration 21 Statement of Comprehensive Income 22 Statement of Financial Position 23 Statement of Changes in Equity 24 Statement of Cash Flows 25 Notes to the Financial Statements 26 Directors’ Declaration 67 Independent Audit Report 68 Shareholder Information 70 Corporate Directory 72 iCar Asia Limited and Controlled Entities Directors’ report 31 December 2015 The directors present their report, together with the consolidated financial statements, of iCar Asia Limited and Controlled Entities (referred to hereafter as the 'Group') for the year ended 31 December 2015. -

A Branding Revolutionist

1I SUCCESSFUL BRANDING LESSONS: Jack Ma, Richard Branson & Usain Bolt YUSUF TAIYOOB : The King Of Dates MYDIN : Heartland Retail Empire SAY YES2BRAND : Aspiring for a Better Tomorrow, Today TAN SRI DATO’ SRI LEONG HOY KUM RM15 WM RM18 EM A BRANDING REVOLUTIONIST DECEMBERMAY-JANUARY’ - JUNE’ 1714 #ISSUE4119 II 1 All information herein is correct at time of publication. THE TEAM | The views and opinions expressed or implied in The BrandLaureate Business World Review ADVISOR are those of the authors and contributors and do not necessarily Dr KKJohan reflect those of The BrandLaureate, its editorial & staff. All editorial content and materials are copyright of PUBLISHER/EDITOR-IN-CHIEF THE BRANDLAUREATE BUSINESS WORLD REVIEW Chew Bee Peng No Permit KDN PQ/PP16972/08/2011)(028331) MANAGING EDITOR The BrandLaureate Business World Review is published by Ida Ibrahim THE BRANDLAUREATE SDN BHD (690453K), 39B & 41B, SS21/60, Damansara Utama, 47400 Petaling Jaya. Tel: (603) 7710 0348 Fax: (603) 7710 0350 SENIOR WRITER Ian Gregory Edward Masselamani Printed in Malaysia by PERCETAKAN SKYLINE SDN BHD (PQ 1780/2317) WRITERS 35 & 37, Jalan 12/32B, TSI Business Industrial Park, Batu 6 1/2, Nurilya Anis Rahim Off Jalan Kepong, 52000 Kuala Lumpur, Malaysia. Ain M.C. Gerald Chuah CONTRIBUTORS Anu Venugopal, Tony Thompson, Justin Chew, Sean Tan CREATIVE MANAGER Ibtisam Basri ASSISTANT CREATIVE MANAGER Mohd Shahril Hassan SENIOR GRAPHIC DESIGNER Mohd Zaidi Yusof MULTIMEDIA DESIGNER Zulhelmi Yarabi EDITORIAL ASSISTANTS Kalwant Kaur Lau Swee Ching For suggestions and comments or further enquiries on THE BRANDLAUREATE BUSINESS WORLD REVIEW, please contact [email protected]. “Position Your Brand on a World Class Platform” THE BRANDLAUREATE • BUSINESS WORLD REVIEW MAY - JUNE’ 17 #ISSUE41 2 3 PUBLISHER NOTE | What’s in a name, you may ask? Minister of Canada show that age does not really W Everything if I may say! matter. -

Forbes Asia August 2017.Pdf

200 ‘BEST UNDER A BILLION’: JAPAN JUMPS AUGUST 2017 • WWW.FORBES.COM PLUS 50SINGAPORE’S RICHEST 5-STAR STIR SONIA CHENG IMPORTS ROSEWOOD HOTEL BRAND UNDER WING OF HER HONG KONG CLAN AUSTRALIA...............A $12.00 INDIA............................RS 375 KOREA........................W 9,500 PAKISTAN....................RS 600 TAIWAN......................NT $275 CHINA....................RMB 85.00 INDONESIA............RP 77,000 MALAYSIA...............RM 24.00 PHILIPPINES..................P 260 THAILAND......................B 260 HONG KONG................HK $80 JAPAN.................¥1238 + TAX NEW ZEALAND.......NZ $13.00 SINGAPORE..............S $12.50 UNITED STATES........US $10.00 CONTENTS — AUGUST 2017 VOLUME 13 NUMBER 7 S PAGE 20 10 | FACT & COMMENT // STEVE FORBES “I WAS SHOCKED, Crackdown on North Korea unavoidable now. EVERYBODY WAS SHOCKED.” SINGAPORE’S 50 RICHEST — Sushi King founder 42 | MAYO FOR THE MAINLAND FUMIHIKO KONISHI Loo Choon Yong is taking his Raffles hospital brand to China. on Malaysia’s large appetite BY JANE A. PETERSON for sushi 46 | WHEN THE ‘LOVE’ GOES Choo Chong Ngen woos a different customer to his new inn brands. BY JESSICA TAN 50 | THE LIST Fortunes rise amid a bitter battle in Singapore’s first family. BY NAAZNEEN KARMALI BEST UNDER A BILLION 26 | MAKE IT FLOW Zhang Chunlin gave up a prized state job to hustle for China’s burgeoning water industry. BY JANE HO 29 | LESSONS LEARNED Asset-heavy Indian schooling firms sink after good early marks. BY ANURADHA RAGHUNATHAN 30 | EYEING NEW MARKETS Why China’s largest ophthalmological chain is focusing on the U.S. BY ELLEN SHENG 32 | THE LIST Sales of our top 200 publicly traded Asia-Pacific companies grew an average 55% last year. -

Catcha Group Or That SEA Would Have More Internet Here’S a Midway Checkpoint of Those Users Than the US? Predictions

December 2018 8 Predictions for the Southeast Asian Tech Scene – A Checkpoint Plus 3 New Predictions for Indonesia 2 FOREWORD Hey folks! brand-new ones just for Indonesia! Even I never expected that SEA’s tech If you know me, you know how much of entrepreneurs would be killing it at this Let’s see how many we get right. And a Southeast Asia (SEA) believer I am! level! more importantly, let’s see if SEA can surpass even Catcha’s wildest I’m always impressed, inspired and But my team and I like a challenge. So expectations in the next 24 months! invigorated by the talent, opportunities, we thought we’d try to predict the BOOM! and growth coming out of this region. future. That’s why, since 2017, we’ve That’s why I’ve focused my entire released our predictions for where the journey as an entrepreneur out of here. SEA tech landscape would go. Would you have guessed that a local Earlier this year, we announced 8 startup would acquire its competitor, predictions which we felt would reshape the largest provider and pioneer of e- the market till 2020. And today, just in Patrick Grove hailing services? time for Wild Digital Indonesia 2018 (our Co-Founder & Group CEO rockin’ premier tech conference), Catcha Group Or that SEA would have more Internet here’s a midway checkpoint of those users than the US? predictions. Bonus: we’ve added 3 If you have any questions on the report, please reach out via [email protected]. Opinions expressed are solely perspective of Catcha Group. -

The Committee Secretariat Advises That the Centre

The Committee Secretariat advises that the Centre for Independent Studies’ submission, as originally published on this website, was updated on 29 September 2016 at the request of the submitter. The new version adds several endnotes missing from the original version. No other changes have been made. The Centre for Independent Studies Level 1, 131 Macquarie St Sydney NSW 2000 Phone: +61 2 9438 4377 Website: www.cis.org.au 23 September 2016 Senate Standing Committees on Economics Parliament House Canberra ACT 2600 Dear Senators Treasury Laws Amendment (Enterprise Tax Plan) Bill 2016 I am pleased to attach a submission on this important Bill. The submission provides a detailed case for a reduction in the company tax rate as contained in the Bill. The submission details the uncompetitive nature of Australia’s company tax system, the benefits of the tax cut, and responses to some of the arguments presented against the policy. The Centre for Independent Studies (CIS) is Australia’s leading independent public policy research institute. The Centre seeks to provide independent, fact based practical research and encourage/provoke debate that promotes liberty, the rule of law, free enterprise and an efficient democratic government. Since 1976, the CIS has produced valuable research that has shaped and influenced public policy. We seek to engage with the general public, business, media, academics, policymakers and politicians across the political spectrum. I would welcome any opportunity to discuss this submission with the Committee. I may be contacted on [email protected] or on the office number 02 9438 4377. Yours sincerely Michael Potter Research Fellow Fix it or Fail: Why we must cut company tax now Related publications RR15: Michael Potter, The case against tax increases in Australia: the growing burden, 2016 PM87: Sinclair Davidson, The Faulty Arguments Behind Australia’s Corporate Tax, 2008 Table of Contents Fix it or Fail: Why we must cut company tax now ......................................................................... -

Asian Founders at Work

ASIAN FOUNDERS AT WORK STORIES FROM THE REGION’S TOP TECHNOPRENEURS Ezra Ferraz Gracy Fernandez Asian Founders at Work: Stories from the Region’s Top Technopreneurs Ezra Ferraz Gracy Fernandez Makati City, Philippines Makati City, Philippines ISBN-13 (pbk): 978-1-4842-5161-4 ISBN-13 (electronic): 978-1-4842-5162-1 https://doi.org/10.1007/978-1-4842-5162-1 Copyright © 2020 by Ezra Ferraz, Gracy Fernandez This work is subject to copyright. All rights are reserved by the Publisher, whether the whole or part of the material is concerned, specifically the rights of translation, reprinting, reuse of illustrations, recitation, broadcasting, reproduction on microfilms or in any other physical way, and transmission or information storage and retrieval, electronic adaptation, computer software, or by similar or dissimilar methodology now known or hereafter developed. Trademarked names, logos, and images may appear in this book. Rather than use a trademark symbol with every occurrence of a trademarked name, logo, or image we use the names, logos, and images only in an editorial fashion and to the benefit of the trademark owner, with no intention of infringement of the trademark. The use in this publication of trade names, trademarks, service marks, and similar terms, even if they are not identified as such, is not to be taken as an expression of opinion as to whether or not they are subject to proprietary rights. While the advice and information in this book are believed to be true and accurate at the date of publication, neither the authors nor the editors nor the publisher can accept any legal responsibility for any errors or omissions that may be made. -

Squeezed Margins AVCJ Research Gps, Lawyers Take the Strain As Asia Fundraising Costs Get Ever Higher Page 7 Data F Ile Page 15

Asia’s Private Equity News Source avcj.com July 23 2013 Volume 26 Number 28 EDITOR’s VieWPOINT Where has it gone wrong for venture capital in Southeast Asia? Page 3 NEWS ADB, Altamont Capital, ASK, Baring, BlackStone, FIrst Reserve, Globis, IL&FS, J-Star, KDDI, Leopard Capital, MBK Page 5 DEAL OF THE WEEK Jungle Ventures sees TravelMob investment reach its destination Page 13 FOCUS How Asia’s coffee shop boom could be the right blend for Pe investors Page 14 Squeezed margins AVCJ RESEARCH GPs, lawyers take the strain as Asia fundraising costs get ever higher Page 7 Data f ile Page 15 FOCUS DEAL OF THE WEEK Liquidity channels Bettin’ on beautiful India SMEs get new fundraising, exit route Page 12 L Capital makes first China cosmetics play Page 13 black and white 1,000 shades answers of grey THE SWEET SPOT One financial advisory and investment banking services firm excels at navigating complex financial issues: Duff & Phelps. Our people have the analytical skills to get to the heart of issues and the experience to know which variables matter more. We find the right balance between analysis and instinct—that sweet spot that powers sound decisions. Learn more at www.duffandphelps.com Beijing: Sammy Lai, [email protected] Shanghai: Bill Snyder, [email protected] Hong Kong: Andy Wong, [email protected] Investment banking services in the United States are provided by Duff & Phelps Securities, LLC; Pagemill Partners; and GCP Securities, LLC. Member FINRA/SIPC. M&A advisory services in the United Kingdom and Germany are provided by Duff & Phelps Securities Ltd.