Final Port Planning and Investment Toolkit

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Boston Tea Party Grade 4

Sample Item Set The Boston Tea Party Grade 4 Standard 7 – Government and Political Systems Students explain the structure and purposes of government and the foundations of the United States’ democratic system using primary and secondary sources. 4.7.2 Explain the significance of key ideas contained in the Declaration of Independence, the United States Constitution, and the Bill of Rights SOCIAL STUDIES SAMPLE ITEM SET GRADE 4 1 Sample Item Set The Boston Tea Party Grade 4 Use the three sources and your knowledge of social studies to answer questions 1–3. Source 1 Boston Tea Party Engraving This engraving from 1789 shows the events of December 16, 1773. Dressed as American Indians, colonists dumped nearly 90,000 pounds of British East India Company tea into Boston Harbor in protest against the Tea Act. SOCIAL STUDIES SAMPLE ITEM SET GRADE 4 2 Sample Item Set The Boston Tea Party Grade 4 Source 2 Writing of the Declaration of Independence This picture shows Benjamin Franklin, John Adams, and Thomas Jefferson writing the Declaration of Independence in 1776. Thomas Jefferson wrote the Declaration of Independence with help from other members of the Continental Congress. SOCIAL STUDIES SAMPLE ITEM SET GRADE 4 3 Sample Item Set The Boston Tea Party Grade 4 Source 3 Timeline of Events Leading to American Revolution Year Event 1764 Britian passes the Sugar Act on Colonists. 1765 Britian passes the Stamp Act on Colonists. 1767 Britian passes Townshend Acts on Colonists. 1770 Boston Massacre occurs when the British Army kills five Colonists. 1773 Colonists protest at the Boston Tea Party. -

Identification of Massachusetts Freight Issues and Priorities

Identification of Massachusetts Freight Issues and Priorities Prepared for the Massachusetts Freight Advisory Council By Massachusetts Highway Department Argeo Paul Cellucci Jane Swift Kevin J. Sullivan Matthew J. Amorello Governor Lieutenant Governor Secretary Commissioner And Louis Berger and Associates Identification of Massachusetts Freight Issues and Priorities Massachusetts Freight Advisory Council Chairman Robert Williams Project Manager and Report Author Mark Berger, AICP Project Support (Consultant) Adel Foz Wendy Fearing Chris Orphanides Rajesh Salem The preparation of this document was supported and funded by the Massachusetts Highway Department and Federal Highway Administration through Agreement SPR 97379. November 1999 Identification of Massachusetts Freight Issues and Priorities Table of Contents CHAPTER 1: INTRODUCTION...................................................................................................................1-1 Purpose...........................................................................................................................................................1-1 Massachusetts Freight Advisory Council.........................................................................................................1-1 Contents of Report..........................................................................................................................................1-1 CHAPTER 2: SOLICITATION OF FREIGHT ISSUES..................................................................................2-1 -

Director of Airline Route Development

About Massport The Massachusetts Port Authority (Massport) is an independent public authority in the Commonwealth of Massachusetts that is governed by a seven member Board. Massport is financially self-sustaining and contributes to the regional economy through the operation of three airports—Boston Logan International Airport, Hanscom Field and Worcester Regional Airport; the Port of Boston’s cargo and cruise facilities; and property management/real estate development in Boston. Massport’s mission is to connect Massachusetts and New England to the world, safely, securely and efficiently, never forgetting our commitment to our neighbors who live and work around our ports and facilities. Massport is an integral component of a national and worldwide transportation network, operating New England’s most important air and sea transportation facilities that connect passengers and cargo with hundreds of markets around the globe. Massport continually works to modernize its infrastructure to enhance customer service, improve operations and optimize land use, and has invested more than $4 billion over the past decade in coordination with its transportation partners. Massport also strives to be a good neighbor closer to home. Working in concert with government, community and civic leaders throughout Massachusetts and New England, Massport is an active participant in efforts that improve the quality of life for residents living near Massport’s facilities and who make sacrifices every day so that Massport can deliver important transportation services to families and businesses throughout New England. Boston Logan International Airport Boston Logan International Airport (BOS) is New England’s largest transportation center and an economic engine that generates $13.3 billion in economic activity each year. -

The South Boston Haul Road – RAIL CORRIDOR

Intermodal Corridor To the Port of Boston: The South Boston Haul Road – RAIL CORRIDOR Frank S. DeMasi RTAC Freight Committee November 2009 History of the South Boston Haul Road In the 1850s, the South Boston Haul Road (SBHR) route began to be used for railroad access to Boston from south of the growing city. Before 1900, it was made a two-track, depressed route with 12 overhead bridges. Extensive freight yards and maintenance facilities were constructed near the South Boston waterfront. The present MBTA Red Line subway tunnel, constructed in 1913 along Dorchester Avenue, crosses the cut on a diagonal under a bridge. The top of the tunnel is about 0.6 m (2 feet) below the railroad track on a three-level multimodal structure: passenger subway below freight railroad below highway. The depressed railroad route was widened from two tracks to four by 1920. After the 1940s, passenger service was discontinued and freight service levels declined. The result was that two tracks in the depressed track area and seven yard tracks remained in various levels of deferred maintenance. The other two tracks remained in service for the (usually) daily local freight until the mid-1980s. The route was suggested as a possible multimodal shared-access corridor early in the Central Artery/Tunnel (CA/T) project; community reaction was favorable, and a study of feasibility was authorized in 1987. Rail Facilities Port of Boston Circa 1950 The South Boston Haul Road – RAIL CORRIDOR Property Acquisition During the onset of construction of the Central Artery Tunnel Project, much railroad right-of-way was owned by Conrail, portions owned by Amtrak and Massachusetts Bay Transportation Authority (MBTA). -

Shaped by Function: Boston's Historic Warehouses

124 Sara E. Wermiel Shaped by Function: Boston’s Historic Warehouses This paper discusses the history of warehouses built before had the leading port. Boston’s port remained one of the busi- 1920 in Boston, Massachusetts, U.S.A., with a focus on est through the nineteenth century, and in the latter nine- those in the Fort Point Channel Landmark District (FPCLD). teenth century, port facilities – including piers, warehouses, The FPCLD is a roughly 55-acre (22.3 hectares) area in the and railroad service – expanded in the South Boston area. South Boston neighborhood of the city, and it contains 85 In the twentieth century, other North American ports grew Figure 1: Warehouses in Fort Point Channel District, photo 1925 historic warehouses and lofts, which were built between to outrank Boston. Today, most of the wharves and facilities 1880 and 1930. This is the largest collection of warehouses of the old harbor have disappeared. In South Boston, the in a definable area in the city, and it probably is also one warehouses and lofts of the FPCLD survive. Although they of the most intact warehouse districts in the United States. now serve purposes other than storage and manufacturing, Before discussing the history of the FPCLD, the paper pres- these warehouses and lofts continue to physically represent ents an overview of the development of Boston’s old har- a time when maritime commerce and industry dominated bor and the distinctive warehouse blocks that were once a the city’s economy. These building feature a special form prominent feature of it. Until the mid-eighteenth century, of heavy-timber interior framing, adapted from a regional Boston was the most populous North American town and construction tradition. -

The Boston Economy - 2003

589 The Boston Economy - 2003 THOMAS M. MENINO, MAYOR CITY OF BOSTON Boston Redevelopment Authority Mark Maloney, Director Clarence J. Jones, Chairman Consuelo Gonzales Thornell, Treasurer Joseph W. Nigro, Jr., Co-Vice Chairman Michael Taylor, Co-Vice Chairman Christopher J. Supple, Member Harry R. Collings, Secretary Report prepared by Dominic Modicamore Jim Vrabel Luis Rosero Policy Development and Research Gregory Perkins, Interim Director Report #589 October 2003 TABLE OF CONTENTS Boston’s Economy – 2003 ...............................................................................................................1 General...........................................................................................................................................1 Overview of Current Economic Conditions……………………………………………………….1 Statistical Data……………………………………………………………………………………..2 New England, Massachusetts, and Metropolitan Boston Economies .............................................................................................2 Employment Structure, Employment Trends, and Occupational Changes.............................................................................................................3 Unemployment...............................................................................................................................6 Largest Employers .........................................................................................................................7 Labor Force and Education............................................................................................................8 -

Christopher M. Gordon

CHRISTOPHER M. GORDON Chris Gordon is a Lecturer at the Massachusetts Institute of Technology Center for Real Estate and a Senior Lecturer at the Harvard Business School teaching and writing primarily on the subject of complex capital projects. Until 2010 he served as the Chief Operating Officer of the Allston Development Group at Harvard University. In that role he oversaw the development of Harvard’s proposed campus expansion in the Allston section of Boston as well as development projects on the historic Cambridge campus. Before stepping into the role of Chief Operating Officer (COO) for the Allston Development Group in late 2005, Chris was director of Capital Programs and Logan Modernization for the Massachusetts Port Authority. During his decade at Massport, he was responsible for capital programming and project delivery for all capital projects at all Massport facilities, including Logan International Airport (the 13th busiest airport in the world), Hanscom Airfield, Tobin Memorial Bridge, Maritime Terminals on the Port of Boston, and the Worcester Regional Airport. He oversaw the successful completion of the $4.4 billion Logan Modernization Project and as Director of Capital Programs, oversaw a $500 million annual budget. Chris is a former board member of the National Research Council’s Board on Infrastructure and the Built Environment, a former trustee of the Engineering Center Education Trust, a former corresponding editor of the American Society of Civil Engineers Engineering Management Journal, and has been a speaker at numerous conferences. Chris was named the 2001 Person of the Year for the Construction Management Association of America for both the New England region and the country, and was named the 2000 Government Engineer of the Year by the Boston Society of Civil Engineers. -

Environmental Issues and Solutions in the Boston Metropolitan Area

Environmental Issues and Solutions in the Boston Metropolitan Area Sponsor: Boston Project Center Director Professor Susan Vernon-Gerstenfeld Submitted to: Project Liaison: Professor Susan Vernon-Gerstenfeld Project Advisors: Susan Vernon-Gerstenfeld, WPI Professor Alexander Wyglinski, WPI Professor Submitted by: Gabriel Louzao Thales Oliveira Oliver Rich Date: October 12, 2010 i ABSTRACT The goal of this project was to help the Boston Project Center refocus its future projects to address environmental problems in the City of Boston. To do this, our objectives were to identify the major environmental problems in Boston, which organizations are addressing these problems, and where they will focus their resources in the future. We concluded that funding is being directed towards addressing climate change and implementing clean energy solutions. Provided in this report is a list of individuals and organizations that could be approached as future project sponsors and a GIS map presenting the locations and general information of these organizations. ii ACKNOWLEDGEMENTS We would like to thank Mr. Douglas Fine from the Massachusetts Department of Environmental Protection, Mr. Derek Lennon from the Department of Conservation and Recreation, Mrs. Vivien Li from The Boston Harbor Association, Mrs. Kate Plourd from the Massachusetts Clean Energy Center, Mr. Paul Stordy from Massport, and Mr. Vincent DeVito for taking the time to answer our question so that we could better understand Boston‟s environmental situation. Also we would like to thank our project sponsor Professor Susan Vernon-Gerstenfeld and our advisor Professor Alexander Wyglinski for their continuous help. iii EXECUTIVE SUMMARY The greater Boston region must address the issues of pollution and climate change in the upcoming years if it is to continue sustainable growth. -

Conley Terminal Modernization Program Soil Reclamation and Reuse Initiatives

American Association of Port Authorities (AAPA) 2020 Environmental Improvement Awards Conley Terminal Modernization Program Soil Reclamation and Reuse Initiatives June 30, 2020 Conley Terminal Modernization Program - Soil Reclamation and Reuse Initiatives Executive Summary Conley Container Terminal is an important economic asset for the New England region, serving more than 2,500 businesses, including nearly 700 enterprises based in rural areas. Increasing demand has led to four consecutive container volume records at Conley Terminal, including 300,762 TEUs in CY2019, a 1 percent jump from CY2018 and the fifth consecutive year of record-breaking volume. Altogether, the working port is now home to more than 9,000 blue-collar jobs and responsible for $8.2 billion in annual economic impact. To maintain its competitiveness, in 2014, the Massachusetts Port Authority (Massport) commenced the Conley Terminal Modernization Program, an $800 MM investment into the infrastructure of the Port of Boston. This Program included partnering with the US Army Corps of Engineers (USACE) on the dredging and deepening of the Boston Harbor, rehabilitation of two existing berths at Conley Terminal (Berths 11 and 12), construction of a new deep-water berth (Berth 10) and expansion of Conley Terminal yard onto an adjacent property, the location of a former oil storage facility. Rather than manage these projects piece- meal, Massport recognized the opportunity to develop and execute a comprehensive and cost-effective Soil Management Program to test, manage, treat, process, and reuse soils onsite for all construction projects at Conley. This successful Soil Management Program allowed Conley Terminal to: Maximize soil reuse onsite. Minimize the amount of imported fill as part of construction. -

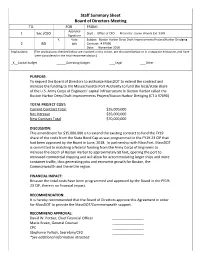

Staff Summary Sheet for Boston Harbor Deep Draft Improvements Projects

Staff Summary Sheet Board of Directors Meeting TO FOR FROM: Approval 1 Sec./CEO Dept.: Office of CFO Presenter: Susan Woods Ext: 9145 Signature X Vote Subject: Boston Harbor Deep Draft Improvements Project/Harbor Dredging 2 BD Info Contract: # 97690 Date: November 2018 Implications: (The implications checked below are involved in this action, are discussed below or in a separate enclosure, and have been considered in the final recommendation.) _X__Capital Budget ___Operating Budget ___Legal ___Other PURPOSE: To request the Board of Directors to authorize MassDOT to extend the contract and increase the funding to the Massachusetts Port Authority to fund the local/state share of the U.S. Army Corps of Engineers’ capital infrastructure in Boston Harbor called the Boston Harbor Deep Draft Improvements Project/Boston Harbor Dredging (CT # 97690) TOTAL PROJECT COST: Current Contract Total: $35,000,000 Net Increase $35,000,000 New Contract Total $70,000,000 DISCUSSION: This amendment for $35,000,000 is to extend the existing contract to fund the FY19 share of the costs from the State Bond Cap as was programmed in the FY19-23 CIP that had been approved by the Board in June, 2018. In partnership with MassPort, MassDOT is committed to matching a federal funding from the Army Corps of Engineers to increase the depth of Boston Harbor to approximately 50 feet, opening the port to increased commercial shipping and will allow for accommodating larger ships and more container traffic, thus generating jobs and economic growth for Boston, the Commonwealth and the entire region. FINANCIAL IMPACT: Because the total costs have been programmed and approved by the Board in the FY19- 23 CIP, there is no financial impact. -

Ocm40693443-1960.Pdf

i Q k O C‘ IVTRODUCTIOIV In order to present a frame of reference in which to Under this trusteeship, the Massachusetts Port Authori place the Massachusetts Port Authority and its efforts to ty on February 17, 1959, sold a revenue bond issue of aid the commerce of the Commonwealth, we offer the $71,750,000 bearing interest at 4%%, and took over following background information: operation of the Port of Boston facilities, Logan Inter national Airport, Hanscom Field, and the Mystic River The taxpayers of the State provided approximately Bridge. $30 million after World War II for improved ship-truck- The Authority is moving toward objectives. It was railroad facilities on the Boston waterfront. Over a longer authorized and empowered in its enabling act “to in period, the taxpayers invested approximately $70 million vestigate the necessity for the development and improve in airplane-automobile-truck facilities at Logan Inter ment of commerce in the city and the metropolitan area national Airport. surrounding the city and for the more expeditious han Despite these huge investments and the efforts of State dling of such commerce, including but not limited to, managerial agencies, sizeable annual deficits had to be additional traffic facilities, bus and truck terminals, off- met from tax revenues. In accordance with the “equal and street parking facilities, and passengers at steamship, proportional” tax provision of the State Constitution, the railroad or motor terminals or airports, and to make such users and the non-users of the facilities were treated alike. studies, surveys and estimates as may be necessary to To relieve non-users of additional tax burdens, the determine the feasibility of any such facility . -

Port of Boston Update

Port of Boston Update Andrew G. Hargens, AICP | LEED AP, Senior Project Manager Massachusetts Port Authority Economic Planning and Development Department Regional Transportation Advisory Council Advisory Transportation Regional Massachusetts Port Authority • State authority created in 1956 • Board appointed by Governor • Self-financing • Primary line departments and facilities – Aviation Department • Logan International Airport • Hanscom Field • Worcester Airport – Maritime Department • Port of Boston terminals • Commercial development Regional Transportation Advisory Council Advisory Transportation Regional Massachusetts Port Authority Economic Planning and Development Department Port of Everett Boston Chelsea Geography and East Ownership Charlestown Boston North End Massport Financial Property District Regional Transportation Advisory Council Advisory Transportation Regional Massachusetts Port Authority Economic PlanningSouth and DevelopmentBoston Department Port of Everett Boston Chelsea Geography and East Ownership Charlestown Boston North End Massport Financial Property District Other Public (USCG & BRA) Regional Transportation Advisory Council Advisory Transportation Regional Massachusetts Port Authority Economic PlanningSouth and DevelopmentBoston Department Port of Everett Boston Chelsea Geography and East Ownership Charlestown Boston North End Massport Financial Property District Other Public (USCG & BRA) Private Port Regional Transportation Advisory Council Advisory Transportation Regional Facilities Massachusetts Port Authority